Unlocking LTV to Stimulate the Housing Market

By Kanit Amaskul, Krungthai COMPASS

Key Highlights

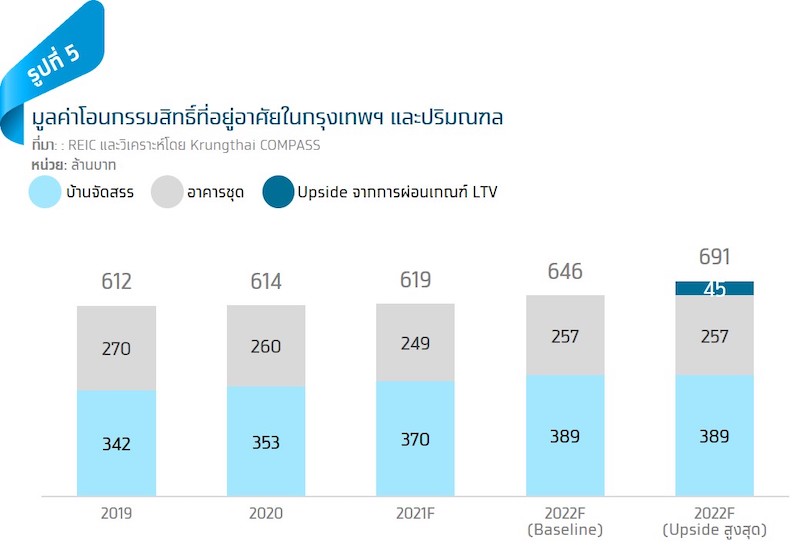

- Krungthai COMPASS predicts that the relaxation of the LTV regulations could stimulate the housing market value in Bangkok and its vicinity by approximately 45 billion baht, representing a maximum upside of 7%. This would lead to an increase in the value of property transfers in Bangkok and its vicinity for 2022, rising from 646 billion baht in the baseline scenario to around 691 billion baht. However, the high level of household debt remains a significant pressure factor for consumers seeking to purchase homes, potentially resulting in a lower upside than estimated.

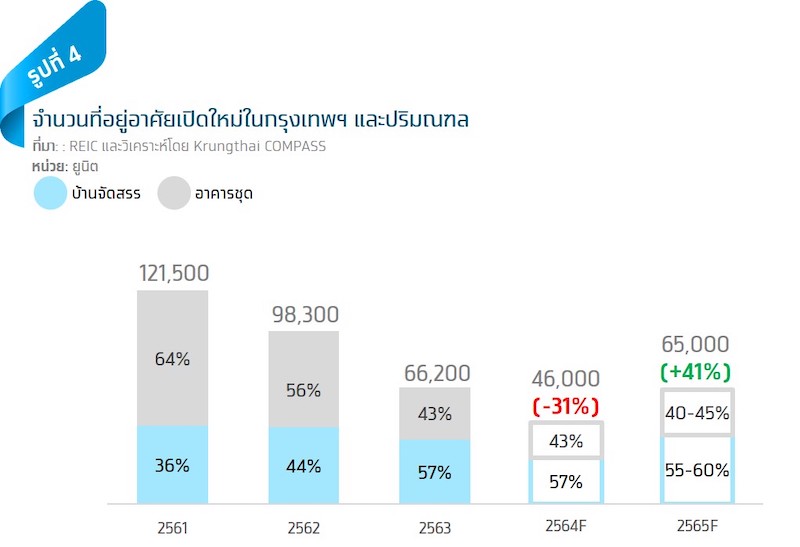

- Developer confidence is expected to rise due to the relaxation of LTV regulations, which is a positive continuation from the news regarding measures to stimulate foreign property buyers. It is anticipated that this increased confidence will lead developers to invest in more new projects. We expect new unit launches in Bangkok and its vicinity in 2022 to grow by 41% YoY to 65,000 units, with 55-60% of new units focusing on completed housing projects within the year to maximize consumer benefits from the relaxed LTV criteria.

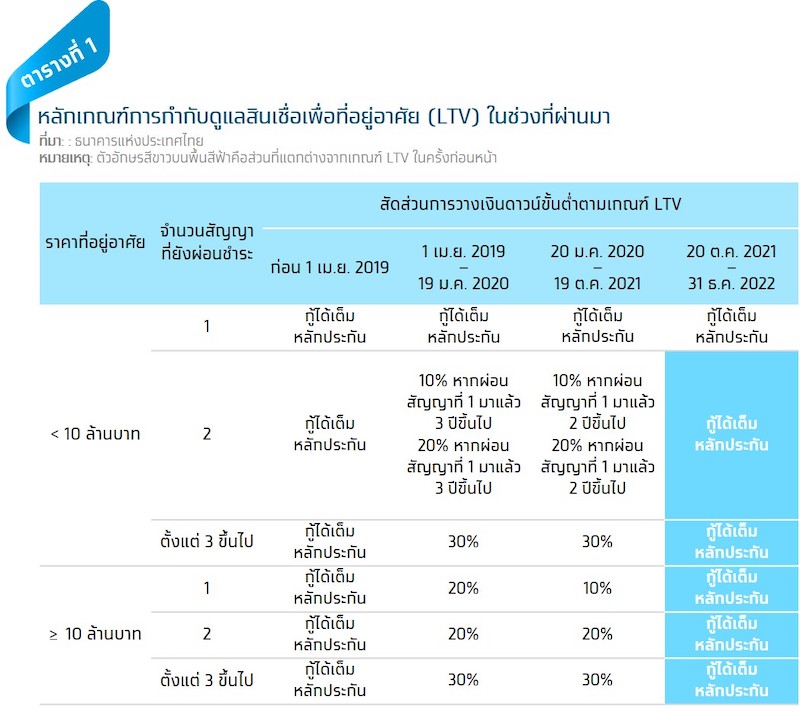

On October 21, 2021, the Bank of Thailand announced measures to relax the regulations governing housing loans and related loans (LTV), allowing homebuyers to borrow the full collateral amount for all contracts temporarily. The key aspect of this LTV relaxation is setting the loan-to-value (LTV) ratio ceiling at 100% for housing loans valued at 10 million baht from the second contract onward, and for properties valued at 10 million baht and above from the first contract onward. This allows homebuyers to borrow the full collateral value, as opposed to the previous requirement of a 10-30% down payment (see Table 1). However, the Bank of Thailand stated that this LTV relaxation will only be temporarily effective for loan contracts signed from October 20, 2021, to December 31, 2022.

Krungthai COMPASS believes that the primary reason for the Bank of Thailand's decision to relax the LTV is that the current housing market is facing negative factors:

1) LTV criteria

2) The COVID-19 pandemic has significantly impacted the performance of housing developers compared to previous periods.

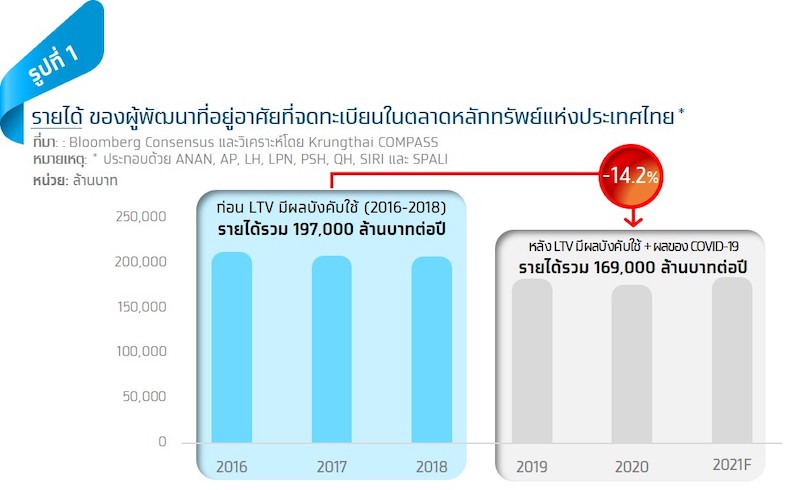

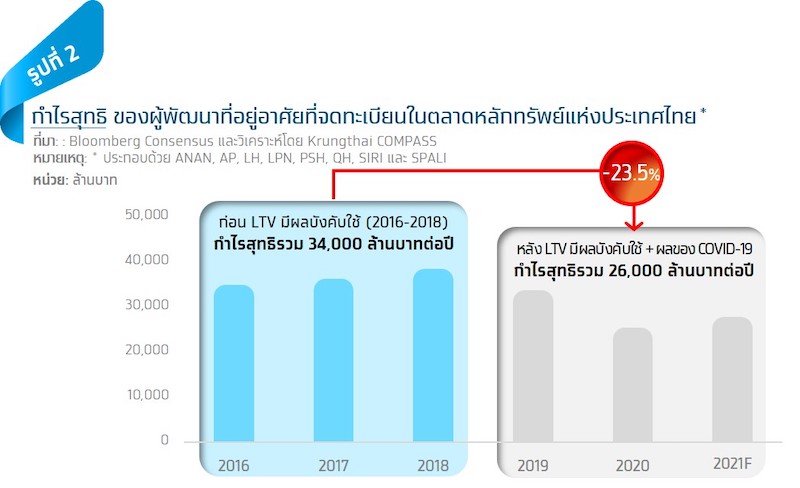

This is reflected in the performance of housing developers listed on the stock exchange, which remains significantly below historical levels, with total revenue decreasing by 14.2% from 197 billion baht per year during 2016-2018 to 169 billion baht per year during 2019-2021F (Figure 1). Similarly, net profit has dropped by 23.5% from 34 billion baht per year to 26 billion baht per year during the same period.

Krungthai COMPASS initially assesses that the relaxation of LTV criteria could impact the housing market in two key areas:

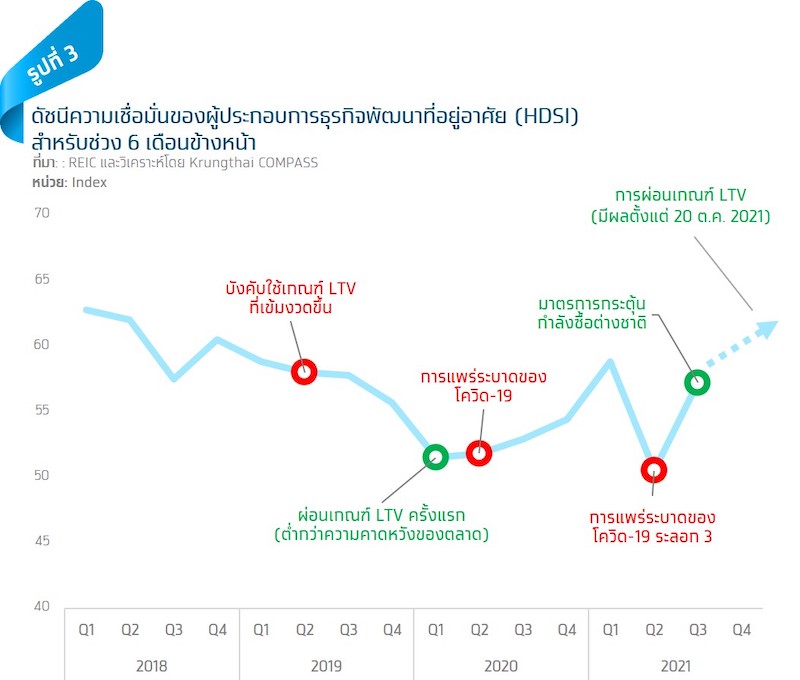

Issue 1: “Market sentiment is likely to improve.” If we consider the Housing Developer Sentiment Index (HDSI) for the next six months, we see that the index has risen from 50.5 points in Q2/2021 to 57.2 points in Q3/2021, driven by news of measures to stimulate foreign property buyers. The relaxation of LTV criteria is expected to further enhance developers' confidence in Q4/2021 (Figure 3).

Increased confidence among housing developers will promote more economic activity in the real estate sector, especially in terms of new project investments, which will have positive ripple effects on businesses within the housing development value chain, including construction, building materials production and distribution, as well as furniture manufacturing and interior design. We expect new housing units to be launched in 2022 to reach 65,000 units, a 41% increase from 2021, with over 55-60% of new units focusing on completed housing projects that can be finished within the year (typically taking 3-6 months to build), maximizing consumer benefits from the LTV relaxation (Figure 4).

Issue 2: The relaxation of LTV criteria allowing homebuyers to borrow the full collateral amount for all contracts could lead to an increase in property transfers in Bangkok and its vicinity in 2022 by up to 45 billion baht, representing a maximum upside of 7% for the market. Our assessment is based on two assumptions: 1) The relaxation of LTV will positively impact the condominium market more than the housing market, as consumers purchasing housing typically represent real demand and already have a significant proportion of first-contract loans, and 2) The relaxation of LTV will affect properties priced below 10 million baht more than those priced at 10 million baht and above, as we believe that consumers capable of borrowing for properties valued at 10 million baht must have a monthly income of at least 100,000 baht, which is sufficient for the 10-30% down payment required under the previous LTV criteria.

These two assumptions reflect our view that the relaxation of LTV is likely to stimulate borrowing for condominiums priced below 10 million baht from the second contract onward, allowing full borrowing of 100% of the collateral value again. Based on our estimated value of condominium transfers in Bangkok and its vicinity for 2022 in the baseline scenario (without LTV relaxation) at 257 billion baht, we expect about 70% will be transfers of condominiums priced below 10 million baht, amounting to 180 billion baht. Historically, condominiums in this price range have a borrowing proportion of 25% for second contracts onward, equating to a value of 45 billion baht.

Given the current condominium market, which has been affected by COVID-19 and the trend of Thai consumers leaning towards housing developments, the proportion of borrowers from the second contract onward is currently very low or nonexistent. We anticipate that the relaxation of LTV will provide an upside for the overall value of property transfers (both housing and condominiums) in 2022, potentially increasing by up to 45 billion baht from 646 billion baht in the baseline scenario to 691 billion baht (Figure 5). However, the actual upside may be lower than our estimates, depending on the current proportion of borrowers from the second contract onward. For example, if the current proportion is 12.5% or half of the historical average, the LTV relaxation could yield an upside of only 22.5 billion baht. Additionally, the high level of household debt, reaching 89.3% of GDP in Q2/2021, will also pressure consumers' ability to purchase homes.

Our View: Krungthai COMPASS assesses that the housing market in 2022 will benefit from various government measures, including the stimulus for foreign property buyers and the relaxation of LTV criteria by the Bank of Thailand. We expect the value of property transfers in Bangkok and its vicinity in 2022 to be around 646 billion baht in the baseline scenario, potentially increasing to a maximum of 691 billion baht due to the LTV relaxation.

Housing developers who will benefit the most from the LTV relaxation are those with projects ready for transfer by the end of 2022, as the Bank of Thailand's conditions state that the LTV relaxation will be temporary until December 31, 2022. For developers without projects ready for transfer by the end of next year, it is advisable to consider launching housing projects that typically take only 3-6 months to build. If they can complete construction within the year, consumers will benefit the most from being able to borrow the full collateral value.