IMF Sees Global Economy Recovering This Year Close to Previous Expectations Amid Inflation Uncertainty

Key Highlights

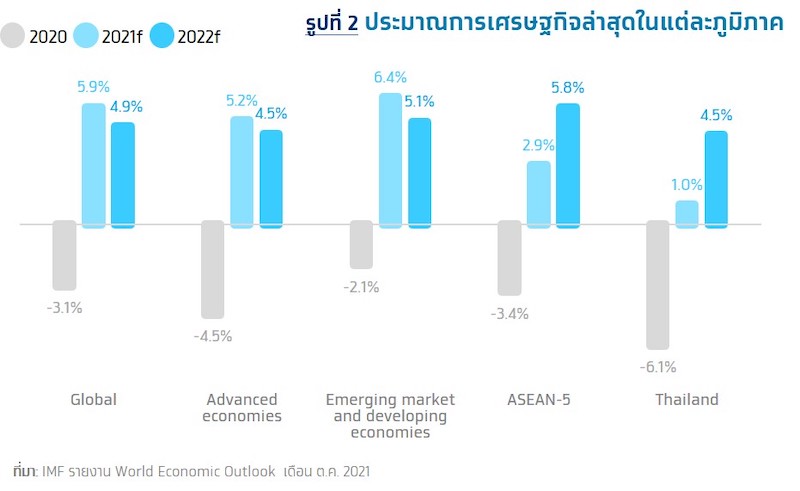

- IMF estimates that the global economy will grow by 5.9% in 2021, close to the previous forecast of 6.0%. Despite the impact of supply disruptions, this is offset by increased commodity exports from emerging and developing economies. For 2022, global economic growth is expected to be 4.9%, with developed economies recovering before emerging markets that have lower vaccination rates.

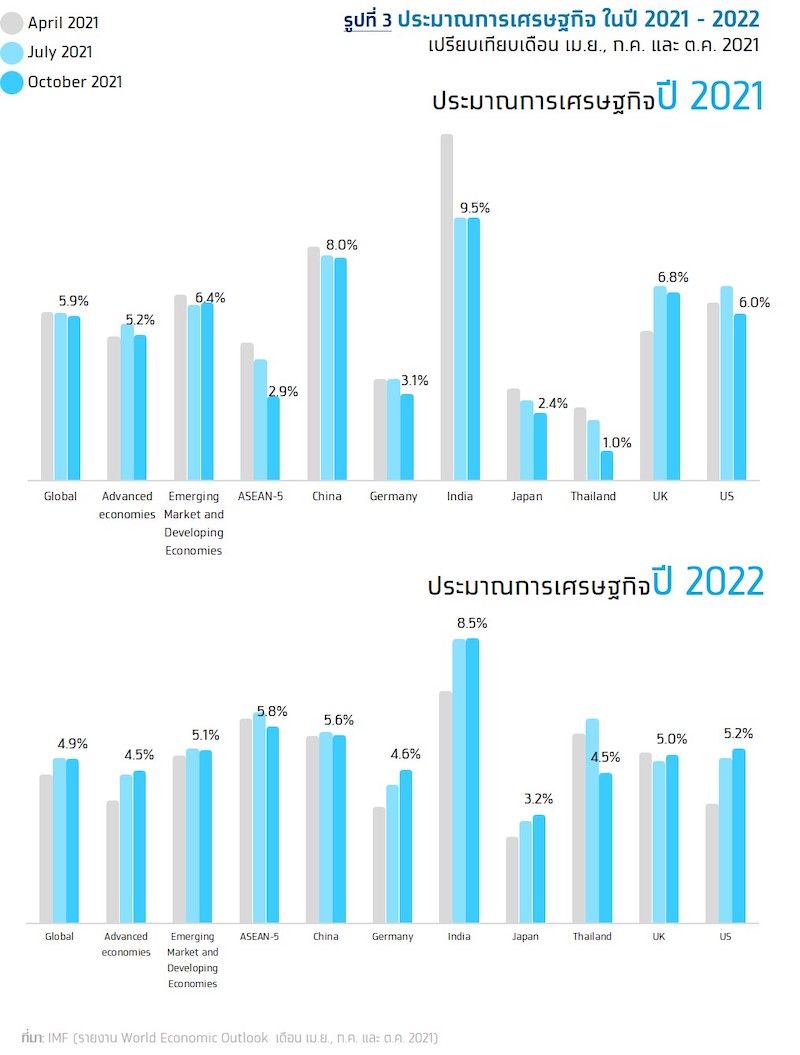

- IMF has revised Thailand's economic growth forecast down to 1.0% and 4.5% for 2021-2022, aligning with Krungthai COMPASS's view that the economy is recovering slowly due to the Delta variant outbreak, low numbers of foreign tourists and investors, and the export sector facing high raw material and shipping costs.

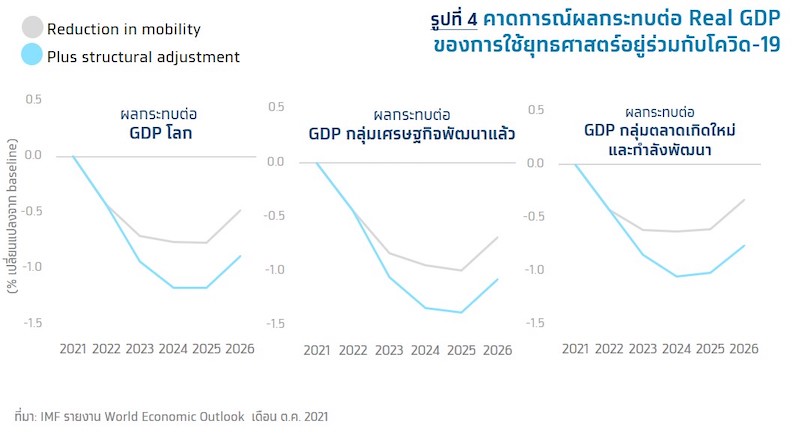

- Thailand's strategy to coexist with COVID-19 as an endemic disease will lead to restructuring and changes in business activities, impacting productivity in the medium term. Thailand is not expected to face significant stagflation risks, as inflation is likely to accelerate only temporarily, but government stimulus measures will need to be monitored as a boost to the Thai economy.

IMF Revises Global Economic Growth Forecast for 2021 to 5.9%, Slightly Lower than Previous Estimates Amid Inflation Uncertainty and Varied Recovery Rates Across Countries

IMF estimates that the global economy will grow by 5.9% in 2021 according to the World Economic Outlook (WEO) report released in October 2021, a slight decrease from the July 2021 estimate of 6.0%. This is due to a slowdown in growth in developed economies affected by supply disruptions and worsening pandemic situations in low-income countries. The recovery levels vary among countries based on the progress of COVID-19 vaccinations. For 2022, IMF maintains its global economic growth forecast at 4.9%, with key highlights as follows:

• Global economic momentum has begun to slow since the second quarter due to the COVID-19 outbreak in emerging and developing economies, along with the impact of supply disruptions affecting investments during this period, resulting in a slower overall recovery in the third quarter.

• Global trade has significantly grown in line with economic recovery despite facing supply disruptions. Global trade is expected to expand by 9.7% in 2021 and 6.7% in 2022, particularly in emerging and developing economies, which are projected to see import and export growth of 12.1% and 11.6%, respectively, in 2021, driven by rising commodity prices.

• Employment recovery is expected to be slow due to workers' concerns about infections, especially in occupations requiring close contact with others, childcare constraints during lockdowns, automation displacing jobs, unemployment compensation measures, and temporary unemployment caused by labor market stagnation.

• In the medium term, the global economy is expected to grow at an average of 3.3% from 2023 to 2026, with developed economies returning to pre-COVID levels by 2022, primarily due to anticipated additional economic stimulus measures from the United States. In contrast, emerging and developing economies and low-income countries are not expected to recover to pre-COVID levels within the forecast period due to slow vaccination rates and limited government assistance measures.

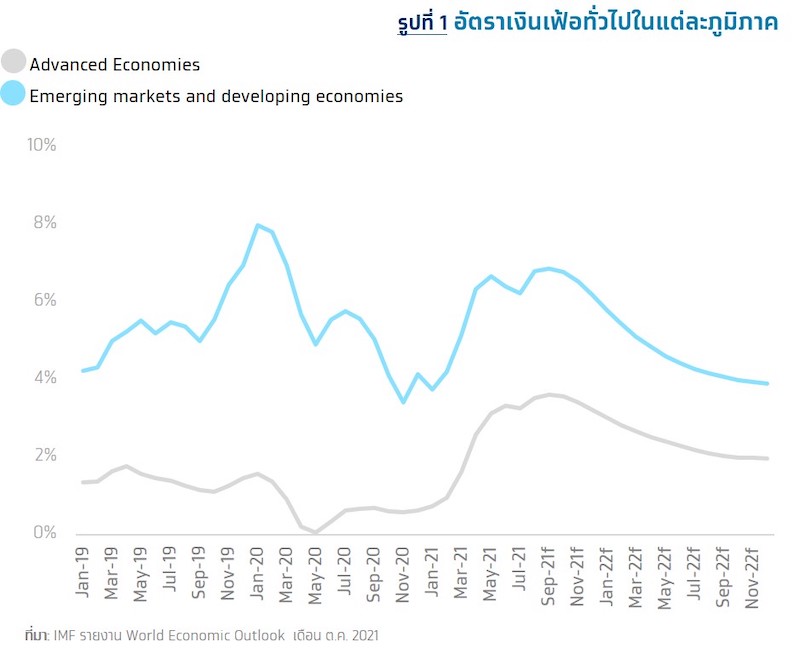

• General inflation is expected to accelerate to high levels for the remainder of this year before decreasing in 2022 (see Figure 1) due to tight supply, leading to higher commodity prices, along with the end of government assistance measures in several countries. However, price pressures in many countries are expected to ease in 2022, especially in emerging and developing economies, which are likely to face prolonged price pressures due to rising food prices, slower responses to global oil price increases, and local currency depreciation increasing import prices in the future. Additionally, there are issues related to labor supply slack, prolonged supply disruptions, and rapidly rising commodity and housing prices.

IMF Forecasts Thai Economy to Grow by 1.0% Before Recovering to 4.5% Next Year, Still Below Global and ASEAN-5 Averages

• Developed economies are expected to grow by 5.2% and 4.5% in 2021 and 2022, respectively, with the 2021 forecast revised down from July 2021's estimate of 5.6%, primarily due to a slower recovery in the U.S. economy, driven by reduced inventories and consumption in the third quarter, as well as raw material shortages in the manufacturing sector (e.g., in Germany) and renewed lockdowns (e.g., the fourth state of emergency declared in Japan during July-August).

• Emerging and developing economies are expected to grow by 6.4% and 5.1% in 2021 and 2022, respectively, with the 2021 forecast slightly revised up from July 2021's estimate of 6.3%. This is mainly due to increased commodity export prices compensating for output contraction from the new wave of the pandemic, except for China, where the forecast was downgraded due to a larger-than-expected reduction in public investment.

• Thailand's economy is expected to grow by 1.0% in 2021, lower than the previous estimate of 2.1% in July 2021, and is expected to grow by 4.5% in 2022, with an average growth rate of 3.5-4.0% between 2023-2026. Additionally, inflation is projected to be at 0.9% and 1.3% in 2021 and 2022, respectively, while the current account balance is expected to record a deficit of 0.5% of GDP in 2021 and return to a surplus of 2.1% of GDP in 2022, respectively.

Coexisting with COVID-19 as an Endemic Disease is Necessary but Comes with Economic Costs

• The IMF has indicated that adopting a strategy to coexist with COVID-19 as an endemic disease is a downside scenario that will impact future economic forecasts. This scenario is highly likely to occur, as even with widespread vaccination, it will not eliminate the disease's spread due to reduced vaccine efficacy in preventing and mitigating severity after vaccination. Additionally, issues such as vaccine shortages and hesitancy to get vaccinated mean that there will always be unvaccinated individuals at risk of infection. This implies that business activities will need to adjust to align with this assumption.

• Adjusting business activities under this scenario will lead to actual economic growth figures being lower than forecasted, as the economy must adapt to reduce infection risks through various methods, including: 1. Travel restrictions 2. Restructuring and changing business activities (e.g., using hybrid work models and remote work). Such adjustments will prevent contact-intensive economic activities from returning to pre-COVID levels. Furthermore, business restructuring will require additional investment in capital goods, impacting productivity temporarily, and natural unemployment will rise during the transition of workers needing to shift to other sectors. Considering these factors will result in GDP levels being lower than forecasted in the baseline (see Figure 4).

Implications

• The downward revision of Thailand's economic growth forecast to 1.0% and 4.5% for 2021-2022 by the IMF aligns with Krungthai COMPASS's view, which predicts Thailand's economic growth at 0.5% and 3.9% for 2021-2022, indicating that the economy is still recovering slowly due to the Delta variant outbreak, low numbers of foreign tourists and investors. Although Thailand plans to reopen to foreign tourists starting November 1, 2021, the number of tourists is unlikely to increase significantly due to high daily COVID-19 infection rates in Thailand. While the export sector is recovering, there are still negative factors slowing this recovery, including rising raw material costs for manufacturing and shipping, as well as the Thai baht likely appreciating in the second half of 2022.

• Medium-term growth forecasts for Thailand may need to consider the downside scenario of coexisting with COVID-19 as an endemic disease. The IMF predicts that in the medium term, Thailand's economy will grow between 3.5-4.0% from 2023-2026, but considering the endemic coexistence scenario, GDP growth in the medium term could decrease by about 0.4-1.0% (compared to the estimates for emerging and developing economies) due to productivity losses during the transition to new business models, temporary increases in unemployment, and travel restrictions, causing Thailand's economy to recover to pre-COVID levels more slowly than expected.

• It is expected that the Bank of Thailand will not rush to raise policy interest rates due to relatively low inflation risks in Thailand amid concerns that the Thai economy may enter a stagflation scenario due to a slower recovery compared to rising global inflation rates. Krungthai COMPASS views that although Thailand's economy has been growing slower than emerging markets for an extended period, and the crisis-affected economy has not fully recovered across all sectors (K-shape recovery), particularly the labor market facing severe scars from the COVID-19 crisis, leading to some at risk of long-term unemployment, inflation in Thailand is expected to accelerate only temporarily due to the composition of Thailand's inflation basket, which is based on global oil prices, having mechanisms to stabilize energy prices from fluctuating according to global market trends under the Fuel Oil Fund Act of 2019, along with the proportion of imported goods (Import content) being relatively low compared to exported goods (Export content), limiting the pass-through of rising production costs to inflation in Thailand.

• Krungthai COMPASS believes that government stimulus measures are essential for driving Thailand's economic momentum, as reflected in the IMF's assessment of Thailand's economy in 2022, which is expected to grow below previous estimates at 4.5%. This aligns with Krungthai COMPASS's view that Thailand's economy will only grow by 3.9% next year, indicating that the transition of Thailand's economic cycle is likely to shift from stagnation to recovery more slowly than before. Therefore, accelerating fiscal measures in line with the increase in public debt ceilings will not only support domestic consumption but also enhance confidence in the investment sector, helping the Thai economy recover faster. Additionally, measures should be implemented to expedite the restructuring of the business sector and reduce labor market slack to support productivity that may be affected by the downside scenario of coexisting with COVID-19 as an endemic disease.

• Countries with low vaccination rates will recover economically slowly, impacting Thailand's international trade, whether in emerging economies with limited vaccine access or developed countries like the United States, where some populations are hesitant to get vaccinated, leading to slower economic growth and higher inflation rates, posing risks of stagflation that could hinder Thailand's trade growth with these countries in the future. Therefore, it is essential to monitor both vaccination progress and economic support measures in these groups, particularly employment promotion measures that help reduce economic slack. For Thailand itself, measures should be in place to help diversify risks and reduce dependence on importing raw materials or exporting goods to any single country excessively in the short to medium term.