Reviving Relations with Saudi Arabia: Advancing FTA to Gain Competitive Edge

- The revival of relations between Thailand and Saudi Arabia marks a positive start, helping to boost Thai exports by an additional 1 billion baht over the next three years. However, this year, Saudi Arabia's economic recovery driven by oil prices and purchasing power will significantly support Thai exports to Saudi Arabia, which are expected to rebound to pre-COVID-19 levels, reaching nearly $1.9 billion, a 15% increase. Key driving products include passenger cars, pickup trucks, automotive parts, halal food (processed seafood, rice, processed food), processed wood, rubber products, rubber hoses, and electrical appliances (televisions, refrigerators, air conditioners).

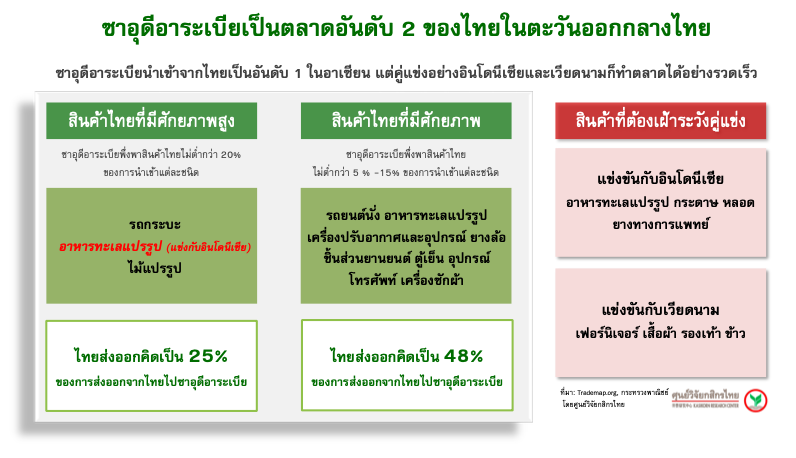

- Currently, Saudi Arabia imports the most Thai goods in ASEAN, with Thai products meeting diverse needs, although the volume is still relatively low. Thailand will face competition from rivals in the Saudi market, similar to other export markets, with Indonesia being a significant competitor, overlapping in products such as passenger cars, wood panels, processed seafood, and refrigerators, while also needing to watch out for rice and washing machine products from Vietnam.

The revival of relations between Thailand and Saudi Arabia for the first time in 30 years is expected to enhance economic connectivity in various sectors. In 2021, Thailand's trade value with Saudi Arabia was only $7.3 billion, heavily reliant on oil and chemical imports amounting to $5.66 billion, while exports generated only $1.64 billion, accounting for just 0.6% of Thailand's total exports. Kasikorn Research Center believes that this strengthened relationship creates new opportunities for Thai products and businesses moving forward, while also highlighting competitive challenges from Vietnam and Indonesia in the Saudi market.

- Thai products stand out in meeting Saudi Arabia's needs more than any other ASEAN country. Saudi Arabia is primarily an oil producer and exporter. Despite its wealth, it has production limitations and relies heavily on imports, totaling $130 billion annually, with China being the main source at 20% of Saudi imports, followed by the U.S. (10%) and the UAE (7%). Thailand ranks as the 12th largest source of imports for Saudi Arabia, accounting for 1.7% of total imports, and is the most prominent in ASEAN, followed by Indonesia, Singapore, and Vietnam.

- Among the top 30 essential products that Saudi Arabia needs to import, which account for 44% of total imports, Thai products can meet a wide range of demands compared to competitors, including passenger cars, smartphone parts, medical supplies, HDDs, rice, televisions, tires, medical equipment, automotive parts, pickup trucks, and processed food. Thai products in these categories have a strong market presence, except for smartphones, vehicles, and tires, where competition is increasing from Indonesian and Vietnamese rivals.

- Excluding industrial products, food items are significant for Thailand. Rice is the most sought-after food item by Saudi Arabia, with 78% of imports being Indian basmati rice, leaving Thai rice with a minimal share (1.7%), while Vietnam also struggles to compete (1.5%). Canned seafood, canned fruits, and dried fruits are areas where Thailand has high market potential, holding 54%, 36%, and 25% of the market, respectively, indicating opportunities for future market expansion. Other products that Saudi Arabia seeks to consume and present future opportunities for Thailand include rice, meat, poultry, milk, processed food, cheese, bread, corn, barley, sugar, fruits, and coffee.

Recently, several Indonesian products have begun to compete with Thailand, such as passenger cars and rubber products (Saudi Arabia imports 4.8% and 3.8% from Indonesia, respectively). Notably, processed seafood imports from Indonesia account for 30%, along with other food products. Indonesia, being a Muslim country, has credibility in producing food products that adhere to halal principles, posing a challenge to Thailand's food market in Saudi Arabia. Currently, Vietnam's products differ from Thailand's, mainly focusing on smartphones, clothing, and footwear, but rice products may increasingly compete with Thai rice.

Currently, competition between Thailand and its rivals is relatively equal, with an average import tax of 5.6% (MFN rate). Countries with preferential trade rights with Saudi Arabia are quite limited, as Saudi Arabia, despite trading globally, remains relatively closed off. It has established FTA agreements primarily within the Middle East and North Africa, such as with the Gulf Cooperation Council (GCC) and the Pan-Arab Free Trade Area (PAFTA). Currently, only Singapore has a prior agreement with the GCC, while several other countries, including South Korea, China, the UK, Australia, and New Zealand, are in negotiations.

Saudi Arabia is Thailand's second-largest market in the Middle East, following the UAE. In terms of market potential, it holds significant growth opportunities due to its wealth, with a per capita income of around $20,000 per year, half that of the UAE, but with a population of 30 million, more than three times that of the UAE. Nevertheless, Kasikorn Research Center anticipates that in 2022, the global economic recovery and rising energy prices will boost income and domestic purchasing power, leading Thai exports to Saudi Arabia to return to near-normal levels before COVID-19, with a potential growth of 15%, reaching an export value of around $1.9 billion. Furthermore, positive signals from the revival of relations with Thailand are likely to stimulate investment, business, and tourism between the two countries, enhancing the recognition and marketability of Thai products. There is a possibility that Thai exports to Saudi Arabia could accelerate by another $1 billion over three years, reaching a value of $2.6 billion, positioning it as a trading partner comparable to the UK market, driven mainly by halal food (processed seafood, rice, seasonings), automotive products and components, rubber products, and electrical appliances.

However, to fully realize the potential for Thai export growth, government support will be essential. Currently, the Middle East region is relatively closed off, and there are not many FTA agreements with foreign countries. If the Thai and Saudi governments can seize the opportunity to strengthen their relationship and initiate FTA negotiations ahead of other ASEAN countries, potentially following Singapore's model through the GCC agreement, it would create a competitive advantage for Thai products to access the market more effectively.