EIC Assesses COVID Crisis: Unemployment Hits Record High, Straining Households with Only 3 Months of Savings

The EIC assesses that the 2020 crisis has broadly impacted the labor force, risking unprecedented unemployment and exacerbating the vulnerability of households.

- The Thai economy is currently in a crisis with an uncertain endpoint due to the COVID-19 pandemic, which has affected nearly every business sector, particularly the tourism industry. This crisis poses a risk to the labor market, which has shown signs of weakness even before the pandemic. The most at-risk groups include temporary workers, freelancers, and employees of SMEs, who make up 62% of the Thai workforce and are highly sensitive to economic conditions.

- The EIC estimates that the number of unemployed individuals could rise to approximately 3-5 million, a level higher than any previous crisis in Thailand. This is due to the widespread impact of the pandemic and the sudden halt of many economic activities, while the agricultural sector may not be able to absorb unemployed workers from other sectors as it has in the past due to drought issues.

- The EIC believes that many workers, even if not unemployed, will see a significant reduction in working hours and income, with some potentially earning nothing during certain periods. The recovery of the labor market is expected to be slow, following a U-shaped economic recovery, and the effects of COVID-19 will persist until a treatment or vaccine is available.

- The risks in the labor market are likely to continue affecting the quality of life for already vulnerable households, with about 60% of Thai households having insufficient financial assets to cover expenses for more than three months.

The EIC has identified several signs of weakness in the Thai labor market even before the COVID-19 crisis:

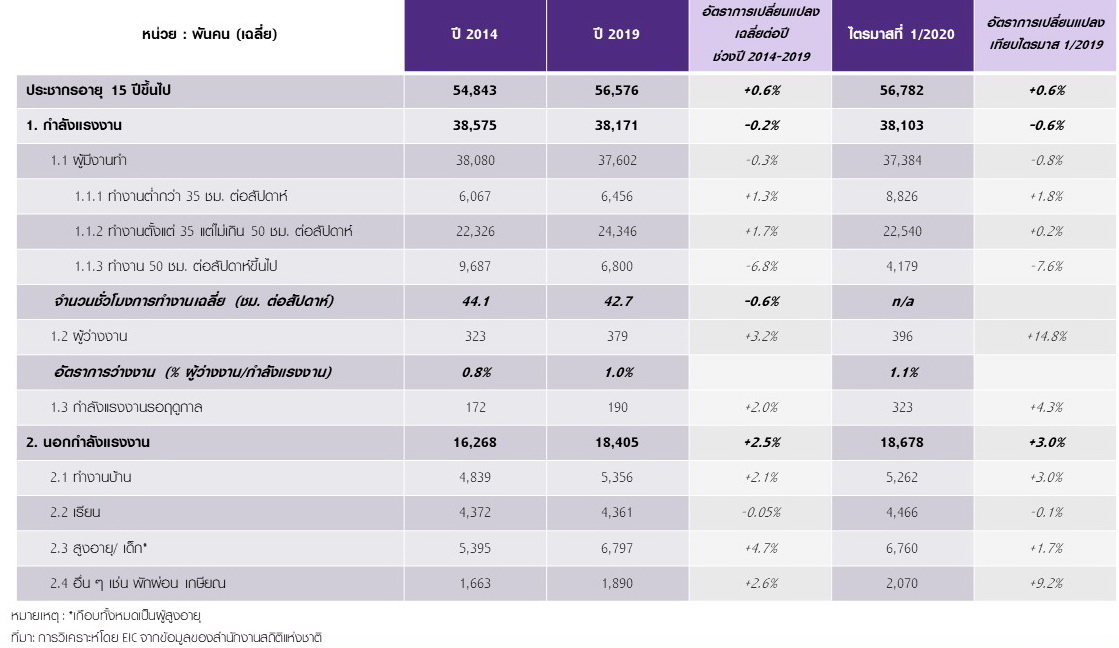

1) Decrease in Employment According to the National Statistical Office, the number of employed individuals in Thailand has been declining over the past few years, with an average of 37.6 million employed in 2019, down by 480,000 compared to the average in 2014. This decline is attributed to both cyclical factors, such as the economic slowdown reducing labor demand, and structural factors, particularly the exit of older workers from the labor force, which increased from 5.4 to 6.8 million during the same period. The average number of employed individuals in the first quarter of this year is still on a downward trend, at 37.4 million, a decrease of -0.8% YOY, marking four consecutive quarters of contraction.

2) Decrease in Working Hours The average working hours for Thai workers in 2019 were 42.7 hours per week, a continuous decline from 44.1 hours per week in 2014. This decline is primarily due to a reduction in the number of overtime workers (those working 50 hours or more per week), which decreased from 9.7 to 6.8 million, a loss of 2.9 million during that period. The trend of decreasing working hours continues to be observed in the first quarter of this year, reflected by a -7.6% YOY decline in the number of overtime workers.

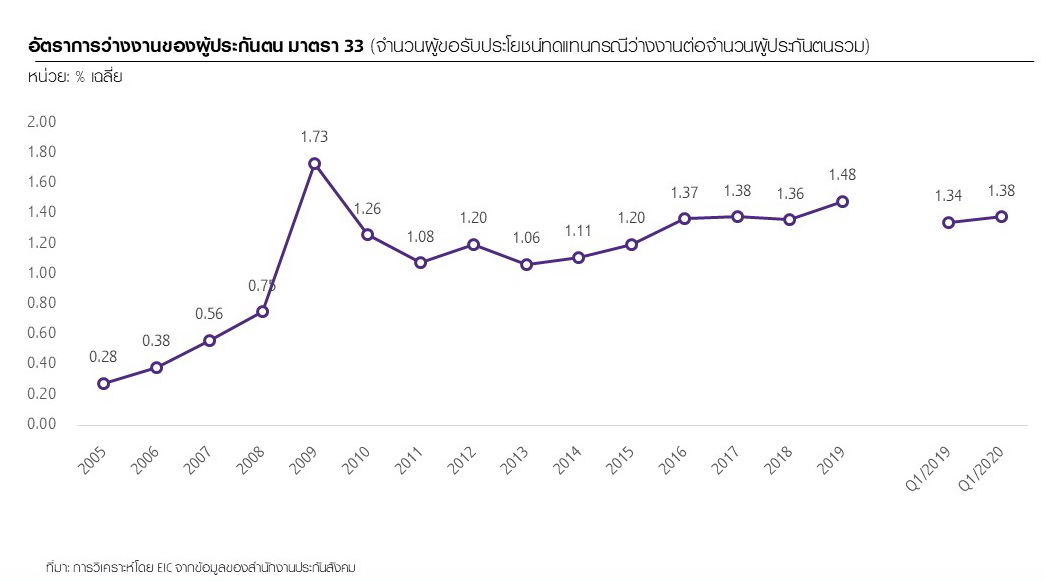

3) Increase in Unemployment The average number of unemployed individuals in the first quarter of this year is approximately 400,000, an increase of 14.8% YOY, marking three consecutive quarters of increase. Additionally, data from the Social Security Office shows that in the first quarter of 2020, the average number of insured individuals who were unemployed was 160,000, up 4.5% YOY, with the unemployment rate among insured individuals under Section 33 continuously increasing since the global financial crisis of 2008-2009.

Working Conditions of the Thai Population

Given the pre-existing weakness in the labor market, combined with multiple negative factors such as the COVID-19 outbreak, global economic contraction, and drought issues, this crisis is expected to have widespread impacts on labor across various industries. The sectors most at risk are undoubtedly those related to tourism, including hotels, restaurants, entertainment, and retail, as they are directly affected by the loss of tourists and lockdown measures.

Other business sectors will also experience significant direct and indirect impacts from the severe economic downturn and the anticipated slow recovery (U-shaped recovery). Labor in the agricultural sector will be particularly affected by severe drought this year and may also face indirect impacts from reduced purchasing power, limiting their ability to absorb unemployed workers from other sectors during this crisis.

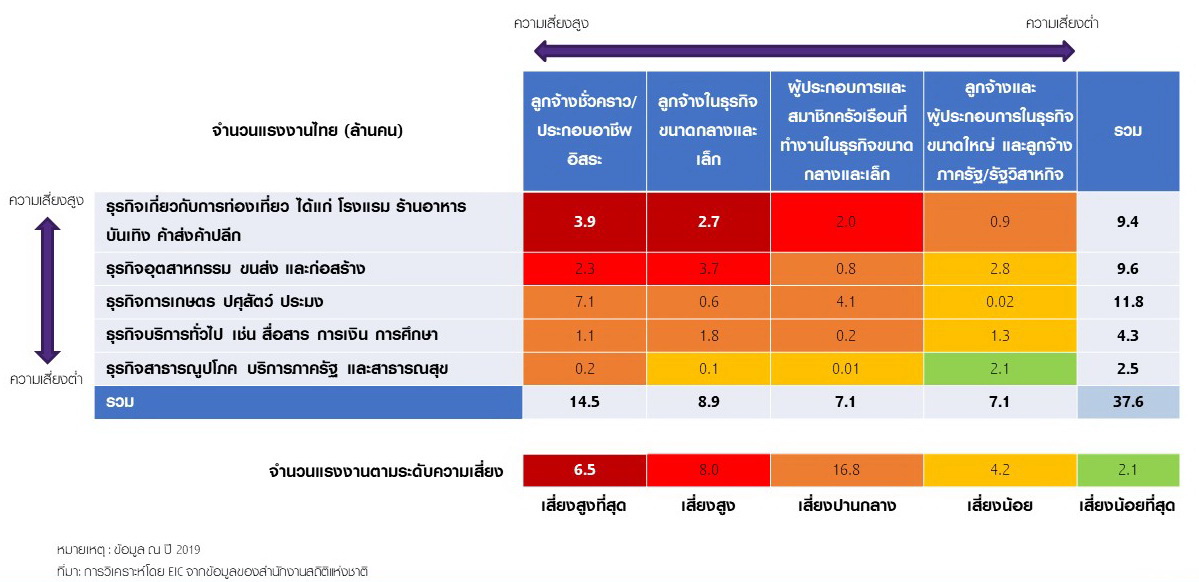

The EIC believes that the nature of employment will be another crucial factor affecting income risk and job security. Temporary workers, freelancers, and employees of SMEs, totaling 23.4 million, represent 62.2% of total employment and are often sensitive to economic conditions, making them a high-risk group across all business sectors.

Considering both business sectors and employment characteristics, the highest-risk labor group will be temporary workers, freelancers, and SME employees in the tourism industry, totaling 6.5 million, or 17.3% of total employment. Following them are SME operators in tourism and those with similar employment characteristics in affected sectors such as industry, transportation, and construction. Employees in large businesses and the public sector are likely to face lower risks; however, they represent a minority of total employment.

Risk Levels for Thai Labor in the 2020 Economic Crisis

Given the risk levels, the EIC estimates that the number of unemployed individuals could rise to approximately 3-5 million, which would represent an unemployment rate of about 8%-13% of the current labor force, the highest level recorded since data collection began in 1985. This would surpass the previous record high unemployment rate of 5.9% in 1987, far exceeding the unemployment rate during the Tom Yum Goong crisis at 3.4% in 1998 and the global financial crisis of 2008-09 at 1.5% in 2009.

The reason for the expected higher unemployment this time is due to the widespread impact of the economic crisis on business sectors and households that have been vulnerable even before the pandemic, compounded by lockdown measures necessary to control the outbreak, which have led to a sudden halt in economic activities. Additionally, the agricultural sector, which has traditionally absorbed labor, is likely to face limitations in fulfilling that role this time due to severe drought issues.

The EIC also anticipates that many workers, even if not unemployed, will see a significant reduction in working hours and income, with some potentially earning nothing during certain periods. If the impacts extend into the second half of the year or longer, the number of unemployed could rise significantly beyond the initial estimates due to more businesses closing, particularly in high-risk sectors with insufficient liquidity.

After the lockdown measures are lifted, the labor market situation is expected to improve, but recovery will be slow, following a U-shaped economic recovery, with the effects of COVID-19 continuing to impact the economy and people's lives until a treatment or vaccine is available. Businesses are likely to remain cautious in spending and hiring due to the ongoing uncertainties in such a situation.

Loss of income and unemployment will lead to significant distress for many households due to limited financial buffers.

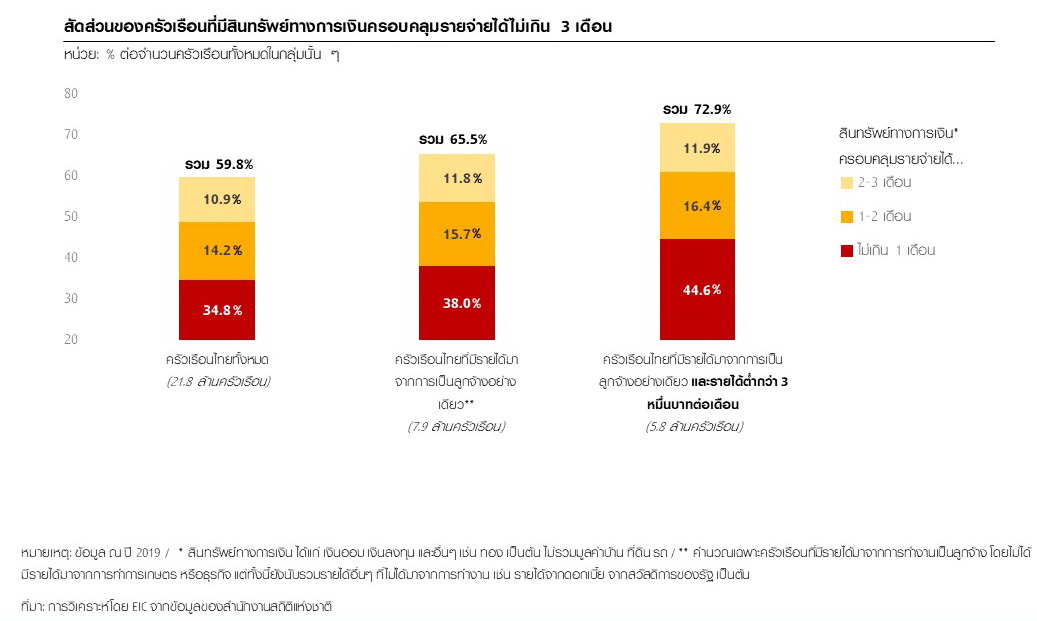

According to the 2019 household economic and social survey, there are 7.9 million households in Thailand that rely solely on income from wage labor, accounting for approximately 36.2% of all households. Among this group, 5.2 million households, or 65.5%, have financial assets covering expenses for no more than three months.

If we consider households earning less than 30,000 baht per month, there are 4.3 million out of a total of 5.8 million households, or 72.9%, that have insufficient financial assets to cover expenses for three months. This will likely force these households to significantly reduce consumption, sell or mortgage their assets, or incur debt to cover expenses, further increasing their vulnerability in the future.

SOURCE: www.thaipublica.org