World Bank Concerned About Household Debt Among Low-Income Groups - Political Factors as Economic Risks for Thailand

The October 2019 edition of the East Asia and Pacific Economic Update, titled "Weathering Growing Risks," published today (October 10, 2019), reveals that the weakening global market demand, including a decline in demand from China, along with increasing uncertainty in trade tensions between the United States and China, has led to a decrease in export and investment growth, posing a test of the region's economic resilience.

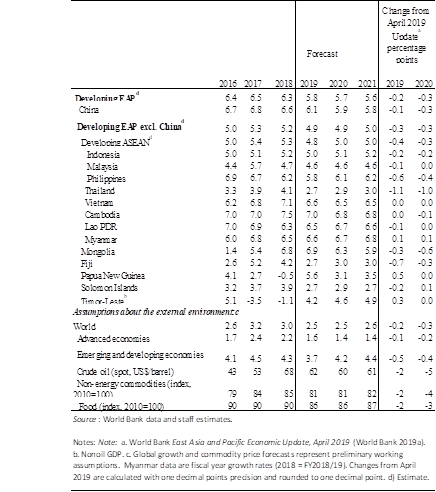

The economies of developing countries in the East Asia and Pacific region have slowed from a growth rate of 6.3% in 2018 to 5.8% in 2019, and are projected to further decline to 5.7% and 5.6% in 2020 and 2021, respectively, reflecting a broad decline in export growth and manufacturing activity.

In this region, excluding China, consumption continues to grow, albeit slightly lower than the same period last year, supported by monetary and fiscal policies. Meanwhile, small economies in the region have shown strong growth, particularly in tourism, real estate, and mining, reflecting the unique contexts of each country.

"As economic growth slows, the rate of poverty reduction will also decline," said Victoria Kwakwa, World Bank Vice President for East Asia and Pacific. "Currently, we estimate that nearly one in four people in developing countries in East Asia and the Pacific live below the poverty line of $5.5 per day, which translates to nearly 7 million people, a figure we projected back in April when the region's economy was still growing strongly."

The report clearly states that increasing trade tensions are adversely affecting the long-term economic growth of the region. While some countries hope to benefit from the new global trade patterns, the inflexibility of global value chains means that countries in the region are unlikely to gain from this in the short term.

"As companies seek ways to avoid tariffs, it becomes challenging for developing countries in East Asia and the Pacific to replace China's role in global value chains in the short term due to insufficient infrastructure and limited production capacity," said Andrew Mason, Chief Economist for the East Asia and Pacific region.

The report warns of increasing negative risks to economic outlooks. Prolonged trade tensions between China and the United States will continue to adversely affect investment growth due to high uncertainty. China's economy is slowing faster than anticipated, issues in the European Union and the United States, along with ongoing turmoil regarding Brexit, may lead to a further decline in demand for exports from this region.

Additionally, high and rising debt levels in some countries limit the ability to use fiscal and monetary policies to mitigate the impacts of the global economic slowdown. Sudden changes in global financial conditions could increase borrowing costs, leading to stagnant credit growth, which may affect private investment and economic growth in the region.

Although the global economy remains at increasing risk, the report advises countries to prepare appropriate policies for fiscal measures or monetary policies to stimulate the economy while safeguarding fiscal sustainability and debt levels. Countries in the region will benefit from trade openness and increased regional trade integration.

The trade conflict between the United States and China, coupled with the global economic slowdown, requires countries in the region to reform to improve productivity and economic growth, including regulatory reforms that will facilitate trade and investment, attracting more foreign investment, and easing the transport of goods, technology, and knowledge transfer.

Concerns Over Household Debt and Political Economic Risks

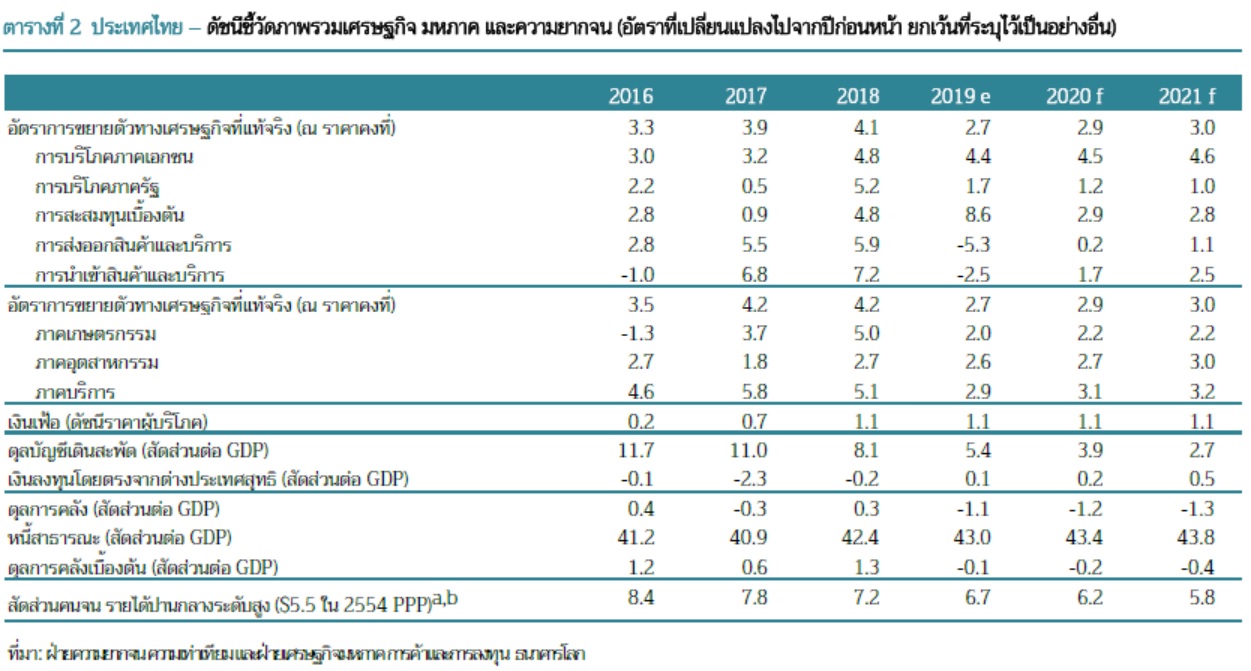

Recently, Thailand's economy has expanded moderately for the second consecutive quarter due to shrinking exports and weakening domestic demand. Exports of goods and services fell by 6.1% and 7.0% in the first and second quarters of 2019, respectively. Domestic demand, a key driver, showed signs of weakening, with private consumption growth stabilizing at a moderate level of 4.9% in the first quarter and 4.4% in the second quarter of 2019. Consumer confidence dropped to its lowest level in 22 months in July due to concerns about economic slowdown, political instability, trade tensions between the United States and China, and low agricultural prices.

The growth rate of private investment decreased by more than half from 4.4% in the first quarter to only 2.2% in the second quarter, while investors faced pressure. Public investment expanded only moderately at 1.4% in the second quarter of 2019 due to delays in implementing public infrastructure investment plans amid a prolonged government transition that took four months to establish a new government after the election. Agricultural output fell by 1.1% in the second quarter of 2019, while the industrial sector contracted by 0.2% (growing 0.6% in the first quarter of 2019), aligning with the decline in exports.

Financial and fiscal buffers remain sufficient, reflected by slowing public spending, low inflation, and a low public debt-to-GDP ratio, along with a small and stable fiscal deficit in the first half of 2019. Although government revenue has decreased, the growth rate of public spending has also slowed. Therefore, it was unexpected that the Bank of Thailand announced a 0.25% reduction in the policy interest rate to 1.5% on August 7, 2019, to mitigate the impact of the slowing global economy.

Weak export potential has narrowed the current account surplus in the second quarter of 2019. However, the level of foreign reserves remains sufficient for imports and short-term external debt. The Thai baht appreciated to its highest level against the US dollar in six years in late August. The financial sector remains stable with strong commercial bank capital buffers. However, high household debt remains a concern, particularly among low-income households.

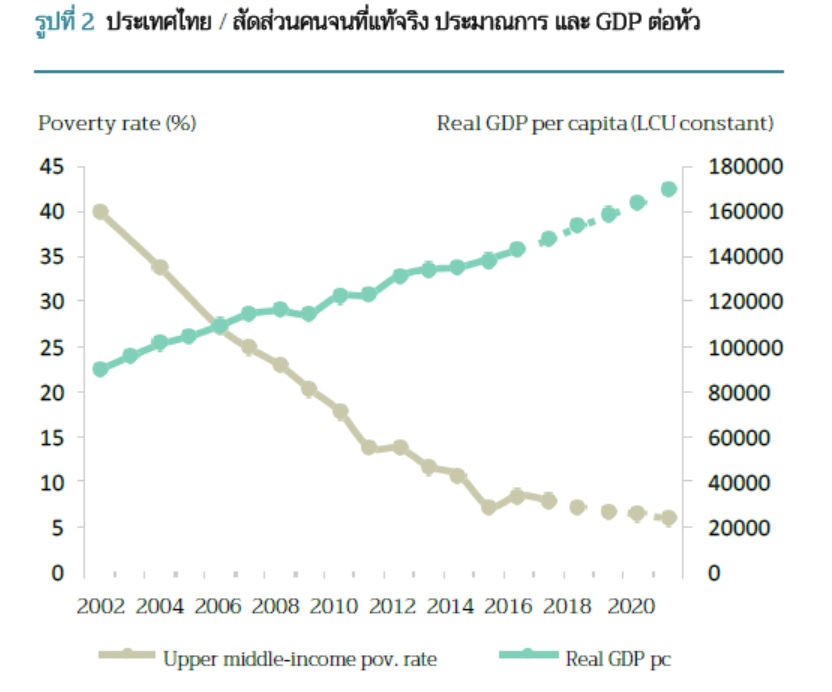

Although extreme poverty is low, the reduction of poverty has stabilized, and poverty in some regions has increased between 2015 and 2017. Employment in agriculture, agricultural price indices, and income from agriculture are all trending downward, negatively impacting the welfare of the poorest 40% of households according to income distribution metrics. State policies currently under consideration include increasing funds for elderly care and expanding registration for those eligible for state welfare cards.

The report forecasts that Thailand's economy will grow only 2.7% in 2019 and 2.9% in 2020. The projected economic growth rate for 2019 has been revised down from 3.5% to 2.7% due to several factors, including: 1) a larger-than-expected decline in exports during the first half of 2019; 2) Thailand experiencing its worst drought in a decade; 3) low public investment disbursement rates hindering public investment figures. Economic stimulus measures announced in August 2019 target farmers, small and medium enterprises, and low-income households through direct cash transfers and extended debt repayment periods.

Tax refunds from tourism activities and the extension of visa exemptions for travelers from designated countries are among the measures that are unlikely to have a significant impact on economic growth in 2019. In the medium term, the impact of these measures will depend on the strength of fiscal multipliers.

The new government's non-fiscal policies emphasize the country's competitiveness, sector-specific development, and overall growth. There is continuity in implementing major policies and projects, such as the Eastern Economic Corridor, and expanding measures targeting the agricultural sector, for example, income guarantees, stabilizing agricultural prices, and improving productivity across the agricultural supply chain.

Fundamentally, private consumption and investment are expected to recover and drive the economy in the medium term, supported by expectations that public investment will resume as large infrastructure investments begin. Trade and investment in the region, particularly in Cambodia, Laos, Myanmar, and Vietnam, will help mitigate external headwinds.

The risk scenario is trending negatively. Political uncertainty remains the most significant risk factor that could raise doubts about the stability of the new coalition government formed from 19 political parties. Delays in implementing large public infrastructure investment plans may negatively impact investor sentiment and consumer confidence.

Ultimately, this may weaken domestic demand. Although projects related to the Eastern Economic Corridor are progressing, there is still a risk of delays in implementation. Increasing trade tensions between the United States and China may further weaken demand for Thai exports and undermine private investment, particularly in export-oriented industries.

The Thai baht was the strongest in the region in mid-2019 as foreign investors sought refuge in Thailand's bond market. If the baht continues to appreciate, it may hinder the competitiveness of Thai exports in both the industrial and tourism sectors.

Thank you for the information from thaipublica.org