Rising Defaults: No Impact on China's Economy (Kasikorn Research Center)

China's economic stimulus measures following the global financial crisis in 2008 have successfully driven the country's growth to an average of no less than 6% per year over the past century. However, these measures have also created lingering issues that need to be addressed, particularly the corporate debt problem, which surged from 94% of GDP in 2008 to 161% of GDP in 2020. The issue of China's debt has resurfaced as concerns grow over continuous reports of bond defaults. The scale of these defaults has significantly increased amid the ongoing global COVID-19 pandemic and escalating international political tensions. Nevertheless, the Kasikorn Research Center assesses that the defaults occurring at this time represent company-specific risks that are unlikely to escalate into systemic risks. However, it is essential to closely monitor household debt and the real estate bubble, as failure by the Chinese authorities to control these issues could exacerbate existing problems and potentially lead to a financial crisis.

In the first half of 2021, defaults by large Chinese companies continued to raise concerns, even though the number of defaults decreased from 17 cases worth 92 billion yuan in the first half of 2020 to only 11 cases worth 95 billion yuan in the first half of 2021. However, the average value of defaults per case has significantly increased, reflecting that defaults are occurring among larger companies, which could have a more substantial impact on the market and investors, particularly with the rising defaults among state-owned enterprises in traditional energy and real estate sectors. This trend has been observed since the Chinese authorities reduced their intervention in 2015 to reform unprofitable state-owned enterprises (zombie companies), allowing these companies to gradually go bankrupt according to market mechanisms to reallocate resources to more productive economic activities. Despite the significant debt issue in China, the risk of defaults is not seen as likely to lead to a financial crisis for the following reasons:

1) The financial position and reserves of Chinese commercial banks remain strong. The banking sector has managed the risks arising from the COVID-19 crisis effectively and plays a crucial role in supporting economic recovery. The non-performing loan (NPL) ratio has decreased from last year's peak of 1.96% in September 2020 to 1.75% in June 2021, while the capital adequacy ratio has continuously strengthened, standing at 14.48% in June 2021 compared to 14.21% in the same period last year.

2) The Chinese authorities can manage the timing and magnitude of NPL recognition. This will help mitigate the risk of widespread market impact, as potential bad debts primarily involve state-owned enterprises rather than household debts. Most of these debts are owed to state-controlled commercial banks, allowing the authorities to choose the timing and industry types for assistance to minimize broader impacts.

3) The outlook for China's economic growth remains positive. In 2020, when the global economy faced recession amid heightened geopolitical risks, China's exports may slow down in the future. However, China is preparing to reduce its reliance on exports and shift towards domestic consumption, with consumption accounting for 37.7% of GDP at the end of 2020, which is low compared to Western countries (e.g., the U.S. has a consumption ratio of 67.9% of GDP). China is also focusing on rapidly developing R&D to lead in technology in the new era and in clean energy technology, as reflected in long-term strategic plans such as becoming a leader in artificial intelligence (AI 2030) and setting new technology standards (China Standards 2035), along with the goal of carbon neutrality by 2060. These strategies will drive China's economy in the coming era.

However, the Kasikorn Research Center emphasizes two factors that need close monitoring: household debt and the real estate bubble. If the Chinese authorities cannot control these issues, they could significantly exacerbate the existing problems of state-owned enterprise debt and potentially lead to a financial crisis.

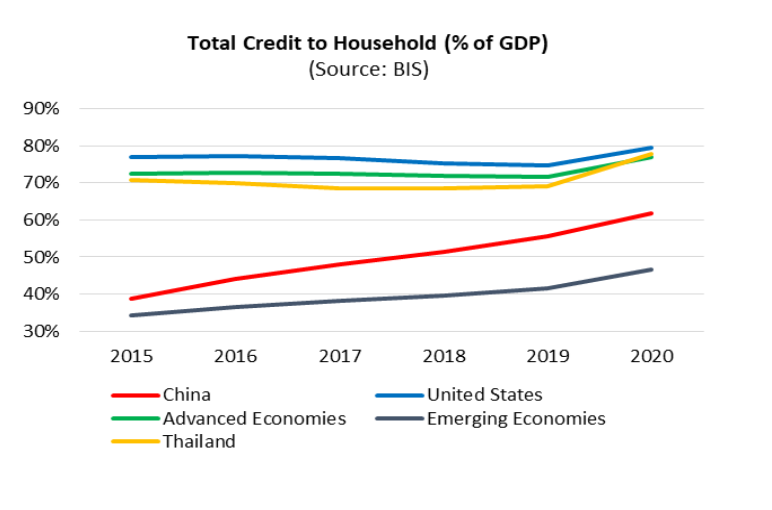

1) The accelerating household debt problem. Although China's household debt ratio at the end of 2020 was still low at 61.7% of GDP compared to developed countries (77.1% of GDP) and lower than Thailand (77.8% of GDP: according to BIS), the rapid increase has raised concerns among the authorities, leading to a more active role in managing this issue. This is evident from the suspension of IPO sales by major companies primarily engaged in consumer lending, as well as the introduction of additional regulations regarding online consumer lending.

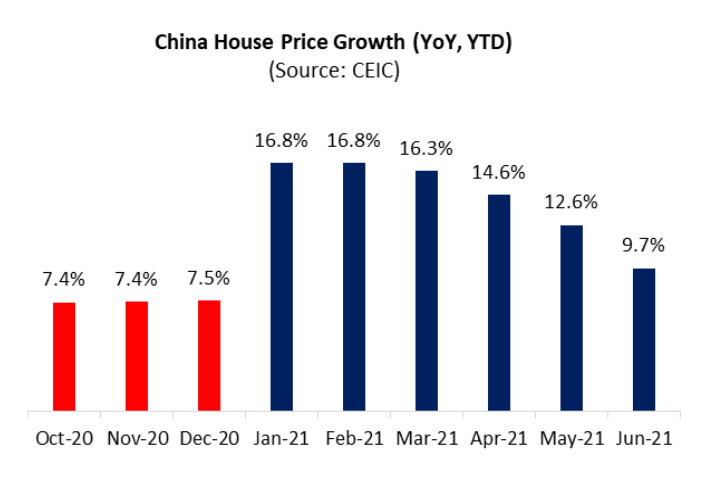

2) The real estate bubble problem. Real estate prices in China rose sharply in early 2021, prompting the authorities to implement various measures to prevent a potential bubble, such as setting price ceilings, increasing down payment rates, raising borrowing interest rates, and imposing quotas on property purchases. However, while average housing prices nationwide have declined, prices in major cities remain high. Although the measures implemented have somewhat cooled the real estate market, it remains a critical issue that requires close monitoring.

In summary, the current debt defaults in China are a result of the country's state-owned enterprise reforms and the decision to let market mechanisms address the zombie company issue. It is believed that the Chinese authorities are still capable of managing these issues without allowing widespread impacts. However, household debt and the real estate bubble remain risks that could exacerbate existing problems amid an economic environment still facing uncertainties from the COVID-19 pandemic and escalating tensions between China and the U.S. and its allies.

Thank you for the information from the Kasikorn Research Center.