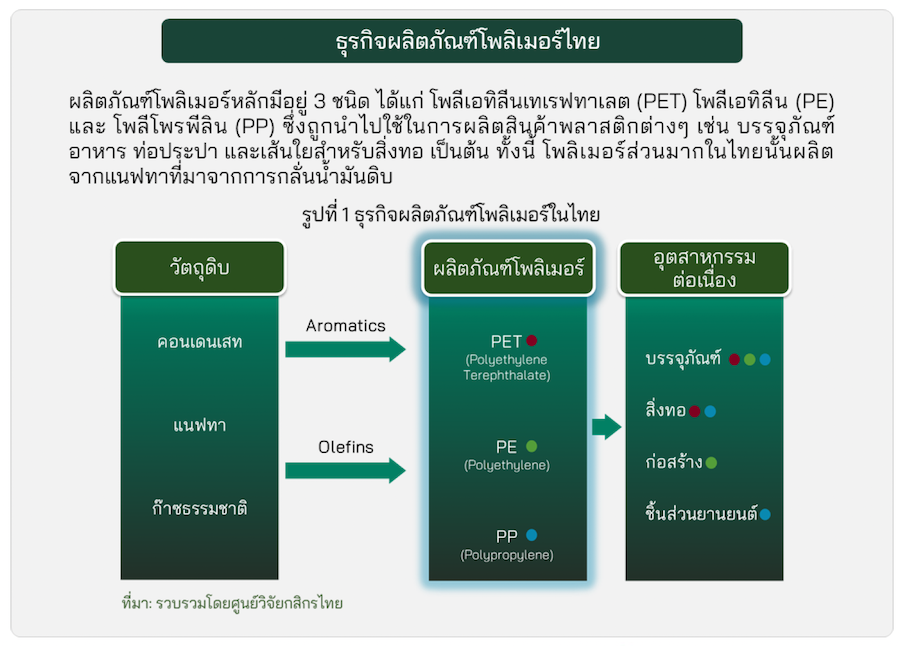

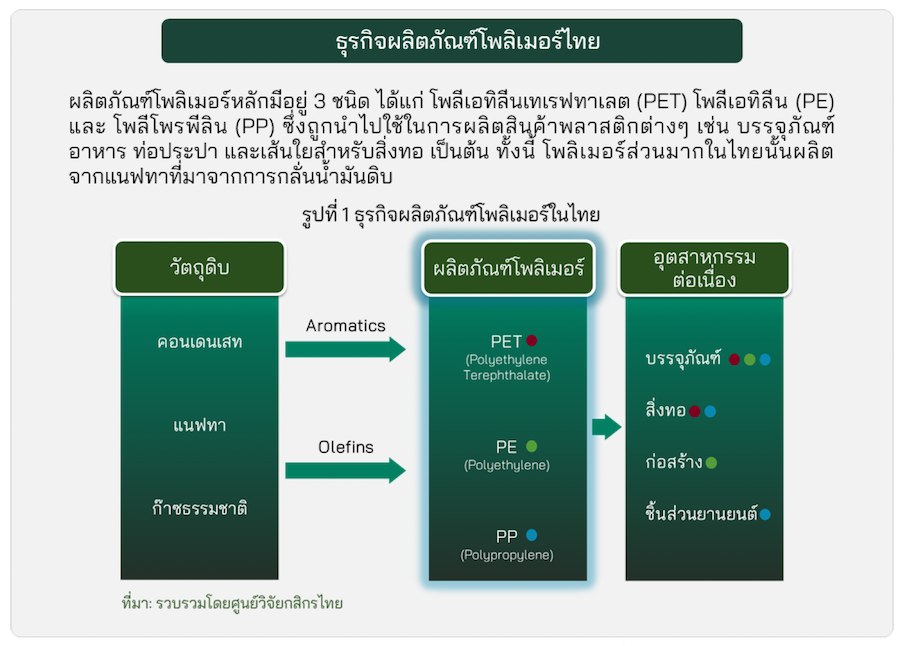

Trends in the Thai Polymer Industry

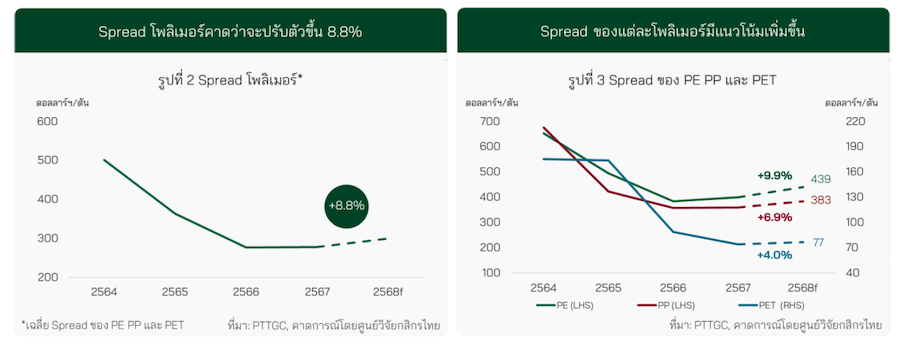

In 2025, the profits of the Thai polymer business are expected to improve, although still lower than in 2022. This is due to the spread between polymer prices and raw material costs, which, despite increasing by 8.8% following the downward trend of naphtha prices, remains 17% lower than in 2022.

Meanwhile, the demand for Thai polymers is projected to grow by 1.6% due to the expansion of plastic packaging in the food and beverage sector and an increase in sales of automotive spare parts. However, the contraction in the apparel market will limit the growth of polymer demand.

The volume of polymer exports is expected to decrease by 2.7% this year, with exports of PE/PP to China declining due to increased production capacity in China, while PET exports are also expected to drop in line with exports to the United States.

Profits in the polymer business are trending upward in 2025, but still below the levels seen in 2022.

As polymer demand is expected to increase slightly, the spread between polymer prices and raw material costs, while rising, remains 17% lower than in 2022 (Figure 2).

This year, the spreads for PE, PP, and PET are expected to increase by 9.9%, 6.9%, and 4.0%, respectively (Figure 3) due to:

The prices of raw materials, particularly naphtha, are expected to decline in line with falling Dubai crude oil prices, which are projected to decrease by 12% from 2024 to around $70 per barrel.

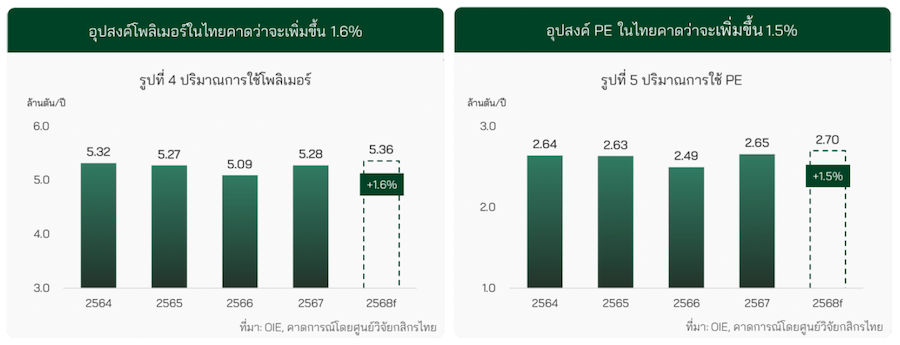

Polymer prices in Asia are not expected to drop as sharply as raw material prices due to demand support from China, which is focusing on stimulating consumption and has raised its budget deficit target to 4% of GDP to boost the economy in 2025. The demand for polymers in the Thai market is expected to grow by 1.6% in 2025 (Figure 4).

[1] Forecast as of March 2025 by Kasikorn Research Center.

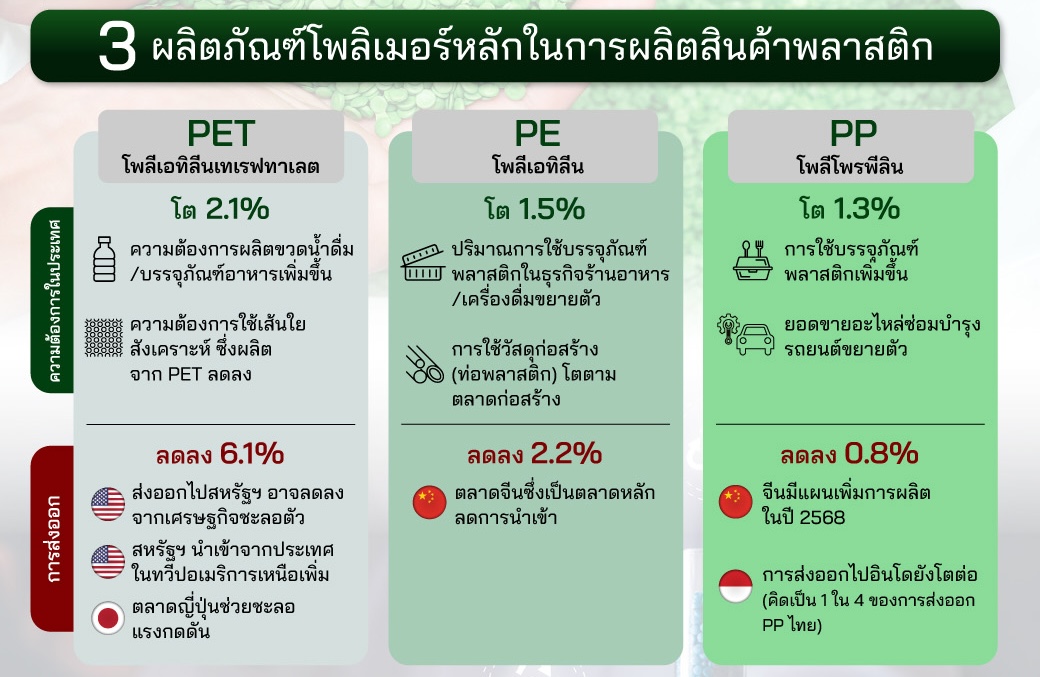

Domestic demand for PE is expected to grow by 1.5% (Figure 5).

This growth is driven by the increasing use of plastic packaging in the food and beverage sector, which is expected to expand by 4.6% this year. Additionally, the use of construction materials, such as plastic pipes, will grow in line with the construction market, particularly public sector projects that are resuming after budget disbursement delays in 2024.

[1] Source: Article on Trends in the Food and Beverage Business from Kasikorn Research Center.

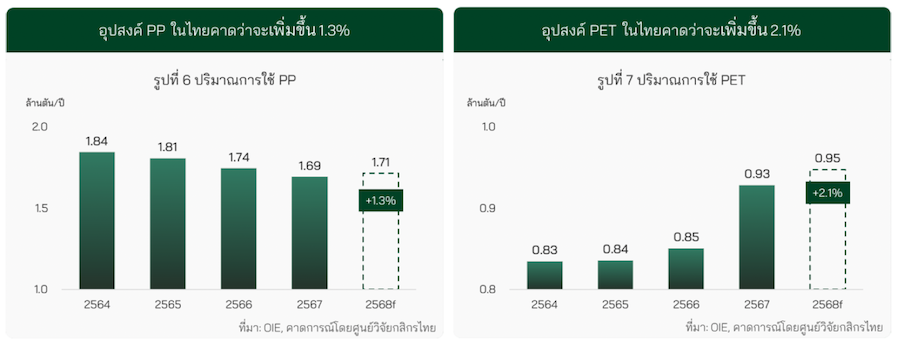

Demand for PP is expected to increase by 1.3% (Figure 6).

This growth is attributed to the rise in plastic packaging usage mentioned above, along with a projected 3.6% increase in sales of automotive spare parts in Thailand this year, driven by the growing number of registered vehicles, which currently stands at around 20 million.

Demand for PET is expected to grow by 2.1% (Figure 7).

This growth is in line with the increasing demand for PET in the production of drinking bottles and food packaging. However, it faces pressure from the declining demand for synthetic fibers made from PET, which is expected to decrease due to the contraction of the apparel market, as competition arises from affordable ready-made garments imported from China.

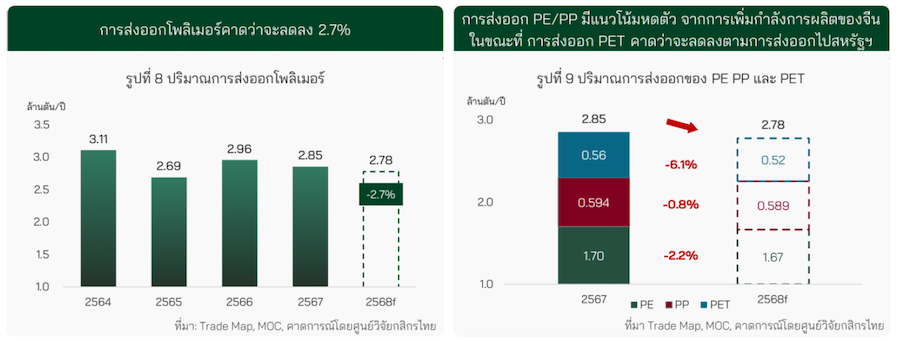

The export of Thai polymers is expected to contract by 2.7% in 2025 (Figure 8).

The export of Thai polymers is not significantly affected by the United States' imposition of reciprocal tariffs, as PET, which accounts for about one-fourth of total exports to the U.S., is exempt from these tariffs. Meanwhile, Thailand currently exports very little PE and PP to the U.S.

The export trends for each polymer product can be analyzed as follows (Figure 9).

[1] Source: Article on Trends in the Thai Automotive Parts Industry from Kasikorn Research Center.

[2] PET (HS Code: 390761 and 390769) is one of the products listed in Annex II, which is exempt from reciprocal tariffs.

The volume of PE exports is expected to decrease by 2.2% because China, the top market for Thai PE exports, is likely to reduce its PE imports due to plans to increase its PE production capacity by about 5 million tons and 6.5 million tons this year and next year, respectively.

The volume of PP exports is expected to decline by 0.8% as China plans to increase its PP production capacity by 7.1 million tons in 2025. However, PP exports are not expected to drop significantly this year, as exports to Indonesia continue to show growth after the Indonesian government lifted its previous restrictions on PP imports. Currently, Thailand's PP exports to Indonesia account for about one-fourth of total PP exports, similar to the volume exported to China.

The volume of PET exports is expected to contract by 6.1% due to a decline in PET exports to the U.S., resulting from the slowing U.S. economy and the U.S. shifting to import PET from North American countries like Mexico. However, the Japanese market remains a significant supporting factor, as the demand for plastic bottle packaging in Japan's beverage industry continues to grow, helping to mitigate some pressure on Thai PET exports.

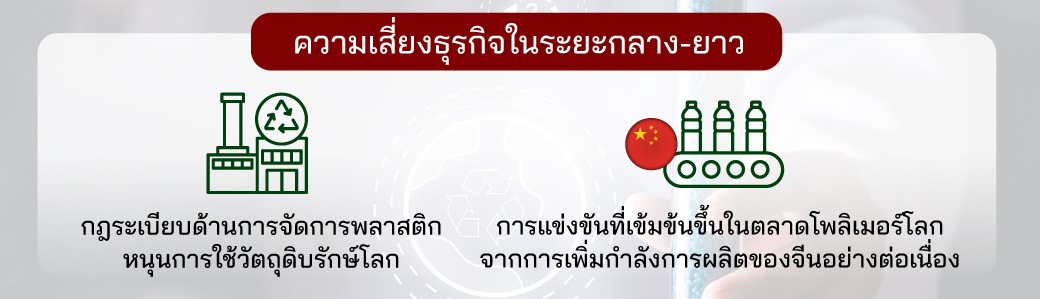

Risks for the Thai polymer industry in the medium to long term:

The introduction of plastic management regulations may push for the use of environmentally friendly raw materials. Thailand's Phase 2 Plastic Waste Management Plan (2023 - 2027) mandates that producers of products using plastic as a raw material must take responsibility for collecting and managing plastic waste, which may lead manufacturers to increasingly adopt environmentally friendly materials, including bioplastics and recycled plastics.

Intensifying competition in the global polymer market, driven by China's continuous increase in production capacity, has resulted in an average overall production capacity growth of 6% from 2021 to 2025, while global demand is growing at an average of only 3%. This has led to an oversupply situation, putting pressure on global polymer prices.