September Exports Recover from Previous Two Months Amid Improved Global COVID-19 Situation, but Inflation Remains a Concern

September exports have rebounded from the previous two months as the global COVID-19 situation improves, but rising inflation driven by increasing energy prices remains a pressing concern moving forward.

• The value of exports in September expanded by 17.1% YOY, continuing to grow across all major products and markets except for Australia, which saw a slight contraction due to gold. When compared to the previous month on a seasonally adjusted basis, exports grew by 4.2% MoM_sa, reflecting a clear improvement in the global COVID-19 situation during September, leading to a recovery in demand. Additionally, the impact of production halts due to the COVID-19 outbreak has also improved.

• Although exports have recovered from the improved COVID-19 situation, they will still face new pressures for the remainder of the year due to rising energy prices, which could accelerate global inflation rates. This may lead to a short-term slowdown in consumer purchasing power, particularly in countries that rely on energy imports. It is expected that the situation will gradually improve in the future. Furthermore, attention must be paid to China's economy, which faces risks from the energy crisis and the real estate sector due to the Evergrande case, which could impact Thailand's exports to China for the rest of the year.

• The EIC continues to forecast Thailand's exports for 2021 at 15% YOY as the latest export data aligns with previous forecasts that anticipated a recovery in exports for the remainder of the year following the severe Delta variant outbreak in July and August, although levels will not be as high as in the second quarter. For 2022, Thai exports are expected to continue growing at 4.7% in line with the global economy's slower growth rate. Exports to developing countries are expected to perform well next year due to the acceleration of economic recovery from increased vaccination progress.

Key points

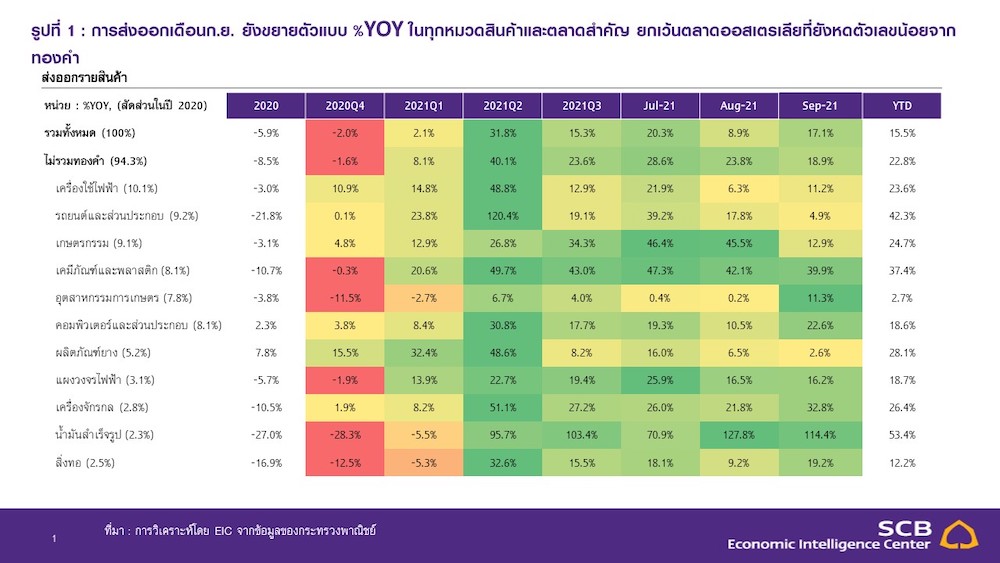

The value of exports in September 2021 grew by 17.1% YOY, accelerating from the previous month's 8.9% YOY. Excluding gold, exports would have expanded by 18.9% YOY, resulting in a 15.5% YOY growth in export value for the first three quarters of 2021.

In terms of exports by product, growth continued in % YOY across the board.

• Refined oil grew by 114.4% YOY, continuing to expand for seven months due to high energy demand and oil prices, with growth in all major markets such as Cambodia (87.73% YOY), Malaysia (284.7% YOY), Singapore (186.5% YOY), and the Philippines (913.3% YOY).

• Computers and components grew by 22.6% YOY, continuing for ten consecutive months, with significant growth in the U.S. (18.5% YOY), Hong Kong (33.2% YOY), China (27.7% YOY), and Malaysia (132.9% YOY), while the Netherlands (-16%) was a significant drag.

• Chemical exports grew by 55.8% YOY, continuing for the tenth month, with growth in all major markets such as China (75.9% YOY), Japan (48% YOY), and India (115.7% YOY), except for Vietnam, which contracted (-30.1% YOY).

• Plastic pellets grew by 40.3% YOY, continuing for the tenth month, with growth in all major markets such as China (14.1% YOY), India (75.3% YOY), and Indonesia (81.1% YOY).

• Rubber grew by 83.6% YOY, continuing for twelve months, with growth in all major markets such as China (125.6% YOY), the U.S. (249% YOY), and India (231.7% YOY).

• Machinery and components grew by 32.8% YOY, continuing for eight months, with growth in all major markets such as the U.S. (28.6% YOY) and China (98.1% YOY), except for India (-6.8% YOY).

• Fresh, chilled, frozen, and dried fruits saw a contraction of -22% YOY, marking the first decline in six months, due to a -15.2% YOY drop in exports to China, which accounts for 83.4% of Thailand's total fruit exports.

• Automobiles and components grew by 4.9% YOY, slowing from the previous month's 17.8% YOY growth. Although the YOY growth rate has slowed, when compared to the previous month on a seasonally adjusted basis, automobile exports increased by 4.5% MOM_sa after contracting in the previous two months, reflecting signs of recovery in line with the global economic direction.

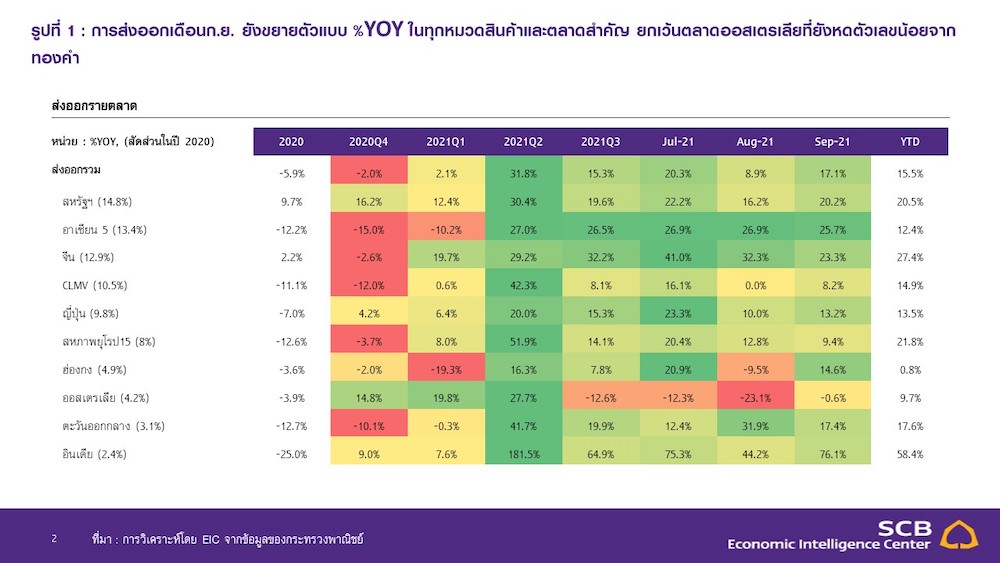

In terms of exports by market, growth was observed in all major markets except for Australia, which continued to see a slight contraction due to gold.

• Exports to India continued to grow at a high rate of 76.1% YOY, marking eight consecutive months of growth, with stable or growing exports in all major products such as fats and oils (426.4% YOY), plastic pellets (75.3% YOY), and chemicals (115.7% YOY).

• Exports to China grew by 23.3% YOY, supported by significant factors such as plastic pellets (14.1% YOY), cassava products (52.2% YOY), computers and components (27.7% YOY), and chemicals (75.9% YOY). However, fresh, chilled, frozen, and dried fruits, which contracted -15.2% YOY, shifted from being the most significant supporting factor in the past to a drag this month.

• Exports to CLMV rebounded to grow by 8.2% YOY after remaining stable at -0.03% YOY in the previous month. By country group, exports to Cambodia, Laos, and Myanmar grew by 48.9% YOY, 19.8% YOY, and 48.9% YOY, respectively, while exports to Vietnam contracted -23.3% YOY due to a severe COVID-19 outbreak in Vietnam. Exports to Myanmar rebounded due to significant growth in electrical wires and cables, which expanded by 7,308.7% YOY.

• Exports to Hong Kong rebounded to grow by 14.6% YOY after contracting -9.5% YOY in the previous month, supported by significant factors such as computers and components (33.2% YOY), electrical circuit boards (16.3% YOY), and jewelry (21.7% YOY), particularly gold, steel, and steel products (1,124.6% YOY). However, fax machines, telephones, and components (-44.4% YOY) continued to be a significant drag.

• Exports to Australia contracted for the fourth consecutive month at -0.6% YOY, slowing from the previous month's -23.1% YOY, with major export products that contracted including automobiles and components (-14.2% YOY) and gold (-100% YOY), with gold exports to Australia contracting by over 90% YOY for three consecutive months.

Figure 1: September exports continued to grow % YOY across all product categories and major markets, except for Australia, which saw a slight contraction due to gold.

Source: Analysis by EIC based on data from the Ministry of Commerce

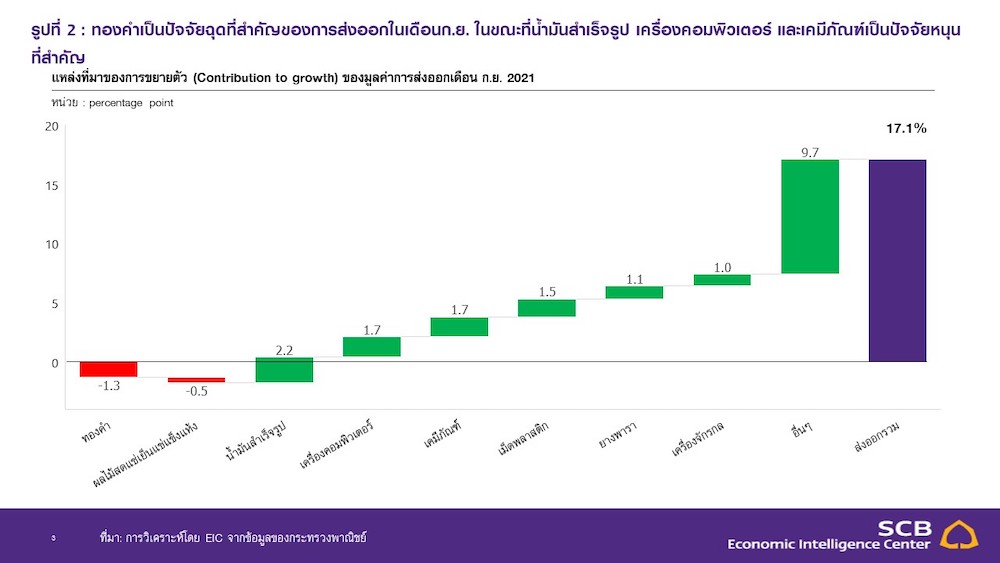

Figure 2: Gold is a significant drag on exports in September, while refined oil, computers, and chemicals are major supporting factors.

Source: Analysis by EIC based on data from the Ministry of Commerce

In terms of import value, September 2021 saw a growth of 30.3% YOY, slowing from the previous month's 47.9% YOY.

This growth was observed across all major import categories, including fuel products (43.9% YOY), which expanded due to both a low base and significantly increased prices compared to the previous year, capital goods (16.1% YOY), consumer goods (22.2% YOY), and vehicles and transportation equipment (16.2% YOY). Meanwhile, imports of raw materials and semi-finished products also grew at 44.6% YOY, and excluding gold, would grow at 43.6% YOY. For the first three quarters of 2021, imports grew at 30.9% YOY, with a trade surplus in September of $609.8 million. When combined with the first three quarters of 2021, the surplus amounts to $2,016.8 million.

Implication

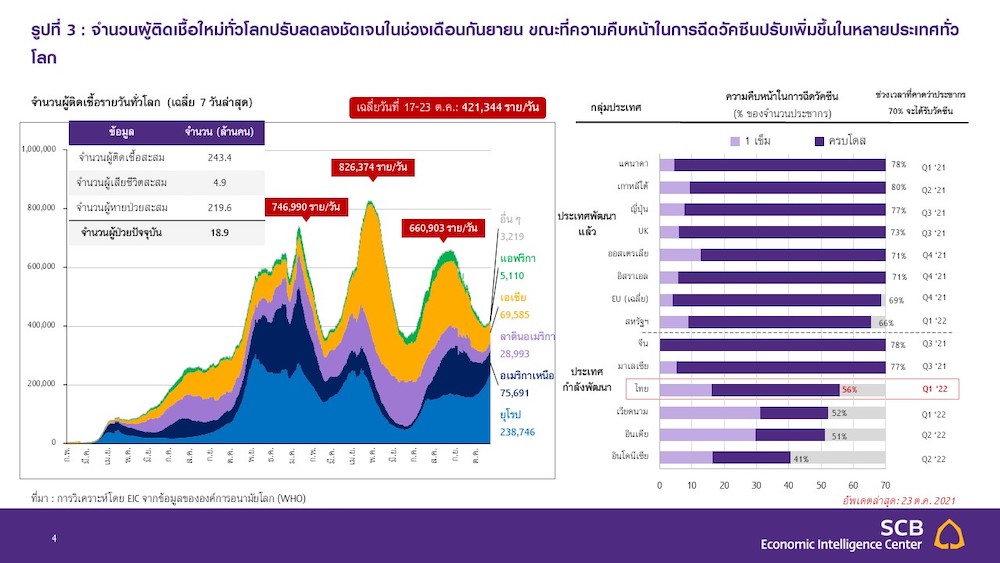

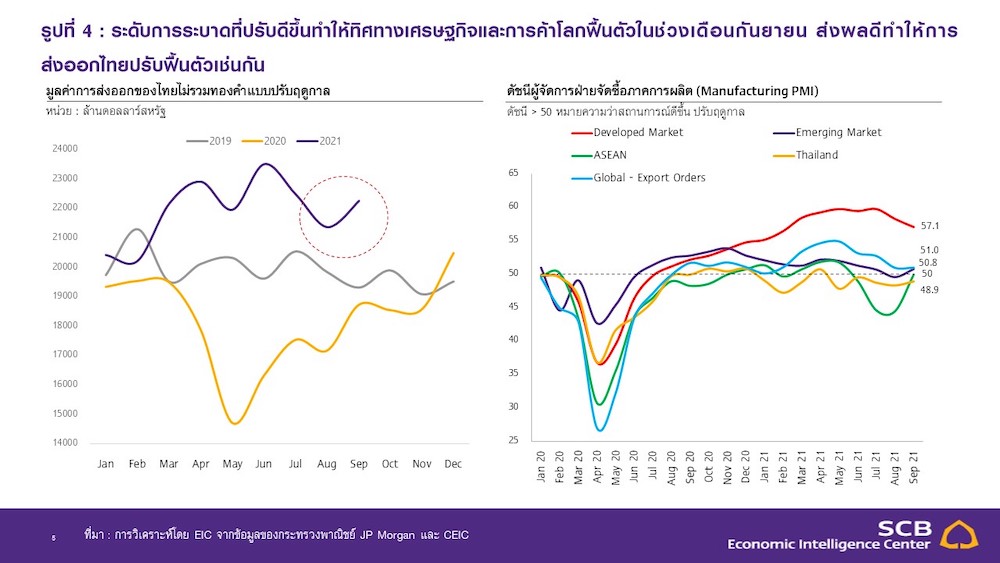

September exports have rebounded from the previous period due to the improved global pandemic situation. Exports in July and August had clearly decreased due to the impact of the global Delta variant outbreak, but the situation has improved since September (Figure 3), leading to a global economic recovery that positively impacts Thailand's export sector, resulting in a 4.2% increase in Thailand's export value excluding gold when compared to the previous month on a seasonally adjusted basis (mom_sa), in line with the Global Manufacturing PMI Export Orders and Manufacturing PMI in emerging markets (EM) and ASEAN, which have recovered from the previous period. Meanwhile, the Manufacturing PMI in developed countries has slowed but remains well above the 50 level (Figure 4).

Figure 3: The number of new infections worldwide has significantly decreased in September, while vaccination progress has increased in many countries around the world.

Source: Analysis by EIC based on data from the World Health Organization (WHO)

Figure 4: The improved outbreak levels have led to a recovery in the global economy and trade direction in September, positively impacting Thailand's exports as well.

Source: Analysis by EIC based on data from the Ministry of Commerce, JP Morgan, and CEIC

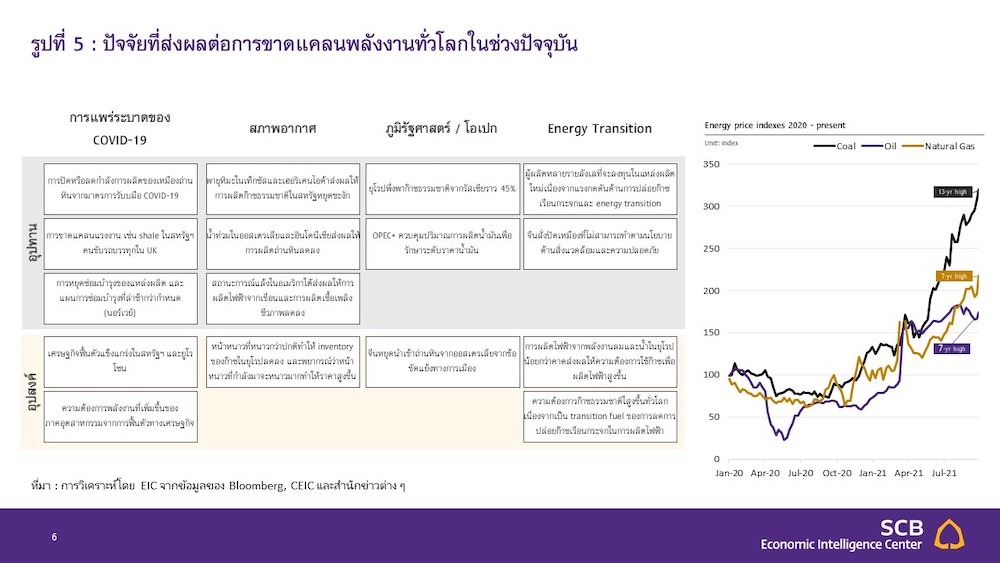

However, despite the recovery in exports from COVID-19, new pressures remain due to global energy shortages leading to rising inflation rates. The current global energy shortage is attributed to four main factors (Figure 5):

1) COVID-19 impacted energy production in the past, leading to reduced supply, while the current economic recovery has increased demand, resulting in energy shortages.

2) Unpredictable weather has affected the production of various energy types, such as natural gas and coal, and the upcoming winter will increase energy demand for heating.

3) Geopolitical issues, such as the uncertainty surrounding natural gas supplies from Russia to Europe and the conflict between China and Australia over coal.

4) The transition to clean energy (Energy Transition) has led to reduced or slowed investment in fossil fuel production, while clean energy is not yet able to fully replace it, contributing to the current global energy shortage. This shortage has caused significant increases in energy prices, raising concerns about inflation and stagflation (a situation where the economy grows slowly or contracts while inflation accelerates). Analysts expect that the current issues will only have short-term impacts, as the global economy, despite some short-term slowdowns due to purchasing power affected by rising inflation, still shows a good growth trend from the recovery of economic activities following vaccination progress. Therefore, the risk of stagflation remains low.

Figure 5: Factors contributing to the current global energy shortage.

Source: Analysis by EIC based on data from Bloomberg, CEIC, and various news agencies.

Additionally, attention must be paid to China's economy, which faces risks from the energy crisis and the real estate sector due to the Evergrande case, which could also impact Thailand's exports to China. Other pressures on Thailand's export sector include the ongoing semiconductor (chip) shortage, which will affect the automotive and electronics industries, as well as the shortage of shipping containers, which has kept shipping costs and delivery times significantly higher than normal.

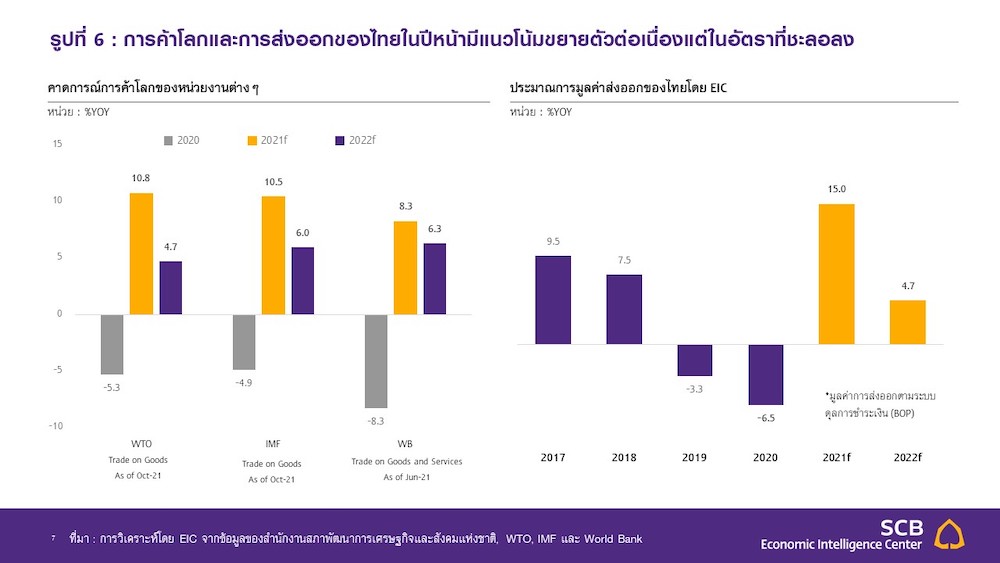

Although Thailand's exports face several pressures for the remainder of 2021, the EIC still forecasts a 15% YOY growth (export figures in the balance of payments system) as the latest export data aligns with previous forecasts that expected exports to recover in the remainder of the year following the severe Delta variant outbreak in July and August, although levels will not be as high as in the second quarter. For 2022, Thai exports are expected to continue growing at 4.7% in line with the global economy's slower growth rate. Exports to developing countries are expected to perform well next year due to the acceleration of economic recovery from increased vaccination progress.

Figure 6: Global trade and Thailand's exports are expected to continue growing next year, but at a slower rate.

Source: Analysis by EIC based on data from the National Economic and Social Development Council, WTO, IMF, and World Bank.

Analysis by... https://www.scbeic.com/th/detail/product/7892

Authors of the analysis:

Dr. Panundorn Aruneeniramarn ([email protected]), Senior Economist

Vishal Gulati ([email protected]), Analyst

Economic Intelligence Center (EIC)

Siam Commercial Bank Public Company Limited

EIC Online: www.scbeic.com