Warehouse Market Surges Despite Economic Challenges, Rental Rates Reach 88.9%

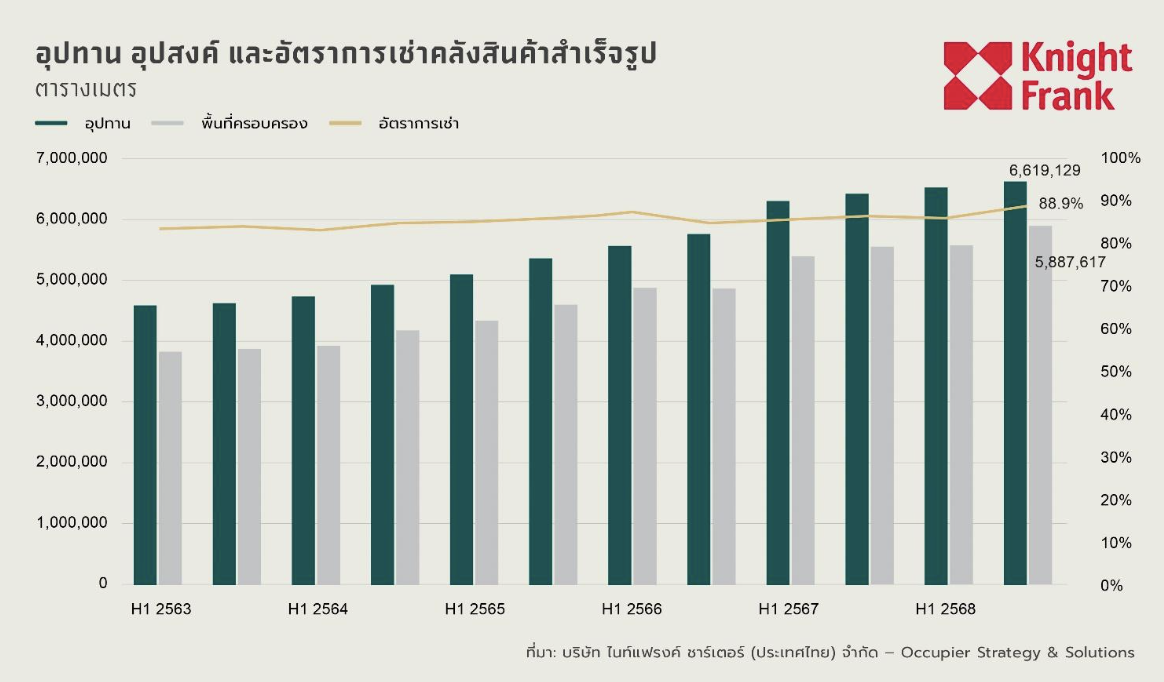

The Thai logistics real estate market in the second half of 2025 continues to show remarkable strength, with demand for warehouse space on the rise. This is occurring even as the overall economy recovers unevenly and domestic consumption remains cautious. The national warehouse rental rate has increased to 88.9%, up 3.1 percentage points from the first half of the year, driven by a surge in rental activity and effective absorption of new supply. Total warehouse supply has slightly expanded to 6.62 million square meters, a 1.9% increase from the first half, while occupied space has grown at a much higher rate of 5.6%, reaching 5.89 million square meters. This reflects a clear recovery in market demand as operators continue to lease space to meet trade activities, inventory management, and supply chain adjustments.

Improved demand is particularly evident in the country's logistics hubs, with the central region experiencing the highest rental rate increase of 5.6 percentage points, reaching 92.0%. Meanwhile, Bangkok and its vicinity maintain a high rental rate of 92.6%. The Eastern Economic Corridor (EEC), a strategic industrial area, continues to show positive trends, with rental rates rising to 83.5%, supported by the export manufacturing sector. This growth occurs despite ongoing macroeconomic volatility, as Thailand's GDP in the fourth quarter of 2025 improved to 2.5% from 1.2% in the previous quarter, bolstered by government spending, a recovery in tourism, and stabilizing domestic demand. However, the overall economy is still recovering unevenly, with the manufacturing sector contracting and general inflation remaining at a negative level of around -0.5%, reflecting fragile purchasing power and cautious consumption.

Amid this context, current logistics demand is not solely driven by overall economic growth but is increasingly supported by structural factors within the production and trade systems. The export sector remains a key driver, with export value in the fourth quarter reaching 2.22 trillion baht, while inventory levels have returned to a buildup phase, indicating early signs of restocking. This has led businesses to seek more warehouse space to accommodate product storage and enhance distribution network efficiency. Industries with high logistics intensity, such as electronics, which are experiencing strong growth in semiconductors and data center-related components, as well as the steel and automotive sectors, continue to see increased demand for storage space, distribution, and inventory management. Although rental rates have improved, the growth of rental prices remains relatively stable, with average rents rising slightly to around 161.7 baht per square meter per month, reflecting operators' price discipline despite improved demand conditions.

Looking ahead, Thailand's logistics real estate market is likely to continue benefiting from trade activities, supply chain restructuring, and ongoing investments in export-oriented manufacturing. While the overall economy may still expand at a moderate pace, the logistics sector's ability to meet demand linked to global trade and industrial restructuring will ensure that this sector remains a crucial mechanism for strengthening the Thai economy in the long term. Marcus Berthenshaw, Partner – Head of Logistics and Industrial Advisory at Knight Frank Thailand, stated, "What we are seeing in the logistics market now is not just a recovery in demand but a structural shift in supply chain management. Operators are placing greater emphasis on flexibility, inventory management, and operational efficiency, which supports the demand for high-quality warehouses in strategic locations, even amid overall economic uncertainties."