November Exports Continue to Grow Strongly, Accelerating from the Previous Month Supported by Consumption Recovery

November exports continue to grow strongly, accelerating from the previous month, supported by the recovery of consumption, global production, the depreciation of the Thai baht, and the rising prices of commodities.

Key Summary

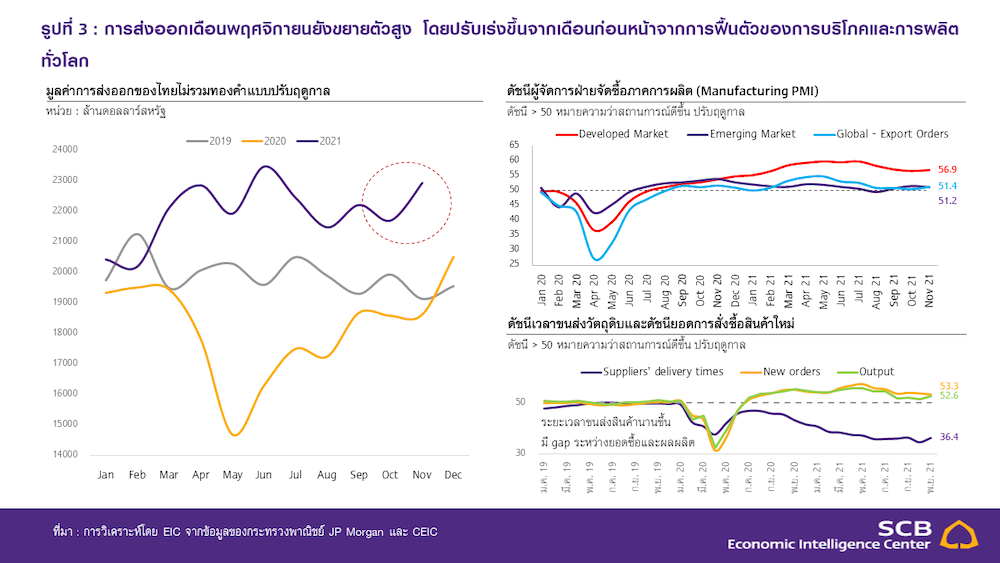

• November exports maintained a high growth rate of 24.7% YOY, expanding across all major product categories except rubber products, and in all major markets except Japan, which remained stable. Compared to the previous month, exports adjusted for seasonality and excluding gold grew by 5.7% MOM SA, reflecting the recovery of consumption and global production, as indicated by the global Manufacturing Purchasing Managers' Index (PMI) remaining above 50.

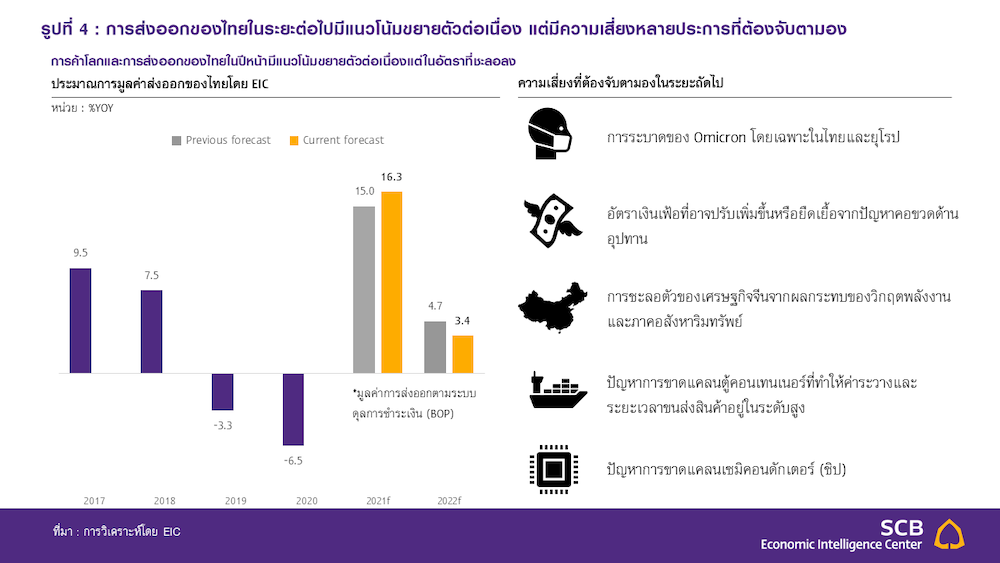

• EIC forecasts a 16.3% YOY growth in exports for 2021. Although exports are recovering in line with the expansion of the global economy and trade as the COVID-19 situation eases, new pressures have emerged towards the end of the year due to a resurgence of outbreaks in Europe and the emergence of the Omicron variant, along with global supply chain bottlenecks leading to rising inflation in many countries, affecting consumer purchasing power. This may result in a short-term slowdown in the global economy and trade.

• Thai exports in 2022 are expected to continue growing in line with the global economic and trade recovery, but at a slower rate. EIC estimates a 3.4% YOY growth in exports for 2022, but several risk factors need to be monitored, particularly concerns regarding the COVID-19 Omicron variant outbreak, as well as inflation that may increase or persist due to supply chain bottlenecks, the slowdown of the Chinese economy due to the energy crisis and real estate sector issues, and the semiconductor shortage that will pressure exporters next year.

Key Points

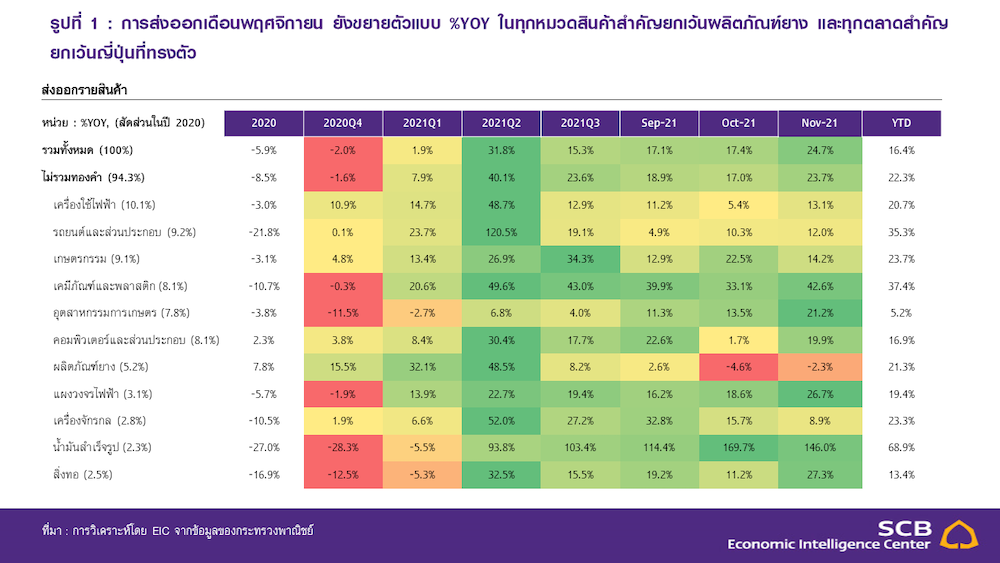

November 2021 export value grew by 24.7% YOY, accelerating from the previous month's 17.4%. Excluding gold, exports would grow by 23.7%, resulting in a 16.4% growth in export value over the first 11 months of 2021.

In terms of exports by product, exports continued to grow YOY in almost all major products except rubber products, which contracted.

• Refined oil grew by 146% YOY, continuing to expand for 9 months due to high energy demand and oil prices, with growth in all major markets such as Malaysia (545.1% YOY), Singapore (205.4% YOY), and the Philippines (1,749% YOY).

• Chemicals grew by 63.4% YOY, continuing to expand for the 12th month, with growth in all major markets such as China (31% YOY), Japan (67.6% YOY), and India (145.5% YOY).

• Plastic pellets grew by 41.9% YOY, continuing to expand for the 12th month, with growth in all major markets such as China (26.5% YOY), India (60.5% YOY), and Indonesia (38.9% YOY).

• Cars and components grew by 12% YOY, continuing to expand for 13 months, with significant support from markets like the Philippines (26.7% YOY) and Indonesia (65.1% YOY), while Australia (22.4% YOY) was a significant drag in the previous month, and Japan (-38% YOY) and Vietnam (-10.1% YOY) were significant drags this month.

• Steel, iron, and products grew by 51.9% YOY, continuing to expand for the 12th month, with growth in almost all major markets such as Japan (35.5% YOY), the USA (90.2% YOY), and Taiwan (265.5% YOY), while China (-1.5% YOY) and Cambodia (-0.3% YOY) contracted slightly.

• Computers and equipment returned to high growth at 19.9% YOY after only growing 1.7% YOY in the previous month, with significant support from markets like the USA (18.9% YOY), China (64.8% YOY), and the Netherlands (37.8% YOY), while Hong Kong (-8.4% YOY) and Germany (-12.8% YOY) were significant drags.

• Electrical circuit boards grew by 26.7%, continuing to expand for the 12th month in line with global electronic goods demand, with growth in all major export markets such as Hong Kong (28.2% YOY), Singapore (12.1% YOY), and Japan (38.9% YOY).

In terms of exports by market, Japan and Hong Kong reversed to contraction, while Australia continued to contract, while other markets continued to expand.

• Exports to India continued to grow at a high rate of 61.1% YOY, marking 10 consecutive months of growth across almost all major products such as plastic pellets (60.5% YOY), air conditioners and components (37.4% YOY), and chemicals (145.5% YOY), except for machinery and components (-3.5% YOY), which contracted slightly.

• Exports to ASEAN-5 grew by 55.1%, marking 7 consecutive months of growth, driven by almost all countries in the group, including Malaysia (42.6% YOY), Indonesia (56.5% YOY), Singapore (91.4% YOY), and the Philippines (37.4% YOY), except for Brunei (-4.7% YOY).

• Exports to Australia reversed to growth at 9.6% YOY after contracting for 4 consecutive months, with major export products that grew including cars and components (22.4% YOY), steel, iron, and products (83.1% YOY), and plastic pellets (39.1% YOY). However, several products faced downward pressure, such as gems and jewelry (-56.7% YOY) and rubber products (-13% YOY).

• Exports to Hong Kong reversed to growth again at 4.7% YOY after contracting -2.5% YOY in the previous month, with several important products showing growth, such as electrical circuit boards (28.2% YOY) and electrical appliances and components (56.8% YOY). However, several important products continued to contract, such as computers and components (-8.4% YOY) and gems and jewelry (-7.4% YOY).

• Exports to Japan remained stable at -0.1% YOY after contracting -2% YOY in the previous month, marking the only contraction in 12 months, with significant drags from cars and components (-38% YOY), processed chicken (-5.8% YOY), telephones (-26.3% YOY), and electrical appliances (-7.1% YOY), while chemicals (67.6% YOY), electrical circuit boards (38.9% YOY), steel, iron, and products (35.5% YOY), and plastic pellets (49% YOY) were significant supports.

Figure 1: November exports continued to grow YOY across all major product categories except rubber products, and in all major markets except Japan, which remained stable.

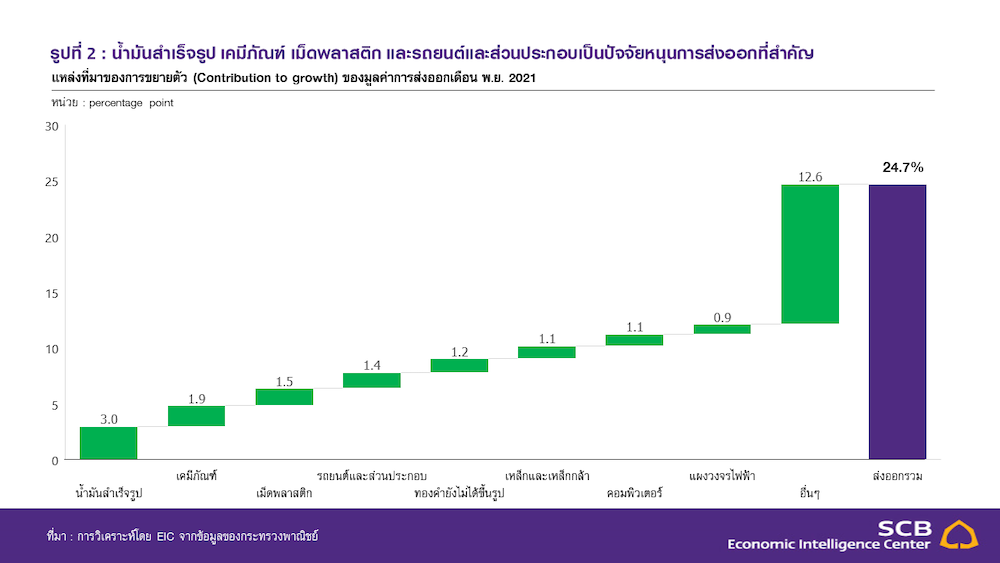

Figure 2: Refined oil, chemicals, plastic pellets, and cars and components are significant factors supporting exports.

Source: Analysis by EIC from the Ministry of Commerce data.

In November 2021, the value of imports grew by 20.5% YOY, slowing from the previous month's 34.6% YOY.

This growth occurred across all major import categories, including fuel products (71.7% YOY), which grew significantly due to high price increases compared to the previous year, capital goods (11% YOY), consumer goods (17.9% YOY), and vehicles and transportation equipment (3.7% YOY). Meanwhile, imports of raw materials and semi-finished products also grew by 18.6% YOY, and excluding gold, would grow by 39.3% YOY. Over the first 11 months of 2021, imports grew by 29.4% YOY. The trade balance in November showed a surplus of $1,018.7 million, and for the first 11 months of 2021, there was a surplus of $3,927.3 million.

Implication

November exports continued to grow strongly at 24.7% YOY and accelerated from the previous month by 5.7% MOM SA (excluding gold exports and seasonally adjusted) due to the recovery of consumption and global production, as reflected by the Manufacturing PMI remaining above 50.

There is also support from the trend of the Thai baht's depreciation, which has allowed Thai products to compete on price in the global market. The depreciation of the baht will positively impact the income and profits of exporters, especially those with a high local content, such as agricultural exporters. Meanwhile, the rising prices of certain commodities, such as agricultural products and crude oil, positively affect the export value of oil-related products such as refined oil, chemicals, and plastic pellets. However, high oil prices will increase pressure on Thailand's current account deficit in the future, as Thailand is a net importer of oil and oil products.

Figure 3: November exports continued to grow strongly, accelerating from the previous month due to the recovery of consumption and global production.

Source: Analysis by EIC from the Ministry of Commerce, JP Morgan, and CEIC.

Although exports are recovering from the expansion of the global economy and trade as the COVID-19 situation eases, new pressures have emerged towards the end of the year due to a resurgence of outbreaks in Europe and the emergence of the Omicron variant, along with global supply chain bottlenecks leading to rising inflation in many countries, affecting consumer purchasing power, and potentially resulting in a short-term slowdown in the global economy and trade. EIC forecasts a 16.3% YOY growth in exports for 2021 (based on balance of payments data). For 2022, exports are expected to continue growing in line with the global economic and trade recovery, with exports to developing countries showing improved growth due to the acceleration of the economy benefiting from increased vaccination progress. Meanwhile, exports to developed economies are expected to continue growing next year but at a slower rate after previous economic recovery.

However, Thai exports in 2022 will still face various risk factors, particularly the spread of the Omicron variant. EIC estimates a continued growth of 3.4% YOY in exports for 2022, but exporters will face several risk factors that need to be monitored, especially concerns regarding the COVID-19 Omicron variant outbreak, as well as inflation that may increase or persist due to supply chain bottlenecks.

The slowdown of the Chinese economy due to the energy crisis and real estate sector issues, the semiconductor shortage, and the anticipated slowdown in imports from the US due to smaller economic stimulus measures, along with consumers shifting to more spending in services, and the container shortage causing shipping costs and delivery times to remain higher than pre-crisis levels, are expected to continue to be ongoing issues into next year. The situation is anticipated to begin to improve in the second half of 2022 onwards, driven by investments to expand production capacity. The estimated 3.4% growth in exports for 2022 is based on the assumption that the Omicron outbreak will be present globally, including in Thailand, in the first quarter of 2021, but will not be severe enough for the government to impose strict lockdown measures, while vaccine development can be delivered starting from the second quarter onwards.

Figure 4: Thai exports are expected to continue to grow, but there are several risks that need to be monitored.

Source: Analysis by EIC.

Analysis by.. https://www.scbeic.com/th/detail/product/8001

Authors of the analysis

Senior Economist: Dr. Poonyawat Sreesing ([email protected])

Analyst: Vishal Gulati ([email protected])

Economic Intelligence Center (EIC)

Siam Commercial Bank Public Company Limited

EIC Online: www.scbeic.com