Analyzing the Thai Economy from the Perspective of Thai Banks

Analysis from Kasikorn Research Center

The COVID-19 pandemic, which has lasted nearly two years, reflects various aspects that compel different parties to reconsider. This includes the impact of the pandemic itself as well as pre-existing issues within each economic unit that the pandemic has exacerbated. Consequently, moving forward will require addressing both immediate challenges and medium- to long-term issues to ensure stable and competitive growth in a landscape that will never return to its former state.

Looking back at the commercial banking sector as a lens to examine customer issues reveals several interesting points:

The current net profit situation of the Thai banking system is partly derived from accrued interest income, while Thai banks are financially weaker than their neighbors and are expected to recover more slowly.

• Although the overall commercial banking sector (including registered Thai banks and branches of foreign banks) reported an average net profit exceeding 50 billion baht per quarter in the first half of 2021, part of this was due to recognizing interest income under TFRS9 accounting standards, which did not involve actual cash inflow, particularly from debts under financial assistance measures or those unable to repay principal and interest normally.

Under the new accounting standards implemented since 2020, banks continue to recognize interest income from borrowers facing COVID-related issues as 'accrued rights.' This criterion, combined with the horizontal debt repayment method announced by the Bank of Thailand in October 2020 (effective July 2021, which prioritizes the repayment of the oldest overdue amounts), has resulted in banks holding higher accrued interest than under previous calculations. Currently, when debt restructuring and payment deferral measures are in place, banks will collect debts towards the end of the contract, meaning they will retain accrued interest without certainty about whether and how much borrowers will actually repay. However, under these circumstances, banks can assess the credit risk of borrowers and increase their loan loss provisions, leading to higher provisioning levels in the commercial banking system compared to before the COVID-19 pandemic.

Initially, Kasikorn Research Center has assessed that the impact of the change to TFRS9 accounting in 2020 and the recognition of interest income from debts under financial assistance measures, which increases accrued interest (after deducting increased provisions from before COVID in 2019), may account for no more than 10% of net profit, assuming an average return on the loan portfolio under financial assistance measures is around 3%.

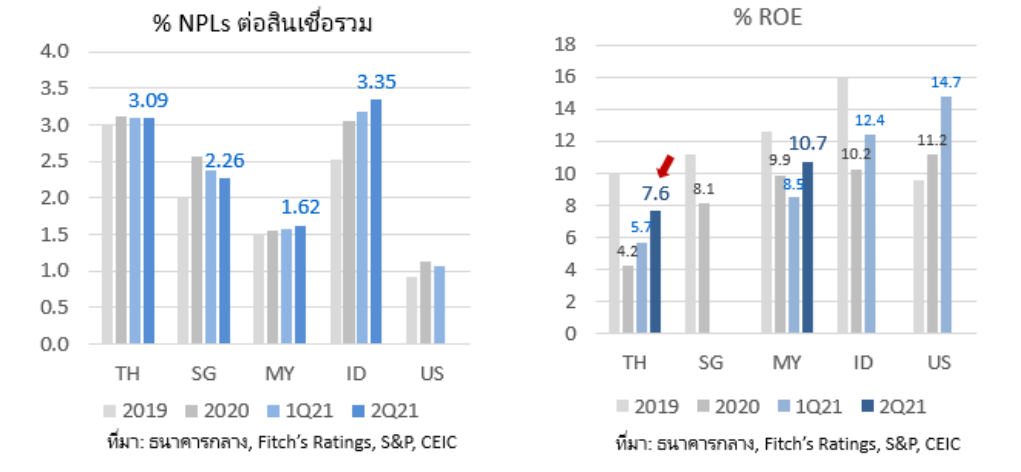

• The slower reduction of debts under financial assistance measures compared to neighboring countries affects accrued interest and the recognition of interest income. Although this international accounting standard is also applied in neighboring countries such as Malaysia and Singapore, the difference that may disadvantage Thai banks is the higher proportion of customers under financial assistance measures, which has decreased more slowly. As of February 2021, this was at 15.4% compared to Singapore's 3% (January 2021) and Malaysia's 15% (February 2021), respectively.

• The issues arising with borrowers also affect the quality of non-performing loans in the commercial banking system, making it worse than in neighboring countries like Singapore and Malaysia. Meanwhile, profitability measured by the return on equity (ROE) is lower than in those countries due to concerns over loan quality, necessitating high loan loss provisions.

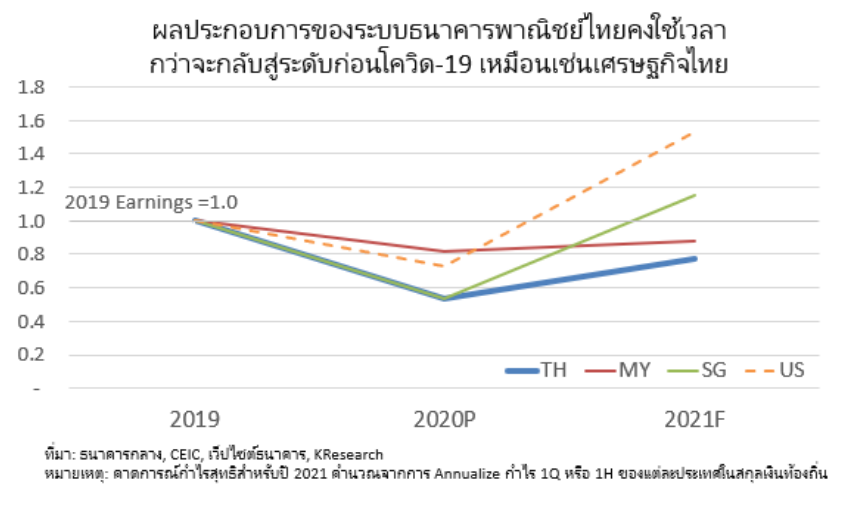

• Given the COVID situation, which has led to a slow recovery of the Thai economy, many commercial banks are focused on customer assistance activities and managing related loan quality issues. This has resulted in the commercial banking system likely experiencing a slower recovery in performance compared to other countries. It seems unlikely that figures will return to pre-COVID levels within the next 1-2 years, while Singapore and the United States are expected to see a recovery in performance returning to pre-COVID levels in 2021. Therefore, the accumulation of profits and capital in the commercial banking system is aimed at preparing for the high level of economic uncertainty that still exists, and to date, no one can definitively say when or if the COVID issue will truly end.

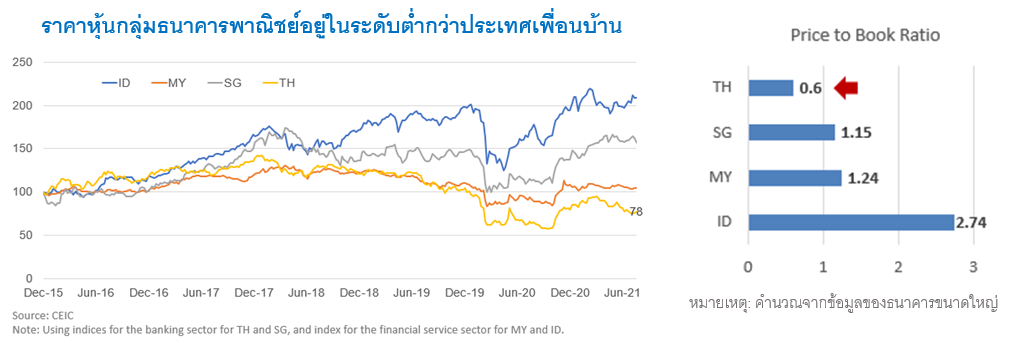

• The pressures on the overall commercial banking system have resulted in the price-to-book ratio being lower than in neighboring countries, reflecting a comparative disadvantage in profitability, which in turn affects the stock prices of these banks compared to their neighbors.

From the banking perspective... it underscores the customer and economic issues in Thailand that must be seriously addressed post-COVID.

The performance of the Thai commercial banking system is likely to recover slowly, with loan quality issues and the slow reduction of debts under financial assistance measures compared to neighboring countries reflecting various economic problems in Thailand, including:

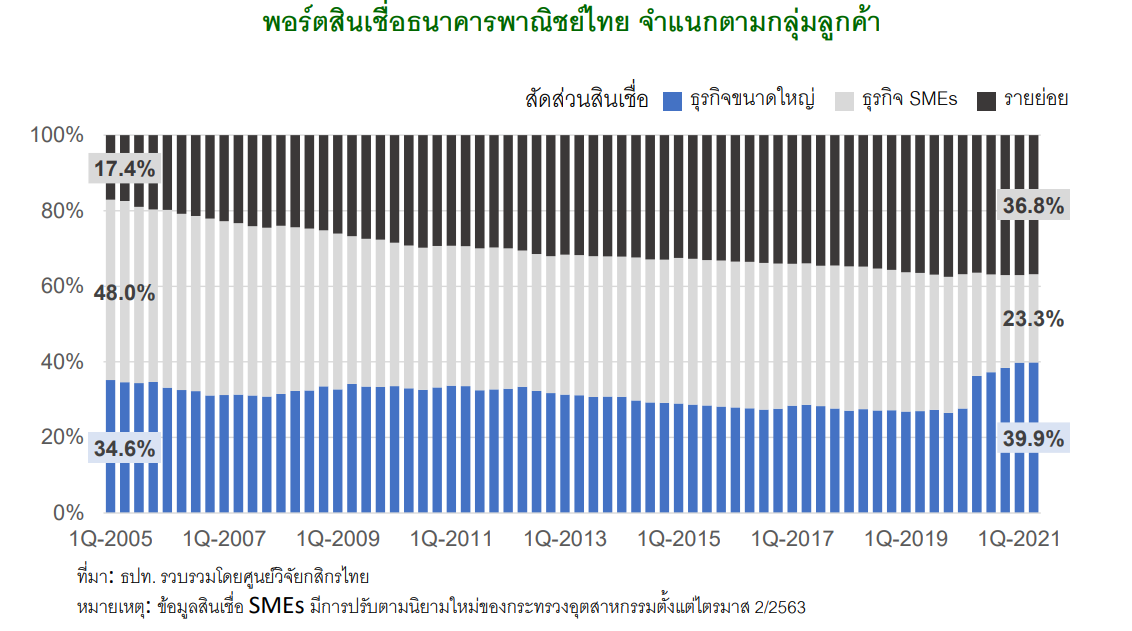

• The economic structure with a high proportion of businesses severely impacted by COVID, such as hotels, transportation, construction, real estate, and wholesale and retail trade, which accounted for approximately 33.1% of GDP (in 2019). These are significant service sector businesses that have driven the economy in the past, leading commercial banks to have a high proportion of loans in these sectors, accounting for 49.0% of total business loans (excluding financial activities) in 2019, although this has slightly decreased to 48.1% by the end of Q2 2021. If focusing specifically on SMEs in these five categories, the proportion has increased to 60.5% by the end of 2019 and 64.0% by the end of Q2 2021.

• The competitiveness issues of the country, which have already posed challenges for many businesses, were exacerbated by COVID in 2020. For example, businesses in the service sector faced already challenging contexts and will face increased challenges from changing customer behaviors both domestically and internationally, competition from digital platforms, and new technologies. This will require traditional operators to adjust their goals and business methods, including creating added value and finding unique selling points. The various forms of disruption mentioned above will significantly impact SMEs.

Thai commercial bank loan portfolios categorized by customer group

Meanwhile, the Thai banking system has shifted its focus towards SMEs in a higher proportion after the 1997 crisis to reduce the concentration of large customer portfolios, with SME loans increasing to nearly 50% in 2005 before gradually declining to 35.6% in Q1 2019 (since Q2 2019, the definition of business size by the Ministry of Industry changed, significantly affecting the proportion of the SME portfolio). Ultimately, this has impacted the status of the Thai banking system due to the competitiveness issues of customers, both directly and indirectly.

• Households have seen their financial status deteriorate further after COVID due to:

1) Increased household debt

2) A slow recovery in the labor market, as the recovery of businesses is uneven, and there are skill-related issues that will take time to recover after facing unemployment or working at low levels for several years, especially in the service sector.

3) Changes in employment patterns leading to fewer permanent employees or reduced additional benefits to lower business costs.

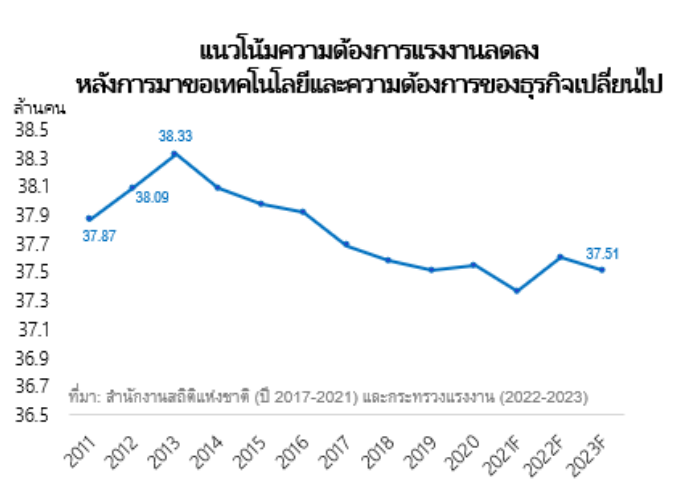

4) A declining demand for labor as businesses increase their use of technology.

As of the latest data from the commercial banking system's loan portfolio, retail customers accounted for 39.9% of total loans by the end of Q2 2021.

In summary, looking ahead, although the commercial banking system may experience a slower recovery in performance or loan quality issues compared to neighboring countries amid ongoing uncertainties surrounding the current COVID situation, the more pressing and concerning challenge will be the survival of businesses and households facing income issues and competitiveness challenges, along with rising debts in a new economic context and environment. Additionally, there is a need to urgently find answers on how Thailand can leverage its business strengths to attract foreign investment amidst technological limitations, as this will determine the sustainability of the economic direction, businesses, households, and the Thai commercial banking sector in the long term.

Meanwhile, during this period, commercial banks will likely address problems and adapt to find ways to confirm alternative income for customers, seek potential clients (which are dwindling), reduce costs in various dimensions, and explore opportunities from new business models beyond traditional finance. While this may help broaden access to financial services for customers and support economic growth, it cannot transform into sustainable growth without serious economic restructuring after COVID ends.