Overview of the Factory and Warehouse Market in the First Half of 2024

In the second quarter of 2024, the Thai economy grew by 2.3% year-on-year, recovering from a contraction of 1.6% in the first quarter, primarily driven by the recovery of the industrial and service sectors. The GDP for the first quarter of 2024 expanded by 1.9%.

In the second quarter of 2024, private consumption expenditure increased by 4.0%, mainly due to higher spending on semi-durable goods, while spending on non-durable goods and services grew at a slower pace. Government consumption expenditure rose by 0.3% due to increases in employee wages and marketing productivity. Total investment contracted for the third consecutive quarter by 6.2%, with private investment decreasing by 6.8% due to an 8.1% drop in machinery and equipment investment. Additionally, public investment fell by 4.3%, with government investment down by 12.8%. Exports of goods and services grew by 4.5% quarter-on-quarter, driven by a 2.7% increase in export value and a 1.7% rise in export prices, while imports expanded by 1.2%, despite a decrease in import value.

In terms of production, the agricultural, forestry, and fishing sectors decreased by 1.1% after a 2.7% decline in the previous quarter, primarily due to reduced agricultural output. However, there was some good news with increased production of sugarcane and palm oil. The manufacturing sector showed signs of recovery, growing slightly by 0.2% after contracting by 2.9% in the previous quarter, supported by a 2.5% increase in domestic industries. Nevertheless, export-oriented industries contracted by 1.5%, with sectors reliant on exports, such as automotive and electronics, also experiencing declines.

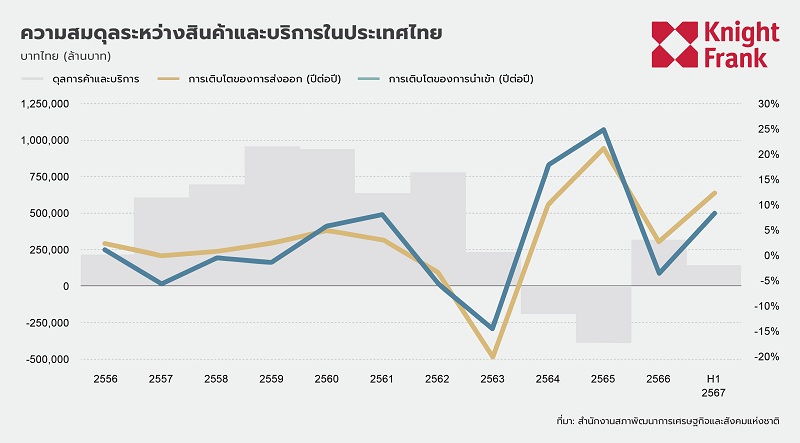

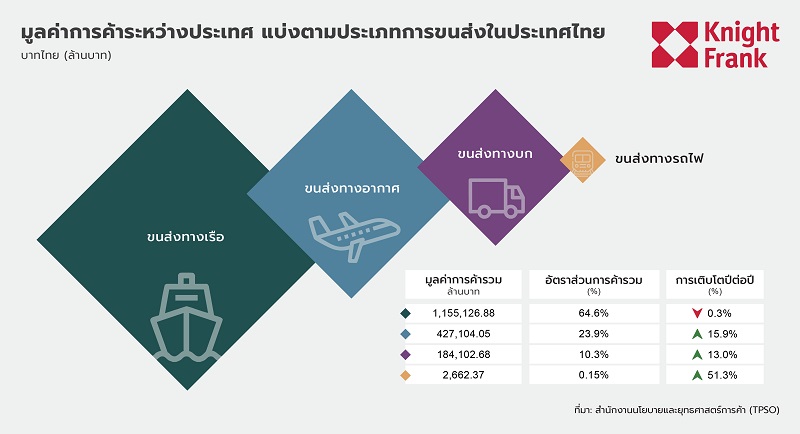

Meanwhile, Thailand's international trade continues to rely heavily on water transport, accounting for 64.6% of total trade, despite a 3.3% year-on-year decrease. Air transport accounted for 23.9%, boosted by high-value goods such as electronics, while land transport made up 10.3%, increasing by 13.0% year-on-year. Rail transport accounted for 0.15%, but saw the highest growth at 51.3% year-on-year.

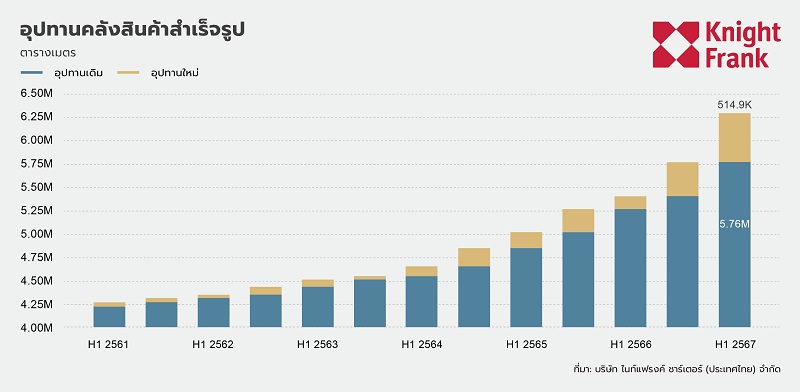

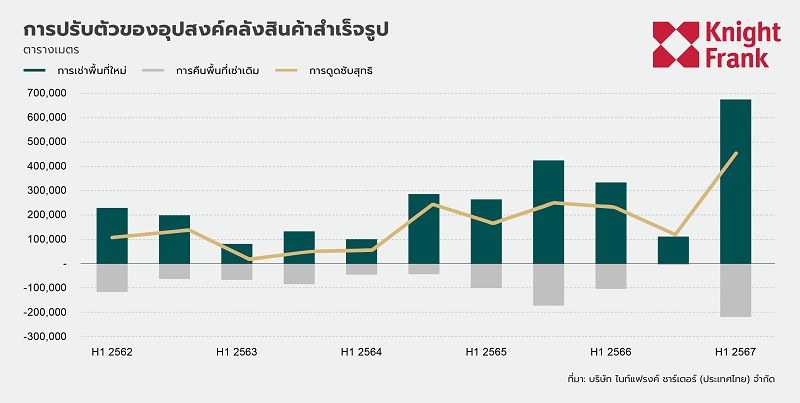

The total supply of ready-built warehouses increased by 8.9% half-on-half, reaching 6.27 million square meters in the first quarter of 2024. New supply accounted for 9% of the total supply added during this period, driven by several projects primarily in Chonburi, Samut Prakan, and Pathum Thani, alongside the expansion of existing industrial estates.

Distribution of Supply

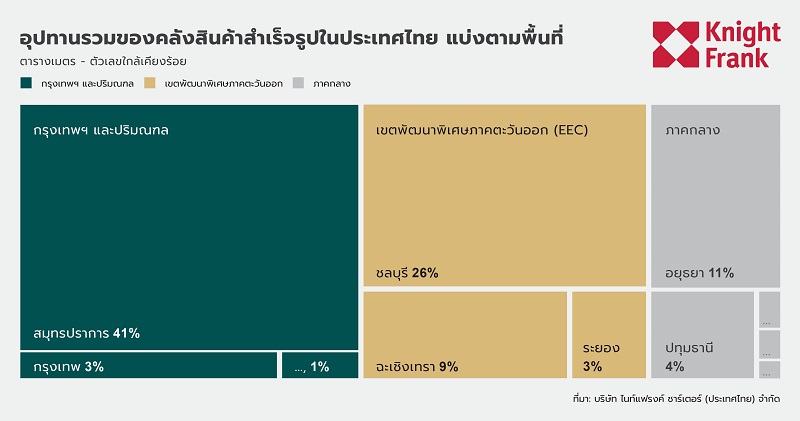

The Bangkok Metropolitan Region and its vicinity continue to hold the largest market share, increasing by 9.9% from the previous half-year to reach 2.8 million square meters, accounting for 45% of total warehouse supply, with 41% located in Samut Prakan province, reinforcing its status as a major logistics hub. The Eastern Seaboard holds the second-largest share, with an area of 2.4 million square meters, representing 38% of total warehouse supply. Chonburi remains the leader in the Eastern Economic Corridor (EEC) with a 26% share, followed by Chachoengsao at 9% and Rayong at 3%. The central region accounts for 16% of the total market share, with approximately 1 million square meters of net leased area, showing moderate supply growth of 5.7% half-on-half. Ayutthaya accounts for 11% of the central region's share, followed by Pathum Thani at 4%. These figures reflect ongoing expansion despite a lack of significant developments in other areas.

Future Supply

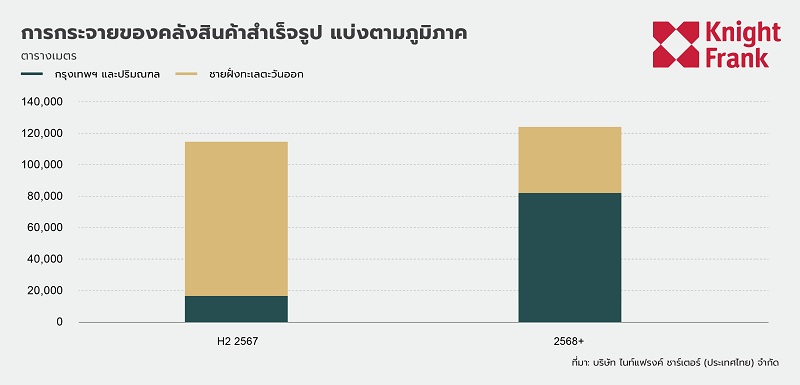

The total future rental space supply stands at 239,000 square meters, comprising 115,000 square meters in the second half of 2024 and an additional 124,000 square meters from 2025 onwards, reflecting ongoing expansion and development. Of the future supply, 59% is located in the Eastern Seaboard, while the Bangkok Metropolitan Region accounts for 41%. This trend indicates continued growth in both regions, with the Eastern Seaboard remaining a key strategic point for future development due to its geographical location and cost advantages.

Demand

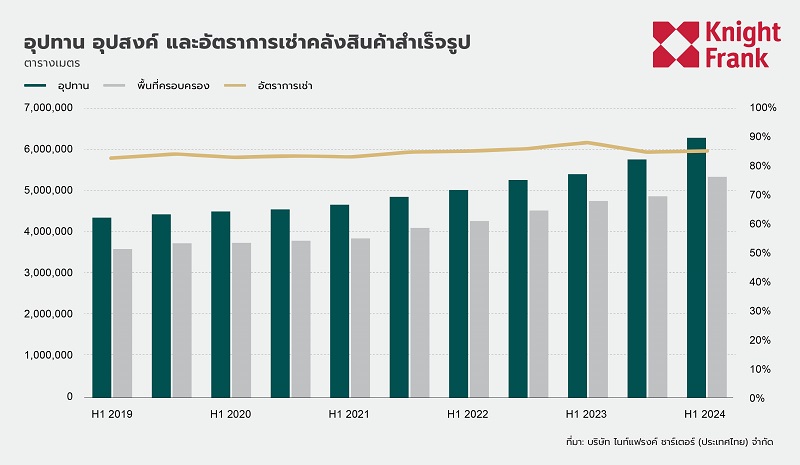

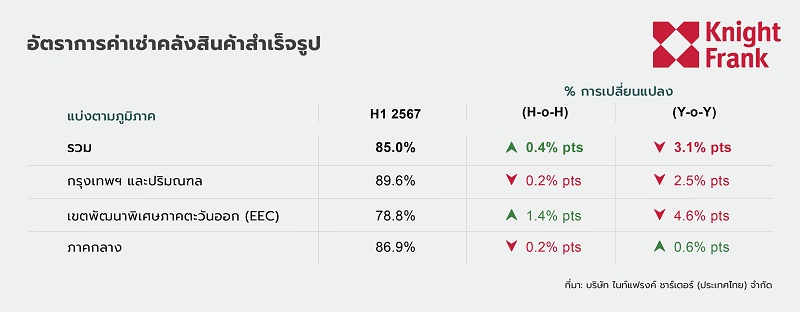

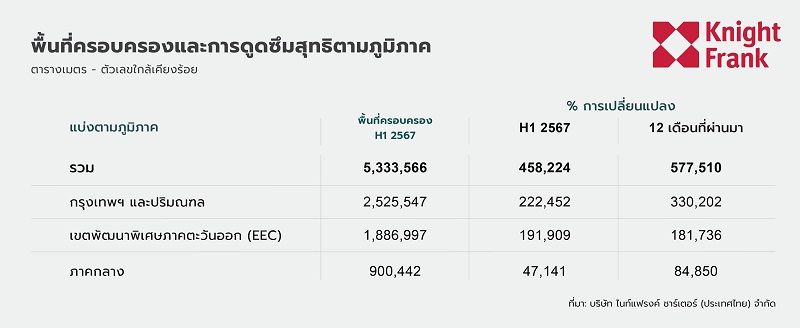

In the first half of 2024, the warehouse market experienced significant growth in both supply and occupancy, with supply exceeding 6.27 million square meters and occupied space increasing to 5.33 million square meters, reflecting strong demand across the market. However, the occupancy rate slightly decreased to 85.0%, lower than the previous year due to the influx of new supply.

The market continues to absorb new supply effectively, driven by strong demand from key industries such as e-commerce, automotive, and electronics, resulting in robust and sustained growth in the logistics real estate market. Meanwhile, the automotive industry is rapidly expanding electric vehicle production and related infrastructure, aligning with global sustainability initiatives. Conversely, demand in the apparel, chemicals, and construction materials industries has decreased. Investors from China, the Netherlands, South Korea, Japan, and Hong Kong have shown strong confidence in Thailand's logistics industry. In addition to financial support, these investors are bringing advanced technology and innovative warehouse solutions to revolutionize the industry, particularly in transportation and cargo handling, which constitutes a significant portion of foreign investment in the logistics market.

As a result of this demand, occupancy in the first half of 2024 surpassed 600,000 square meters, reaching the highest level in recent years. This rapid increase is driven by the influx of new supply, particularly developments designed to meet the specific needs of growing industries. This swift occupancy underscores the market's ability to efficiently accommodate new stock, demonstrating the resilience and growth potential of Thailand's logistics real estate sector.

In the Bangkok Metropolitan Region and its vicinity (BMR), the occupancy rate stands at 89.6%, slightly down by 0.2% half-on-half and down 2.5% year-on-year. This region remains the leader with the highest occupied area of 2.5 million square meters due to the ongoing demand from the e-commerce and logistics industries, and it recorded the highest net absorption of 222,452 square meters in the first half of 2024.

In the first half of 2024, the eastern region saw an increase in supply, resulting in significant warehouse space absorption of 191,909 square meters, reflecting strong demand. The rental rate in this region increased by 1.4 percentage points compared to the previous half-year, reaching 78.8%, primarily driven by the increase in new supply. This additional space positions the Eastern Economic Corridor (EEC) to support future growth and demand in the logistics sector.

Meanwhile, the central region showed stable performance, with an occupancy rate of 86.9%, down 0.2% half-on-half but up 0.6% year-on-year. Net absorption was 47,141 square meters in the first half of 2024, with a total occupied area of 900,442 square meters, indicating a balanced shift in demand and supply.

Although the occupancy rate has slightly decreased, the market remains fundamentally strong, with the increasing supply continuing to be absorbed, reflecting sustainable demand across various industries. The slight decline in occupancy is not a sign of weakened demand but rather a result of faster supply expansion.

Rental Rates

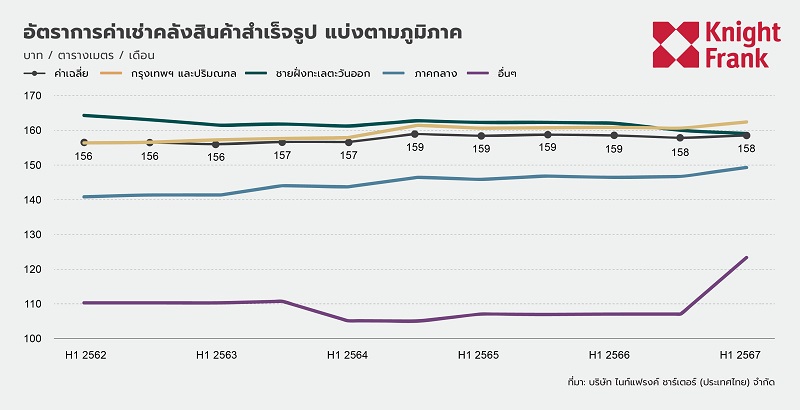

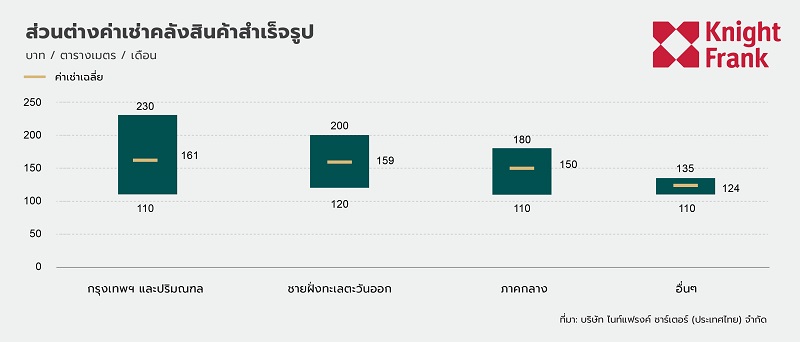

The average rental price for ready-built warehouses remained stable at 158 THB/sq.m/month in the first half of 2024, with some properties reducing rents to clear vacant units, while the average rent for new warehouses is around 160 THB/sq.m/month.

The average rental prices across all areas remained stable, with the Bangkok Metropolitan Region and its vicinity (BMR) slightly increasing to 161 THB, the Eastern Seaboard (EEC) at 159 THB, the central region at 150 THB, and other regions at 124 THB. The 'other' regions saw the highest rental increase, with minimum rents rising from 100 THB to 110 THB, while maximum rents in BMR increased from 200 THB to 230 THB. In contrast, the Eastern Seaboard and central regions maintained maximum rents at 200 THB and 180 THB, respectively.

Market Overview and Trends

The logistics and warehouse market in the first half of 2024 experienced significant growth, driven by economic momentum from the previous year. Total supply increased by 8.9% half-on-half, reflecting strong confidence among operators in this industry, particularly in the Bangkok Metropolitan Region (BMR) and the Eastern Seaboard, which continue to lead in logistics infrastructure. The occupancy rate remains strong at 85.0%, slightly down from previous levels but still reflecting robust demand due to a high net absorption of 458,224 square meters.

Key industries such as e-commerce, automotive, and electronics play a crucial role in driving demand, particularly as e-commerce continues to grow strongly, fueled by the need for last-mile delivery. At the same time, the automotive industry has an increasing demand for warehouse space, driven by the expansion of production bases and electric vehicle infrastructure aligned with global sustainability principles.

Air transport increased by 15.9% year-on-year, driven by the growth of high-value industries such as electronics and medical equipment, while land transport also plays a significant role in the logistics industry, supported by cross-border trade with China and Malaysia. Rail transport is becoming an increasingly popular option, rising by 51.3% year-on-year, indicating potential for future cargo movement, especially in the Eastern Economic Corridor (EEC).

Regarding future supply, particularly in the Eastern Seaboard, there is ongoing confidence in the growth potential of this industry. However, operators are closely monitoring market absorption rates to avoid periods of vacancy. Rental rates remain stable at 158 THB/sq.m, with BMR having the highest rental rate at 230 THB/sq.m for premium properties. In the second half of 2024, the logistics real estate market is expected to remain competitive, with sustainable demand from various industries such as e-commerce, automotive, and electronics, alongside the rise of automated warehouse systems and flexible solutions.