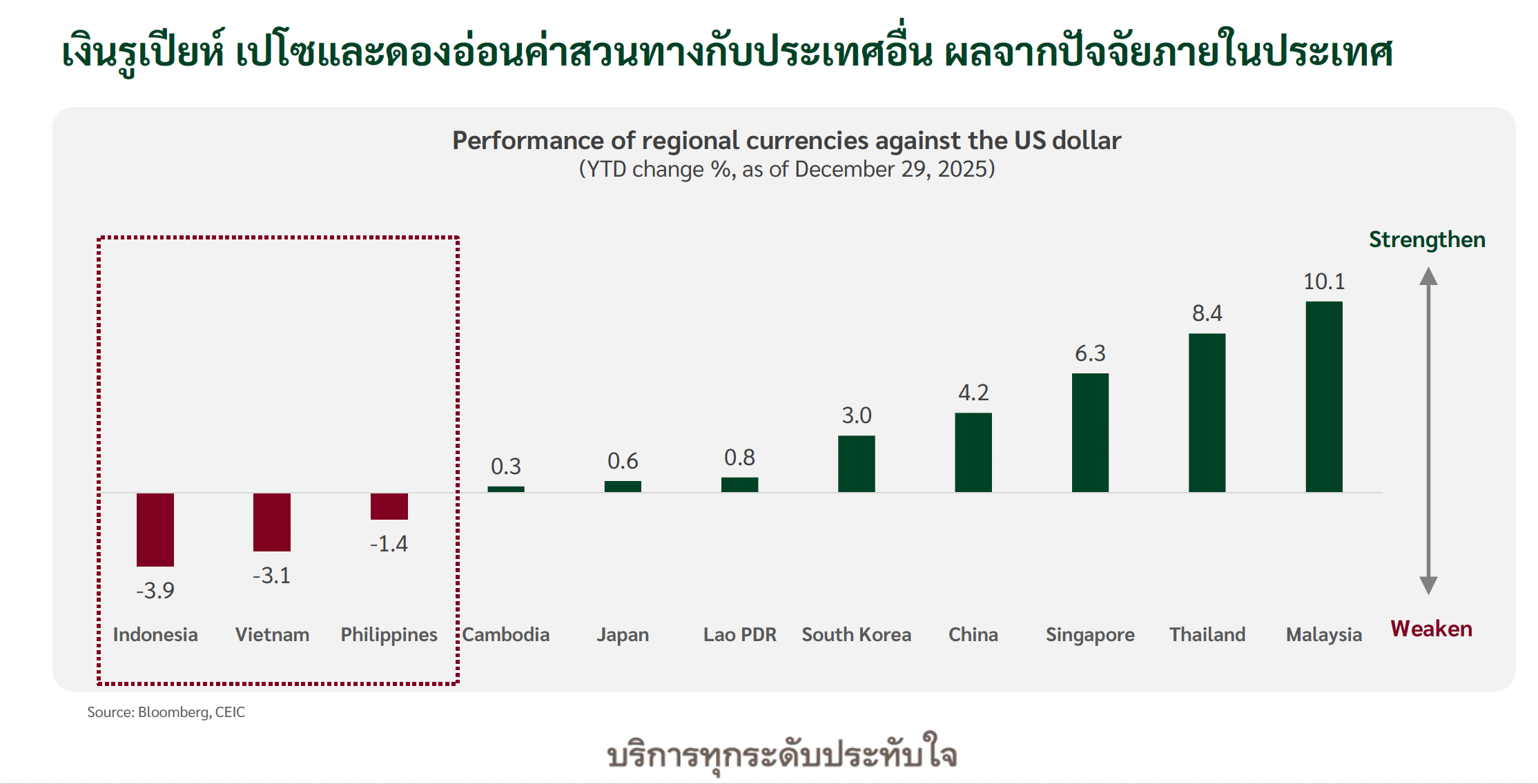

ASEAN-China Economy in 2026: Slowing Global Trade Pressures

Analytical Overview The report ASEAN–China Regional Economic Outlook January 2026 clearly indicates that the economies of East Asia and ASEAN are entering a phase of "slower growth but not recession" under pressure from trade tariffs, trade barriers, and a high economic base from the previous year, with China remaining a key variable impacting the entire region.

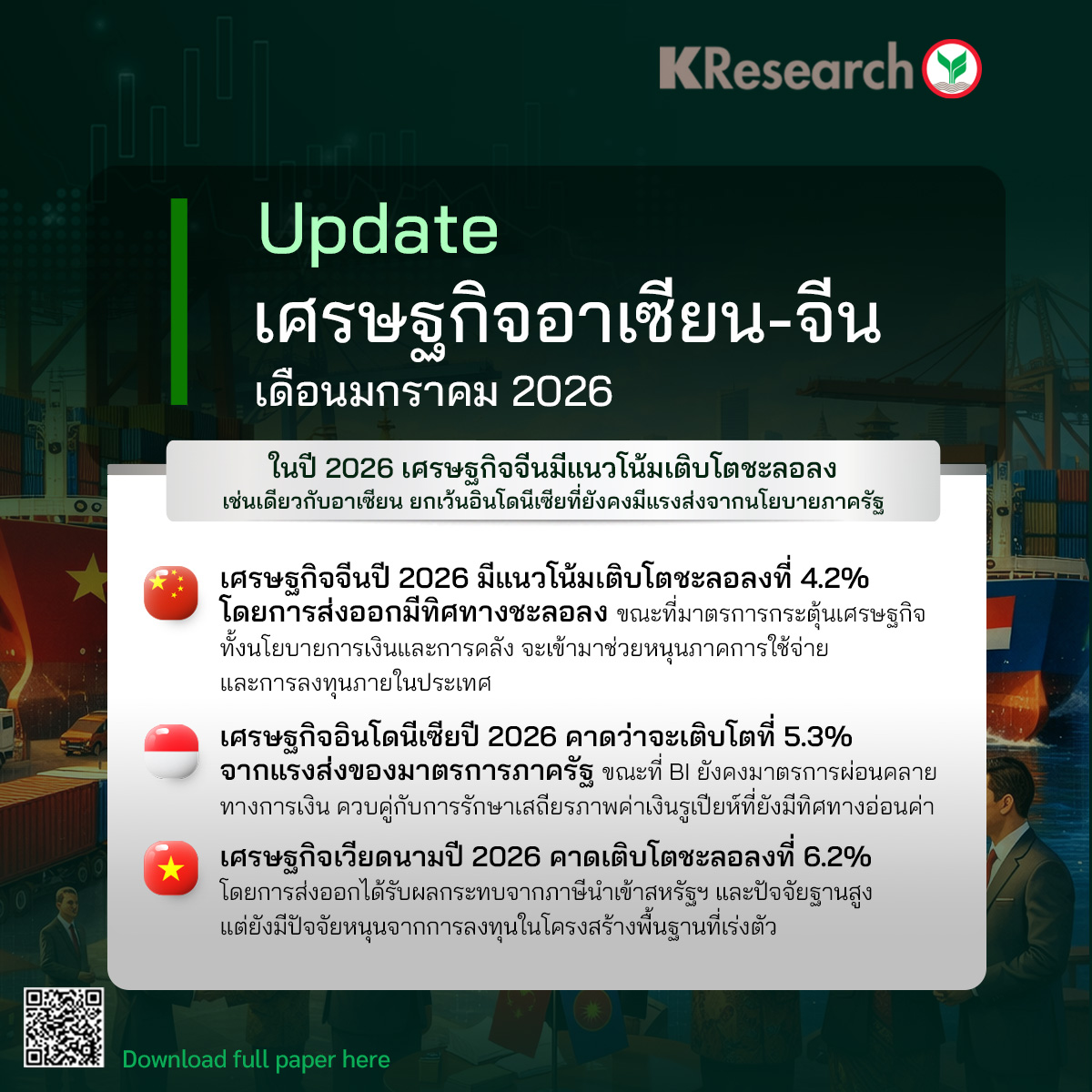

China: The Core Slowing but Supporting the Region

China: The Core Slowing but Supporting the Region

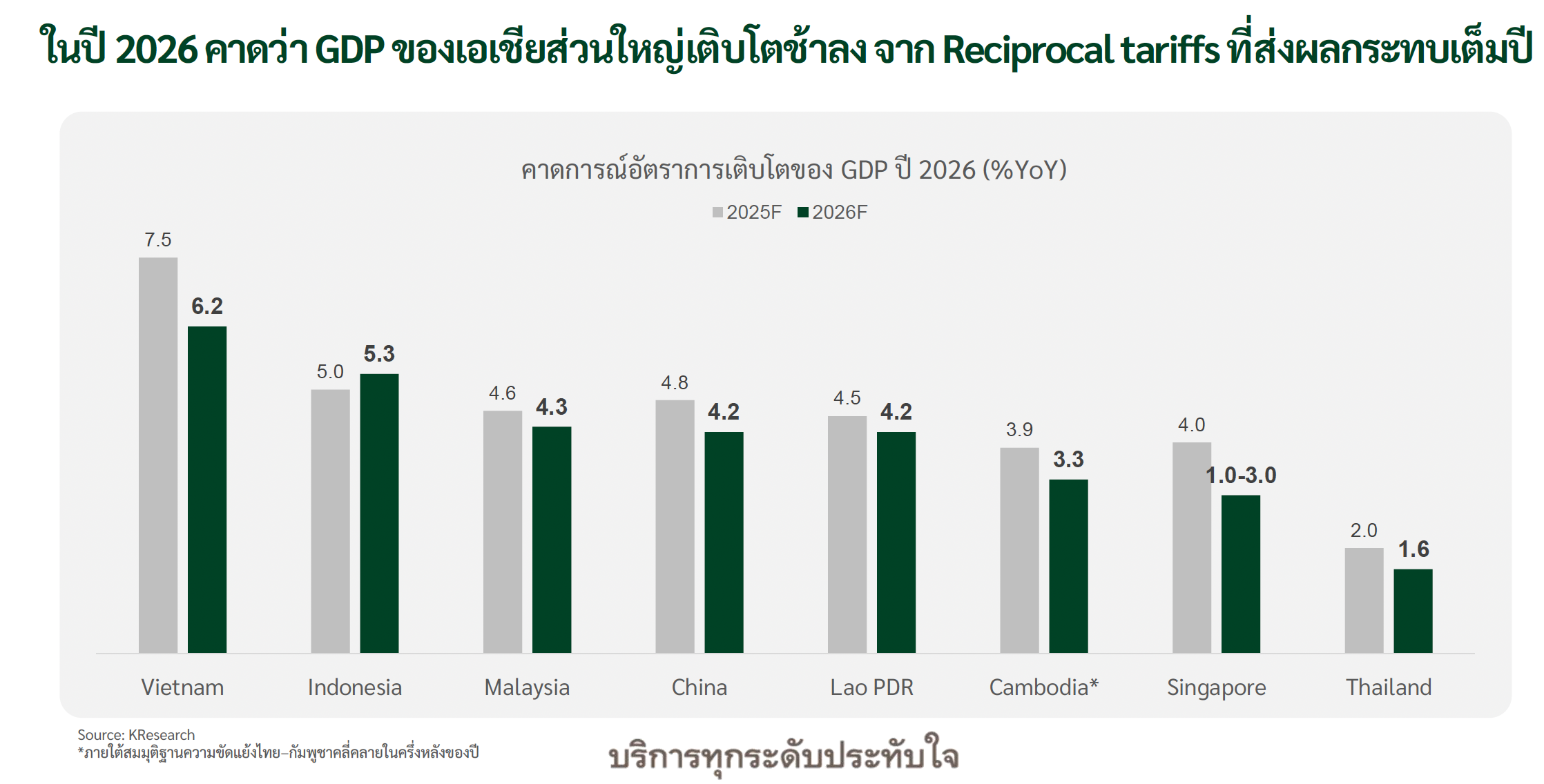

In 2026, China's GDP is expected to grow by only 4.2%, down from the previous year, primarily due to export pressures from the U.S. and the European Union, while the real estate sector remains a structural burden. However, the Chinese government is preparing to implement easing monetary policies and domestic consumption stimulus measures, such as trade-ins and welfare programs, to support domestic demand.

ASEAN: Growing at Different Paces and Drivers

-

Vietnam is expected to grow by 6.2%. Although exports are slowing due to U.S. tariffs, it benefits from over $100 billion in large infrastructure investments during 2026-2030.

-

Indonesia is projected to grow by 5.3% due to government measures and downstream investments, but must watch for off-budget fiscal risks.

-

Malaysia is expected to grow by 4.3%, driven by FDI in the ICT and electronics sectors, as well as tourism.

-

Singapore is slowing to a range of 1–3% after strong growth in 2025 from AI, with AI-related exports accounting for 46% of total exports.

-

Cambodia is expected to grow by only 3.3%, assuming border conflicts ease in the second half of the year.

-

Laos is projected to grow by 4.2%, supported by electricity exports and tourism from the Laos-China railway.

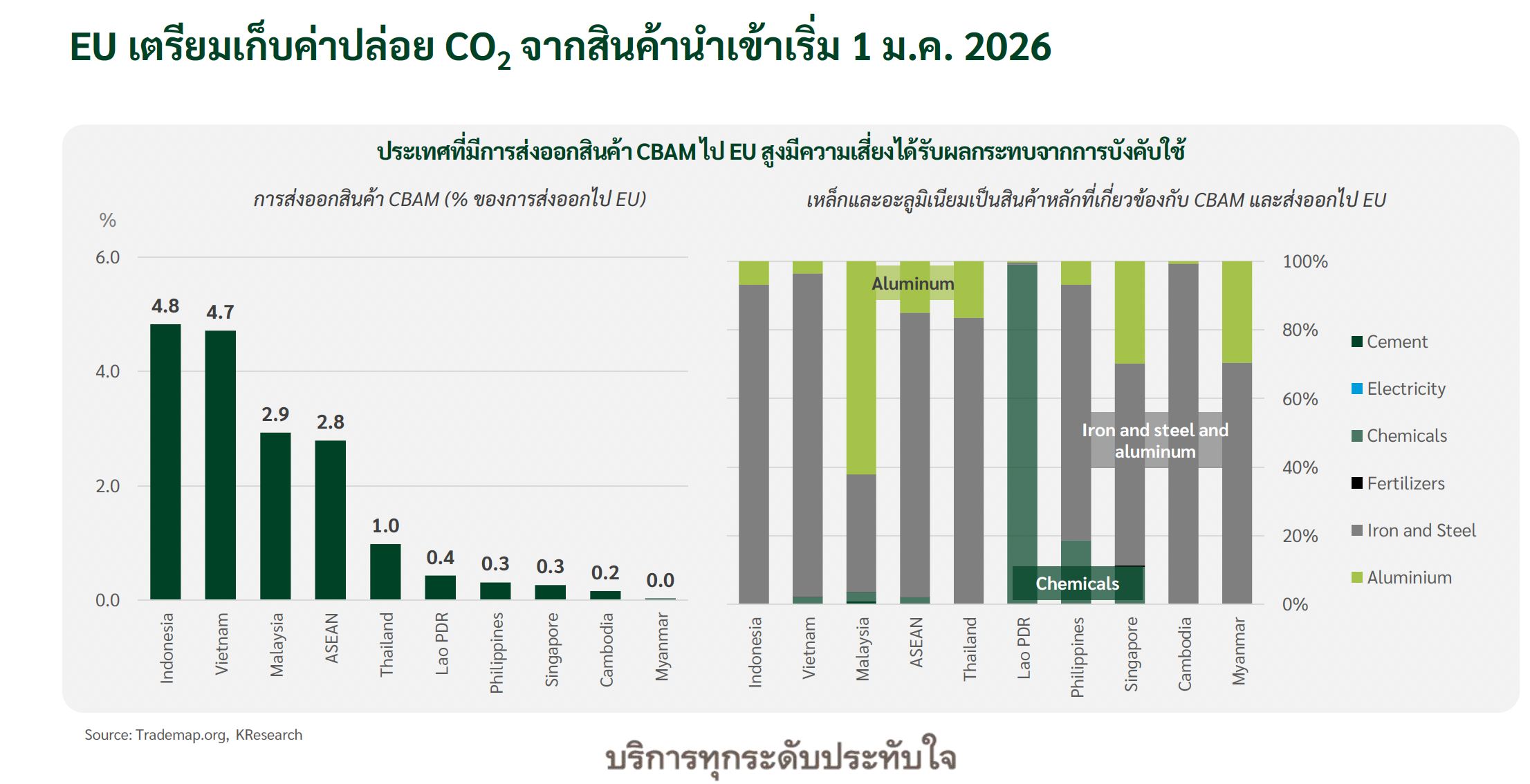

Structural Risks to Watch

2026 marks the first year the EU fully implements CBAM, impacting ASEAN countries that export significant amounts of steel and aluminum to Europe, such as Indonesia and Malaysia. Meanwhile, the "full-year Trump tariffs" will continue to pressure global trade.

Strategic Interpretation

The regional economy is shifting from "export acceleration" to "selecting quality growth." Countries that have strong domestic markets, ready infrastructure, and can quickly connect with AI, clean energy, and digital chains will have an advantage. In 2026, while the pace may slow, the direction remains structurally forward.