Vietnam's Economy in Q2/2024 Grows Higher Than Expected Due to Public Investment and Domestic Spending, but Faces Multiple Risks

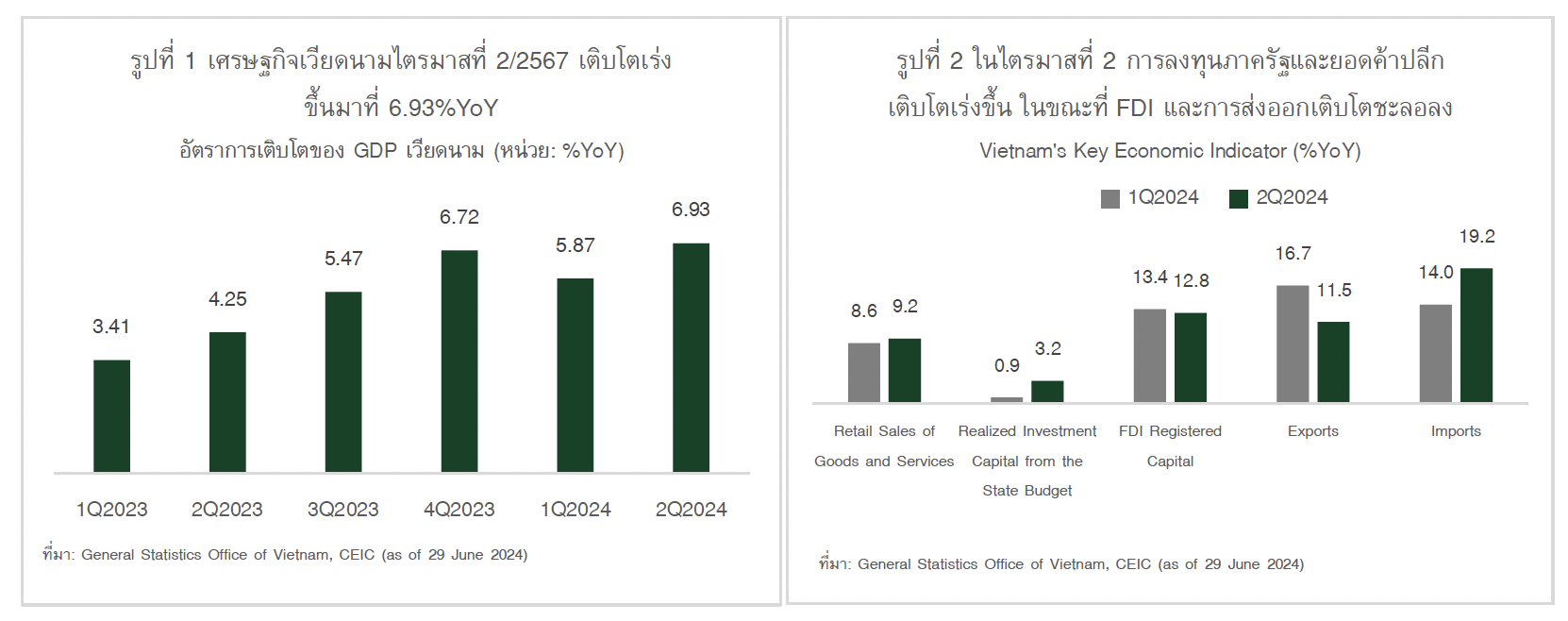

- Vietnam's economy in Q2/2024 grew at a rate of 6.9%YoY, exceeding the consensus of 5.8% and up from 5.9%YoY in Q1/2024. Key points include:

- Supporting factors from household consumption and public investment. Household consumption accelerated, reflected in retail sales of goods and services growing at 9.2%YoY in Q2, up from 8.6%YoY in Q1, particularly with car sales growing for the first time in April-May since the real estate crisis in late 2022. Additionally, public investment expanded at 3.2%YoY in Q2, up from 0.9%YoY in Q1.

- Detracting factors from the slowdown of FDI and exports. FDI in terms of registered capital grew at 12.8%YoY in Q2, slowing from 13.4%YoY in Q1 due to temporary political factors leading to a 9.5%YoY contraction in FDI in April-May, but rebounded to 60%YoY in June after the new president took office. Furthermore, Vietnam's exports slowed across nearly all product categories, including computers and electronics, clothing and footwear, as well as agricultural products, due to uncertainties in the recovery of global demand.

- Vietnam's economic outlook for the second half of 2024 is expected to slow down from the first half, which grew at 6.42%YoY, due to exports likely slowing from last year's high base, compounded by the U.S. countervailing measures and subsidies affecting the export of Vietnamese solar panels, which have been in effect since June this year. Vietnam relies on solar panel exports, accounting for 2.0% of total exports. Household consumption is expected to grow similarly to the first half of the year due to government measures extending the VAT reduction to 8% until the end of this year. For the whole year of 2024, Kasikorn Research Center predicts that Vietnam's economy will grow better than previously forecasted at 6.2% up from 5.8%, based on the significantly better-than-expected economic figures for Q2/2024, along with public investment likely accelerating as political uncertainties begin to ease.

- However, Vietnam's economy still faces several risk factors, including:

- The global economic situation, which is highly uncertain, resulting from the Fed maintaining high interest rates longer than expected, which may lead to a slowdown in the global economy and negatively impact the recovery of global demand, posing a risk to Vietnam's export recovery.

- The unresolved real estate debt problem in Vietnam. The central bank of Vietnam has extended the timeline for assistance measures and debt restructuring until December 31, 2024, reflecting concerns about defaults, while the ratio of NPLs is expected to rise due to bad debts in the real estate sector. This bad debt issue has led banks to become more cautious in lending, resulting in a tightening of credit conditions.

- The depreciation trend of the Vietnamese dong, which is a result of the Fed maintaining high interest rates longer than expected, combined with the still fragile fundamentals of Vietnam's financial sector. In late May, the dong depreciated to a historic low, prompting the central bank to intervene in the foreign exchange market. However, it is expected that currency intervention can only be effective in the short term, considering the need to maintain an appropriate level of foreign reserves.

- Rising inflation, with Vietnam's inflation rate at 4.3%YoY in June, nearing the upper limit of the inflation target of 4.0-4.5%. The central bank of Vietnam is facing the challenging task of balancing the use of policy interest rates to address rising inflation, which may help alleviate the issues of a depreciating dong and the real estate debt problem, as well as tightening credit conditions in the financial sector.

Discussion

Follow breaking news Investment property articles on Facebook, click here.