Thai SME Export Sector Facing New Challenges from US Tax Measures: Key Pressures for Adaptation and Survival

- The export sector plays a crucial role in the Thai SME economy, valued at over 1.2 trillion baht per year, accounting for 18% of SME GDP, with the US as the top export market, representing 18% of total SME exports. Most of the main products from Thai SMEs in the US market heavily rely on the US market and are facing significantly increased import tax rates, especially for product categories with over 60% export share to the US, many of which are taxed at an average of 20-30% or higher.

- SME exporters in 15 out of 31 main product categories exported to the US, such as decorative materials and building equipment, household items, furniture, etc., with an export value of about 24 billion baht per year, are classified as highly vulnerable to extreme vulnerability due to: 1) SMEs relying on the US market for more than 20%, 2) Thai products having a low market share in the US (not exceeding 30%), limiting bargaining power, and 3) Gross Profit Margin not sufficient to fully absorb the additional taxes.

- Krungthai COMPASS believes that Thai SMEs should accelerate production efficiency and reduce costs to alleviate tax cost pressures by adopting digital technology and automation systems. At the same time, they must innovate products to meet international standards and expand into new markets, increasing the use of domestic raw materials and production, which will enhance value and differentiate Thai products. This aligns with Reinvent Thailand's goal to enhance SME potential for sustainable growth, requiring cooperation between the public and private sectors.

The year 2025 will be a significant challenge for global trade due to the US's new trade regulation measures, which include increased import taxes on many items and stricter scrutiny of product origins to reduce trade deficits and protect key US industries. The US imposes a reciprocal tariff of 19% on Thai products exported to the US, along with reciprocal trade agreements for agricultural, energy, and aviation products.

The increase in US import taxes is a significant pressure on the income of the Thai export sector, with the US as the number one export market. From 2022 to 2024, Thailand's export value to the US averaged up to 50 billion USD per year. The increase in import taxes not only raises costs but also challenges the competitiveness of Thai exporters, especially SMEs, which have limited competitive capacity, weak financial status, and are already under pressure from high production costs. This challenge may affect their ability to maintain profit margins and expand markets in the long term.

This article from Krungthai COMPASS aims to illustrate the export situation of Thai SMEs to the US while assessing the vulnerability of SME exporters in each product category to reflect the risks faced by Thai SME operators amid rapidly changing trade contexts and adaptation strategies to survive current and future challenges.

Thai SMEs are vulnerable amid new global trade challenges.

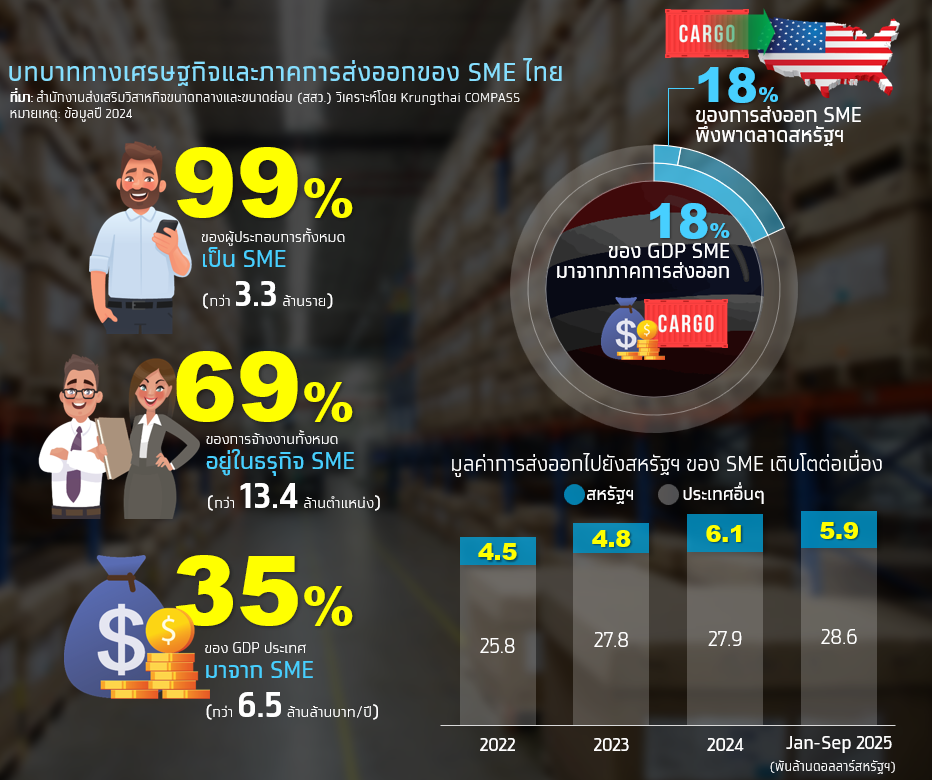

SMEs1 play a significant role in the Thai economy in terms of the number of entrepreneurs, employment, and value creation for the economic system. According to the Office of Small and Medium Enterprises Promotion (OSMEP), in 2024, there are over 3.3 million Thai SME entrepreneurs, accounting for 99% of all entrepreneurs, covering over 13.4 million jobs, which is over 69% of total employment. Thai SMEs generate an economic value of about 6.5 trillion baht per year, or 35% of the country's GDP.

The export sector is one of the main sources of income for Thai SMEs, with the US as the number one export market. Therefore, the risks from the US's strict trade policies are likely to directly impact Thai SME exporters. In 2024, Thai SMEs have a total export value of 34 billion USD (18% of SME GDP), and over the past three years, the export value to the US has continuously grown, reaching an export value of 6.1 billion USD at the end of last year (18% of the total value exported by SMEs worldwide).

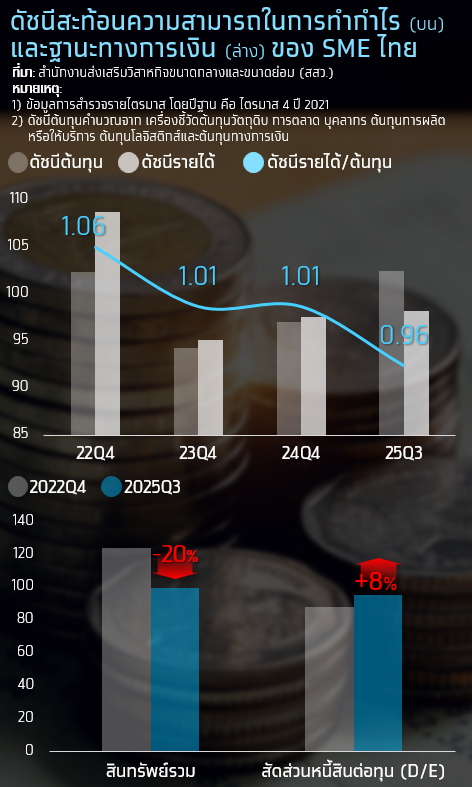

Despite their significant role in the economic system, Thai SMEs still face limitations in absorbing pressures from rising costs and economic volatility in the future. This is clearly reflected in the financial dimension. According to the SME situation indicators from OSMEP, over the past three years, the income index relative to the cost index of SMEs has continuously decreased and is below 1 in 2025, indicating that the ability to generate income for SMEs is not keeping pace with rising operational costs, resulting in squeezed profit margins and reduced financial buffers. Additionally, SME operators, especially micro enterprises2, have limited reserves and liquidity. Furthermore, the total assets of SMEs have decreased, while the debt-to-equity ratio has increased, with ongoing issues in accessing long-term funding from financial institutions, highlighting limitations in capital accumulation and business expansion amid rising debt burdens and reliance on high-cost short-term funding.

Thai SMEs are facing compounded pressures from the changing global trade context, particularly from the US's new trade regulation measures that have increased import taxes on many items and are likely to enforce stricter product origin regulations. Under this new context, SME exporters with thin margins, limited flexibility to restructure costs, and high reliance on imported raw materials are highly vulnerable amid the changes in global trade rules.

1 Definition of SMEs according to the Ministry of Industry's announcement on the characteristics of small and medium enterprises, 2019.

2 Micro = SMEs with income ≤ 1.8 million baht/year.

The increase in US import taxes affects the main export products of Thai SMEs in the US market.

The increase in US import taxes for each product consists of various types of taxes, which together create the total tax burden that exporters must face. The first part is the basic import tax (MFN rate), which is the normal import tax that the US imposes on trading partner countries under the World Trade Organization (WTO) framework. Another part is the additional tax from the US's import tax increase measures, which includes 1) retaliatory tariffs (Reciprocal tariff) that the US imposes on trading partners differently to create trade balance, 2) sectoral tariffs (Sectoral tariff) that the US sets specifically for certain industries or product types as per additional announcements, such as automobiles, automotive parts, metals, etc., and 3) penalties for transshipped goods (Transshipment penalty) in cases where the origin of goods is misrepresented to evade taxes, or may include products with low Regional Value Content (RVC) or Local Value Content (LVC)3 being taxed an additional 40%. However, there are still some products currently exempt from the increased import taxes under the US's new trade regulation measures.

For Thailand, it is currently subject to a retaliatory tax rate of 19% and sectoral taxes, with some products exempt from the increased import taxes under these measures. Regarding penalties for transshipped goods, although they are not yet widely enforced, the direction of US trade policy in the future is likely to emphasize scrutiny of product origins and added value generated within the country of origin, especially for products with high reliance on imported raw materials or low RVC and LVC ratios, which poses structural risk factors that exporters need to closely monitor.

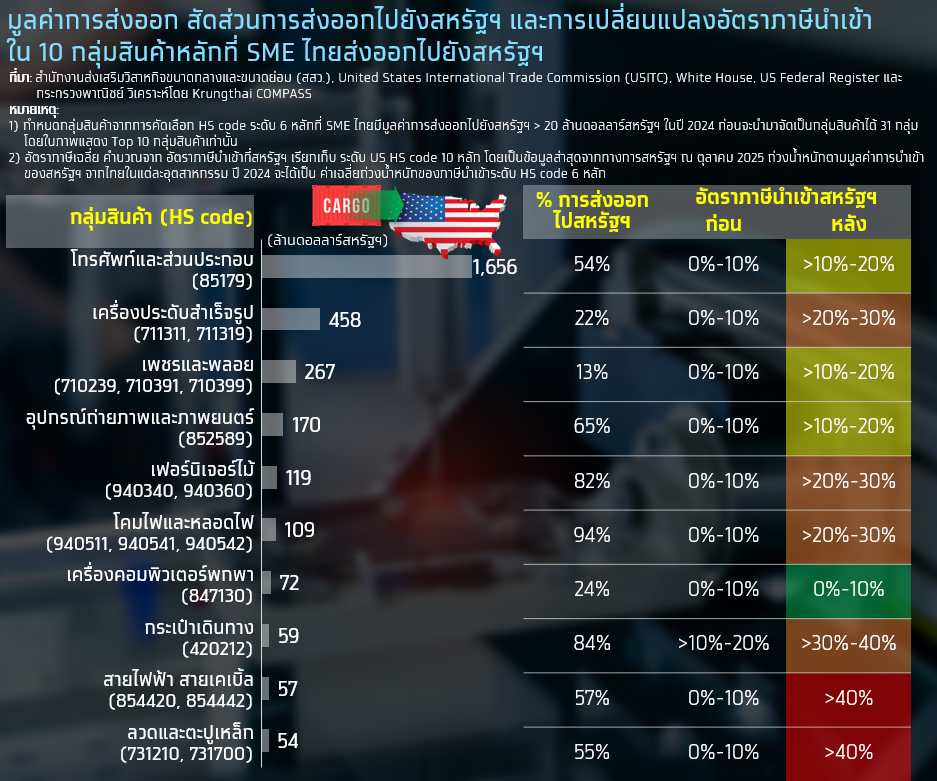

The main products of Thai SMEs exported to the US rely heavily on the US market and are facing significantly increased import tax rates. Considering the export data at the 6-digit HS code level that Thai SMEs exported to the US exceeding 20 million USD in 2024, it was found that phones and components are the number one product exported by Thai SMEs to the US, with an export value of over 1.7 billion USD per year, accounting for over 27% of the total export value to the US from Thai SMEs, with an export share to the US as high as 54% compared to the export value to the world. It is clear that exporters of phones and components must face higher import taxes, similar to other main export products of SMEs such as finished jewelry, diamonds and gems, photographic and film equipment, etc.

The proportion of added value generated from domestic or regional production processes compared to the total value of all products, under the ASEAN Trade in Goods Agreement (ATIGA), products that are considered to originate in ASEAN and are entitled to tax privileges must have a Regional Value Content of no less than 40%.

Products that Thai SMEs rely heavily on the US market are likely to be subjected to higher import taxes as announced by the US, with the relationship between the proportion of exports to the US and average import tax rates showing a similar trend. Particularly for product groups with over 60% export share to the US, many items are taxed at an average level of 20-30% or higher. This tax burden increases while exporters may have limitations in passing costs onto US importers, especially in cases of lower bargaining power, which will pressure the profitability of Thai SME exporters. Exporters of products that heavily rely on the US market are therefore likely to be more vulnerable than exporters of other product groups. This leads to the next analysis of how much tax burden SME exporters can absorb compared to their current performance to reflect the level of vulnerability of exporters in each product group.

Which product groups of SME exporters are likely to be highly vulnerable?

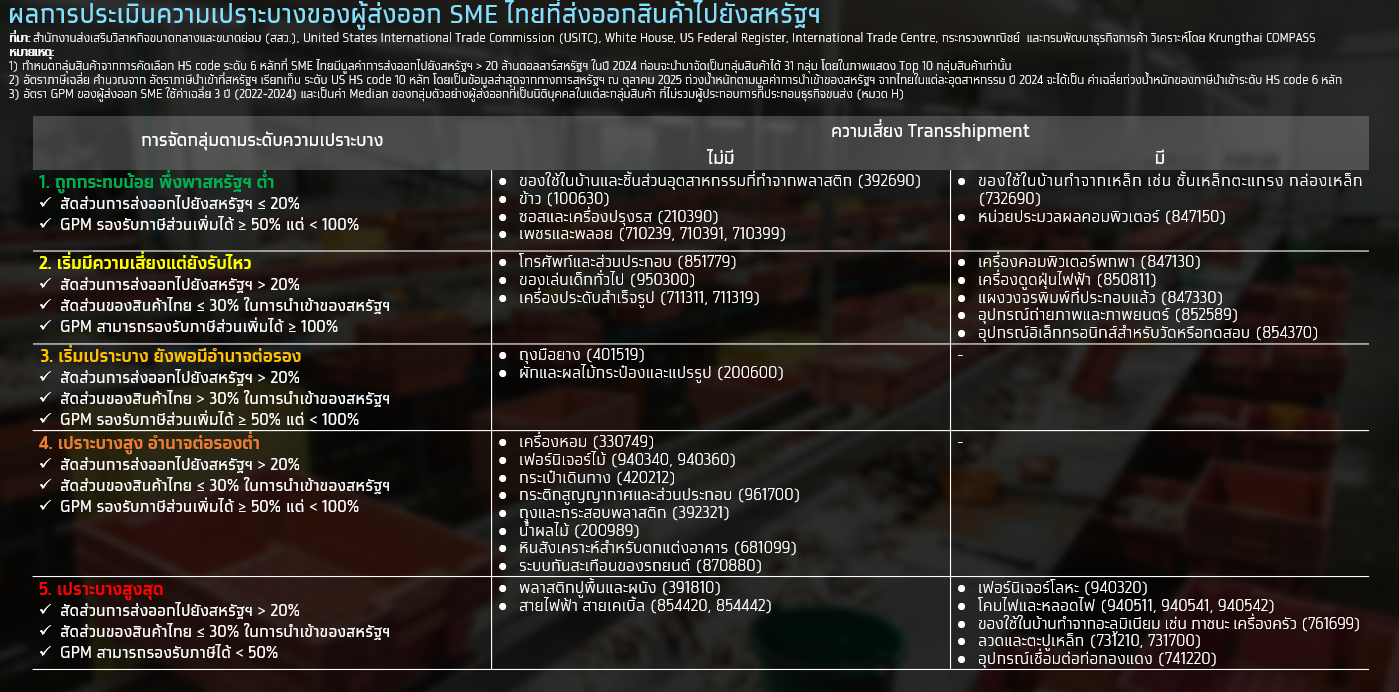

Krungthai COMPASS assesses the vulnerability of Thai SME exporters exporting products to the US, with the scope of analysis being products at the 6-digit HS code level that Thai SMEs exported to the US exceeding 20 million USD in 2024, then categorizing them into 31 groups while considering the vulnerability of SME exporters based on three factors:

1) The proportion of reliance on the US market of the main export products that Thai SMEs export to the US, with the criteria being the proportion of export value to the US compared to total exports of each product group ≤20% and >20%, which is close to the average proportion of reliance on the US market of SME export products overall.

2) The proportion of Thai products in US imports to reflect the bargaining power of Thai exporters, with the criteria being the proportion of the value of goods imported from Thailand by the US compared to total imports of the same product group ≤30% and >30%, in line with the Mercator Institute for China Studies (MERICS) which states that significant bilateral suppliers are countries with export shares exceeding 30% of total imports of those goods by the importing country.4

3) The ability of SME exporters to absorb US import taxes by considering the increased import tax rates compared to Gross Profit Margin (GPM) under two assumptions: that exporters absorb 50% of the additional tax and that exporters absorb 100% of the additional tax.

The assessment results of the vulnerability of Thai SME exporters exporting products to the US are divided into five groups, with exporters of 15 out of 31 groups classified as highly vulnerable to extreme vulnerability. This is due to 1) being exporters in product groups that SMEs heavily rely on the US, with export value to the US >20% compared to total export value, 2) Thai products having a low market share in the US, with the proportion of the value of goods imported from Thailand by the US ≤30% compared to total imports of the same product group, reflecting limited bargaining power, and GPM not being able to fully absorb the additional taxes.

The 15 product groups mentioned above have a total export value in 2024 of over 678 million USD or 23,723 million baht, accounting for 11% of the export value to the US in the same year. If categorized by product type, the category with the highest export value is decorative materials and building equipment, such as synthetic stones for building decoration, flooring and wall plastics, as well as lamps and light bulbs. The next category is general household items, such as fragrances, luggage, vacuum flasks and components, aluminum household items, and plastic bags and sacks. Additionally, they are spread across other product categories such as furniture, metal equipment, automotive parts, and food.

Moreover, there are several product groups at risk of being identified as Transshipment due to their tendency to use raw materials from the region or domestically at low proportions, reflecting the additional risks of the main products that SMEs export to the US and the structural vulnerabilities of Thai SMEs' supply chains. Increasing the proportion of domestic production and the use of domestic raw materials, along with having a transparent and verifiable traceability system, is therefore a crucial approach to mitigate such risks and enhance the credibility of Thai product origins in other groups.

Implication & Recommendation:

Enhancing production efficiency and cost management is a crucial buffer for Thai SME exporters in a situation where trade costs and import taxes are rising, especially for exporters in the highly vulnerable to extreme vulnerability group, who have thin GPM and cannot absorb additional import taxes and lack bargaining power. This also increases competitive opportunities from Trade Diversion for products that still have low market shares in the US and have potential for price competition due to having high GPM, to increase opportunities for price competition and capture market share in the US from competitors facing higher taxes. This can be achieved through the adoption of digital technology and automation systems to streamline workflows, reduce time and unit costs, minimize errors and reliance on labor, enhance inventory management accuracy, and reduce waste in the production process.

Creating added value for Thai products through innovation and international standard certification is key to enhancing the competitiveness of Thai SMEs in the long term, especially for products in the highly vulnerable to extreme vulnerability group that heavily rely on the US market, while having limited bargaining power and profitability. Investing in research and development, designing differentiated products, and obtaining international environmental or sustainability standards will enable Thai products to compete on quality rather than price and elevate their role in the global value chain to a higher level, whether it is producing complex and high-value products or developing products/services that meet environmental and sustainability trends, thus expanding into new markets and reducing reliance on any single market. This aligns with Reinvent Thailand's goal to transform the economic structure towards value-added production and enhance the growth potential of Thai industries, which requires cooperation from all sectors, including the government, business, and finance.

Developing domestic industries and increasing the proportion of Local Content, along with having a transparent traceability system, is crucial for strengthening the export sector and the overall economy of SMEs through investment promotion measures, international knowledge exchange, developing skilled personnel, and linking large enterprises with SMEs. This not only helps reduce risks related to trade regulations but also increases the transparency of product origins and enhances the credibility of Thai products in the global market. Additionally, it creates new income bases and distributes income within the country by linking large producers with domestic SMEs, resulting in increased circulation of added value within the economy, which will help elevate the income of Thai SME operators in the supply chain and reduce the leakage of added value to foreign countries.