B2C E-commerce Product Sector in 2021 Grows Over 30% as Entrepreneurs Face Tougher Purchasing Power and Competition (Kasikorn Research Center)

Analysis by Kasikorn Research Center

• Kasikorn Research Center believes that while COVID-19 has accelerated the growth of the B2C E-commerce market value, which is expected to outpace overall retail business growth, the resulting competition has become tougher and more intense due to the increasing number of players. This is occurring amidst cautious consumer spending, and the growth of E-commerce may not stem from an overall increase in consumer spending but rather from a shift in purchasing channels from physical stores to online platforms, especially in the food and personal care product categories. This presents a challenge for entrepreneurs to adapt their sales channels to align with the constantly changing consumer behavior. If incoming revenue is insufficient or inconsistent, they are likely to face difficulties in business operations.

The online trading of goods, or B2C E-commerce, has accelerated in the past two years, with Kasikorn Research Center estimating that the market value for B2C E-commerce in 2021 will grow by 30% compared to the previous year, amounting to approximately 300 billion baht. The primary factors driving this growth include the COVID-19 pandemic, which has altered consumer purchasing behavior in terms of both the number of buyers and the variety of products, along with the adaptation of supply chain entrepreneurs, including last-mile delivery and payment channels that enhance convenience and build consumer confidence. It is anticipated that essential goods like food and beverages will see increased popularity during COVID-19, accounting for over 33% of the market value, followed by health and beauty products at 23%, while the remaining 44% consists of non-essential goods such as fashion items, furniture and home decor, electronics, and personal care products (e.g., shampoo, toothpaste, soap).

Forecast of B2C E-commerce Market Value by Product Category

However, Kasikorn Research Center observes that while the B2C E-commerce market continues to show growth potential, individual entrepreneurs are likely to face increasingly challenging business operations. This is a crucial issue that entrepreneurs must plan for and adapt to, especially if incoming revenue is insufficient or inconsistent, impacting business liquidity, particularly for small entrepreneurs who may be more adversely affected than larger ones.

- The increasing number of market players contrasts with consumers' cautious spending, resulting in tougher competition for entrepreneurs as they vie for limited consumer purchasing power. Although the COVID-19 pandemic has spurred rapid growth in the B2C E-commerce market, it has also negatively impacted consumer purchasing power broadly, leading consumers to spend only as necessary due to uncertainties about future income. The growth of E-commerce may not be due to an overall increase in consumer spending but rather a shift in purchasing channels from physical stores to online platforms, particularly in food and personal care products, which are expected to see online sales grow by no less than 30% YoY in 2021. It is possible that if the situation returns to normal, some consumers may revert to spending through traditional channels, especially for food and beverages, but likely not to the same extent as before COVID, as consumers have begun to adapt to and become accustomed to online channels.

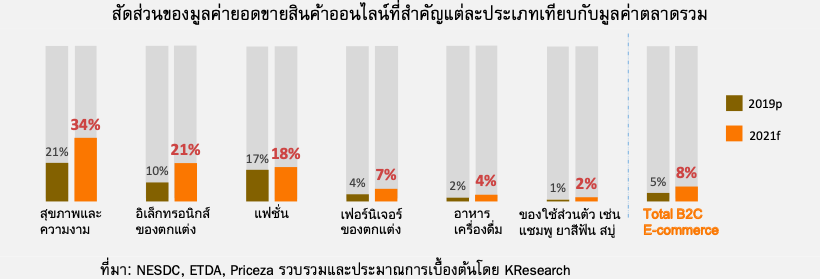

Therefore, entrepreneurs may need to plan and adapt their sales channels, reflecting the increasing importance of an omni-channel marketing approach that integrates online and offline platforms to gather big data. Importantly, the success or returns from investing in big data should provide clearer insights for businesses. - The online sales of various product categories are still expected to grow from their relatively low proportions compared to the overall market value, but this will depend on consumer adaptation and the readiness of entrepreneurs in the business chain. When considering the proportion of online product value for each category compared to the total market value, most products still have proportions of no more than 35%, indicating opportunities for each product category to expand their market share through online channels in the future, particularly in food, beverages, and personal care products, which currently have very small shares and are essential goods that consumers are expected to continue spending on through these channels more than on fashion or health and beauty products, which may not see rapid increases due to purchasing power constraints.

Nevertheless, expanding market share must consider consumer behavior alongside the readiness of entrepreneurs. For example, the recent severe COVID-19 outbreak has impacted critical businesses in the supply chain, such as delivery services or last-mile delivery, causing temporary halts in deliveries in some areas or longer delivery times, inevitably affecting each E-commerce entrepreneur, especially in food and beverages. Although demand increased during this period, they were unable to deliver products, and the high shipping costs for food products may influence customers' purchasing decisions once the situation normalizes. Additionally, consumer behavior regarding confidence in product quality, payment systems, and the quality of service from sales and delivery personnel remains a current issue.

Therefore, if businesses can adapt and alleviate concerns in various aspects of the supply chain, the proportion of product value on online platforms is likely to increase. This could include expanding warehouses or distribution centers to new potential areas, increasing investment in food delivery services to meet demand, building confidence in product quality, and maintaining consistent service quality from staff.

Proportion of Online Sales Value for Key Product Types Compared to Total Market Value

- In the near future, new technologies and ever-changing consumer behaviors are likely to alter the competitive landscape of the retail business further, making it difficult to determine who will emerge as market leaders. Each player faces challenges or has their own issues. Currently, competition among entrepreneurs on E-commerce platforms, whether it be

1) E-marketplaces that, despite showing increasing revenue trends each year, still experience continuous losses of around 30-40% annually (2018-2021), or even

2) Online modern trade that has become a seemingly advantageous platform as consumers increasingly purchase food and consumer goods, which are essential products with opportunities, yet must also compete with producers or suppliers who are selling through online channels, as well as 3) Social commerce platforms, where most are SMEs, which will have both successful and unsuccessful entrepreneurs depending on which can adapt and differentiate themselves more effectively.

Moreover, in the future, if consumer behaviors change from the present, there may be new or existing entrepreneurs entering with new retail business models to compete with the existing market. Ultimately, it may be challenging to determine who will play a role or become market leaders, or whether new players will emerge, as this will depend on consumer responses and the experiences or satisfaction they receive.

Thus, the flexibility of entrepreneurs to adapt to consumer behaviors is crucial for doing business amid these changes. It is evident that entrepreneurs on online platforms, especially larger ones, are continuously adapting to stimulate domestic sales, as well as seeking new avenues for revenue growth, such as cross-border E-commerce or even expanding investments in other businesses like finance and logistics.