Thailand's GDP in Q2/2021 Grows 7.5% Due to Low Base Effects, Supported by Exports and Government Spending

Thailand's GDP in Q2/2021 grew by 7.5% due to low base effects, supported by exports and government spending. Meanwhile, domestic private sector demand has entered a recession, contracting for two consecutive quarters due to the impact of the third wave of the outbreak.

• The Thai economy in Q2 2021 expanded by 7.5% year-on-year, primarily due to a low base from the previous year. The quarter-on-quarter seasonally adjusted growth of 0.4% reflects a relatively stable economy with limited momentum. The recovery of the Thai economy is uneven across sectors; the export sector has rebounded well alongside continuous government spending, while private sector demand (consumption and private investment) remains sluggish and has entered a recession, contracting for the second consecutive quarter due to the impact of the third wave of the outbreak. In terms of production, the Thai economy also shows uneven recovery; the agricultural sector has rebounded well due to favorable weather conditions, while industrial production has recovered in line with the export sector, but the services sector continues to contract and has entered a recession.

• Looking ahead, the EIC expects the economy in Q3/2021 to continue to decline due to the prolonged outbreak and the impact of lockdown measures that began on July 20, 2021. Mobility indicators from both Google and Facebook indicate that the impact of the outbreak has worsened since July, suggesting a high likelihood of further economic decline in Q3. However, if the outbreak can be better controlled in Q4, along with progress in vaccination, it will help the economy start to recover, which is a positive factor for reducing daily infection rates and easing lockdown measures, allowing more economic activities to resume.

• Overall, the latest GDP figures align with the EIC's forecast that the Thai economy will grow by 0.9% in 2021 under the baseline scenario, relying heavily on exports and government stimulus measures. The ongoing domestic outbreak has significantly impacted business operations and reduced consumer spending, exacerbating economic scars related to business closures, labor market conditions, and debt burdens, leading to a sluggish economy with slow recovery prospects.

• Additionally, the Thai economy faces several downside risks, particularly regarding the current domestic outbreak, which may worsen beyond expectations in terms of infection rates and control duration, as well as potential delays in vaccination. Furthermore, monitoring the closure of several factories that may impact production and exports is essential. There are also risks related to government spending measures that may be less than anticipated, and finally, the emergence of new virus variants that may resist vaccines, which could affect global economic recovery.

Key points

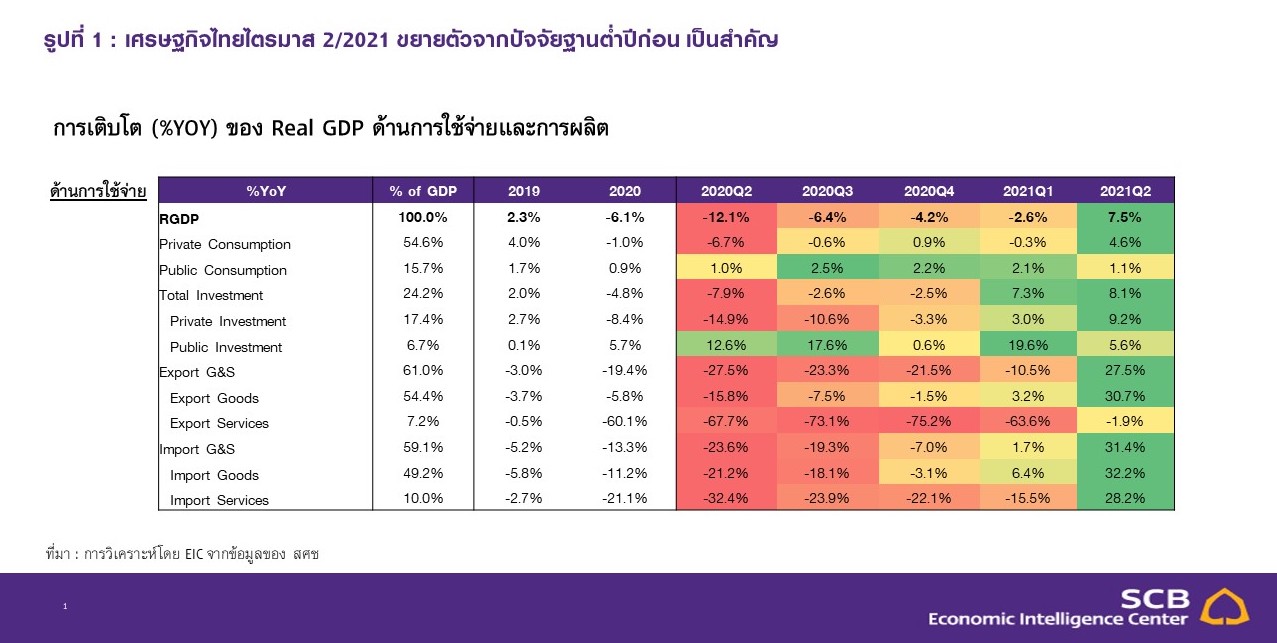

The Thai economy in Q2 2021 grew by 7.5% year-on-year after contracting -2.6% year-on-year in the previous quarter. When compared to the previous quarter on a seasonally adjusted basis (%QOQ_sa), the Thai economy expanded slightly by 0.4% QOQ_sa (compared to 0.2% QOQ_sa in Q1/2021).

Figure 1: Thailand's economy in Q2/2021 grew significantly due to low base effects from the previous year.

Source: Analysis by EIC from NESDC data.

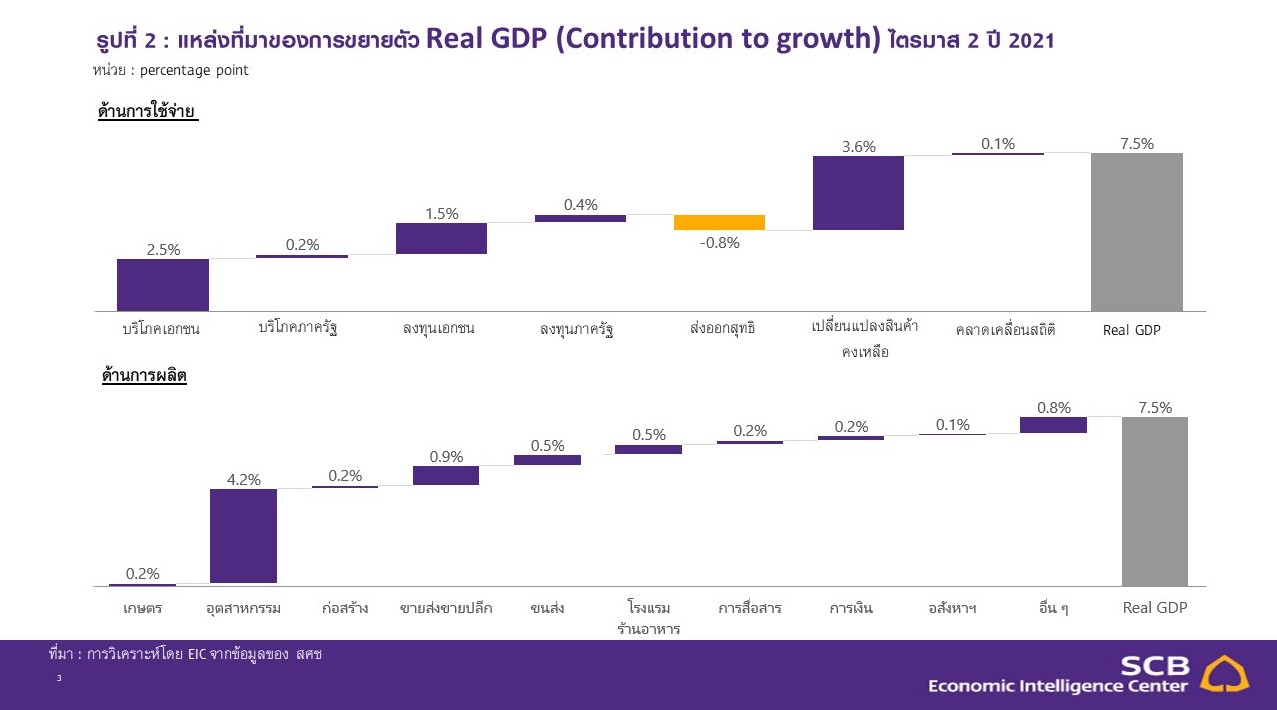

Figure 2: Sources of Real GDP growth (Contribution to growth) in Q2 2021.

Source: Analysis by EIC from NESDC data.

In terms of expenditure, all sectors of the economy expanded due to low base effects, except for the services export sector, which continued to contract.

• The value of real goods exports grew at an accelerated rate of 30.7% year-on-year, mainly due to low base effects in Q2/2020 and the recovery of the global economy, which positively impacted Thai exports, particularly in the automotive, electronics, electrical appliances, metals, machinery, chemicals, and petrochemical sectors.

• Public investment grew by 5.6% year-on-year, especially in construction, which expanded by 9.0% year-on-year, while investment in machinery contracted by -4.7% year-on-year. Public spending expanded by 1.1% year-on-year, continuing from the previous quarter.

• Private consumption rebounded, growing by 4.6% year-on-year after a slight contraction of -0.5% year-on-year in the previous quarter. This growth was mainly due to low base effects in Q2/2020, along with government economic stimulus measures that provided some support. However, when compared to the previous quarter on a seasonally adjusted basis, private consumption contracted by -2.5% QOQ_sa, reflecting the impact of the third wave of the outbreak that began in April.

• Private investment grew by 9.2% year-on-year due to improved investment in machinery (12.2% year-on-year), aligned with the export sector, while construction investment continued to contract by -0.2% year-on-year. However, when compared to the previous quarter on a seasonally adjusted basis, private investment contracted by -2.5% QOQ_sa due to the impact of the recent outbreak.

• The services export sector, particularly tourism, continued to contract at -1.9% year-on-year, although the situation improved with increased revenue from freight services and other business services. However, revenue from tourism and passenger transport remained significantly low due to the limited number of foreign tourists.

• The value of goods imports grew at an accelerated rate of 32.2% year-on-year, following the recovery of goods exports, while service imports rebounded, growing by 28.2% year-on-year from a previous contraction of -15.4% year-on-year in the prior quarter, mainly driven by increased freight service costs, while tourism expenditure continued to contract.

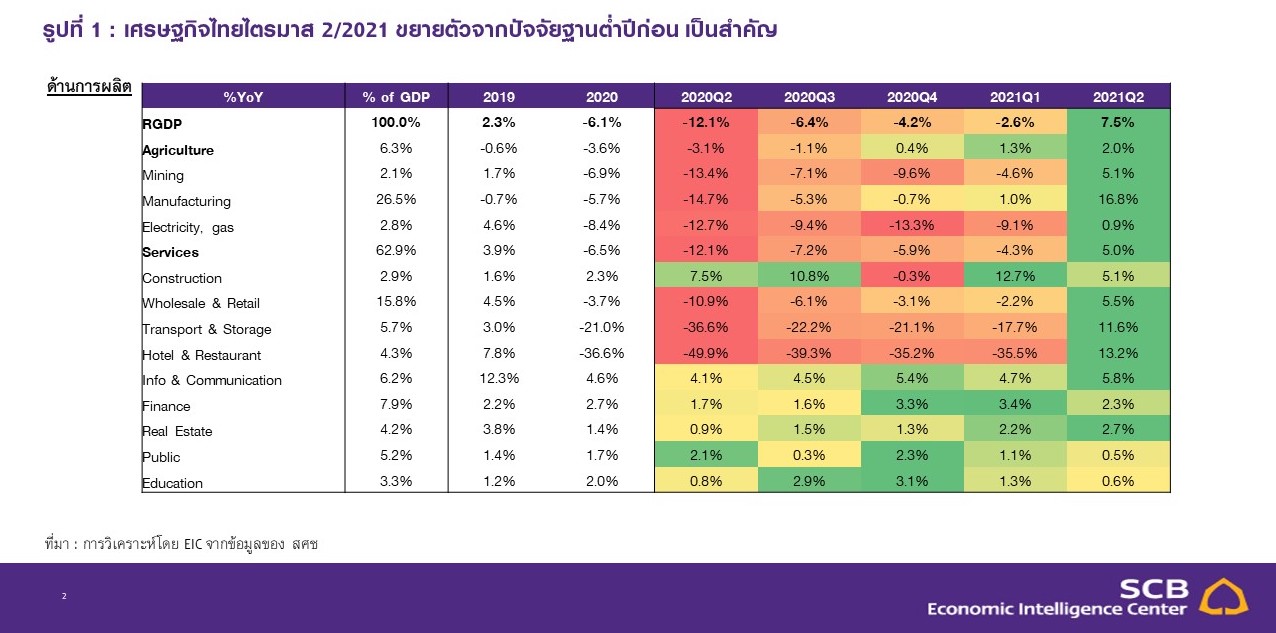

In terms of production, all production sectors expanded significantly due to low base effects.

• The agricultural sector grew at an accelerated rate of 2.0% year-on-year, up from 1.3% year-on-year in the previous quarter, driven by the growth of key crops such as paddy, rubber, pineapple, and cassava.

• The industrial sector expanded at an accelerated rate of 16.8% year-on-year, primarily due to the growth of the export sector.

• The wholesale and retail trade sector rebounded, growing by 5.5% year-on-year after contracting -2.2% year-on-year in the first quarter, driven by low base effects and government economic stimulus measures.

• The accommodation and food services sector grew by 13.2% year-on-year, recovering from a decline of -35.5% year-on-year in the first quarter, due to low base effects, domestic tourism activities in April and May, and government support measures that helped stimulate some spending.

Implications

The Thai economy in Q2 2021 was impacted by the third wave of the outbreak, resulting in continued low stability.

Due to the abnormal low base effects from the previous year, analyzing the figures as a percentage year-on-year with high growth rates may not accurately reflect the current economic situation. Therefore, a seasonally adjusted quarter-on-quarter analysis (%QOQ_sa) shows that overall GDP grew slightly by only 0.4% QOQ_sa in Q2 (after a slight growth of 0.2% QOQ_sa in the first quarter), indicating continued low stability since the end of the previous year due to the impact of the third wave of the outbreak that occurred in April, despite support from the export and public sectors. This economic condition aligns with EIC's previous expectations, but the actual figures were better than market forecasts, as reflected by the median of Bloomberg consensus, which anticipated GDP growth of only 6.6% year-on-year or a contraction of -1.1% QOQ_sa (EIC expected 6.4% year-on-year and -1.2% QOQ_sa), differing from the actual figures where %QOQ_sa still showed growth, preventing the Thai economy from entering a technical recession in Q3. The Thai economy continues to exhibit significant differences in recovery, with the export sector recovering well while domestic private sector demand remains sluggish due to the outbreak.

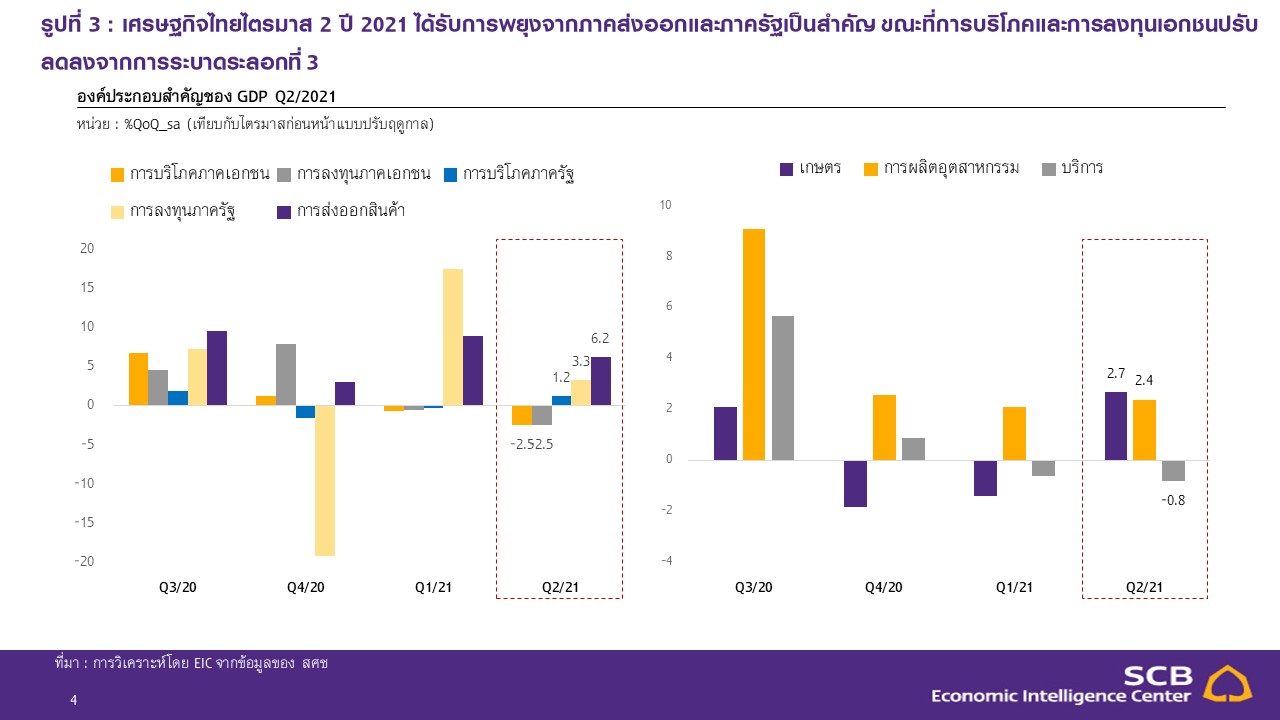

As seen in Figure 3 (left), it is clear that the Thai economy in Q2 was significantly supported by the export sector, although the contribution of net exports was negative due to high import growth. However, exports still indirectly supported the economy through improved income for exporters and workers in the export sector, as well as an increase in inventory changes for various industrial goods to accommodate foreign orders, such as plastics, synthetic rubber, computers, automotive equipment, jewelry, and gemstones. Additionally, the government continued to inject funds into the economy in Q2, both in terms of consumption and public investment, especially in construction. There were also funds to support citizens through various measures, such as the 'We Win' project and the 'M33 We Love Each Other' project, which will be recorded in private consumption. However, domestic private sector demand has already entered a recession, reflected by negative growth rates in consumption and private investment on a %QOQ_sa basis for two consecutive quarters due to the impact of the third wave of the outbreak.

In terms of production, the Thai economy also shows uneven recovery. The agricultural and industrial sectors continue to grow, while the services sector remains sluggish. As seen in Figure 3 (right), agricultural production has rebounded well due to favorable weather conditions, while industrial production has continued to recover in line with the export sector. However, the services sector, which includes several key businesses such as wholesale and retail, transportation, hotels, and restaurants, continues to contract compared to the previous quarter due to the direct impact of the third wave of the outbreak in Q2, which has put high-risk service businesses into recession as well.

With two consecutive quarters of contraction on a %QOQ_sa basis, the services sector is the most critical part of the Thai economy in terms of GDP share and employment, accounting for about 62.8% of GDP in 2020 and 46.6% of total employment (approximately 17.6 million people). Therefore, the continued pressure on the services economy from the outbreak will keep the overall economy sluggish, even with some benefits from the recovery of the agricultural and industrial sectors.

Figure 3: The Thai economy in Q2 2021 was primarily supported by the export and public sectors, while private consumption and investment declined due to the third wave of the outbreak.

Source: Analysis by EIC from NESDC data.

Looking ahead, the economy in Q3/2021 is expected to continue to decline due to the prolonged outbreak

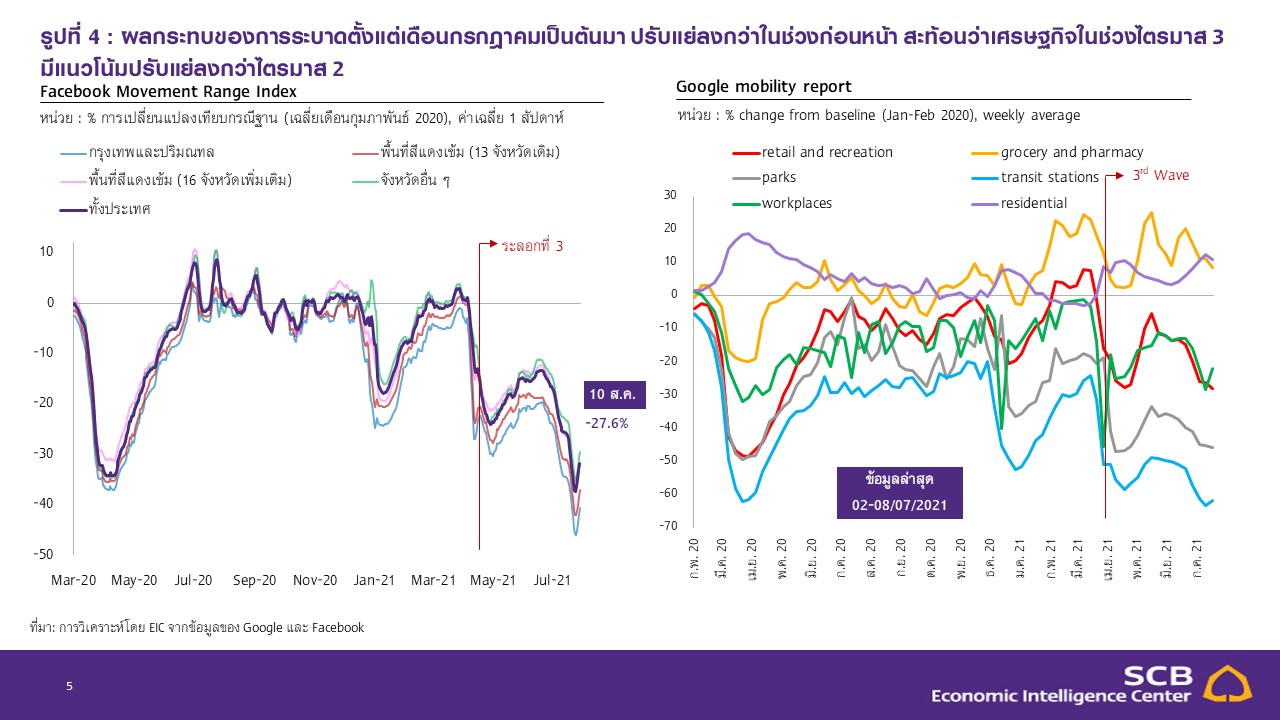

before starting to recover in Q4/2021. The economy in Q3 will still be affected by government lockdown measures that began on July 20, 2021, preventing restaurants, shopping malls, and other businesses from fully opening. Meanwhile, consumer spending is expected to be cautious, and many sectors' incomes will significantly decrease, especially face-to-face businesses such as hotels, restaurants, massage, spas, and nightlife businesses, which will negatively impact employee income and employment conditions. High-frequency data in Figure 4 clearly shows that mobility indicators from both Google and Facebook indicate that the impact of the outbreak has worsened since July, reflecting that the Thai economy may further decline in Q3. However, in Q4, the economy is expected to start recovering in line with vaccination progress, with an estimated 30-40% of the population receiving at least one vaccine dose by the end of Q3, which is a positive factor for reducing daily infection rates and allowing various economic activities to resume fully, such as restaurants, shopping malls, beauty services, and tourism from both Thai and foreign visitors.

Figure 4: The impact of the outbreak since July has worsened compared to the previous period, indicating that the economy in Q3 is likely to decline further than in Q2.

Source: Analysis by EIC from Facebook and Google data.

Overall, the Thai economy in 2021 is expected to be another year of sluggishness due to the impact of the domestic outbreak.

However, it will be driven by strong growth in goods exports and government measures. Although global trade has slowed down somewhat recently, it continues to grow, especially due to the strong recovery of economies in developed countries. In terms of the domestic economy, it is expected to remain sluggish due to the impact of the current domestic outbreak, along with worsening economic scars, including worsening business closures, a more fragile labor market, and high household debt burdens, which will be significant obstacles to future recovery. Nevertheless, government measures will be crucial in supporting the economy, and the EIC expects that the government will need to implement additional measures beyond the current ones, leading to the overall use of loans from the 1 trillion baht emergency decree and an additional 200 billion baht from the 500 billion baht emergency decree.

Moreover, the Thai economy still faces several downside risks, particularly regarding the current domestic outbreak, which may worsen beyond expectations in terms of infection rates and control duration, as well as potential delays in vaccination. Additionally, monitoring the closure of several factories that may impact production and exports is essential. There are also risks related to government spending measures that may be less than anticipated, and finally, the emergence of new virus variants that may resist vaccines, which could affect global economic recovery. In summary, the Q2 economic figures align with the latest EIC forecasts, which project that the Thai economy will grow by 0.9% in 2021. In the meantime, the EIC is conducting a detailed analysis of the current situation and will release updated forecasts in early September.

Analysis by SCB EIC >>>> https://www.scbeic.com/th/detail/product/7740

Authors of the analysis: Ph.D. Aruneeniramarn ([email protected]), Senior Economist

Vishal Gulati ([email protected]), Analyst

Economic Intelligence Center (EIC)

Siam Commercial Bank Public Company Limited

EIC Online: www.scbeic.com