Insights into the Thai Construction Industry for the Remainder of 2021 and Trends for 2022

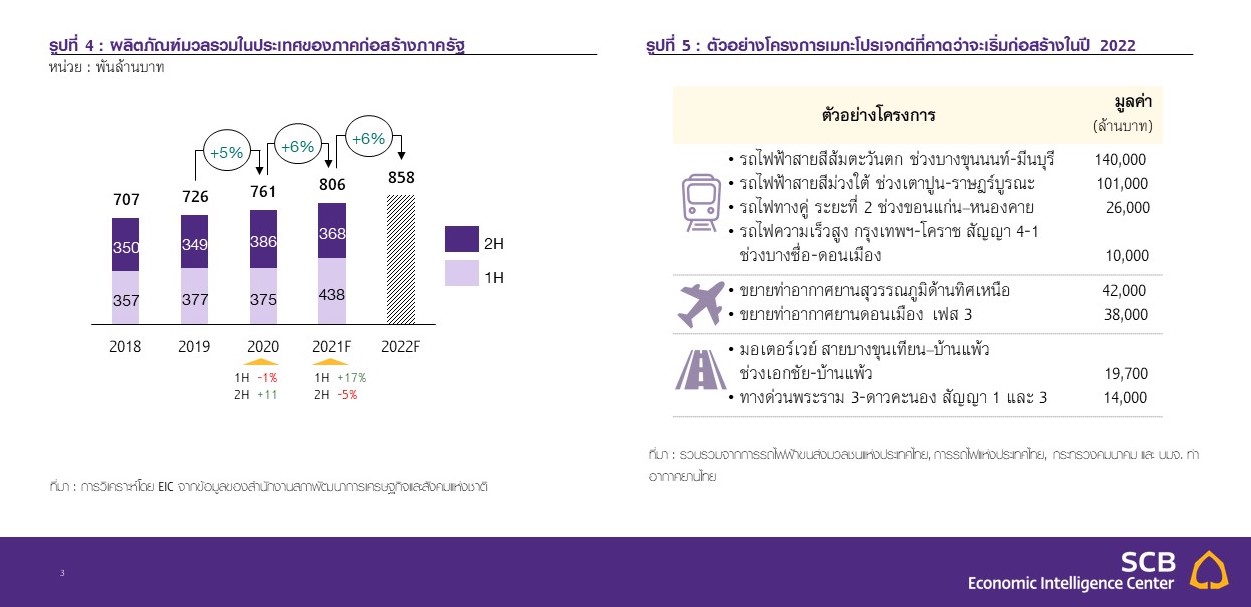

- The construction sector has been significantly affected by the new wave of COVID-19. Although the value of public construction expanded by 17% YTD in the first half of 2021, the order to close construction worker camps in July 2021, along with the risks of COVID-19 outbreaks in these camps and the implementation of construction activities under the Bubble and Seal measures, may delay future construction projects. This is expected to slow down the value of public construction in the second half of the year. EIC predicts that the value of public construction in 2021 will be around 806 billion baht (+6% YoY). For 2022, the value of public construction is expected to grow by 6% YoY due to the progress of ongoing mega-projects and the commencement of new projects, including the expansion of electric train lines, dual-track railways, high-speed rail, airport expansions, and road projects.

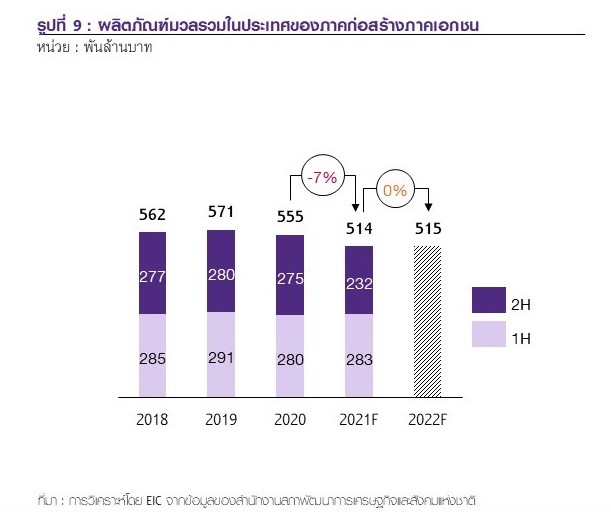

- Private sector construction is also expected to slow down due to the continuous contraction in the real estate sector. EIC estimates that the value of private construction in 2021 will be around 514 billion baht (-7% YoY), and in 2022, the value of private construction is expected to remain stable as it continues to face challenges from the slow recovery of the real estate sector.

- In 2022, operators are likely to adjust their strategies to take on more public construction projects amid the slow recovery of the real estate sector. They will also face high costs of steel and labor, as Chinese steel prices remain high, which will keep Thai steel prices elevated. Additionally, the closure of construction worker camps in July 2021 led to laborers leaving Bangkok and its vicinity, and many have not yet returned, resulting in a labor shortage and rising labor costs that may extend into 2022.

- A key challenge for the future growth of the construction sector is improving productivity. Currently, productivity has not improved significantly compared to the past. Furthermore, the low basic wage in the construction sector has led to a flow of labor to other industries, compounded by a decreasing proportion of young workers in construction due to the aging society trend. This, alongside the high demand for basic labor, means the construction sector continues to rely heavily on foreign labor.

- EIC believes that the widespread adoption of construction technology will help increase productivity. Large and medium-sized operators may expand their use of technology beyond just Prefabrication, Modular, BIM, and ERP to encompass the entire supply chain, from sourcing construction materials to site surveying, project delivery, and system maintenance services. Smaller operators may start with BIM and ERP, which can reduce the need for basic labor, allowing them to upskill workers for higher-skilled tasks, ultimately leading to improved labor productivity and operational efficiency in the long term.

EIC forecasts that the value of public construction in 2021 will grow by 6% YoY, supported by the progress of mega-projects. However, the COVID-19 outbreak in construction worker camps and the implementation of construction activities under the Bubble and Seal measures are putting pressure on the construction sector for the remainder of the year. In 2021, public construction has been bolstered by the commencement of mega-projects such as the high-speed rail connecting three airports (Don Mueang-Suvarnabhumi-U-Tapao), the development of Laem Chabang Port Phase 3, the Eastern Aviation City Phase 1, and Suvarnabhumi Airport's third runway. Additionally, several projects that are currently under construction from previous years are making progress, such as the expressway from Bang Yai to Kanchanaburi and the Bang Pa-In to Nakhon Ratchasima route, resulting in continuous cash flow into public construction.

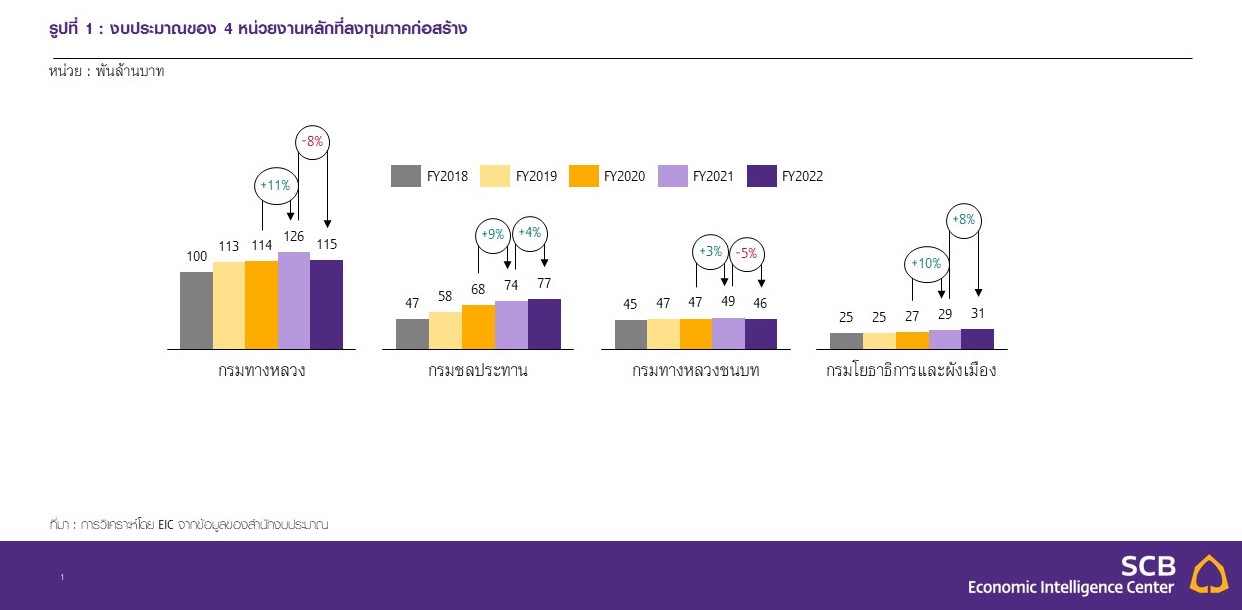

For the fiscal budget of 2021 (B.E. 2564) for the four main agencies investing in construction, namely the Department of Highways, the Royal Irrigation Department, the Department of Rural Roads, and the Department of Public Works and Town & Country Planning, there has been growth from the previous year. Notably, the Department of Highways received a budget of over 126 billion baht (+11% YoY), primarily for the construction and improvement of highways and bridges, while the Royal Irrigation Department received over 74 billion baht (+9% YoY), mainly for expanding irrigation areas.

Figure 1: Budget of the four main agencies investing in construction

Source: Analysis by EIC from Budget Bureau data

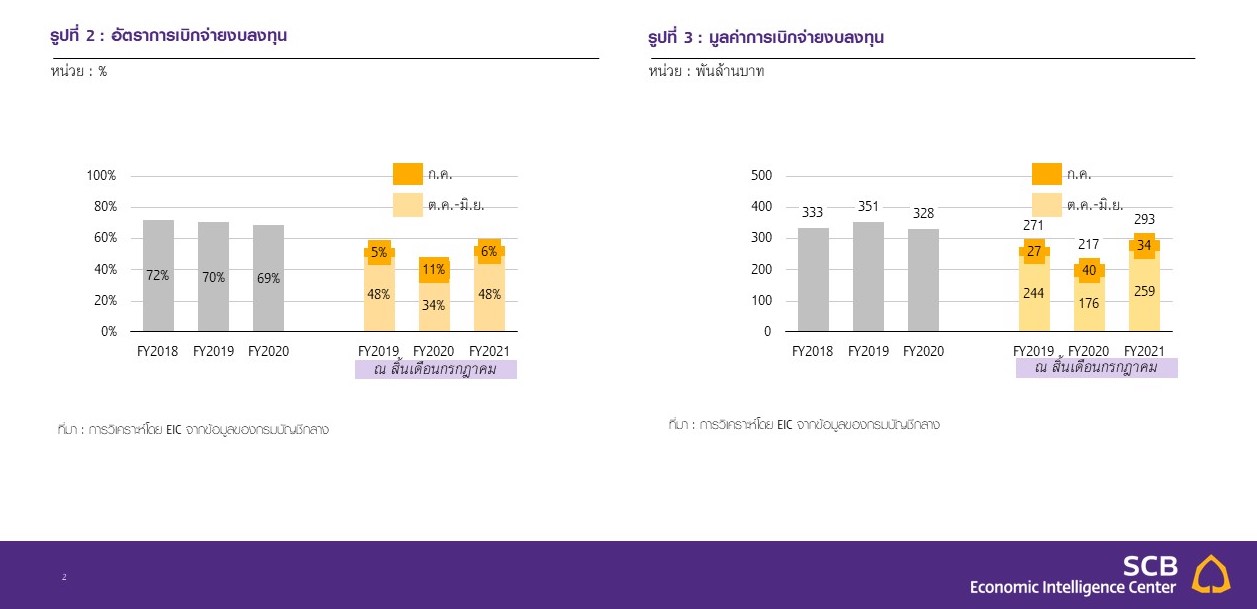

Furthermore, the disbursement rate of the investment budget for the fiscal year 2021 (B.E. 2564) as of the end of June 2021 was at 48% of the investment budget, higher than the same period last year, which was at 34% of the investment budget. This resulted in the value of disbursement at the end of June 2021 being 258,583 million baht (+47% YTD), supporting a high flow of funds into public construction in the first half of 2021.

With the progress of mega-projects, both those that commenced construction in 2021 and those that are ongoing from previous years, along with the budget of the main agencies investing in construction in the fiscal year 2021 (B.E. 2564) that has grown from the previous year, combined with the high value of disbursement in the first half of 2021 compared to the same period last year, it is expected that the value of public construction in the first half of 2021 will be 438,295 million baht (+17% YTD).

EIC believes that although the value of public construction expanded at a high rate in the first half of 2021, the construction sector is another business that has been affected by the new wave of COVID-19. The order to close construction worker camps in July 2021 has caused public construction projects in Bangkok and its vicinity to come to a halt, which aligns with the value of disbursement in July 2021 dropping to 33,966 million baht (-15% YoY). Additionally, the risk of COVID-19 outbreaks in construction worker camps for the remainder of the year may lead to the closure of some construction worker camps again, along with the requirements for conducting construction activities under the Bubble and Seal measures starting from August 2021, creating pressure that may delay various projects due to hygiene and social distancing constraints, potentially reducing construction efficiency.

Moreover, in the second half of 2020, the value of public construction expanded at a high rate of 11% YoY due to effective disbursement of the investment budget, resulting in a high base for the second half of 2020. This leads EIC to predict that the value of public construction in the second half of 2021 will likely contract by -5%, resulting in an overall value of public construction in 2021 of around 806 billion baht (+6% YoY), continuing from the 5% YoY growth in 2020.

For the outlook in 2022, public construction remains a key driving factor for the construction sector due to the progress of mega-projects and the commencement of new projects. EIC predicts that the value of public construction in 2022 will be around 858 billion baht (+6% YoY), resulting from the progress of significant mega-projects that are continuously under construction from the past, such as the high-speed rail connecting three airports, the development of Laem Chabang Port Phase 3, the Eastern Aviation City Phase 1, and Suvarnabhumi Airport's third runway.

Additionally, the commencement of bidding and construction of new mega-projects, including the expansion of electric train lines, dual-track railways, high-speed rail, airport expansions, and road projects, will also lead to a continuous flow of funds into public construction in 2022. However, it is essential to monitor the bidding and signing of contracts for new projects, which may face delays and impact the growth of public construction value in 2022.

Meanwhile, the budget of the main agencies investing in construction in the fiscal year 2022 (B.E. 2565) is expected to shrink, which may not significantly support the value of public construction. The budgets of the main agencies investing in construction, including the Department of Highways and the Department of Rural Roads, are expected to contract by -8% YoY and -5% YoY, respectively, in line with the overall budget allocation for 2022 (B.E. 2565), which has been reduced from the previous year amid the COVID-19 outbreak. Therefore, this budget may not significantly support the value of public construction in 2022, unlike the situation in 2021, where the budget for 2021 (B.E. 2564) of the main agencies investing in construction expanded from the previous year. It can be said that the supporting factors for the value of public construction in 2022 will primarily come from the progress of mega-projects and the commencement of new projects.

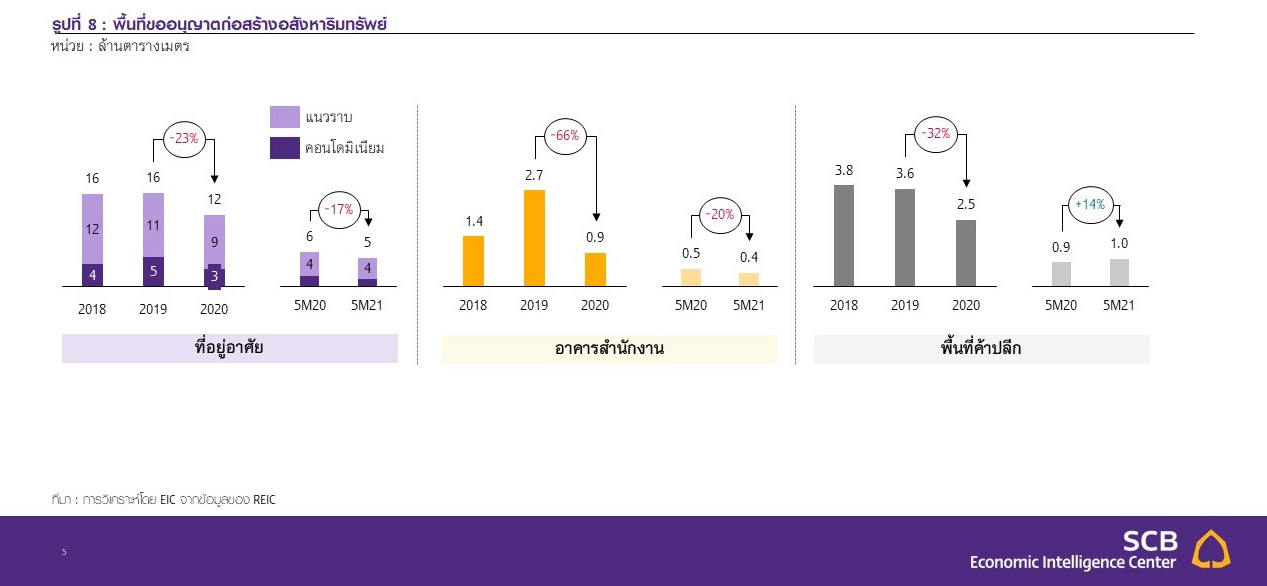

Private construction is still expected to slow down due to the continuous contraction in the real estate sector. EIC estimates that the value of private construction in 2021 will be around 514 billion baht (-7% YoY), reflecting a decline in both residential and commercial real estate construction. The COVID-19 outbreak has caused the number of housing units sold in Bangkok and its vicinity to continuously decrease since 2020. In 2020, the number of housing units sold was 65,279 units (-35% YoY), the lowest level in 11 years. In 2021, since the outbreak intensified in April 2021, it has pressured the number of housing units sold in 2021, which EIC estimates will be 57,300 units (-12% YoY).

This situation has led housing developers to focus on stock clearance and cautiously launch new housing projects. Developers have delayed launching new housing projects for the remainder of 2021, resulting in EIC estimating that the number of new housing units launched in Bangkok and its vicinity in 2021 will be 47,000 units (-36% YoY), continuing to decline from 2020, which had 73,043 new housing units launched (-39% YoY).

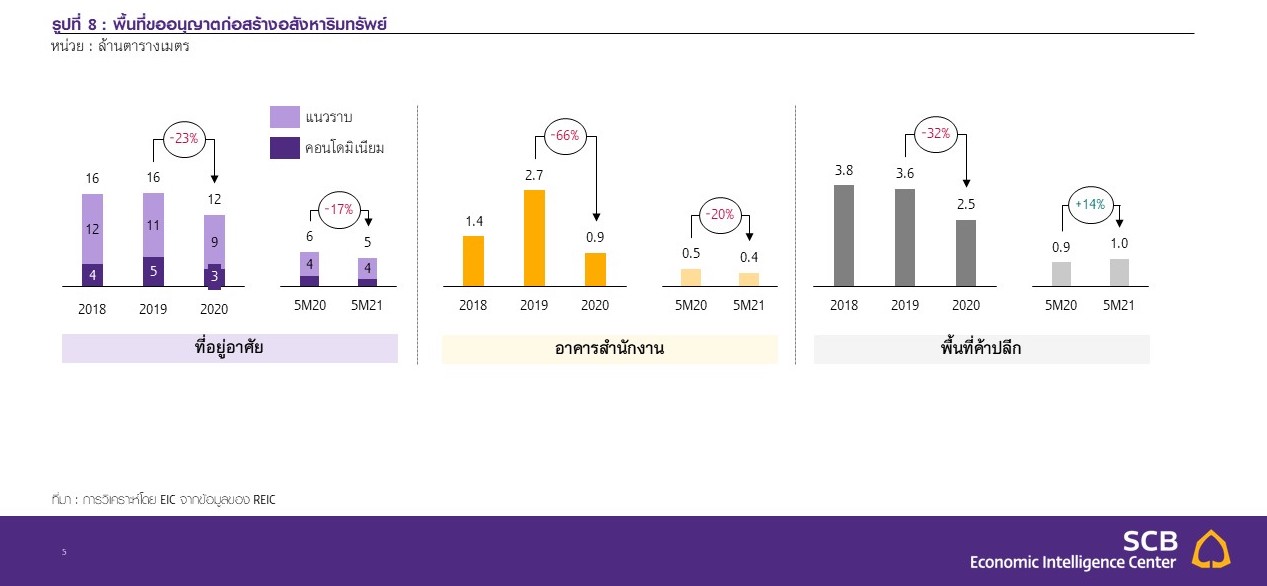

Meanwhile, commercial real estate developers have also been affected by the COVID-19 outbreak. The closure of businesses and the work-from-home measures have led businesses to cancel or reduce office space leases, resulting in a continuous decline in construction permit requests for office buildings during the first five months of 2021. The retail sector has been impacted by previous lockdown orders, allowing only supermarkets and restaurants for takeout and delivery services. This has caused tenants in other areas who could not bear the rental costs to cancel their leases. Although lockdown orders have been relaxed to allow retail spaces to open, the situation is not expected to improve significantly, with rental rates decreasing and operators unable to raise rents. However,

the requests for construction permits for retail spaces in the first five months of 2021 have recovered from a very low base in the first five months of 2020, which contracted by -47% YTD. While operators are still expanding to accommodate the recovery of the retail business, they face challenges from the rapidly growing trend of online shopping, which may reduce foot traffic to physical stores, requiring operators to adjust their strategies to attract customers back to physical stores.

In 2022, the value of private construction is expected to remain stable as it continues to face challenges from the slow recovery of the real estate sector. The business sector is still implementing work-from-home measures alternating with office work, and the rapidly growing trend of online shopping may lead commercial real estate developers to slow down or reconsider large-scale construction projects. Meanwhile, residential developers are likely to develop smaller projects to facilitate quicker sales, with the expectation that the value of private construction will remain stable compared to 2021.

EIC believes that in 2022, large operators are likely to adjust their strategies to take on more public construction projects, while medium and small operators are likely to become subcontractors for public construction projects. Amid the slow recovery of the real estate sector, this pressure is leading large operators to adjust their strategies to take on public construction projects and increase participation in public-private partnerships (PPP) in 2022. They are also focusing on developing organizational capabilities to participate in various public construction bids, while operators primarily focused on private projects may need to adjust their strategies to take on renovation projects, as some commercial real estate developers, especially in retail areas, are renovating spaces to accommodate business recovery.

If the COVID-19 outbreak subsides, medium and small operators will also be affected by the slow recovery of the real estate sector, with a tendency to become subcontractors for public construction projects. The budget of the main agencies investing in construction, particularly the Department of Rural Roads, in the fiscal year 2022 (B.E. 2565), which has contracted from the previous year, may lead to delays or halts in construction projects in the regions, causing medium and small operators to lose opportunities to bid for and construct medium and small projects in the regions.

Additionally, operators will face challenges from high steel and labor costs in 2022. The economic recovery in China has led to continued demand for steel from 2021. However, the declining costs of iron ore due to increased production from the United States and Brazil may help alleviate some of the pressure on Chinese steel prices. EIC predicts that in 2022, the price of Chinese long steel will decrease to 733 baht/ton from 785 baht/ton in 2021. Nevertheless, this price level is still considered high compared to historical levels of around 500-600 baht/ton, and the ongoing high prices of Chinese steel will keep Thai steel prices elevated.

Moreover, the closure of construction worker camps in July 2021 has resulted in migrant workers and workers from other provinces leaving Bangkok and its vicinity, and many have not yet returned. Operators, especially in public projects, must expedite construction to meet delivery deadlines in August and September 2021, which is the final stretch of the fiscal year 2021 (B.E. 2564), leading to labor shortages and rising labor costs. This labor shortage and high labor costs may extend into 2022 as well.

Continuous impacts from the COVID-19 outbreak have led to a new normal lifestyle, requiring operators to monitor emerging trends to adapt construction methods to meet changing consumer lifestyles and the evolving real estate sector. Whether in the housing market, where there is a growing preference for horizontal living, or in office construction, which must respond to trends of people spending more time at home, as well as work-from-home measures alternating with office work, the construction of office buildings will change from focusing on fixed workspaces to more flexible workspaces, emphasizing the expansion of common areas and improving communication systems to support remote work. Retail spaces may also need to adjust construction methods to include more outdoor areas. Furthermore, new construction trends must prioritize the integration of technology, such as automation and sensors, to reduce contact while considering environmental impacts, such as energy-efficient buildings and the use of eco-friendly construction materials.

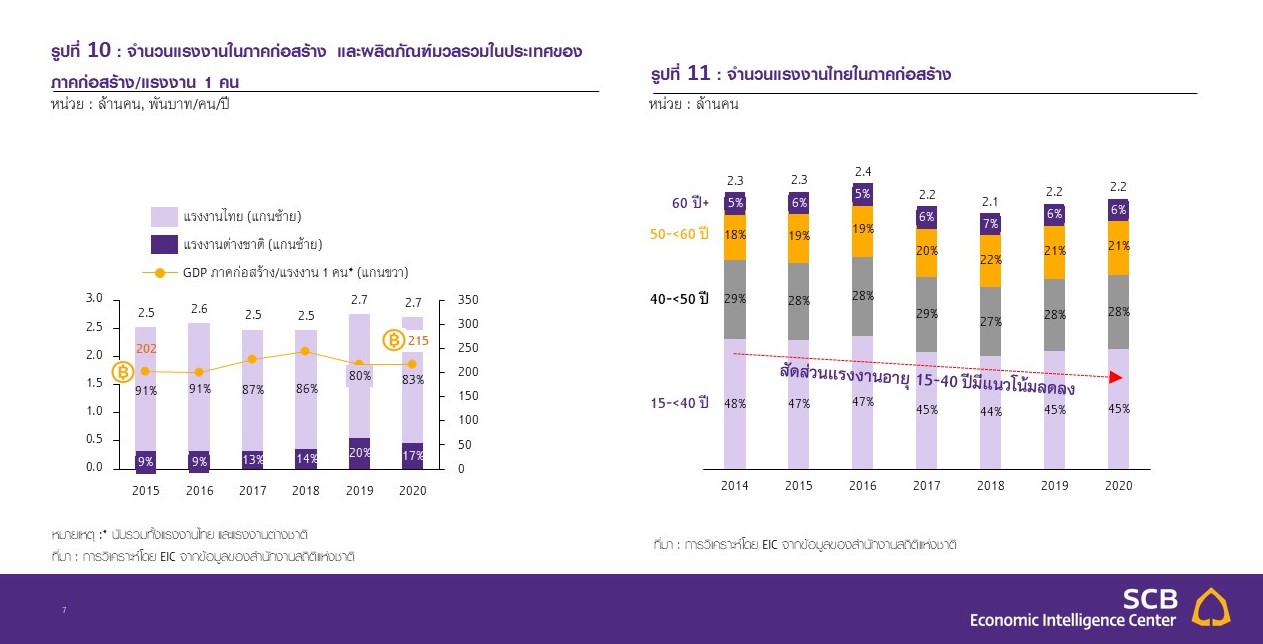

A key challenge for the future growth of the construction sector is improving productivity, as well as the continued reliance on a large number of foreign workers. The construction sector accounts for about 8% of the country's GDP, reflecting its significant role in driving the economy. Construction workers can generate GDP of about 200,000 baht/person/year, but current productivity has not improved significantly compared to the past.

Moreover, the aging society trend is leading to a decrease in the number of workers in the construction sector, particularly among workers aged 15-40, who made up 48% of the total construction workforce in 2014, gradually decreasing to 45% in 2020. Additionally, the basic wage in the construction sector remains lower than in other industries, with the average basic wage in construction in 2020 being 7,529 baht/month, while the basic wages in other sectors such as wholesale/retail, manufacturing, and hotels/restaurants are higher, averaging 8,499 baht/month, 8,845 baht/month, and 9,034 baht/month, respectively. This low basic wage has led to a continuous outflow of labor to other industries, compounded by the decreasing proportion of young workers in construction due to the aging society trend. Amid the high demand for basic labor in construction, the sector continues to rely heavily on foreign labor, with foreign workers accounting for about 17% of the total construction workforce in 2020.

The widespread adoption of construction technology, along with upskilling the workforce, will help elevate productivity in the construction sector. The construction sector remains a business with a high demand for basic labor, while the adoption of technology to enhance productivity is still at a low level. This is due to the distribution of large construction projects with diverse activities and work processes to subcontractors, most of whom are medium and small operators lacking the knowledge and capital to access construction technology. As a result, the use of technology is still concentrated among large operators and some medium-sized operators. Furthermore, despite facing labor shortages, the construction sector has been able to rely on foreign labor, leading to less urgency or motivation to adopt technology to enhance productivity or replace labor.

Currently, the use of technology in the construction sector is mostly limited to certain stages, such as prefabricated construction methods like Prefabrication and Modular, project management using Building Information Modeling (BIM) and Enterprise Resource Planning (ERP). The use of these technologies is still limited to large operators and some medium-sized operators. When considering the supply chain of the construction sector, it is evident that there are various stages and activities, from sourcing construction materials to site surveying, project delivery, and post-delivery system maintenance services.

EIC believes that the increased adoption of construction technology will help enhance productivity in the construction sector, particularly among large and medium-sized operators who have the knowledge and capital to access construction technology. They may expand their use of technology beyond just construction processes and project management to encompass the entire supply chain, from sourcing construction materials to site surveying, project delivery, and post-delivery system maintenance services. Meanwhile, small operators may start with BIM and ERP.

Additionally, the government may play a role in supporting the use of construction technology through various measures, such as promoting investments in construction technology, reducing import taxes on construction technology, lowering corporate income taxes for operators investing in construction technology, and providing funding support for medium and small operators. The widespread adoption of construction technology can reduce the reliance on basic labor, allowing operators to upskill basic labor to perform higher-skilled tasks, both in technology control and skilled work, leading to improved labor productivity and enhanced operational efficiency for operators in the long term.

Analysis by: >>> https://www.scbeic.com/th/detail/product/7770

Author: Kanyarat Kanjanavisut ([email protected])

Senior Analyst, Economic Intelligence Center (EIC)

Siam Commercial Bank Public Company Limited

EIC Online: www.scbeic.com

Line: @scbeic