World Bank Highlights Global Trade Tensions Impacting Investment, Urges Developing Countries to Think Before Accumulating New Debt

The World Bank has released a report titled Global Economic Prospects: Heightened Tensions, Subdued Investment, indicating that the global economy is slowing at its lowest rate in three years. While it remains stable, the outlook is still fragile with multiple risks.

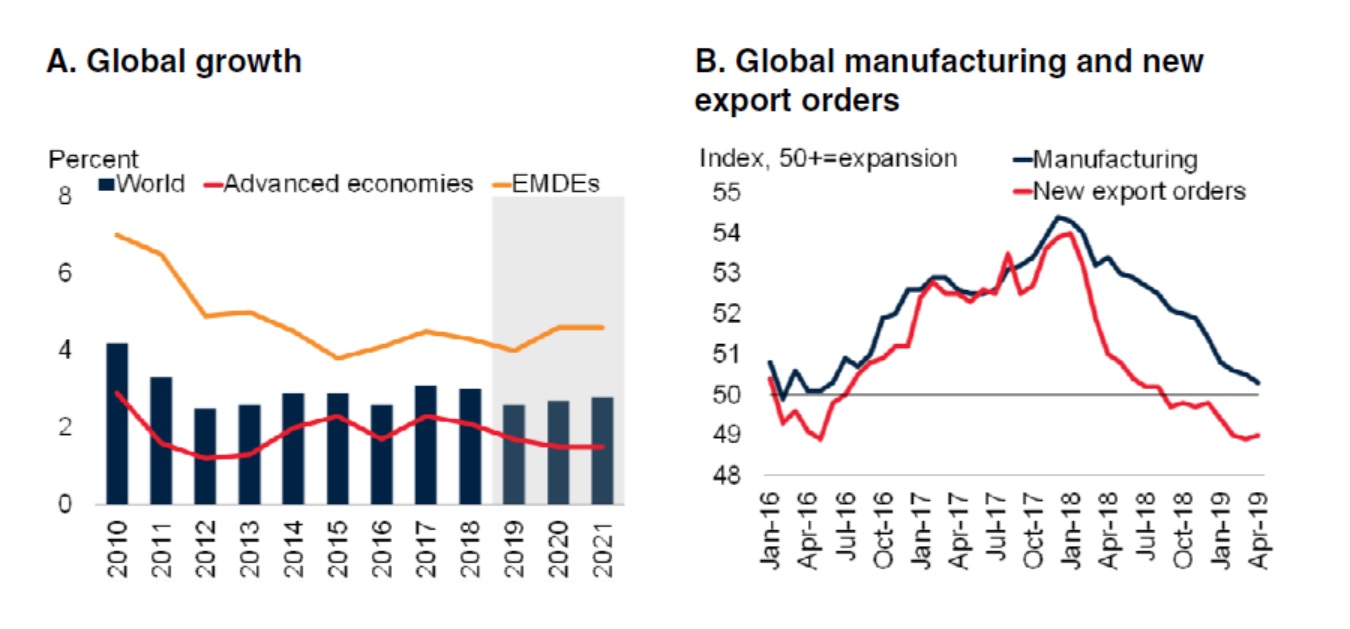

The World Bank estimates global economic growth for this year at 2.6%, down from 2.9%, before improving to 2.7% in 2020.

International trade and investment have been weaker than expected since the beginning of the year, with significant domestic economic activity, particularly in the Eurozone and several large emerging economies, including developing countries where growth has been weaker than previously assessed.

Risks that could impact growth prospects include escalating trade conflicts among major economies, potential new financial crises in emerging and developing countries, and unexpected stagnation in large economies.

A primary concern is the slowdown in global trade, which has reached its lowest level since the financial crisis a decade ago, along with business confidence.

The U.S. economy is expected to grow by 2.5% this year and slow down to 1.7% in 2020, while the Eurozone is projected to grow by 1.4% this year and next, with trade and domestic demand affecting economic activity, despite ongoing support from monetary policy.

The Asia-Pacific region is expected to grow by 5.9% this year and next, marking the first time this region has grown below 6% since the financial crisis of 1997-1998. China is projected to grow by 6.2%, down from 6.6% last year, due to the slowdown in global trade, stable commodity prices, global financial conditions, and the government's ability to implement monetary and fiscal measures to address external challenges.

Other countries in the Asia-Pacific are expected to see economic growth decline to 5.1% before slightly recovering to 5.2% in the following years.

Growth in emerging and developing economies is expected to stabilize next year as volatility and uncertainty in many countries have decreased since late last year and this year.

The Global Economic Prospects report is published biannually in January and June, providing in-depth analysis of the macroeconomic development of major world economies and their impacts on other countries, along with policy recommendations to support achieving development goals.

Emerging and developing economies are projected to grow at a low of 4% this year, the lowest in four years, but will expand by 4.6% next year. Many countries are managing to cope with financial pressures and political uncertainties, and these impacts are expected to lessen.

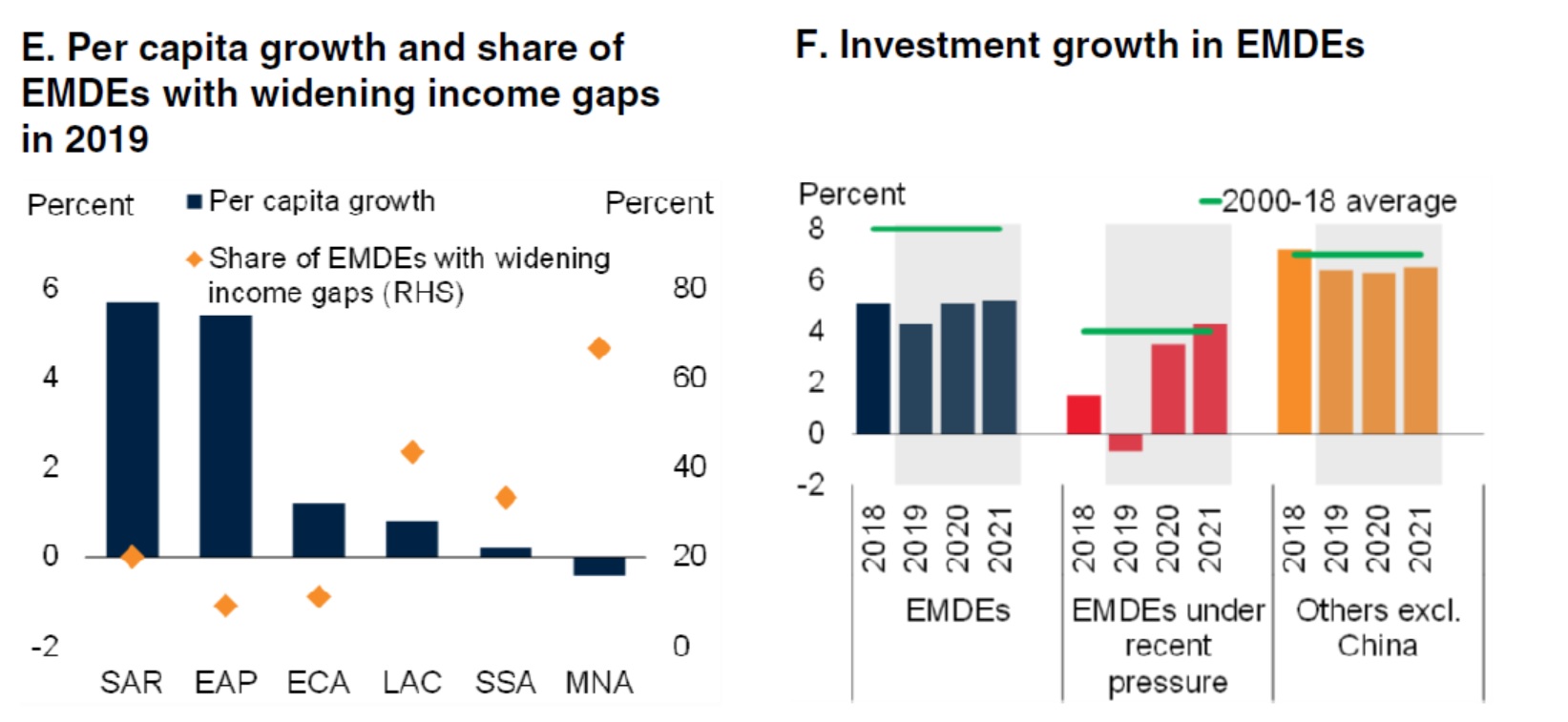

The economies of low- and middle-income countries are expected to grow by 6% in 2020, up from 5.4% this year, but this is still insufficient to reduce poverty. While some low-income countries have transitioned to middle-income status between 2000 and 2018, the remaining low-income countries face challenges in advancing to middle-income status due to their vulnerability, geographical disadvantages, and reliance on agriculture.

"Strong economic growth is crucial for reducing poverty and improving living standards," said David Malpass, President of the World Bank, adding that "current economic momentum is weak, and the rising debt burden and declining investment in developing countries hinder potential growth. Urgent structural reforms are needed to improve the business environment and attract investment, along with addressing debt burdens and ensuring transparency, which is paramount for new debt to foster growth and investment."

In addition to concerns about the global economic slowdown, slow investment growth raises worries about the long-term growth of emerging and developing economies. Although investment is starting to recover, it remains below the average levels of previous years.

Low investment levels in emerging and developing economies are a result of the global economic slowdown, fiscal policy constraints, and structural limitations. The recovery of investment is crucial for achieving development goals, and reforming the business environment will help promote private sector investment.

Slow investment growth is causing emerging and developing economies to lag behind advanced economies, while slow capital accumulation and transfer are affecting the productivity of these countries, widening the development gap over the next decade. The recovery of investment is essential for achieving sustainable development goals.

Allocating budgets away from non-productive sectors and improving spending efficiency is a way to stimulate public investment. Removing business constraints, creating a conducive business environment, addressing market inefficiencies, and strengthening corporate governance will also promote private sector investment. Additionally, governments can provide clarity in policy direction and reinforce their role in the global production chain.

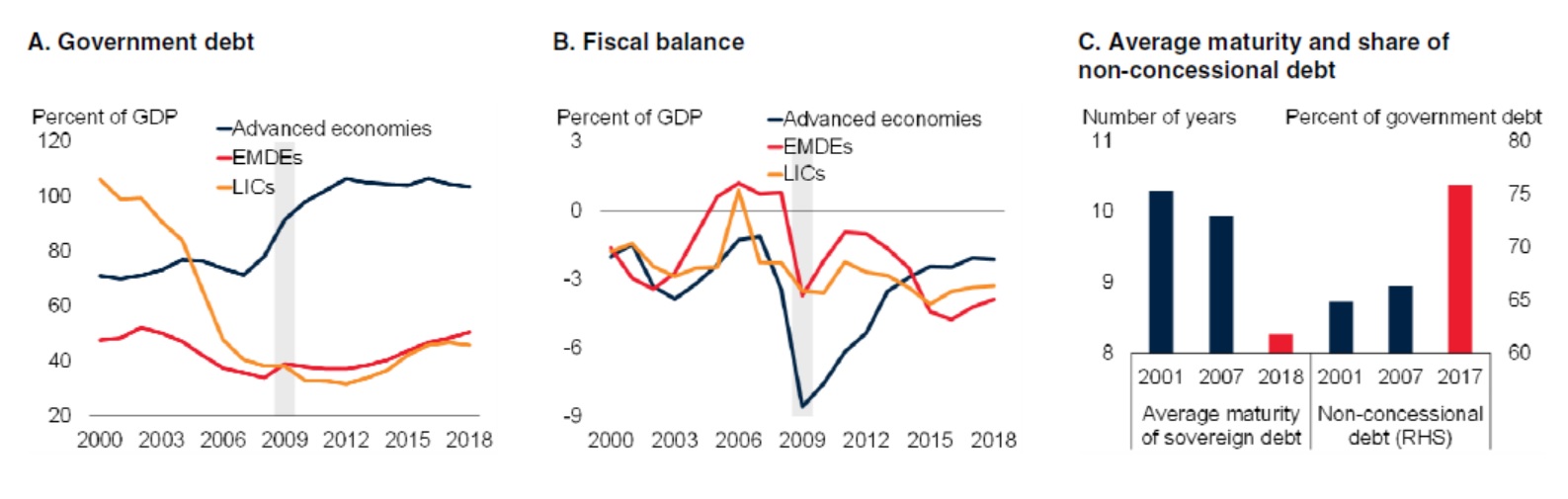

Developing countries often borrow to compensate for declining private sector investment, which increases financial stability risks if the global economy slows further. Increased trade barriers create financial pressures for countries reliant on trade.

"Currently, global interest rates are very low. Stagnant investment may lead governments to incur additional debt to finance growth-generating projects. However, historical financial crises indicate that debt is not free," said Ayhan Kose, head of the Prospects Group at the World Bank.

The report also indicates that rising debt levels are a concern, as many emerging and developing countries are borrowing heavily, while their ability to reduce public debt burdens has diminished compared to previous efforts to significantly lower debt before financial crises.

Debt in emerging and developing countries increased by an average of 15 percentage points to 51% of GDP in 2018. While this increase in debt is acceptable to support growth-impacting projects such as investments in infrastructure, health, and education, the demand for these is immense.

However, excessive debt poses high risks. Even in periods of low interest rates, debt can escalate to unsustainable levels.

Government spending is primarily directed towards debt repayment, limiting allocations to other critical areas. High debt burdens may also lead governments to increase tax rates to offset budget deficits, impacting businesses and consumer spending. In the worst-case scenario, rising debt could lead to defaults requiring bailouts.

Emerging and developing countries must balance economic growth with debt accumulation and avoid the risks associated with massive debt. Additionally, prudent government spending will help these countries navigate economic downturns.

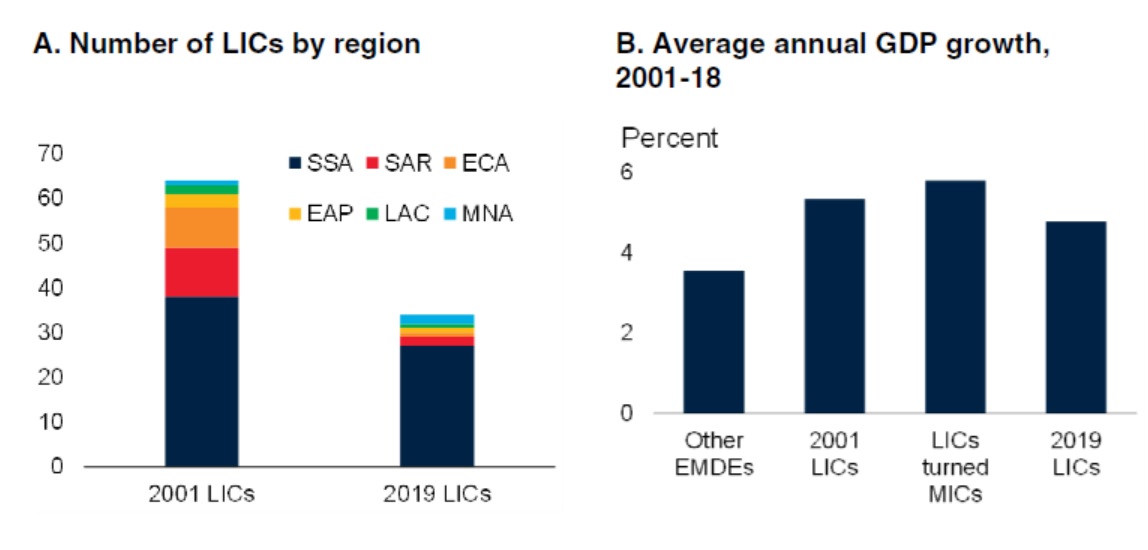

For low-income countries, the report states that the number of low-income countries has decreased from 64 in 2001 to 34 in 2019 due to reduced conflicts in many countries, decreased debt burdens, and trade with larger, growing economies. However, the challenges faced by the remaining low-income countries are greater than those that have transitioned to middle-income status.

The World Bank analysis found that low-income countries (with annual incomes of $995 or less) and middle-income countries require approximately $640 billion to $2.7 trillion in annual investments to achieve sustainable development goals by 2030.

Some low-income countries began with weak financial positions, and more than half of low-income countries are affected by vulnerability, conflict, and violence, with many facing geographical disadvantages due to lack of access to the sea, making it difficult to engage in global trade.

Additionally, low-income countries rely heavily on agriculture, making them very vulnerable to extreme weather conditions and unable to integrate into global production chains. While there may seem to be opportunities from commodities, demand is weakening due to the slowdown in major economies, while rising debt burdens pose vulnerabilities, leading to bleak advancement prospects.

For low-income countries to achieve strong growth, policymakers, citizens, and the global community must consider both internal and external factors contributing to growth, including strategies to mitigate risks. Internally, there must be development of a robust financial system and promotion of inclusive access to financial services, along with strengthening governance and the business environment to support the private sector.

Engaging in global trade and promoting foreign direct investment are strategies that must be considered, in addition to domestic growth.

The report also warns that equitable growth is crucial for alleviating poverty and achieving shared prosperity. Emerging and developing economies must strengthen their resilience to sudden economic changes.

Policymakers and stakeholders face several key issues to maintain growth in a fragile environment, including:

1) The rising debt burden makes project selection increasingly important to maximize benefits, along with improved debt management and clarity on debt obligations.

2) Declining investment in emerging and developing economies raises concerns about how these countries will meet expanding investment needs to achieve development goals.

3) The concentration of poverty in low-income countries raises questions about how to overcome barriers to achieve rapid growth.

4) The risk of renewed financial pressures highlights the importance of central bank strength and monetary policy frameworks to mitigate the impacts of currency depreciation on inflation.

Thank you for the information from thaipublica.org