Opportunities in the COVID-19 Crisis: Where to Invest After Lockdown

In a situation where the economy and stock market are highly volatile due to uncertainties from the COVID-19 crisis, what will investment opportunities look like in 2020? Join us for in-depth information for investors with Mr. Sukit Udomsirikul, Managing Director of Research at Siam Commercial Bank Securities (SCBS) and Dr. Kampon Adireksombat, Senior Director of Economic and Finance Market Research at SCB, in a discussion moderated by Mr. Sornchai Sunetta, Managing Director of the Chief Investment Office at Siam Commercial Bank Securities.

How Will the Economy Recover After COVID-19: V, U, or L Shape?

As the number of COVID-19 cases decreases and the country begins to ease lockdown measures, the stock market has already adjusted to the good news. After the severe impact on the economy in the second quarter, what will the Thai economy look like moving forward? Will it recover quickly? Dr. Kampon explains that the recovery can be defined in three shapes by economists: V Shape, U Shape, and L Shape. This is assessed based on growth figures compared to what was lost during the crisis. For instance, if the normal figure is +3%, during the crisis it drops to -3%, and then recovers to +5%, followed by +3% the next year, this is termed V Shape, indicating a recovery greater than what was lost during the crisis. If the normal figure is +3%, during the crisis it drops to -5%, and recovers to +3% the following year, this is termed U Shape. However, if the normal figure is +3%, during the crisis it drops to -7%, and recovers to +2.8%, followed by +2.8% the next year, this is termed L Shape.

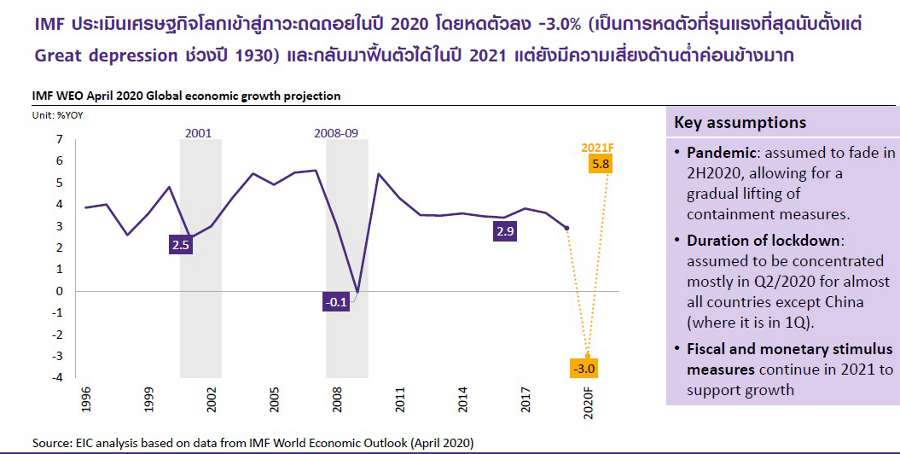

In 2020, the global economy is entering a recession, with the IMF predicting a contraction of -3%, similar to the Great Depression era. However, it is expected that in 2021, the global economy will improve by 5.8% based on three conditions: 1) COVID-19 must be controlled within the first half of 2020, 2) most countries must reopen after the second quarter to allow economic activities to resume, and 3) financial and fiscal measures used to stimulate the economy must be effective. Thus, the economy is expected to recover next year. The IMF views the recovery as a gradual U Shape, dependent on the three factors mentioned, as well as changes in consumer and producer behavior post-crisis.

How Do Government Measures Affect the Economic Machinery?

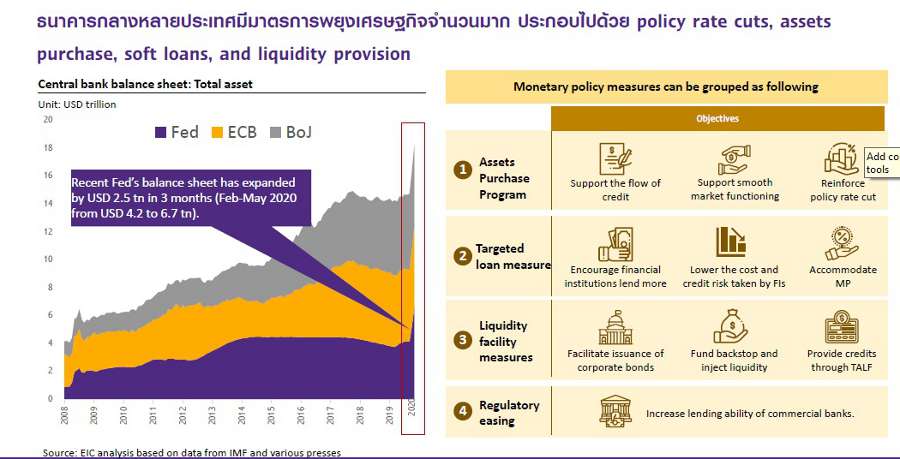

During the crisis, governments worldwide implemented massive financial measures to inject liquidity into the private sector, resulting in a global economy characterized by 1) high debt from bond issuance and budget deficits, 2) low growth, and 3) a trend towards isolationism (low globalization), which had been evident since the trade war. How will this situation impact the business sector, which drives the Thai economy?

In this regard, Dr. Kampon believes that the economy has a chance to recover, but it may take time. The COVID-19 crisis is different from previous crises because the government had to control the disease by ordering lockdowns, halting economic activities (sudden stop), which severely impacted the real economy and global financial markets, leading to a loss of liquidity and panic. Consequently, central banks worldwide, such as the FED, ECB, and BOJ, had to implement liquidity-boosting policies, such as lowering interest rates and unlimited quantitative easing (QE), to restore market confidence (calm the market down) by injecting a large amount of money quickly. Similarly, the Ministry of Finance had to support the economy to compensate for the lost income of businesses and individuals through unprecedented fiscal measures.

With policies from both the central bank and the government, the economy is expected to recover, following the sequence of business reopening. Initially, when COVID-19 broke out, uncertainty halted investments. As the virus spread, tourism ceased, and with city lockdowns, consumption and production stopped. As the number of infections decreases, businesses will gradually recover sector by sector. The first sector to recover will be daily consumer goods, as people still need to eat and use essential items, possibly shifting to online sales. As daily spending resumes, the production sector will also recover, starting with essential goods before luxury items. For exports, businesses producing goods for countries that have already recovered, like China, will bounce back sooner than others.

As travel becomes easier, tourism will begin to return, starting domestically, followed by the reopening of international travel. If effective treatments or vaccines are developed to control the disease, and there is confidence in avoiding a second outbreak, international investments will also resume.

Current and Future Outlook for the Thai Stock Market

In Mr. Sukit's view, the Thai stock market has passed its worst point compared to March when the circuit breaker was triggered. At that time, investors feared COVID-19 and a severe economic downturn, leading them to hold cash, causing the market to drop over 950 points. However, with the government and central banks worldwide injecting liquidity and implementing measures to mitigate the impact during the lockdown, the investment situation in the stock market has improved, restoring investor confidence and alleviating market pressure. Additionally, investors believe that stock prices were too low, prompting them to return to the market, and the easing of lockdowns has also contributed to the market's recovery. Stocks that have rebounded quickly are partly those heavily impacted by COVID-19. Overall, the hope for reopening cities has driven the index to test the 1,200 point level.

Although the second quarter profit figures are expected to be poor, stock prices in the market have risen significantly. Regarding whether stock prices are too high compared to the past and if they can continue to rise, Mr. Sukit believes it is essential to divide this into two points: 1) The stock market is not currently looking at this year's profits but is anticipating next year's profits. Even though first-quarter profits are expected to drop by about half and decrease further in the second quarter, the nature of the stock market is to decline before the economy and earnings reports are released. For example, if it is believed that profits will decrease in the second quarter, the stock market will decline starting in the first quarter and will begin to look for recovery in the second half of the year.

As for the question of whether stock prices are already too high, Mr. Sukit explains that if we compare the overall profit figures of companies in the stock market this year with current stock prices, the answer is yes, they are high. If we use profit figures for the next 12 months to compare with current stock prices, the answer is still yes. What the stock market indicates today is that there is confidence that profits in the next 12 months will improve, resembling a V Shape, which differs from the expectation that the economy will recover in a U Shape. In Mr. Sukit's view, it is unlikely that the Thai stock market will rise above 1,300 points, and volatility is expected.

The factors driving the market include: 1) Investor confidence, which is influenced by government measures, 2) Expectations for recovery, and 3) For the stock market to continue rising, it must rely on actual earnings, which is still too early to be confident about, especially as we have just begun to ease lockdown measures.

What Impact Will Rising Public Debt Have?

Dr. Kampon believes that as governments worldwide have implemented unprecedented massive liquidity injections to mitigate the economic impact of lost income during lockdowns, they have had to issue bonds to raise funds, resulting in increased public debt. The side effects of these measures are evident in the massive liquidity and low interest rates that will persist for some time. Because the government is borrowing a lot through bond issuance, if interest rates rise quickly, the government will have to pay high interest. Therefore, keeping interest rates low means the government does not have to pay high interest, which stimulates economic growth. To assess whether public debt is high, it should be compared to GDP figures. If GDP can recover quickly, the ratio of public debt to GDP will also decrease rapidly.

In this regard, Mr. Sukit adds that high debt will affect purchasing power and consumption. If public debt is high, it will reduce the role of government spending and investment, but private investment will take its place. In this low-interest environment, investment strategies can be defined by choosing to invest in defensive stocks, such as essential goods and services, and those offering dividend yields, such as real estate funds and infrastructure, which are assets that provide returns in a low-interest environment with uncertainty.

Will Liquidity Be Withdrawn After the COVID Crisis?

There is a question about whether, with so much liquidity in the system, after the COVID crisis passes and economic figures improve next year, governments worldwide will reduce their injections and withdraw liquidity, known as QE Tapering, potentially causing the stock market to experience significant declines. In Mr. Sukit's view, the issue of withdrawing liquidity can be seen in two dimensions: 1) For the business sector, it may happen gradually, and 2) For the financial sector, QE Tapering may occur, as seen in 2013. The funds injected from 2009 to 2013 benefited emerging markets, including Thailand, which received about 200 billion baht. Therefore, when QE Tapering occurred in 2013, the Thai stock market experienced a significant decline.

Mr. Sukit believes that this time, the liquidity injected has not yet reached emerging markets. Since the beginning of the year, the Thai stock market has seen net foreign sales of about 170 billion baht and around 100 billion baht in the bond market. If this trend continues, the impact of QE Tapering this time is unlikely to be severe on the Thai stock market. Regarding where the injected funds are currently, part of it is in developed markets like Japan and the USA, while another portion is likely in the bond market, as most central banks focus on helping private debt securities refinance/roll over due to last month's panic sell in the bond market. In summary, there is a possibility of QE Tapering this time, but it is unlikely to happen this year; it may occur next year when the COVID situation improves, so keep an eye on developed countries and the bond market.

What Lessons Has COVID Taught the Economy?

Mr. Sornchai notes the economic policies in many countries that focus primarily on increasing GDP figures. However, the COVID situation has taught countries that when faced with shortages of consumer goods and medical supplies, governments must shift their focus to these essential items rather than just monetary growth. Dr. Kampon comments that over the past 20-30 years, international trade policies have emphasized maximum efficiency and profit, leading to the creation of a Global Supply Chain through outsourcing production to reduce costs, becoming a trend of globalization. However, in recent times, particularly during President Trump's era in the U.S., there have been questions about whether this form of globalization is appropriate if it negatively impacts domestic industries and people's livelihoods. Even before COVID-19, there were issues related to trade wars, such as the high-tech goods sector being affected. The COVID crisis has further highlighted that despite high production efficiency, outsourcing production abroad can lead to shortages of essential items, like masks and medical equipment, during emergencies.

Given both the trade war and the COVID crisis, it is expected that the likelihood of returning to full globalization as seen in the past 1-2 decades will be low. The trend may shift towards regionalization, where supply chains are more localized rather than spread globally as before. Additionally, governments may regulate that certain critical industries produce domestically to ensure availability during emergencies, such as masks and essential medical equipment, which will be crucial for businesses to consider, even as they ultimately aim for maximum profitability.

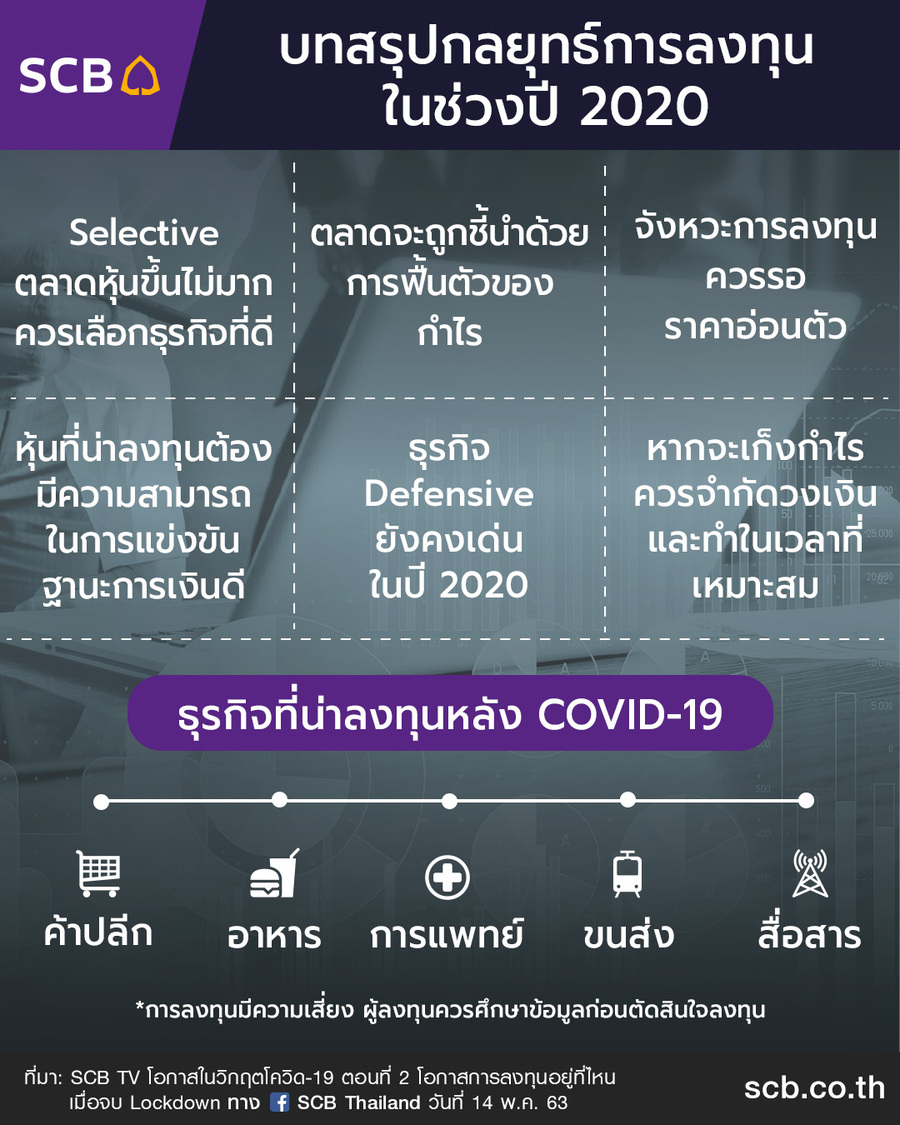

Investment Strategy Summary for 2020

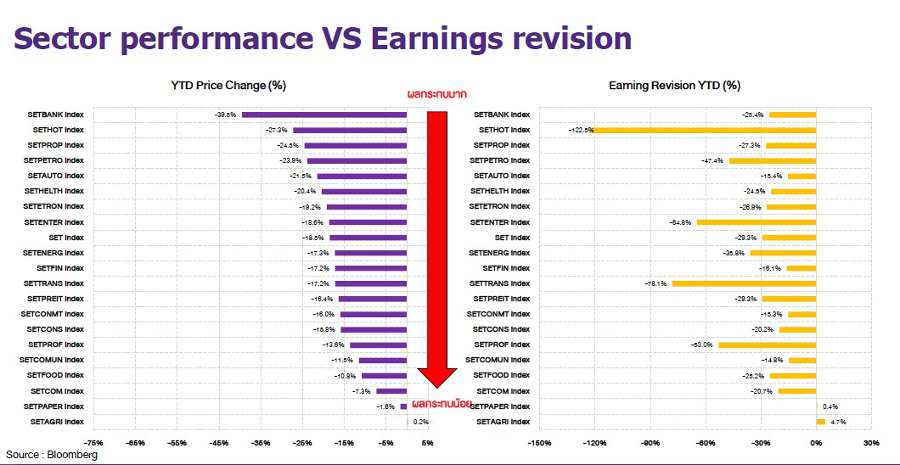

Despite a projected 30% decline in total net profit for the SET in 2020, it remains higher than the total net profit figures during the 1997 Tom Yum Kung crisis and the 2008 Hamburger crisis, reflecting that listed companies in the stock market have better fundamentals than during the previous two crises. SCBS estimates that this year, net profit will decrease from 672,953 million baht in 2019 by about 21% to 534,565 million baht, and in 2021, it will adjust to 668,506 million baht, indicating a U-shaped recovery that will take some time.

Mr. Sukit believes that industries of interest post-COVID crisis should be evaluated based on impact factors, divided into two dimensions: those less affected, such as the infrastructure sector (e.g., power plants) and food businesses, and those affected but recovering faster, such as retail, medical, and domestic transport (excluding aviation) and telecommunications. Meanwhile, sectors with high uncertainty, such as aviation, tourism, and consumer goods like homes and cars, are currently considered risky. For 2020-2021, the SET index is projected to be between 1,450 and 1,150 points, with standout stocks for investment during this period including BDMS, CPF, BEM, BTS, and MINT, which are leaders in their respective sectors and currently have relatively low prices with higher returns than the market index.

SOURCE: www.scb.co.th