Real Estate Under the Winds of the Thai Economy

Dr. Don Nakornthap, Assistant Governor of the Bank of Thailand, reflected on the state of the Thai real estate market in 2026 during the seminar "Real Estate Under the Winds of the Thai Economy." He noted that the Thai economy is facing pressures from external factors, standing amidst waves not solely caused by domestic issues but also by global geopolitical shocks, particularly the conflict in the Middle East. This situation has impacted energy prices, inflation, business costs, and consumer purchasing power in a chain reaction. Just as the Thai economy was beginning to recover, it now faces new pressures that significantly slow down growth. Even before the outbreak of war, the Thai economy showed positive signs from consumption, investment, and exports, but the current situation has rapidly changed the entire equation.

The Thai Economy Continues to Slow Due to War

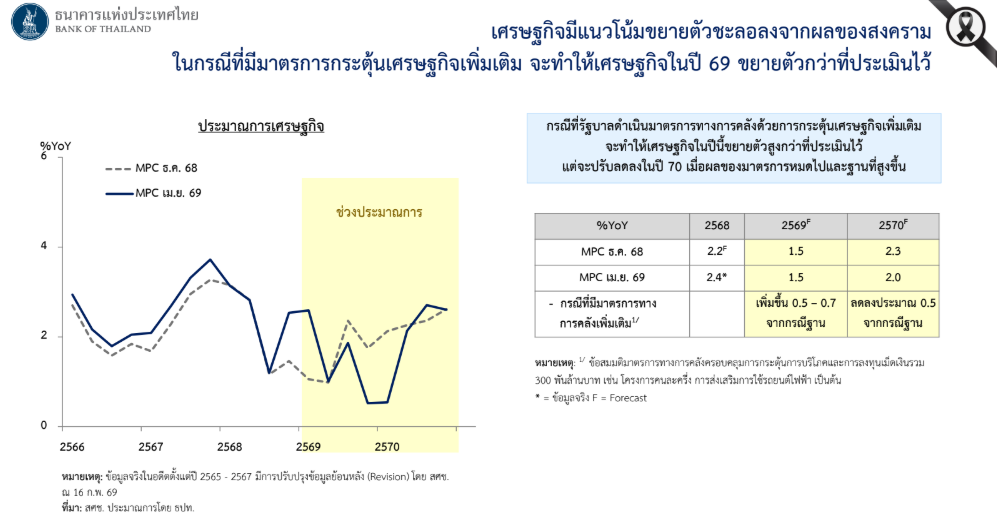

Before the war, the Thai economy showed signs of recovery from consumption, investment, and exports. However, the latest developments have quickly altered this equation. The Bank of Thailand estimates that in 2026, the economy will grow by only 1.5%, and in 2027, it will expand by about 2.0%. These figures reflect growth that is "significantly below potential." Although there are opportunities for stimulation through fiscal policies, such as a 300 billion baht economic stimulus package that could boost GDP by about 0.5-0.7% in the short term, there are also potential negative repercussions in the following period. This means that the Thai economy at this time is not driven solely by fundamental factors but is heavily reliant on "policy" and "timing."

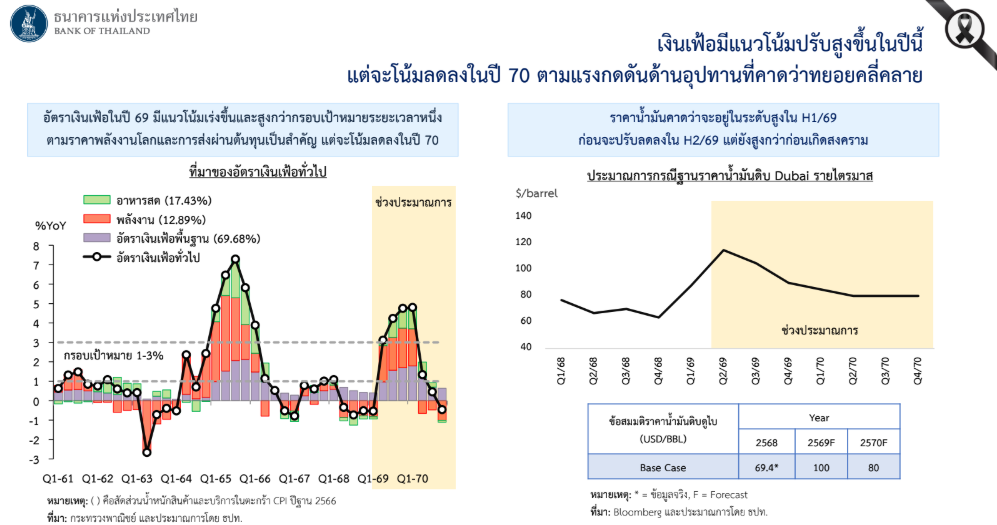

One of the key shocks is “cost-push inflation” driven by soaring global energy prices. Inflation in 2026 is expected to exceed the target of 1-3%, potentially reaching 3-5% in the short term before decreasing in 2027. However, this round of inflation is not driven by strong demand but by energy costs and supply chain issues, limiting long-term risks. Key factors that help alleviate pressure include a labor market that does not experience a wage-price spiral, fragile purchasing power, and inflation expectations remaining within bounds.

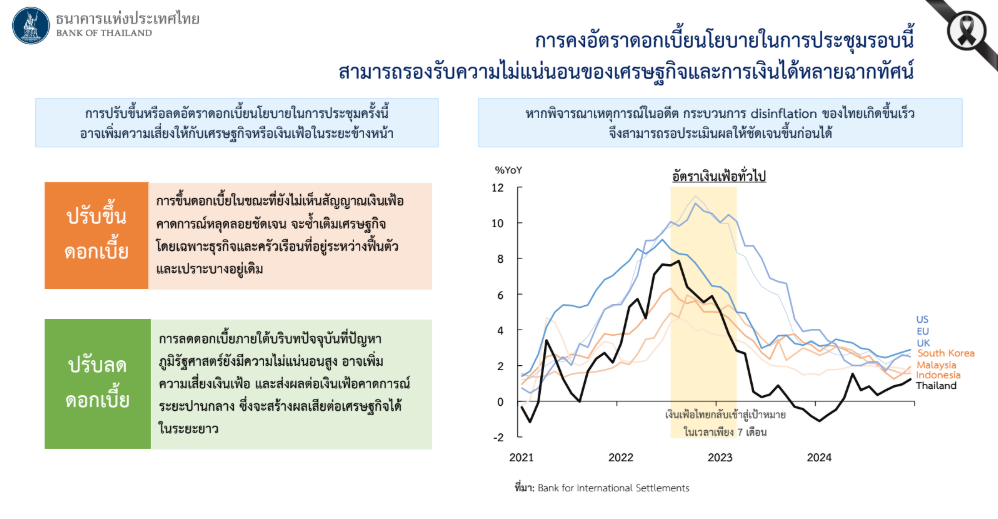

The Monetary Policy Committee unanimously decided to maintain the interest rate at 1.00%. The main reason is that "raising interest rates" would exacerbate the economy and households, while "lowering interest rates" could increase inflation risks. Therefore, maintaining the interest rate is a choice for "balance" during a time of high uncertainty.

Real Estate Faces Three Layers of Pressure

When linked to the real estate sector, multiple dimensions of pressure can be observed:

1. Increased Development Costs - Rising energy prices have impacted construction material costs, such as steel, cement, aluminum, and asphalt. Many operators cannot fully "pass on costs to prices" due to weak consumer purchasing power.

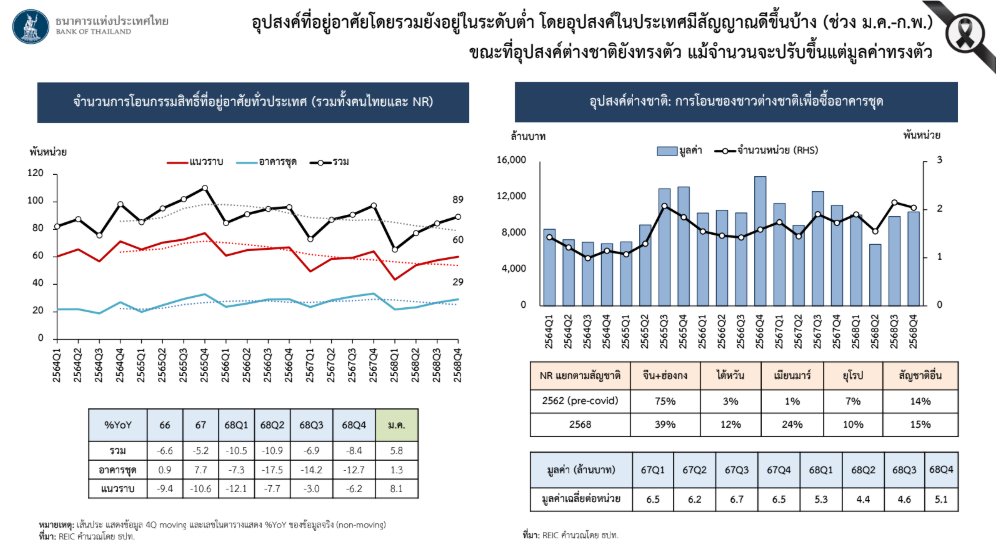

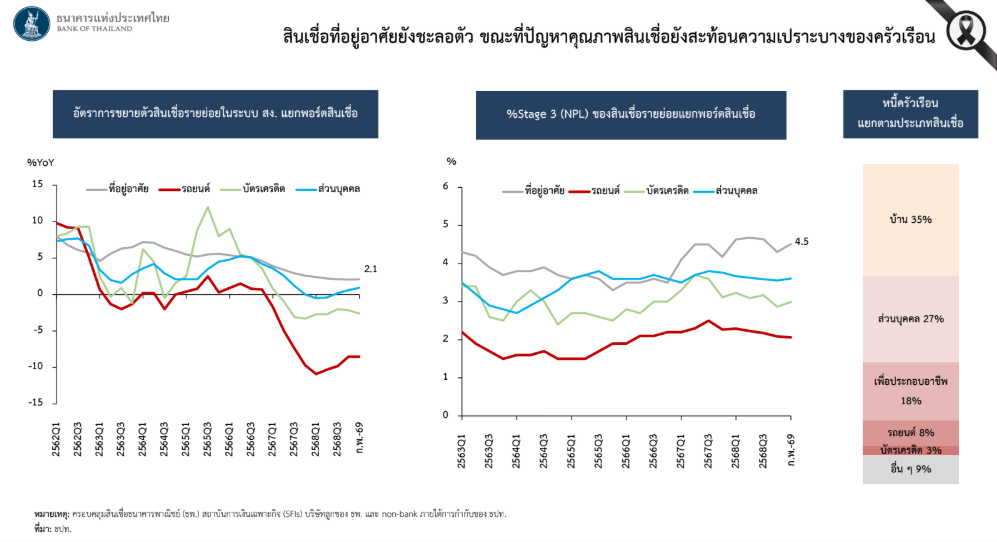

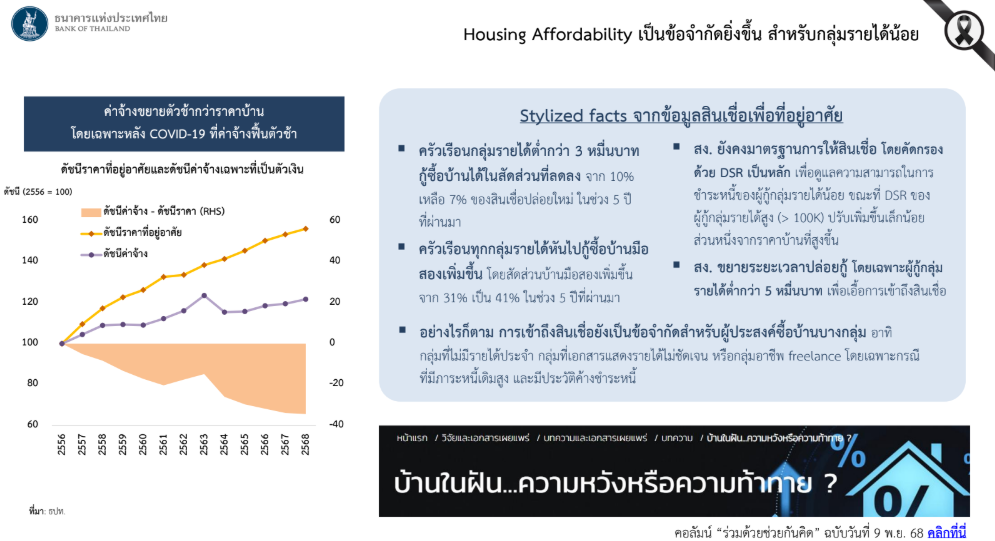

2. Decreased Consumer Purchasing Power - Data clearly shows that the cost of living is rising faster than income, reducing borrowing capacity and worsening housing affordability, especially for low-income groups. As a result, consumers are delaying purchasing decisions, leading to a decrease in demand for new homes, with the market shifting towards second-hand homes (increasing from 31% to 41%).

3. Slower and Tighter Lending - Financial institutions are becoming more cautious in granting loans, with housing loans growing slowly and stricter screening (DSR being a key variable). Household debt remains high, which is the "heart of demand" for real estate. When lending slows, the market follows suit.

4. Uncertainty Causes the Market to “Wait” - Fluctuations in asset prices, the baht, and financial markets have led consumers to enter a "Wait & See" mode, resulting in a slowdown in transfer and sales volumes.

Housing Affordability and Limitations for Low-Income Earners

Housing affordability is worsening, particularly for low-income groups, due to the widening gap between "housing prices" and "income" that has expanded since the COVID-19 period. Housing prices have continuously increased, while wages have grown at a significantly slower pace, resulting in a real decrease in consumer purchasing power. Even though incomes have increased somewhat, they have not kept pace with rising housing prices, making homeownership increasingly "distant" for many, especially first-jobbers or entry-level income earners. "Stylized facts" reinforce structural problems, revealing that:

- The proportion of those earning less than 30,000 baht who can borrow to buy a home has decreased from 10% to only 7% over the past five years.

- Consumers are "adapting" by increasingly purchasing second-hand homes (increasing from 31% to 41%) because they are more affordable.

- Banks remain strict in granting loans, using DSR as a primary criterion, making it difficult for low-income groups to access credit.

- Even with "extended loan terms" to help ease monthly burdens, the main issue of insufficient income to support housing prices remains unaddressed.

Additionally, another affected group includes freelancers or those without regular income, who often face limitations in income documentation and existing debt burdens, leading to exclusion from the credit system, even if they have the potential to repay loans.

Data from the Bank of Thailand indicates that the Thai real estate market is clearly entering a period of "screening," evidenced by declining property transfers, high unsold inventory, and low loan growth. Particularly, small operators face more constraints regarding costs and capital, meaning that those who survive must have high liquidity, manage costs effectively, and access funding sources.

However, the crisis also presents opportunities for cash buyers to acquire assets at reasonable prices, while the rental market grows due to purchasing constraints, and the upper market continues to thrive. Projects focusing on "value" will increasingly meet consumer needs.

Ultimately, this is not just a slowdown but a change in the rules of the game, shifting from an era driven by demand and credit to one competing on financial strength and adaptability. The winners will not be those who grow the fastest but those who adapt most accurately.