SCB FM Views Strengthening Baht After Temporary Ceasefire Agreement as an Opportunity to Buy USDTHB

The Financial Markets Group of Siam Commercial Bank (SCB FM) has revealed that the direction of the Thai baht at this time is significantly influenced by the trend of the war in Iran. The recent strengthening of the baht is a result of the temporary ceasefire agreement between the United States and Iran, which presents a good opportunity for importers or investors to purchase USDTHB. However, in the future, uncertainty remains high. If hostilities resume, the market may become risk-averse, causing the baht to weaken again. The conditions for a permanent ceasefire are still ambiguous and differ significantly, so it is advised that operators consider additional risk hedging in case transportation through the Strait of Hormuz increases, although it may not return to the free and safe state it was in before the war. USDTHB may range around 32.15-32.65. In the worst-case scenario, if the ceasefire negotiations fail and the war reignites and drags on into the second half of the year, USDTHB could rise to around 34.00-35.00. However, the likelihood of this worst-case scenario has significantly decreased following the two-week ceasefire agreement, with the market giving an 86% chance that Trump will announce the end of the war by June.

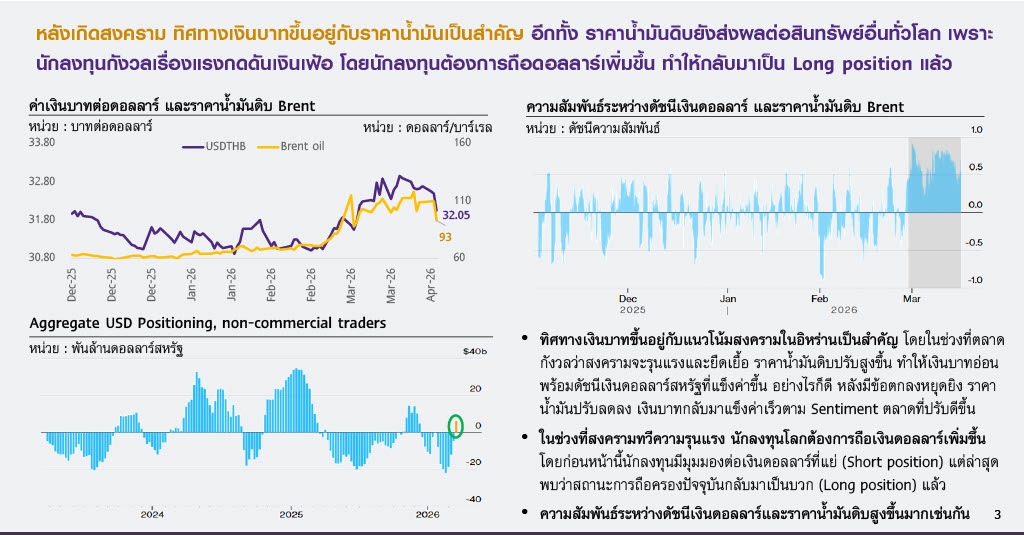

Mr. Patrick Pouliot, Deputy Managing Director and Head of Financial Markets Function at Siam Commercial Bank, stated that the baht has quickly strengthened after the U.S. and Iran reached a two-week temporary ceasefire agreement. Previously, when the market was concerned about the war escalating and dragging on, crude oil prices rose, causing the U.S. dollar index to strengthen as global investors sought safe assets. Additionally, it was observed that the dollar's holdings shifted from a short position to a long position, putting pressure on regional currencies and causing the baht to weaken more than others, as Thailand has the highest proportion of energy imports from abroad (relative to the size of the economy), accounting for about 8% of GDP. However, after the ceasefire agreement, oil prices quickly dropped by nearly 20%, the U.S. dollar index weakened along with U.S. Treasury yields, and improved market sentiment led to an increase in risky assets such as stocks, causing regional currencies, including the baht, to strengthen again.

Looking ahead, the trend of the baht will largely depend on the war in Iran. In thebase case, if the war may reduce in intensity or end within this month, the USDTHB range is expected to be around 32.15-32.65. Mr. Patrick added that if the U.S. and Iran ease their conditions, negotiations may proceed more smoothly. However, it is expected that after the two-week temporary ceasefire, there may still be some minor attacks, as the permanent conditions remain unclear and differ. For transportation through the Strait of Hormuz, it is anticipated that in the base case, it may increase, but it may not return to the free and safe state it was in before the war, which could keep Brent crude oil prices around $90-100 per barrel. In the second half of the year, if the war does not reignite violently and oil transportation through the strait gradually returns to over 80%, oil prices may decrease further to around $80-90 per barrel by the end of the year. Therefore, the baht is likely to weaken the most in the second quarter when the war has high uncertainty, but it should gradually strengthen in the remaining part of the year.

- In the case of abetter case, if the ceasefire negotiations succeed within this month and transportation through the Strait of Hormuz can resume freely and normally, Mr. Patrick sees the USDTHB range in this case at around 31.50-32.00 in the next month. He believes that a quick end to the war will lead to crude oil prices dropping to around $85-95 per barrel, which will increase market sentiment towards risk (risk-on), allowing the baht to strengthen further. However, the likelihood of transportation through the strait returning to normal within this month is still not very high, as reflected by Polymarket, which gives a chance of about 50%.

- In the case of aworst case, if the ceasefire negotiations fail and the war drags on into the second half of the year, the USDTHB range could rise to around 34.00-35.00 as oil prices may continue to rise, reaching $140 per barrel. The global financial market would become risk-averse. In this case, we may see the baht weaken further into the third quarter. However, the likelihood of this scenario has significantly decreased following the two-week ceasefire agreement, with the market giving an 86% chance that Trump will announce the end of the war by June.

Mr. Wachirawat Banchuen, Senior Financial Market Strategist at Siam Commercial Bank, added that for importers, USDTHB around 31.70-32.20 is a level to consider buying. During the ceasefire for negotiations, the market's concerns have eased, providing an opportunity to buy USDTHB. However, uncertainty remains high, and the ceasefire conditions of each party are still unclear, along with the possibility of oil prices decreasing further, which may limit the baht's ability to strengthen significantly. For exporters, USDTHB around 32.65-33.15 is a level to consider selling gradually, as the likelihood of the worst-case scenario has decreased. Therefore, the trend of the baht weakening significantly has diminished, but uncertainty remains high, and there may still be some attacks, which could cause the baht to weaken at times.

Looking back at previous wars may help indicate the direction of the financial market. In the previous Gulf War (1990-91), the war lasted more than three months and caused oil prices to double (from about $20 per barrel to $40 per barrel). Mr. Wachirawat estimates that if the U.S. and Iran fail to negotiate and the war reignites, if the Strait of Hormuz is closed for more than two months, affecting long-term oil supply, it could push Brent crude oil prices up to $130-140 per barrel, which would impact inflation trends, government bond yields, and exchange rates.

Additionally, during the 1990 war, U.S. Treasury yields decreased in less than two months, while crude oil prices took longer (about two months) to decline. The reason for the decline in yields was that the market began to worry more about the impact of the war and oil prices on the economy (growth risk) rather than the initial concerns about inflation (inflation risk). Therefore, yields that had risen due to inflation decreased because the market viewed that monetary policy might need to ease to support the economy. Moving forward, key factors to watch that could lead to a decline in bond yields include:

- Worsening real economic data. However, the latest U.S. economic data is still relatively good, including non-farm employment and retail sales, keeping bond yields stable.

- Continuously rising oil prices affecting households and businesses. In 1990, it was found that a 70% increase in oil prices led to a decrease in bond yields. If this war has a similar effect, crude oil prices around $125 per barrel could make the market more concerned about growth, potentially leading to a further decline in the 10-year yield.

- The Fed begins to signal increased concern about the economy. In 1990, the market priced in that the Fed would raise interest rates, but ultimately the Fed lowered rates instead.

Regarding interest rate outlook, the war in Iran has increased inflationary pressures globally, leading the market to price in the likelihood of interest rate hikes by central banks. Following the two-week ceasefire agreement, the market sees a 50% chance that the Fed will lower interest rates this year, while the European Central Bank (ECB) has a chance of raising rates three times, and the Bank of Japan (BOJ) has a chance of raising rates twice. Mr. Wachirawat believes that the central bank will place more weight on the impact of economic growth, thus he sees a chance for the Fed to lower rates 1-2 times in the second half of this year, while the ECB may raise rates 1-2 times due to higher inflationary pressures in Europe compared to the U.S. Meanwhile, the BOJ may raise rates 1-2 times in response to inflationary pressures and the trend of reducing monetary policy easing (normalization).

In the base case, the Bank of Thailand is expected to maintain the policy interest rate at 1.00%. If the war gradually reduces in intensity and ends within 1-2 months, it may cause Thailand's general inflation rate to rise to around 2-3%, which would still be within the Bank of Thailand's inflation target. Meanwhile, GDP this year may only grow by 1.4% (down from the previous estimate of 1.8%), leading the Bank of Thailand to maintain interest rates as is. However, in the worst-case scenario, if the war drags on into the middle of the year or longer, inflation may rise to the upper limit of the policy target (3%) or more. Nevertheless, the impact on the real economy in this case would be severe, with GDP this year potentially growing by only 1.00%, prompting the Bank of Thailand to focus more on economic issues and decide to lower the interest rate once to 0.75%.