Relaxation of LTV Ceiling Measures Until the End of 2022 Opens Growth Opportunities for Real Estate and Loan Businesses If COVID-19 Eases (Kasikorn Research Center)

The Kasikorn Research Center believes that relaxing the regulations on housing loans and related loans (LTV measures) by temporarily adjusting the LTV ceiling to 100% until the end of 2022 will enhance the potential for home purchases amidst the challenging environment of the housing market and home loan disbursement by financial institutions for the remainder of this year and in 2022.

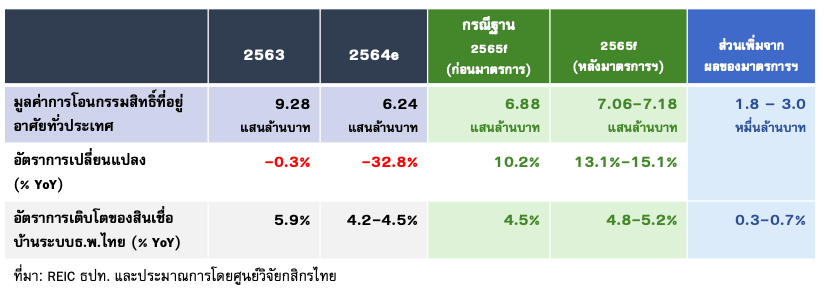

If the Thai economy shows signs of recovery, the COVID-19 situation improves, and domestic inflation remains manageable, the relaxation of the LTV measures this time will support the gradual improvement of the housing market throughout 2022. The Kasikorn Research Center estimates that the value of property transfers nationwide during the period of these measures will increase from previous expectations, amounting to approximately 18,000 to 30,000 million baht compared to a scenario without these measures.

At the same time, the effects of relaxing the LTV measures are expected to allow home loans to grow within a higher range in 2022, with the Kasikorn Research Center initially estimating that the relaxation of the LTV measures will enable home loans in 2022 to grow by an additional 0.3-0.7%, reaching a range of 4.8-5.2%, higher than the forecast range for 2021 of 4.2-4.5%.

• Key issues to monitor will include assessing the readiness for new debt or refinancing existing debt, which encompasses credit risk and the ability of borrowers to repay debts that may face increased liabilities post-COVID, as well as income and employment situations that may not yet fully return to normal, ultimately affecting the loan approval conditions for each borrower.

• The temporary relaxation of the LTV ceiling to 100% until the end of 2022... benefits the housing market by increasing the ability to own homes, but purchasing a home still depends on crucial factors such as confidence in the economic recovery and the readiness of buyers.

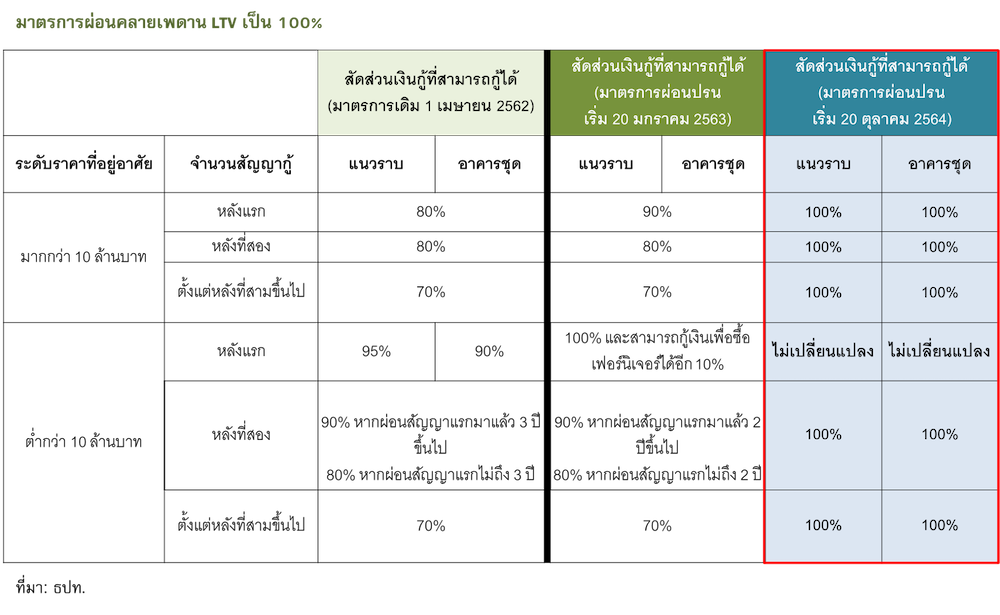

On October 21, 2021, the Bank of Thailand announced the relaxation of regulations on housing loans and related loans (LTV measures) again, after previously easing some criteria. The details of this relaxation include: 1. Adjusting the loan-to-value (LTV) ratio for the purchase of homes priced below 10 million baht for the second contract onwards from 70%-90% to 100%, while the first contract remains at 100%, with an additional 10% loan for purchasing furniture (totaling 110% of the collateral value); and 2. Adjusting the loan ceiling ratio for home purchases priced above 10 million baht from 70%-90% to 100% starting from the first contract onwards, effective for loan agreements from October 20, 2021, to December 31, 2022.

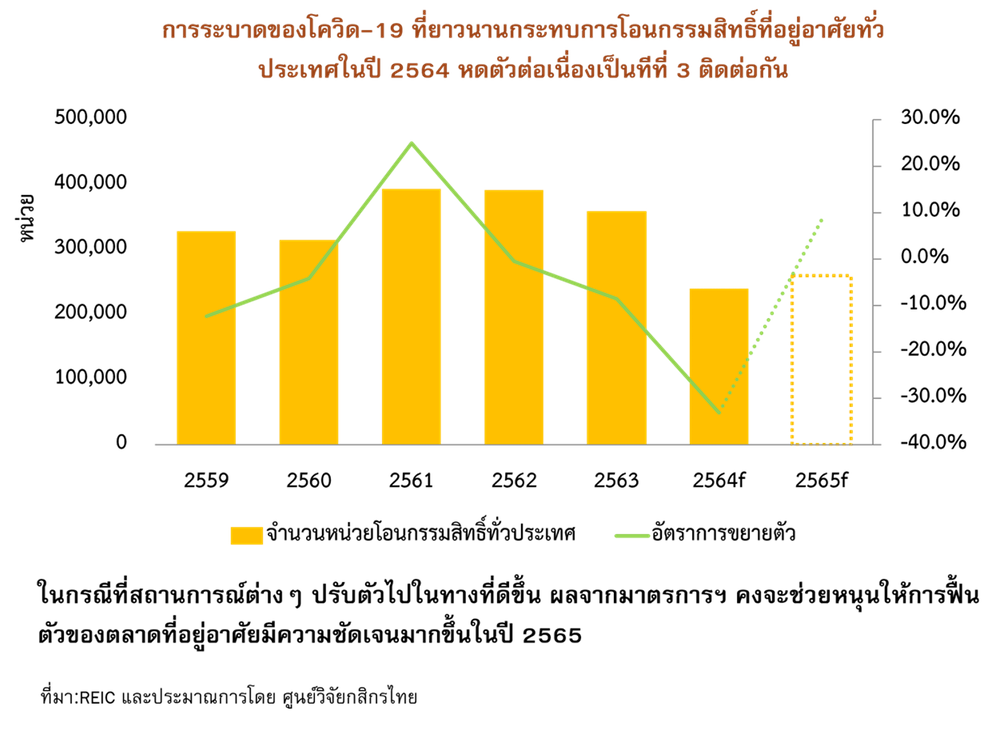

• Looking back since the onset of the COVID-19 pandemic, the housing market has been significantly affected, as evidenced by a sharp slowdown in housing transactions, particularly in provincial areas. In the first eight months of 2021, property transfers nationwide totaled 154,000 units, contracting by 33.2% YoY, with the Bangkok and surrounding areas contracting by 16.8% YoY, while other provinces saw a contraction of 51.4% YoY, with over 39 provinces experiencing property transfers dropping by more than 90%, and about 6 provinces having fewer than 10 property transfers. Additionally, the number of unsold properties remains high, leading to a slowdown in new housing project investments to the lowest level in over 18 years.

Meanwhile, housing loans from the Thai commercial banking system remain the main retail loan product that can sustain growth. As of the end of August 2021, the outstanding housing loan balance of the Thai banking system grew by 6.1% YoY compared to the same period last year and 3.4% YTD compared to the end of 2020 (2020 grew by 5.9% YoY), higher than the overall retail loan growth of only 4.6% YoY and 1.7% YTD. The continuous growth in housing loans this year is primarily for homes priced at 3 million baht and above, which cater to borrowers or households with moderate to high purchasing power and are less affected by the COVID-19 situation, leading financial institutions to assess that they still have the ability to repay debts.

• For the remainder of this year and in 2022, the housing market environment and the direction of home loan disbursement by financial institutions will still face many challenges, including the uncertain COVID-19 situation that will affect the timing of economic recovery and may impact purchasing power confidence and job security. Additionally, purchasing a home still depends on the readiness of buyers and the ability of loan applicants to repay debts. However, the Kasikorn Research Center believes that if the Thai economy shows a gradual recovery, the COVID-19 situation eases, and domestic inflation remains manageable, the relaxation of the LTV measures this time will support the gradual improvement of the housing market. It is expected that the value of property transfers nationwide during the period of these measures will increase from previous estimates, amounting to approximately 18,000 to 30,000 million baht compared to a scenario without these measures, while the total property transfers nationwide for the entire year of 2021 are expected to be around 240,000 units, contracting by 33.1% from 2020, with property transfers in provincial areas (70 provinces) potentially decreasing by more than half from 2020.

• Similarly, the effects of relaxing the LTV measures are expected to allow home loans to grow within a higher range in 2022, assuming that the Thai economy can gradually recover and does not face a new wave of COVID-19. The Kasikorn Research Center initially estimates that the relaxation of the LTV measures, which will extend into 2022, will enable home loans in 2022 to grow by an additional 0.3-0.7%, reaching a range of 4.8-5.2%, higher than the forecast range for 2021 of 4.2-4.5%.

Meanwhile, key issues to monitor will include assessing the readiness for new debt or refinancing existing debt, which will encompass credit risk and the ability of borrowers to repay debts that may face increased liabilities post-COVID, particularly from other consumer debts such as credit cards or personal loans, as well as income and employment situations that may not yet fully return to normal, which may ultimately affect the loan approval conditions for each borrower based on these various conditions.