Monitoring the Real Estate Market Direction: House Prices Surge as the New Year Begins, Contrasting with Slowing Demand for Buying and Renting Amid Economic Conditions

DDproperty, Thailand's leading real estate marketplace website, reveals that the overall real estate market continues to face ongoing challenges due to an economy that is not recovering as expected, high interest rates, and rising living costs. These factors have inevitably impacted household debt and consumer purchasing power, causing consumers to delay their home-buying plans. Consequently, the overall demand for home purchases nationwide decreased by 14% in the latest quarter, affecting all types of housing. This stands in stark contrast to the rising prices of housing across the country, which have increased in line with rising construction costs, creating obstacles for genuine homebuyers seeking affordable housing. Meanwhile, rental indices for both high-rise and low-rise properties have shown interesting growth, despite facing challenges as nationwide rental demand has decreased by as much as 27% in the last quarter, with only single-family homes seeing an increase in rental demand. This reflects the current economic impact on the growth of the real estate market, along with various financial challenges that significantly hinder home ownership at this time.

The latest data from the DDproperty Thailand Property Market Report Q1 2024 analyzes data from property listings on the DDproperty website, revealing that the national housing price index has increased by 1% from the previous quarter (QoQ) and by 2% compared to the same period last year (YoY), indicating a gradual upward trend in housing prices.

This aligns with current construction costs that have risen in accordance with material prices and labor costs, inevitably leading to higher home prices. When considering housing types, only condominiums have seen a price index increase, rising by 2% QoQ (up 4% YoY), while low-rise housing has slightly slowed down, with the single-family home price index decreasing by 1% QoQ (unchanged from last year), and townhouses remaining stable compared to the previous quarter and last year.

Amid challenges from the economic situation, high interest rates, and increasing household debt, concerns remain prevalent, leading most consumers to choose to postpone their home-buying plans. This is evident from the overall national demand for home purchases, which has decreased by 14% QoQ (down 25% YoY) across all housing types. However, compared to the same period before the COVID-19 pandemic (Q4 2019), the long-term demand for home purchases still shows positive growth, with demand for condominiums increasing the most at 12%, followed by low-rise housing such as townhouses and single-family homes (up 10% and 2%, respectively).

Additionally, it was found that housing priced between 1-3 million baht constitutes the largest segment of the market, accounting for 30% of the total housing supply nationwide. This reflects that lower-income consumers still lack sufficient purchasing power to absorb this supply. Corresponding data from credit bureaus indicates that non-performing loans from home loans have increased, as lower-income buyers struggle to keep up with rising living costs. Approximately 60-70% of the impending non-performing loans from housing loans, amounting to about 120 billion baht, stem from individuals with home loans priced below 3 million baht, representing a group of low to middle-income consumers.

Rental Trends Continue to Surge: Demand for Single-Family Homes Dominates the Market

When examining the overall rental market for residential properties nationwide, the rental index shows a promising growth trend, particularly for high-rise housing such as condominiums and apartments, which have seen rental indices increase by 7% QoQ and 18% YoY. Meanwhile, the rental index for low-rise housing, including single-family homes and townhouses, has increased by 2% QoQ and 25% YoY.

Moreover, the long-term rental index continues to grow, with the rental index for low-rise housing increasing by 64% compared to the same period before the pandemic, while the rental index for high-rise housing has risen by 5%.

However, the overall rental demand nationwide has significantly decreased by 27% QoQ and 25% YoY, with only single-family homes experiencing an increase in rental demand, rising by 35% QoQ (up 23% YoY). This is a result of consumers being affected by the prolonged economic situation, leading them to avoid moving or changing residences to reduce the risk of increased expenses that could become burdensome.

In the long term, the overall rental demand for residential properties continues to grow, having increased by 50% compared to the pre-pandemic period, with single-family homes seeing the largest increase at 74%, followed by condominiums at 60%, while only townhouses have decreased by 26%.

The increasing rental demand reflects the growth trend of the rental market, supported by consumers who are not yet ready to own a home or prefer not to have long-term debt, valuing the flexibility of renting over ownership.

Currently, rental properties priced between 10,000-30,000 baht per month dominate the market, accounting for the highest proportion at 44% of the total rental housing supply nationwide, as this price range meets the needs of most consumers and is considered affordable, covering all types of housing except for single-family homes where rental prices exceeding 100,000 baht per month have the largest proportion (52%).

Mr. Witthaya Apirakviriya, General Manager of Think of Living and DDproperty (Developer Side), stated: "Looking at the overall real estate market this year, it may not be very bright due to ongoing challenges from the previous year, including an economy that is still not recovering significantly, high interest rates, rising living costs, and persistent high household debt. These factors are pushing genuine homebuyers to postpone their home purchases.

However, many analysts predict that interest rates are likely to decrease in the near future, which would benefit those planning to buy housing as well as those currently paying off home loans.

Nonetheless, amid these challenges and the unpredictable future, it is essential for middle to lower-income consumers to maintain financial discipline. In addition to having a plan to cope in case interest rates do not decrease, they should also have an emergency plan in case interest rates rise again, to increase their chances of home ownership without losing liquidity, as banks continue to have strict lending measures for this consumer group to prevent potential non-performing loan issues.

Despite these challenges, the real estate market is expected to have positive long-term factors, as the demand for buying and renting remains higher than during the same period before the pandemic, reflecting confidence in the real estate market as an asset that can be held and expected to yield profits in the long run.

Additionally, forecasts from the World Bank indicate that private consumption and tourism will be key factors driving Thailand's economic growth in 2024, which means that rental rates and property prices in the capital and key regions attracting tourism will see interesting growth,” Mr. Witthaya added.

“Another important factor, as significant as the current economic stimulus measures, is the stimulus measures for the real estate sector, which will be the light at the end of the tunnel that both consumers and all operators are waiting for, as the government has yet to introduce new measures or clear policies to stimulate the real estate market. It is expected that if the government introduces other sufficiently attractive measures, it will be a factor that helps revitalize the real estate market and lead to growth in related businesses as well,” Mr. Witthaya concluded.

Summary of the Capital Real Estate Market: Prices Begin to Recover, Contrasting with Short-Term Demand for Buying and Renting Shrinking

The DDproperty Thailand Property Market Report Q1 2024 provides in-depth information on the real estate market in Bangkok in the latest quarter, summarizing the overall price index, rental index, and demand for buying and renting residential properties, along with updates on potential locations where price and rental indices are expected to grow interestingly.

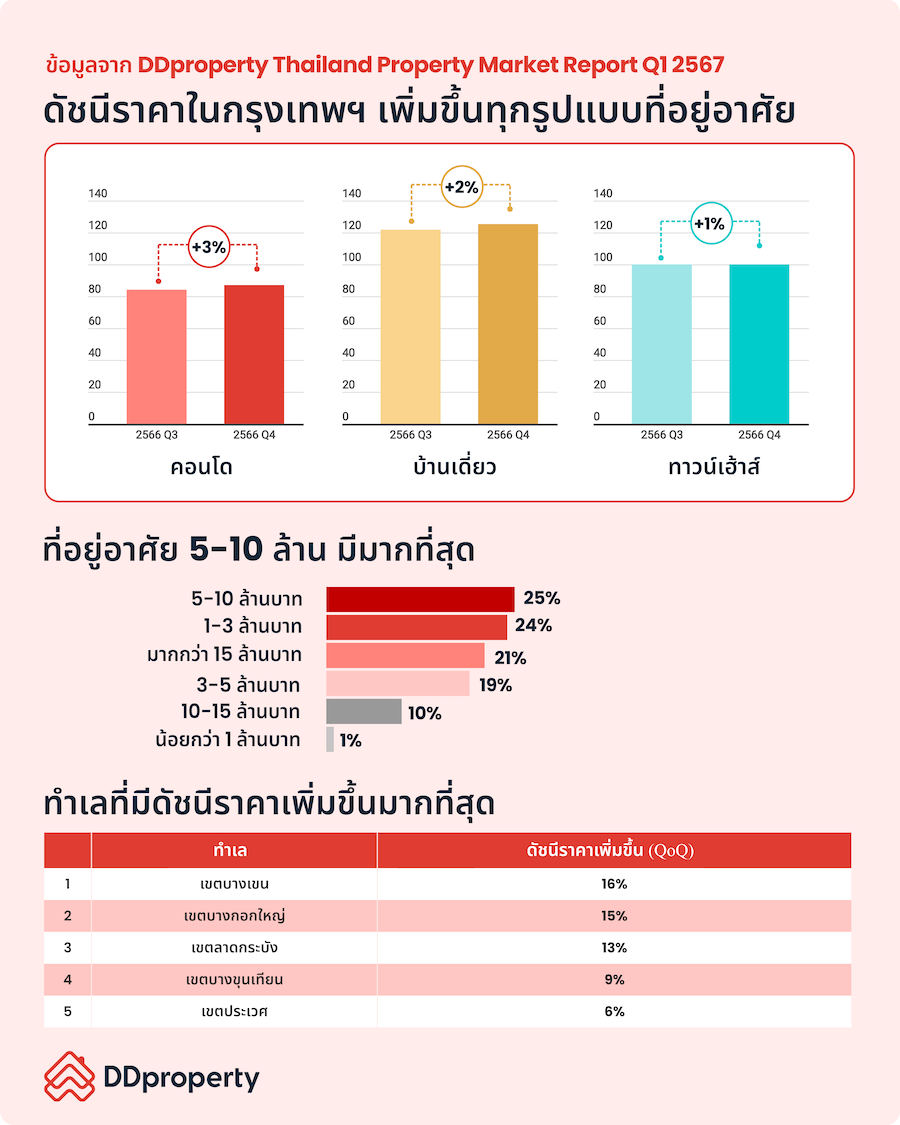

- House prices are rising, reducing buyer demand by 15%. The overall housing prices in Bangkok are trending upwards, similar to the national trend, with the housing price index in Bangkok increasing by 2% QoQ and 4% YoY, reflecting the rising construction costs that pressure operators to adjust prices in line with both costs and consumer purchasing power.

The rising house prices in an era of high interest rates have become a challenge impacting consumer purchasing power, leading to a significant decrease in demand for purchases in Bangkok. Overall demand for purchases has decreased by 15% QoQ and 27% YoY. Notably, single-family homes have seen the largest drop in demand, decreasing by 21% QoQ (down 34% YoY), followed by townhouses down 17% QoQ (down 28% YoY), and condominiums down 12% QoQ (down 23% YoY).

However, looking at the long term compared to the pre-pandemic period, the overall demand for purchases in Bangkok remains positive, with demand increasing by 8%, particularly for single-family homes, which increased the most at 10%, contrasting with short-term demand, followed by condominiums up 8% and townhouses up 5%.

The most common housing price range is between 5-10 million baht, accounting for 25%, followed by 1-3 million baht and over 15 million baht (accounting for 24% and 21%, respectively). When categorized by housing type, condominiums and townhouses priced between 1-3 million baht are the most abundant (25% and 38%, respectively), while single-family homes priced over 15 million baht have the largest proportion (45%), reflecting the trend of developers increasingly targeting middle and upper-income consumers to avoid loan rejection issues from banks for lower-income buyers.

For locations with the highest price index increase in Bangkok in the latest quarter, most are located outside the central business district and in the outskirts of Bangkok. The top area is Bang Khen, which increased by 16% QoQ (up 10% YoY), benefiting from proximity to two electric train lines: the Green Line extension from Mo Chit to Saphan Mai-Khukhot and the Pink Line from Khae Rai to Min Buri, as well as being close to Don Mueang Airport, facilitating convenient transportation. Following this are Bangkok Yai, up 15% QoQ (up 24% YoY), Lat Krabang, up 13% QoQ (down 5% YoY), Bang Khun Thian, up 9% QoQ (up 1% YoY), and Prawet, up 6% QoQ (up 10% YoY).

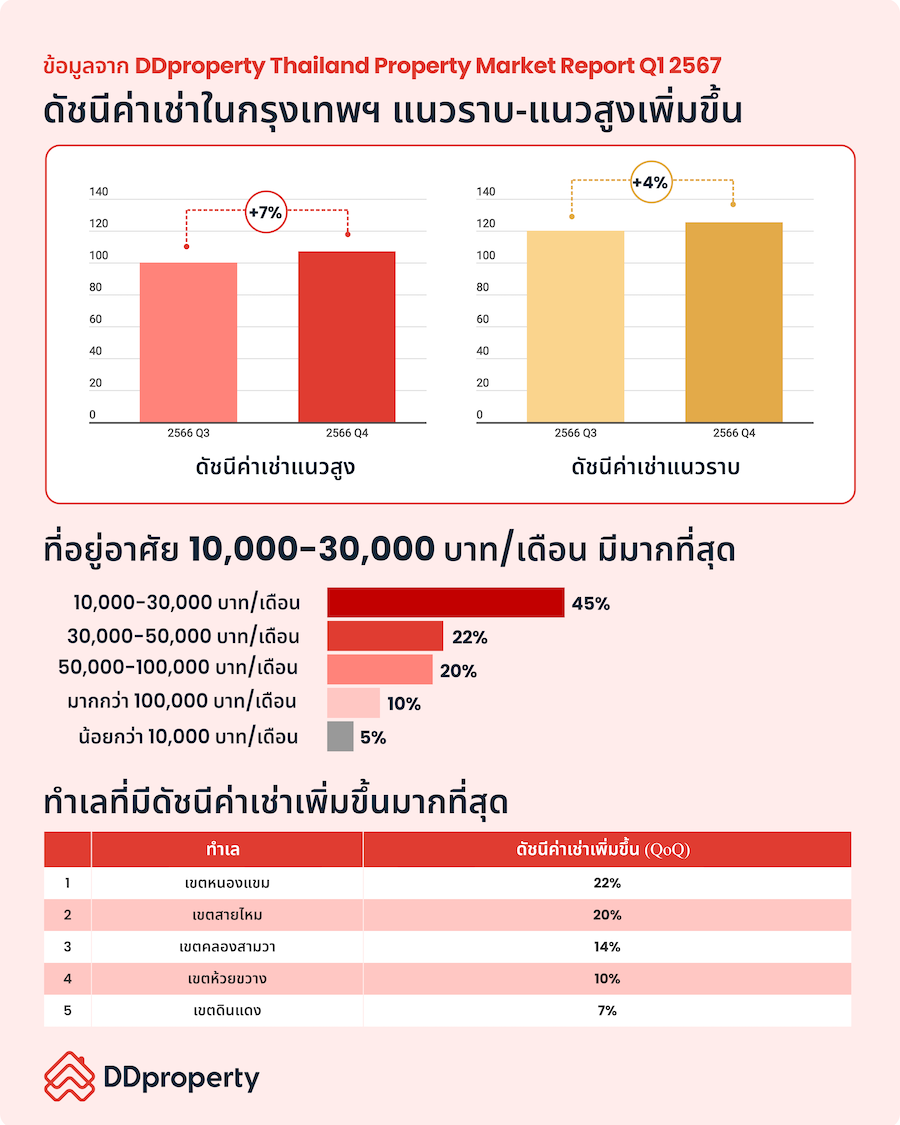

- The rental market remains strong, with demand for single-family homes surging by 51%. The rental market in Bangkok continues to grow interestingly, particularly with continuously rising rents, as evidenced by the rental index for high-rise housing such as condominiums and apartments increasing by 7% QoQ (up 16% YoY), while low-rise housing such as single-family homes and townhouses increased by 4% QoQ (up 15% YoY). Notably, compared to the same period before the pandemic, the rental index for low-rise housing has shown significant growth, increasing by 19%, while the rental index for high-rise housing has risen by 3%.

However, when considering rental demand in Bangkok, it has significantly decreased, with overall rental demand dropping by 33% QoQ (down 22% YoY). When categorized by housing type, the demand for condominiums has decreased the most by 40% QoQ (down 30% YoY), followed by townhouses down 22% QoQ (down 19% YoY), with only single-family homes experiencing an increase in rental demand of 51% QoQ (up 73% YoY), consistent with the national trend.

In the long term, the rental market still shows good growth signals, with overall rental demand in Bangkok increasing by 73% compared to the pre-pandemic period, with single-family homes remaining popular with a rental demand increase of 155%, followed by condominiums up 75%, while only townhouses have decreased by 6%.

When considering the number of rental properties available, the most abundant rental price range is between 10,000-30,000 baht per month, accounting for 45% of the total rental housing supply in Bangkok. When categorized by housing type, condominiums and townhouses in the rental price range of 10,000-30,000 baht per month are the most numerous (accounting for 47% and 33%, respectively), while single-family homes with the highest number will be in the rental price range exceeding 100,000 baht per month, accounting for 52%.

The locations with the highest rental index increase in Bangkok in the latest quarter are primarily in employment areas and near electric train lines, which cater to commuting needs in the capital. The top area is Nong Kham, which increased by 22% QoQ (up 10% YoY), being a suburban area not far from the electric train and large shopping centers, with continuous growth expected along the Blue Line electric train from Hua Lamphong to Lak Si, including the future extension of the Blue Line from Bang Khae to Phutthamonthon Sai 4. Following this are Sai Mai, up 20% QoQ (down 10% YoY), Khlong Sam Wa, up 14% QoQ (up 11% YoY), Huai Khwang, up 10% QoQ (up 18% YoY), and Din Daeng, up 7% QoQ (up 17% YoY).

Note: The DDproperty Thailand Property Market Report is a quarterly report on housing market trends compiled every three months, using data from property listings on the DDproperty website to calculate through statistical methods, analyze, and create indices reflecting price movements, the number of housing units available in the market, and the demand for housing during that time. This report includes the Price Index and Demand Index from both the buying-selling and rental markets, showing the trends of the housing market in Thailand, especially in the Bangkok area and its vicinity over the quarter. Since Q1 2022, the price and demand indices in this report have used data from Q1 2018 as the base year.

Read and study the latest real estate market trend report at DDproperty Thailand Property Market Report Q1 2024.