Outlook Q2/2020: Where is the Thai Economy Heading?

Since February 2020, the world has faced a health crisis due to the COVID-19 pandemic, prompting many countries to implement stricter disease control measures starting from late February. These measures included social distancing policies, which led to a severe contraction of the global economy from the first quarter, continuing with the most intense impact in the first half of the second quarter, affecting economic activities in both the manufacturing and service sectors.

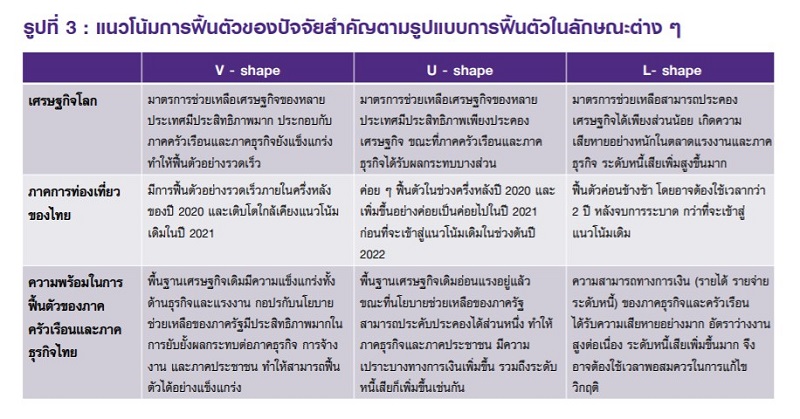

As the COVID-19 outbreak began to slow down, many countries, including Thailand, started to gradually ease lockdown measures. According to the Economic and Business Research Center of Siam Commercial Bank (EIC), it is estimated that the global economy in 2020 will experience a recession, with a revised contraction forecast of -4.0% YOY, marking the lowest level in 90 years. The recovery in the second half of the year is expected to be gradual (U-shaped recovery), meaning that the growth rate of the global economy in 2021 may not be sufficient to offset the contraction in 2020. Overall, the economic value in 2021 will remain below the level it would have been without the COVID-19 outbreak, assuming that each country's government can control the spread of COVID-19 and that there is no widespread second wave.

"Data from early Q2 indicates that the economies of several major countries contracted more than expected, reflecting the impact of strict lockdowns on economic activities broadly and severely."

In the second half of the year, the global economy is expected to recover as disease control measures are relaxed and governments worldwide implement financial and fiscal measures to mitigate the economic impact. However, the recovery will be gradual due to weak domestic demand, with household spending still affected by high unemployment rates and low consumer confidence. Meanwhile, private sector investment will be pressured by sluggish sales, increasingly fragile balance sheets, and high uncertainty, which may lead to a higher risk of defaults among households and businesses in many countries in the future.

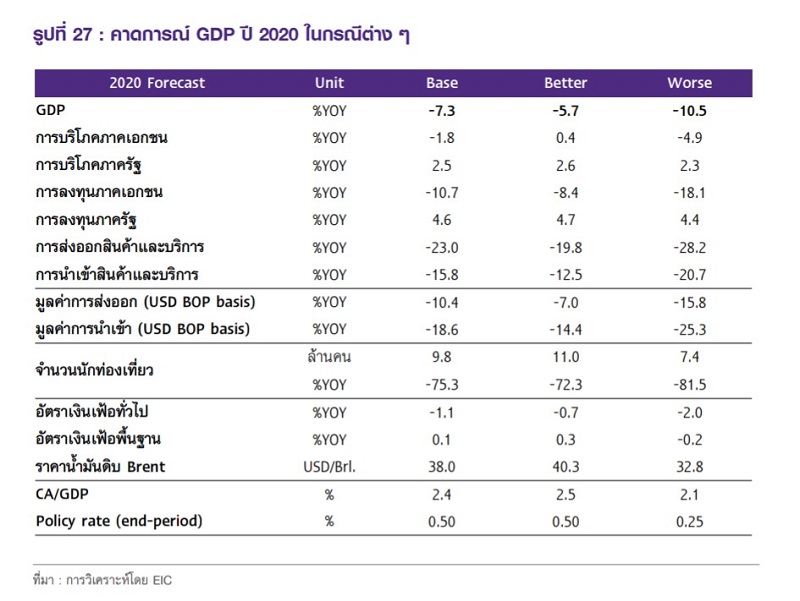

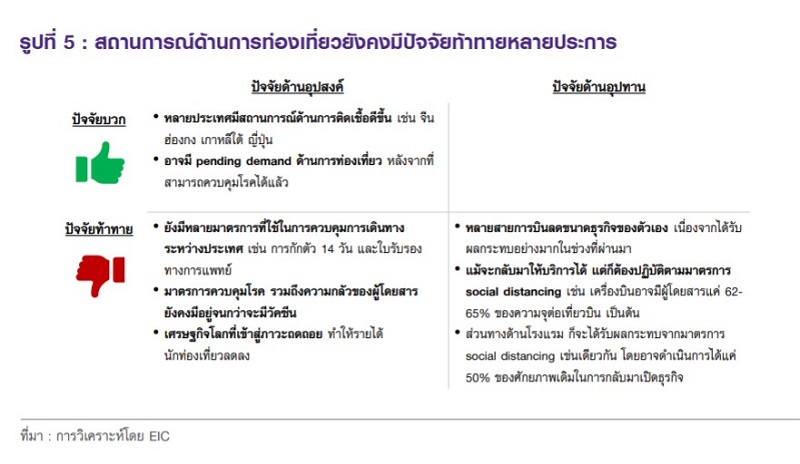

For the Thai economy in 2020, EIC has revised its forecast for a contraction greater than previously expected, from -5.6% to -7.3% due to the impact of COVID-19, especially in the tourism sector and private investment. EIC has reduced its forecast for foreign tourists in 2020 to only 9.8 million (-75.3% YOY) from the previous estimate of 13.1 million, following the extended travel restrictions in Thailand (recently extended until the end of June) and the gradual approach to reopening international travel by various countries, along with the greater-than-expected contraction of the global economy, which will affect tourist income.

Private sector investment is expected to contract further due to sluggish consumption and exports, along with a significant decline in business confidence. Exports are projected to contract sharply at -10.4%, close to expectations due to the global economic recession and lockdown measures in many countries, which have caused supply chain disruptions (however, the overall export value may contract less than the previous estimate of -12.9% due to a significant increase in gold exports, but gold exports do not have a net effect on GDP as they are not classified as economic activities).

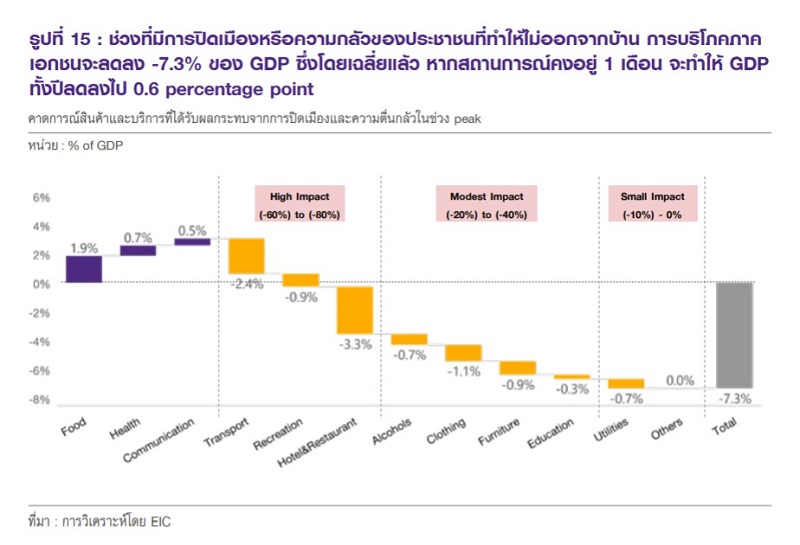

Private consumption has contracted severely, especially during the lockdown period, as reflected by the Consumer Index (PCI) in April, which contracted by over -15.1% YOY. Overall, EIC estimates that the lockdown will impact consumer spending, reducing it by -7.3% of GDP, or approximately 0.6 percentage points of GDP for each month of lockdown.

After the easing of lockdown measures, early indicators suggest that economic activities, particularly domestic travel, are showing signs of recovery, but still remain significantly below pre-crisis levels, as it is expected that most people will continue to exhibit cautious behavior and stay at home for some time. Therefore, overall spending on goods is likely to remain affected, although the impact may lessen somewhat, leading to a gradual recovery of the Thai economy, while the recovery of various business sectors will vary in speed.

“Overall, EIC estimates that the Thai economy will recover in a U-shape, with GDP returning to the levels of 2019, the pre-COVID-19 level, by 2022, due to the slowdown in the driving forces of the Thai economy and the increased financial fragility of households and SMEs even before COVID-19, as well as the severe impact of COVID-19 on several business sectors that are crucial to the Thai economy.”

For the recovery of the tourism sector, especially in areas dependent on foreign tourists, it will be slow due to tourists' concerns if an effective vaccine is not available and ongoing disease control measures, which will significantly impact related businesses such as hotels, restaurants, recreation, and transportation, leading to slow recovery.

The automotive and real estate (housing) sectors, which were already facing declining demand from abroad, will be further exacerbated by reduced domestic sales due to declining employment and household income, along with consumer confidence at historic lows. Additionally, the cautious lending practices of financial institutions will also result in slow recovery. In contrast, spending in essential goods and services, such as food, beverages, medical services, and communication, will recover faster due to support from government cash transfer measures and debt relief measures.

Key risks ahead include the global economy still facing pressures from domestic demand that may recover slowly, with a weak global labor market reflected in rapidly rising unemployment rates in recent times, creating uncertainty for household income and leading households to focus more on saving, which in turn affects consumer purchasing power. There is also an increased risk of household defaults. Furthermore, the global trade war may intensify and impact international trade volumes, particularly due to trade conflicts between the U.S. and China and Europe.

Should there be a severe resurgence of COVID-19 in a second wave, it could cause the economies of countries worldwide to stall again, resulting in prolonged global economic stagnation and increased economic value loss.

What will be the impact globally, and what direction will the Thai economy take next?

EIC assesses that in the near future, the Thai economy is likely to recover gradually (U-shaped) from an already weakened economy before COVID-19, coupled with a tourism sector that is expected to recover slowly, while households and businesses remain significantly fragile due to high debt levels.

According to estimates from the IMF, the global economy is expected to recover in a U-shape. While the IMF predicts a good recovery for the global economy in 2021, analyzing the GDP levels shows that both advanced and emerging economies are below their original trend lines, which aligns with the U-shaped definition mentioned earlier. Therefore, as the global economy is expected to recover slowly, it will also impact Thailand's export sector, which is a crucial part of the Thai economy.

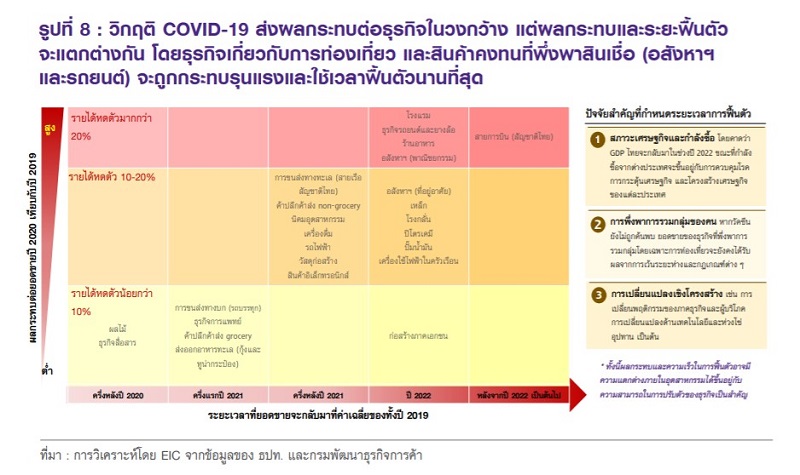

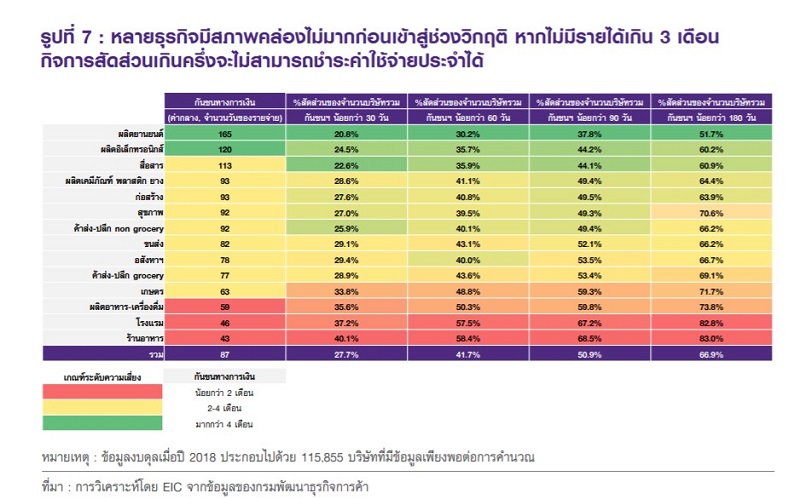

However, most businesses have been affected by COVID-19 and will take a considerable amount of time to recover, with the most concerning sectors being restaurants and hotels, as they were already vulnerable before the crisis and have been severely impacted, with a tendency for slow recovery.

Businesses affected by lockdown measures and social distancing, as well as the export sector, are expected to take a long time to recover, as they rely on consumer and tourist confidence, along with the recovery of consumer purchasing power, especially in durable goods that have been impacted by the economic slowdown in both export and domestic markets, such as the automotive and real estate sectors.

Additionally, lockdown measures have resulted in businesses that were ordered to close losing income, and consumer behavior has shifted, impacting the retail sector, which is expected to contract by -14% YOY, translating to a loss of around 500 billion baht from the retail market value of 2019, which was approximately 3.5 trillion baht, particularly affecting non-grocery stores, which sell non-essential items such as fashion, furniture, and electronics.

After governments in many countries began to gradually ease lockdown measures in May, economic activities started to show signs of recovery from the lowest point. The government plays a crucial role in supporting the economy and maintaining financial system stability.

Therefore, the government has implemented large-scale financial and fiscal measures to support the economy and maintain financial system stability. Global fiscal policies can be categorized into three types:

1) Policies supporting business operations

2) Policies supporting households

3) Policies increasing general government spending

Additionally, most central banks have lowered policy interest rates to the lowest levels in history and have introduced a wider variety of unconventional monetary measures, which can be categorized into four types: 1) Asset purchase measures 2) Lending measures for affected sectors 3) Liquidity support measures for businesses 4) Easing regulations for commercial banks.

“EIC has revised its global economic forecast for 2020 down to -4% YOY and estimates that the recovery of the global economy will be slow (U-shaped recovery), even though government financial and fiscal measures may partially mitigate the economic impact.”

References: Economic Intelligence Center (EIC)