Analyzing the Structure of the Thai Economy Amid Challenges in the Second Half of 2020

The Thai economy, starting from late 2019 to the second quarter of 2020, has been severely impacted by the COVID-19 pandemic, particularly in the tourism sector, which is a key driver of national income. Although the COVID-19 situation in Thailand has improved significantly, there remains a need for vigilance due to uncertainties and high risks.

The Kasikorn Research Center views the economy as recovering in a U-shaped pattern.

The Kasikorn Research Center indicates that the Thai economy hit its lowest point in the second quarter of this year, reflecting a contraction compared to the previous quarter. The outlook for the Thai economy continues to face high uncertainty due to the COVID-19 outbreak, the strengthening of the baht, and political issues. As a result, the Kasikorn Research Center has revised its economic forecast for Thailand in 2020 to -10% from the previous -6%.

It is expected to see a U-shaped recovery, and how quickly the Thai economy can navigate through the U-shaped bottom has become a challenging task for the government, which must weigh the implementation of additional economic measures that are sufficient and timely against the costs of such measures, such as increasing public debt and the risk of another outbreak as the country gradually reopens.

The financial sector anticipates that loans from the Thai commercial banking system will grow by 6.5-8.0% in 2020, compared to a growth of 2.3% in 2019. This higher-than-normal growth reflects the impact of measures to assist customers and businesses seeking liquidity rather than actual economic activities.

However, attention must be paid to the quality of debt, as the non-performing loan (NPL) ratio is expected to rise to around 3.5% by the end of 2020, compared to 3.23% at the end of June 2020. While the government will need to raise significant funds in the financial market, it is believed that the Bank of Thailand's existing tools will help manage interest rates in the system. Currently, deposits in commercial banks are growing at around 9-10% compared to the previous year.

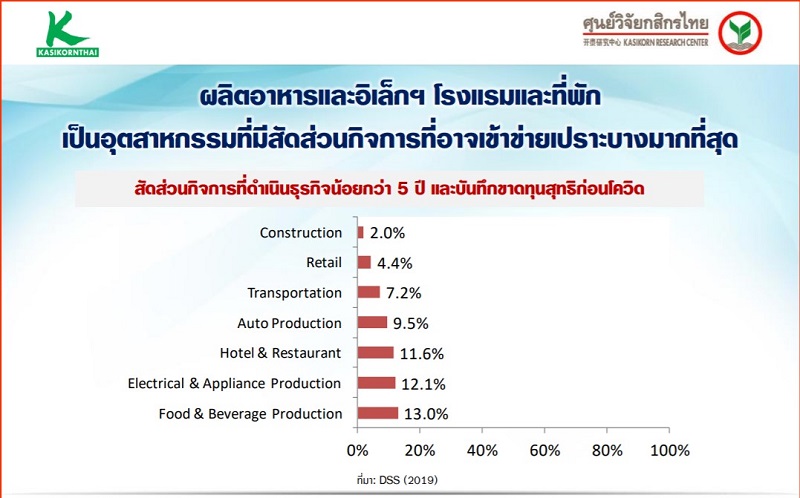

Although some areas may gradually improve due to the government's phased reopening policies and economic stimulus, they are still far from normal conditions. The three most vulnerable business sectors include food and beverage, electrical appliance manufacturing, and the hotel and restaurant industry, which are likely to continue receiving government support.

Thailand must better manage demand and supply risks from abroad.

Dr. Somprawin Manprasert, Assistant Managing Director and Head of Economic Research at Krungsri Bank, provides insight that the current situation is characterized by high uncertainty and risks. Thailand has been significantly affected by its dependence on both demand and supply from abroad. Therefore, Thailand needs to reduce or better manage these risks. While supply may begin to recover, demand has not returned to normal. Trade may improve, but it is unlikely to reach pre-COVID levels due to factors such as tourism, which may take time to recover, as well as trade in other goods and services. Thailand should focus on emerging sectors, enhancing creativity to adapt to changes.

This crisis should be viewed as an opportunity to restructure the economy appropriately, allowing market mechanisms to function to optimize resource allocation. Global trade trends will increasingly come from low to middle-income individuals who still seek quality products at affordable prices. The aging society in both Thailand and globally will shift demand trends for goods and services in the market. Additionally, factors such as the environment, pandemics, and technology will be crucial in changing the economic structure.

The global value chain will shorten, diversify, and increasingly favor regional production to mitigate risks from global landscape changes. Furthermore, the service sector will play a more significant role and come closer to consumers. Businesses must connect services with production to create added value and access future markets. It is expected that Thailand will participate more in economic activities within the ASEAN region. The key question is how to engage in the value chain appropriately and diversify risks to strengthen both Thailand and other countries in the region.

Develop Thai products to add value across the supply chain.

Dr. Kritlert Sumpantharak, Director of the Pooying Uengphakorn Economic Research Institute, states that Thai trade will face uncertainties due to the lack of diversity in exports and the small number of potential exporters, most of whom are foreign companies.

Therefore, Thai businesses must enhance their export capabilities with diverse products that add value across the supply chain. Thailand can promote trade with regional countries rather than compete. Trends affecting global trade include diversifying risks from over-reliance on any single market, focusing more on regional markets, utilizing technology to enhance production, whether through artificial intelligence (AI) or various trading platforms, adapting to an aging society, climate change, and food security. Thailand has the potential to develop in these areas, particularly in the food industry, where it can produce throughout the value chain.

Importantly, issues of inequality significantly impact trade. Thailand should restructure production and trade to be more localized, developing skills for workers in the service sector who cannot return to their previous jobs, enabling them to acquire diverse skills for livelihoods that meet market demands both domestically and internationally, where skilled service workers from Thailand are still in demand. Additionally, we must enhance production efficiency in both agriculture and industry, ensuring that everyone can access systems quickly and comprehensively in a digital world.

High household and business debt levels are another factor hindering domestic spending, posing obstacles to exports, as commercial banks are reluctant to lend to businesses with high debt levels. Therefore, we must find ways for businesses at all levels to access funding sources, leading some businesses to survive while others may need to adapt and grow in new sectors, including returning to local production to restructure and optimize resource use.

Ultimately, it is crucial for Thailand to choose which value chain it will participate in within the region. How will it support and promote production and trade with regional countries in line with their differing capabilities? How can we produce high-value-added goods and services? We may be a destination for global production processes, but we could also be a starting point for regional production. Furthermore, trade liberalization is not just about accessing new markets but also about reforming the country's production and trade structures in ways that benefit the people.

The Office of the National Economic and Social Development Council (NESDC) indicates that the stability of the domestic economy remains good.

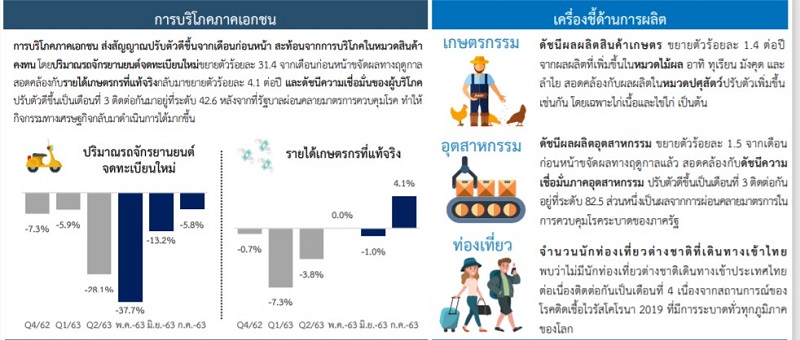

Mr. Wuttipong Jitthangskul, Economic Advisor, revealed that the Thai economy in July 2020, while still slowing down, showed improvement from the previous month, particularly in industrial production, exports, and private consumption, consistent with various economic confidence indices that have been improving continuously, partly due to supportive factors from measures that have relaxed restrictions to allow more economic activities.

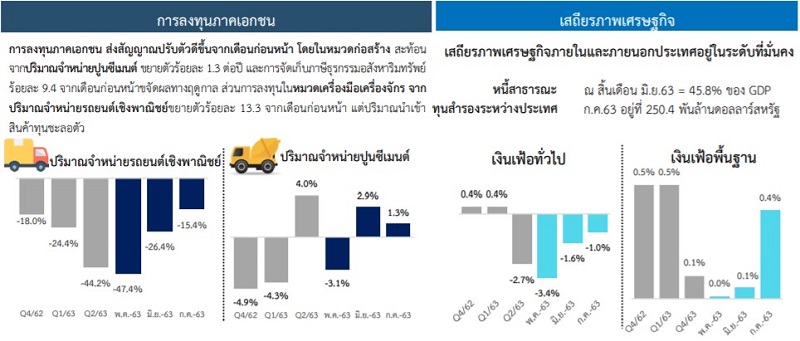

Indicators of private consumption show slight improvement from the previous month, particularly in durable goods consumption, as reflected by a 31.4% increase in new motorcycle registrations.

Indicators of private investment also show slight improvement from the previous month, with construction investments improving from the previous month, as evidenced by a 1.3% year-on-year increase in cement sales, consistent with a 9.4% increase in property transaction tax collection from the previous month.

The international trade sector has improved from the previous month, reflected in the value of exports in US dollars, which grew by 20.8% from the previous month, particularly in food products such as cassava products, palm oil, canned tuna, chilled and frozen pork, chilled and frozen chicken, and pet food, as well as products related to working from home.

When considering the value of exports by major trading partners, it is found that nearly all of Thailand's major trading partners have improved, with exports to the United States continuing to grow significantly for the second consecutive month at 17.8% year-on-year. Similarly, exports to Japan, the European Union, and the ASEAN-9 countries have contracted at rates of -17.5%, -16.0%, and -19.9% year-on-year, respectively, reflecting a gradual recovery trend as trading partners implement economic stimulus measures to accelerate recovery from the impact of COVID-19.

The stability of the domestic economy remains good, reflected by a general inflation rate of -1.0% year-on-year and a core inflation rate of 0.4% year-on-year. Meanwhile, the public debt ratio at the end of June 2020 stood at 45.8% of GDP, which remains within the fiscal discipline framework established under the Fiscal Responsibility Act of 2018. The external stability is also at a stable level, capable of withstanding risks from global economic volatility, as reflected by foreign reserves at the end of July 2020, which remained high at $274.5 billion.