Household Debt Continues to Grow in 2Q/2021, Increasing Borrowers Under Relief Measures Highlights the Urgent Need for Debt Restructuring

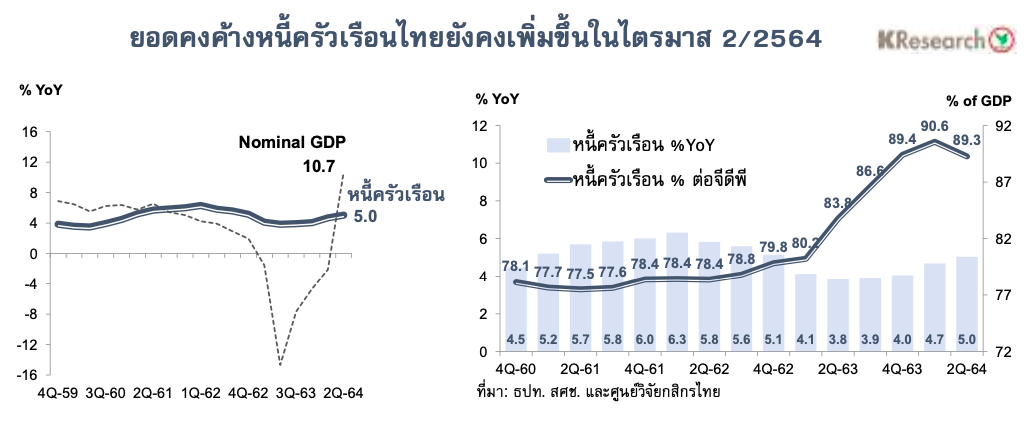

• The latest data on household lending in the second quarter of 2021 shows continued growth. The outstanding household debt in Thailand reached 14.27 trillion baht, accounting for 89.3% of GDP, down from 90.6% of GDP, which was the highest level in 18 years recorded in the first quarter of 2021. This decline is attributed to the Thai economy growing at a rate higher than household debt during the second quarter of 2021, with nominal GDP increasing by 10.7% YoY compared to household debt growth of 5.0% YoY year-on-year.

• However, the Kasikorn Research Center estimates that the decline in the household debt-to-GDP ratio in the second quarter of 2021 is likely a temporary situation and does not indicate a reduced concern regarding household liabilities. On the contrary, the continued increase in outstanding household debt during the quarter reflects that the debt burden remains high and is not significantly different from previous quarters.

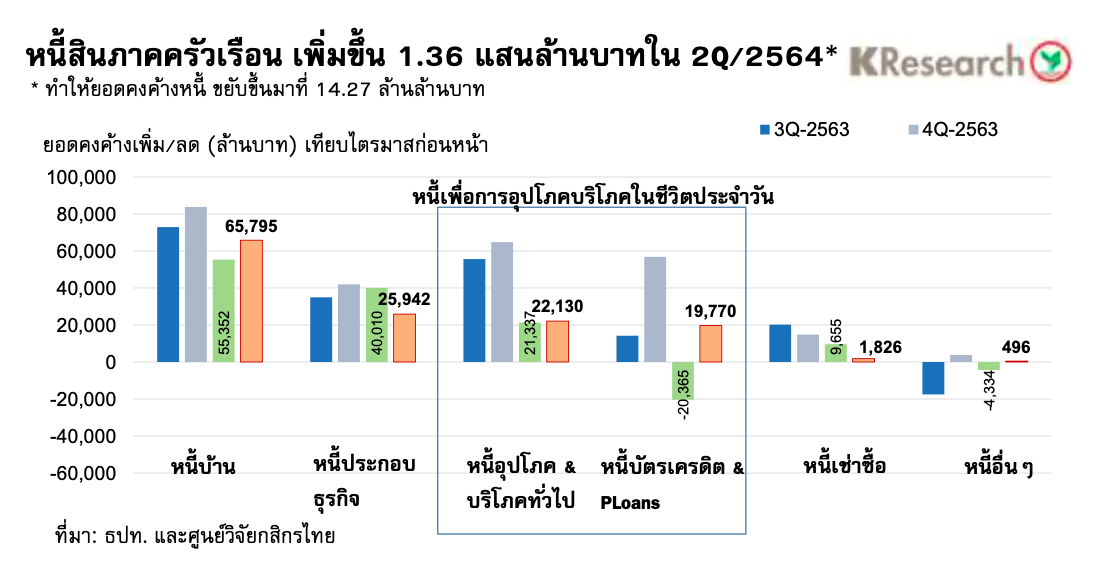

Specifically, household debt increased by approximately 136 billion baht in the second quarter of 2021 (from 14.14 trillion baht to 14.27 trillion baht), primarily due to a surge in two types of retail debt: 1) Housing loans, which continue to rise, both from commercial banks and specialized financial institutions, with new loans for homebuyers totaling approximately 156 billion baht in the second quarter of 2021, particularly for single-family homes and condominiums; 2) Consumer debt for daily living, especially credit card debt and personal loans, which households likely use as a short-term liquidity source to alleviate income and expense imbalances.

• The COVID-19 crisis has exacerbated the financial vulnerability of many households, and borrowers from financial institutions (including commercial banks, non-banks, and specialized financial institutions) have increasingly sought relief measures since April 2021.

According to the latest data from the Bank of Thailand as of July 2021, there were 5.12 million retail loan accounts receiving financial assistance from financial institutions, representing a debt burden of 3.35 trillion baht (up from the low point of 4.77 million accounts and 3.18 trillion baht in April this year). The retail debt under these relief measures accounts for approximately 23.5% of Thailand's outstanding household debt, and the Kasikorn Research Center estimates that this proportion will continue to rise throughout the third quarter of 2021.

• For the remainder of 2021, the Kasikorn Research Center predicts that the household debt-to-GDP ratio in Thailand will rise again as it is expected to approach the upper range of the estimated household debt figures, which the center forecasts to be between 90-92% of GDP. This is due to the high level of household debt and the possibility that some households may incur additional debt in early Q3 2021 (during a period of severe COVID-19 outbreaks in the country), as reflected in the acceleration of both secured and unsecured personal loans.

As lockdown measures to curb the COVID-19 outbreak are gradually eased (starting in September 2021), advancements in vaccination and increased plans for reopening the country are expected to positively impact the economic outlook and household income situations in the near future. However, it must be acknowledged that the ability of many retail borrowers to repay their debts may not return to normal immediately this year, while the number of retail borrowers seeking assistance from financial institutions continues to rise, both in terms of account numbers and debt burdens, highlighting the importance of accelerating debt restructuring to align debt burdens with borrowers' financial situations.

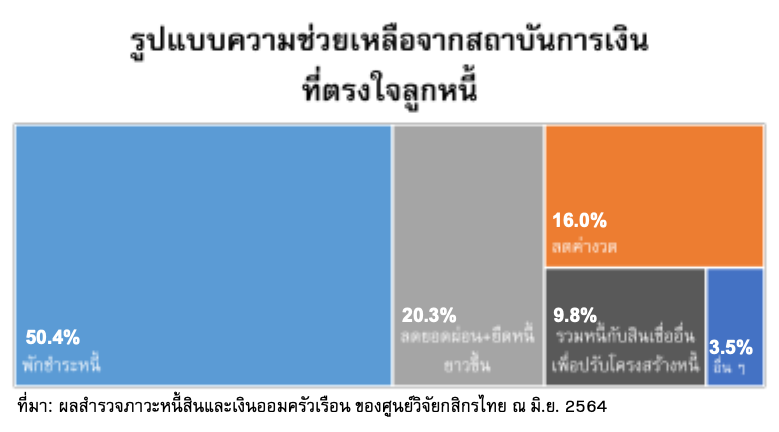

According to a survey on debt and savings among residents in Bangkok and its vicinity in the second quarter of 2021, approximately 62.8% of borrowers expressed interest in applying for assistance measures from financial institutions, with the most appealing measure being debt moratoriums (50.4%) due to short-term liquidity issues faced by borrowers. Many financial institutions have already implemented this in the past. Other measures of interest included reducing installment payments and extending debt terms (20.3%), lowering monthly payments (16.0%), and consolidating debts with other loans for debt restructuring (9.8%). Notably, these latter measures aim to help adjust borrowers' debt burdens to be more in line with their current income-earning capabilities.

Therefore, the key issue moving forward is the urgent implementation of measures to support liquidity and restructure debts to prevent borrowers from becoming non-performing loans (NPLs). Currently, various related agencies, including the Bank of Thailand, commercial banks, and other financial institutions, are preparing to assess the appropriateness of measures and adjust them to align with the economic context and the status of each borrower to ensure clear progress in this matter and sustainably address borrowers' debt issues, ultimately benefiting both borrowers and creditor financial institutions.