The Housing Market in 2022 Reflects Recovery, But Not Universally; In 2023, Support Factors Weaken, Pressuring Growth

The Housing Market in 2022 Reflects Recovery, But Not Universally; In 2023, Support Factors Weaken, Pressuring Growth

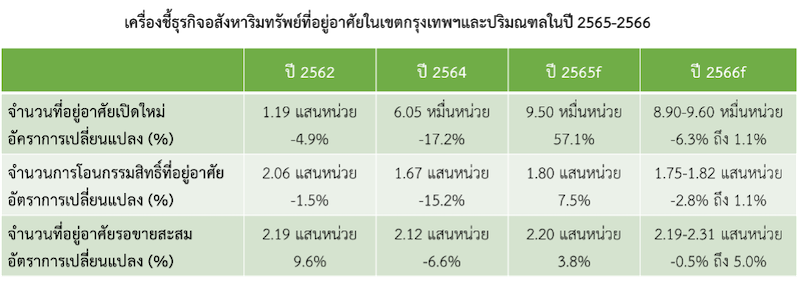

- The indicators of the residential real estate market in 2022 show a better recovery, but it is not widespread. Although the launch of new projects has accelerated, it is driven by specific business factors, while the transfer of ownership for new residential properties or from legal entities remains weak.

- KASIKORN Research Center holds a cautious view on the direction of the housing market in 2023 as support factors begin to weaken. The Bank of Thailand has not extended the LTV relaxation measures (which ended on December 31, 2022), and the market must monitor whether the authorities will extend the measures to reduce fees for purchasing housing. Meanwhile, the uncertain economic recovery, fragile purchasing power, rising interest rates, high competition in the business, and a large number of unsold properties all continue to pressure housing buying and investment activities in the near future.

- KASIKORN Research Center estimates that in 2023, the transfer of ownership for residential properties in Bangkok and its vicinity (including legal entities and individuals) is expected to be around 175,000 to 182,000 units, representing a contraction of 2.8% to a growth of 1.1%, compared to the anticipated growth of 7.5% in 2022.

In 2022, the indicators of the residential real estate market reflect a better recovery, but not universally. While the launch of new projects has accelerated, the transfer of ownership for new residential properties or from legal entities has slowed down.

Confidence in the economic recovery after the easing of COVID-19 and the recovery of the tourism sector has led residential property developers to accelerate investments in new projects. According to AREA data, in the first nine months of 2022, the launch of new residential properties in Bangkok and its vicinity grew by as much as 110% compared to the same period last year (YoY), totaling 77,000 units.

However, the acceleration in launching new residential properties is likely driven by specific business factors, as some developers have reduced their backlog due to the rapid sales of completed properties in the past, affecting future revenue recognition. Therefore, developers still need to continue investing, especially in condominium-type housing that takes more than a year to build. With rising construction and financial costs, some developers chose to launch projects this year to lock in business costs.

For new residential properties launched in 2022, more than half came from condominium launches, with most being in the price range below 2 million baht (accounting for about 55% of the total number of new condominiums launched in Bangkok and its vicinity), resulting from the One Million Houses project, which supports low-interest loans for developers of properties priced below 1.5 million baht.

Meanwhile, the activity of buying new residential properties has not fully recovered due to the overall purchasing power of households still being fragile from the burden of living costs and high debt, while the sales of second-hand properties have received good responses from buyers.

In 2022, the market received significant support from measures to reduce transfer fees and mortgage fees for residential properties, as well as the relaxation of LTV measures. According to REIC data, in the first eight months of 2022, the transfer of ownership for residential properties in Bangkok and its vicinity grew by 8.5% (YoY). However, it is noteworthy that transfers from legal entities or new residential properties decreased by 5.3% (YoY), while transfers from individuals or second-hand properties grew by 26.5% (YoY). This is due to several reasons, including the fact that over the past two years, developers have delayed launching new projects (affecting the number of completed properties entering the market in 2022) and the low take-up rate for new residential properties, which impacted the transfer numbers this year. Additionally, since new residential properties have a higher average price per unit (compared to usable area), even with promotional sales from developers, some consumers have opted to purchase second-hand properties, which have also seen an increase in listings.

However, in the last two months of 2022, there may be an acceleration in the transfer of ownership for residential properties after the relaxation of LTV measures ends this year, but it will still depend on the ability and qualifications of the buyers.

The outlook for the housing market in 2023 presents a more cautious perspective due to the highly uncertain market environment regarding economic recovery and uneven purchasing power, while businesses face increasing challenges.

In 2023, the continuity of the recovery in the residential real estate business will depend on several factors, leading KASIKORN Research Center to adopt a more cautious view. Although it is expected that the country's economic activities and citizens' incomes will gradually improve, those who are ready may decide to purchase housing. Similarly, the purchasing direction for condominiums by foreigners is expected to remain stable, close to that of 2022, due to the reopening of the country and measures to attract high-potential foreigners.

In addition to economic uncertainties, especially from the global economic slowdown, the market also faces several challenging factors that need to be monitored:

- The extension of government measures to alleviate the burden of housing purchase expenses is still awaiting clarity, including measures to reduce transfer fees and mortgage fees for properties priced below 3 million baht, which will end on December 31, 2022. If the authorities extend these measures, it would be a positive factor for the housing market, estimating that for every 1 million baht, homebuyers would save approximately 2.98% or about 29,800 baht.

- KASIKORN Research Center estimates that in 2023, the transfer of ownership for residential properties in Bangkok and its vicinity (including legal entities and individuals) is expected to be around 175,000 to 182,000 units, contracting by 2.8% to growing by 1.1% from the anticipated growth of 7.5% in 2022. This estimate considers the possibility of the authorities extending the fee reduction measures.

- The trend of rising interest rates in 2023 will pressure the purchasing power for housing for buyers who rely on financial institution loans, as most housing loans are on floating interest rates, even with long repayment terms.

- The increase in business costs affects housing prices and the liquidity of developers, as key operational costs are continuously rising, including land prices, construction materials, labor costs, and financial costs. Therefore, when operational costs rise, it will inevitably lead to higher housing prices in 2023. At the same time, some developers may also face increased costs from land and building taxes.

- The supply of unsold properties in the market remains high. Although developers have accelerated marketing efforts, there will still be completed properties entering the market. It is expected that the number of unsold properties in Bangkok and its vicinity at the end of 2022 will be higher than the approximately 207,000 units in the first half of the year, partly reflecting the average take-up rate for new residential properties, which has contracted for single-family homes and townhouses in the first nine months, while condominiums have seen only slight increases.

When combined with the accelerated investment in new projects, especially in the price range of 2.0-5.0 million baht (accounting for about 57% of the unsold properties), which aligns with the purchasing power of most domestic consumers, the market will face even more intense competition amid a recovery in demand that will take time.

KASIKORN Research Center therefore believes that in 2023, the launch of new residential projects in Bangkok and its vicinity may decrease to 89,000-96,000 units, representing a contraction of 6.3% to a growth of 1.1% compared to the acceleration in 2022. The launch of condominiums is expected to slow down from the large number launched in 2022, with new project areas focusing on middle Bangkok and outer areas extending to the provinces due to rising land prices in inner Bangkok, coupled with the development of infrastructure such as the expansion of the electric train network to the outskirts of Bangkok.

Source: REIC, AREA, and estimates by KASIKORN Research Center

*The baseline scenario considers the effects of extending measures to reduce the burden of housing purchase expenses, including measures to reduce transfer fees and mortgage fees for properties priced below 3 million baht.

*The worst-case scenario does not include the effects of extending measures to reduce the burden of housing purchase expenses.

KASIKORN Research Center sees that in the near future, the environment of the residential real estate market remains highly uncertain, leading developers to prepare for business operations to remain competitive in the market. The key variables for the success of upcoming projects, in addition to the product and location, also rely on specific management capabilities in various dimensions, such as cost management in a rising cost environment. Managing costs to be lower means being able to set prices lower than competitors or having higher profit margins than competitors, and construction management by reducing construction time while maintaining quality will also help control supply volumes to meet targets. Additionally, completing housing quickly will build credibility in the eyes of consumers. Furthermore, market research of the areas to invest in is crucial for strategic planning, such as defining target customer groups, pricing, sizes, and housing types that meet the needs of buyers and balancing supply and demand in target areas.