Analysts Predict Omicron May Slow Thailand's Economic Recovery – Concerns Over Inflation

“COVID-19 Variant Omicron” has spread to many areas around the world, with preliminary data indicating that the Omicron variant can spread faster than other strains, resulting in the highest number of COVID-19 infections globally since the pandemic began. However, the rates of severe illness and death appear to be lower than those of previous variants. If the outbreak continues to escalate, it could put pressure on the healthcare systems of various countries.

This situation has led analysts in Thailand to comment that “Omicron” may cause Thailand's economy to recover more slowly than previously anticipated, and could also lead to an increase in inflation rates during the first quarter of the year.

“Krungsri Research” states that the economy in the early part of the year faces challenges from the Omicron outbreak, affecting the continuity of recovery. The latest economic indicators from November 2021 reflect an overall improvement in nearly all sectors, with exports growing significantly (+23.7% YoY) due to recovering demand from trading partners.

Meanwhile, in the tourism sector, the number of foreign tourists has nearly reached 100,000 since the government reopened the country to tourists under the Test & Go measures starting November 1. Private consumption continues to recover (+0.9% MoM_sa) as the domestic outbreak situation improves and vaccination rates increase, boosting economic activities and consumer confidence, similar to private investment (+4.3%) benefiting from recovering demand both domestically and internationally.

In a worst-case scenario, if booster vaccines cannot prevent infections, it could lead to a peak of approximately 32,000 daily infections by mid-February and up to 300 daily deaths. Krungsri Research estimates that the impact on both tourism economic activities and domestic economic activities (which collectively represent GDP) is expected to decrease by 3.0%. However, this forecast does not include other additional factors, such as the positive effects of economic stimulus measures (which may not significantly reduce overall GDP from previous predictions).

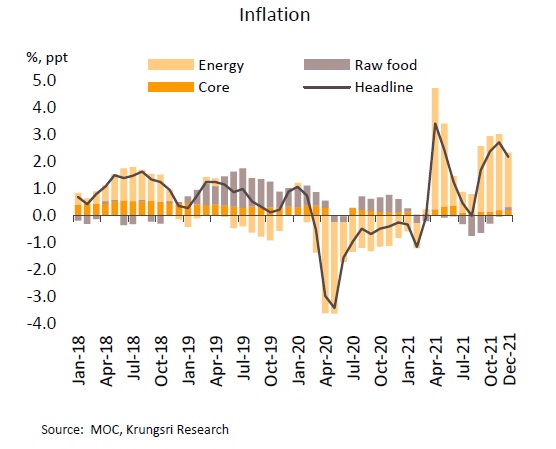

Regarding general inflation in December, it slightly slowed down but is still expected to rise in the first quarter. The general inflation rate in December was 2.17% YoY, down from 2.71% in November, primarily due to measures to cap diesel prices, while prices of fresh food items rose slightly, following an increase in pork prices. The core inflation rate (excluding fresh food and energy) remained at 0.29% as in the previous month. For 2021, the average general inflation and core inflation rates were 1.23% and 0.23%, compared to -0.85% and 0.29% in 2020, respectively.

Overall, inflation is expected to continue rising and reach a peak close to 3% in the first quarter of 2022 before gradually slowing back down to near the lower end of the inflation target range by the end of the year, partly due to a very low base in the first quarter of 2021 and rising global commodity prices, especially crude oil. However, the pass-through of costs to consumer prices may still be limited due to the fragile recovery of the Thai economy from the COVID-19 outbreak caused by the Omicron variant. For the entire year of 2022, the average general inflation rate is expected to be around 1.5%.

On the side of Economic Intelligence Center (EIC) of Siam Commercial Bank commented that the spread of the Omicron variant may lead to a slower-than-expected global economic recovery in the first quarter of this year. However, the outbreak situation is expected to begin to ease, and the global economy will gradually improve from the second quarter onwards, following a sufficient rollout of booster vaccinations and the distribution of new vaccine formulations that can control the outbreak.

It is estimated that the global economy is likely to expand at a slower rate of about 0.3-0.4% compared to before the Omicron outbreak, leading to an expected global economic growth of around 4.1% in 2022, with emerging markets (EMs) likely to be more affected by the outbreak due to lower vaccination rates than the global average, a high dependence on the tourism sector, and limited capacity for monetary and fiscal policy.

The impact on global inflation remains highly uncertain, as inflation rates in the services sector and some commodities are likely to decrease due to reduced demand for out-of-home spending, while inflation for durable goods may rise due to decreased supply and potentially increased transportation costs, following worsening supply chain bottlenecks. Additionally, concerns over new virus infections may increase pressure on the already tight labor shortage, leading to higher wage levels.

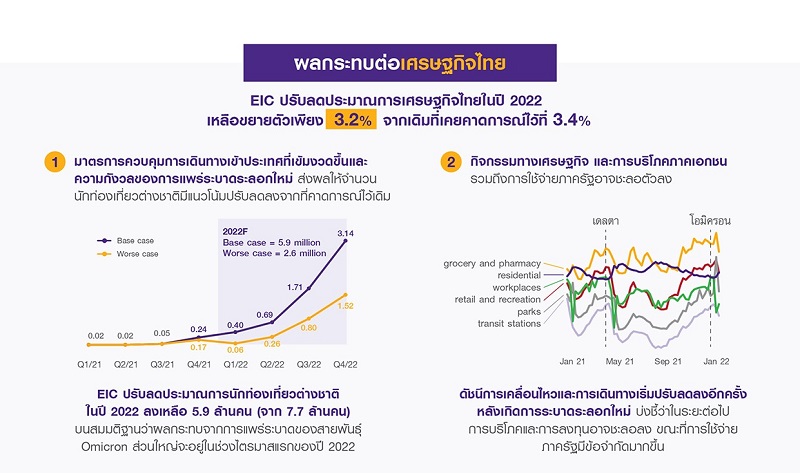

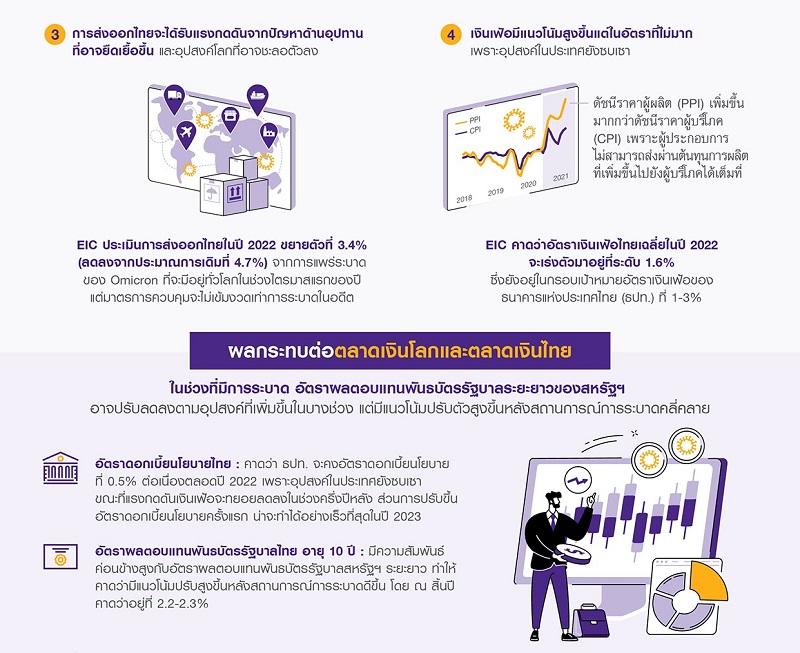

Regarding the impact on the Thai economy, it is expected that the spread of the Omicron variant will affect the recovery of the Thai economy in the first quarter of this year, primarily through the tourism and export sectors, as well as a slowdown in economic activities. EIC has revised down its forecast for foreign tourists in 2022 to 5.9 million (from 7.7 million) and reduced the expected growth rate of Thai exports in 2022 to 3.4% (from 4.7%).

This leads to an expectation that the Thai economy in 2022 will grow by only 3.2% down from the previous forecast of3.4%. However, the uncertainty surrounding the new wave of the outbreak remains high, with factors to watch that could impact the economy including 1) the level of outbreak and severity of the Omicron variant, and 2) government measures to control the outbreak. The impact on Thai inflation is expected to be limited, as weak domestic demand prevents producers from passing on higher costs to consumers.

Regarding the impact on government bond yields, during the ongoing spread of the Omicron variant globally, investors may seek to hold safe assets more, resulting in a decrease in the long-term U.S. government bond yield (10-year) due to increased demand at certain times, which will also affect the bond yields of other countries, including Thailand. However, in the future, after the outbreak situation improves from the second quarter of this year, long-term government bond yields are expected to rise again, following economic recovery, a tightening labor market, and a trend towards tighter monetary policy to control inflation. For Thai long-term government bond yields, which are relatively closely correlated with U.S. long-term government bond yields, an increase is also expected after the outbreak situation improves.

In the Thai financial market, it has been observed that capital flows tend to exit the Thai capital market during periods when the outbreak situation becomes severe and reports of infections in Thailand emerge. However, the outflow of funds is not expected to be severe compared to other emerging markets, as Thailand still maintains strong external stability. As for the Thai baht, EIC expects it to appreciate slightly by the end of 2022, following a reduction in the current account deficit and a gradual recovery of the Thai economy.