In-Depth Analysis of Thailand's Financial Situation - International Context 2020

The economy has significantly slowed down during the COVID-19 crisis, contracting in many countries. The lack of confidence in financial markets has prompted the government to implement large-scale and unconventional financial and fiscal measures to support the economy and maintain financial stability.

The fiscal policy can be categorized into three types:

1) Policies supporting both large businesses and SMEs, such as low-interest loan programs and government loan guarantees. Many countries have introduced temporary financial assistance measures to ensure the flow of credit does not halt during periods of high business risk.

2) Policies supporting households, such as direct financial aid to affected households, unemployment benefits, and extended support periods. The household spending support varies by country; for instance, Hong Kong provides HKD 10,000 to employees over 18, while Singapore offers more support to low-income individuals than to high-income earners. The U.S. has extended unemployment insurance from 26 weeks to 39 weeks and increased benefits by an additional USD 600.

3) Policies increasing general public spending, such as government investment in building and upgrading hospitals or care centers and funding research related to virus prevention and treatment.

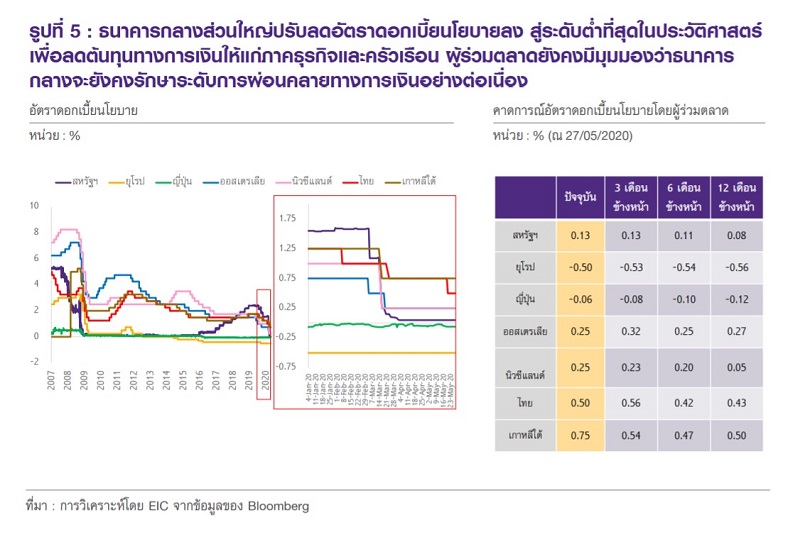

For monetary policy, most central banks have lowered policy interest rates to the lowest levels in history and have implemented a wider range of unconventional financial measures. The aim of reducing policy interest rates is to lower financial costs for businesses and households. Additionally, market participants believe that central banks will continue to maintain this level of monetary easing for at least the next year.

Monetary policy, aside from normal measures, can be divided into four categories:

1) Asset purchase measures to reduce the cost of funding for businesses through the bond market and ensure liquidity in the financial system. This also supports interest rates in the money market moving in the same direction. The types of assets purchased can vary, including government bonds, corporate bonds, mortgage-backed securities, or covered bonds.

In some countries, such as the Eurozone, the UK, and Japan, specific measures have been introduced to support businesses raising funds through corporate bonds. These include purchasing bonds in both primary and secondary markets through programs like the Corporate Sector Purchase Program (ECB) or the Corporate Bond Purchase Scheme (BOE), with most bonds purchased needing to have a good credit rating (investment-grade bonds). The result of these asset purchases has led to a rapid increase in the size of central bank balance sheets.

2) Targeted soft loan measures where central banks provide low-interest loans to commercial banks for onward lending to businesses or households. For example, the EU's Targeted Longer-Term Refinancing Operations (TLTROs) require commercial banks to lend to a target level to receive low-interest loans from the ECB.

3) Liquidity support measures for businesses to facilitate funding in the bond market and inject liquidity into the system to prevent defaults by financially distressed companies (funding backstop). Another type of measure aims to support the continued lending of commercial banks during crises.

4) Relaxation of regulatory requirements for commercial banks to make it easier for them to lend, such as relaxing the supplementary leverage ratio (SLR) in the U.S.

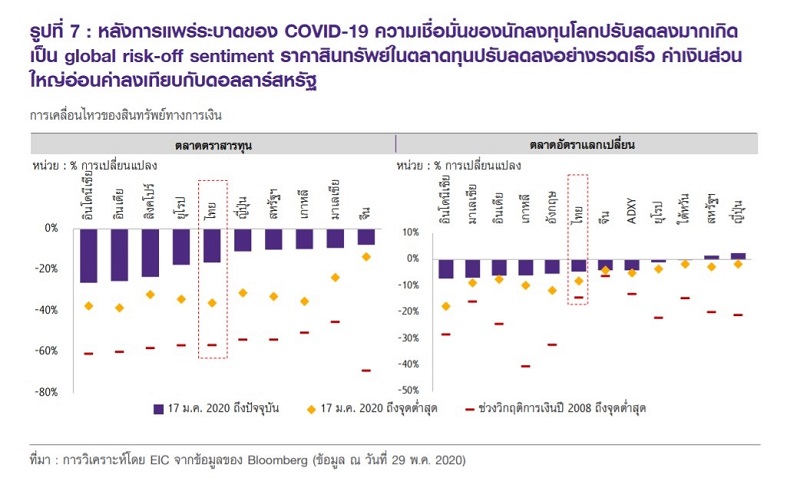

The global spread of COVID-19 has led to a decline in investor confidence, creating a global risk-off sentiment and a dash for cash, with the U.S. dollar rapidly strengthening as investors turned to highly liquid assets like cash. Meanwhile, major global stock indices fell by approximately 30-40%.

Although this decline was less severe than during the GFC, where declines were around 50-60%, the rate of decline during the COVID-19 crisis was faster when compared over the same time frame from the onset of the crisis. The stock indices in the banking, energy, and transportation sectors fell more than the average stock market index due to being more adversely affected by the COVID-19 outbreak.

However, governments and central banks worldwide have implemented economic stimulus policies that have helped restore some investor confidence, leading to a gradual increase in the prices of certain financial assets, with stock markets rebounding after a severe contraction in March when COVID-19 cases surged.

Meanwhile, most currencies depreciated against the U.S. dollar, with the EM currency index weakening by about 3% since the virus was detected (having previously weakened by as much as 5% in early March). Government bond yields rose slightly, while corporate bond yields also decreased.

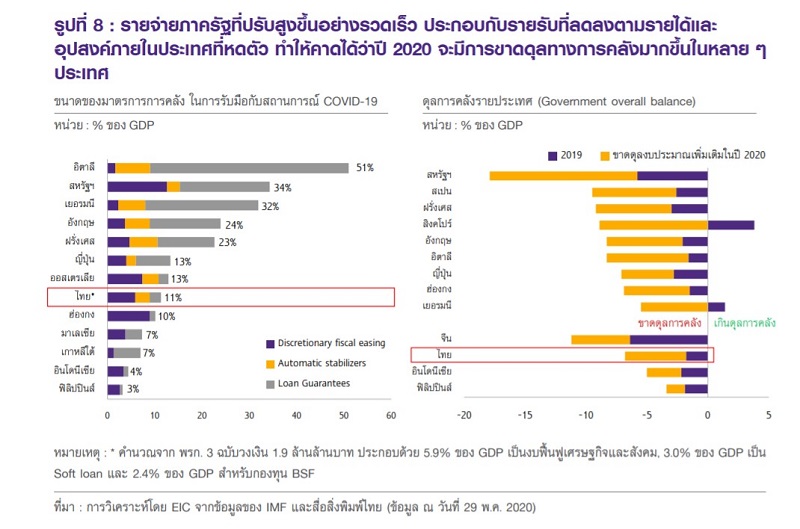

The rapid increase in public and private debt raises the risk of credit rating downgrades due to default risks in the future. To mitigate the impact of COVID-19, governments and central banks worldwide have introduced large fiscal policies supported by relaxed monetary policies, allowing governments to borrow at low costs for economic stimulus measures. However, the rapid increase in public spending and expected declines in tax revenues due to shrinking domestic income and demand will lead to larger fiscal deficits in many countries this year.

IMF forecasts that public debt in advanced economies will rise to 122.4% of GDP in 2020 from 105.2% of GDP in 2019.

Public debt in developing countries is expected to rise to 62% of GDP in 2020 from 53.2% of GDP in 2019.

When considering individual countries, the U.S., Italy, and France are expected to see the largest increases in public debt, while Japan, Italy, and the U.S. will continue to have the highest debt-to-GDP ratios, at 251.9%, 155.5%, and 131% of GDP, respectively.

In the near future, if fiscal deficits and public debt continue to rise, it may adversely affect the economy, leading to a reduction in long-term economic growth, diminishing independence in monetary policy, and increasing risks to the sustainability of public debt.

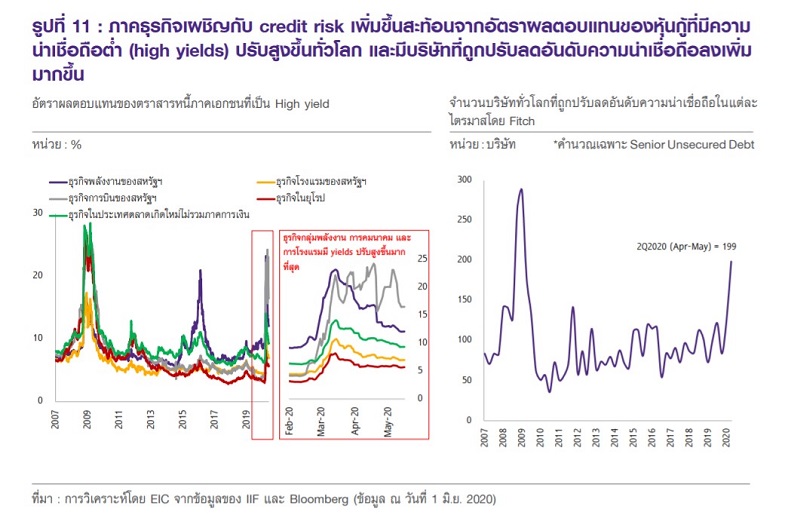

The private sector also faces increased stability risks, reflected in the rising yields of low-rated bonds (high yields) across major economies like the U.S., Europe, and emerging markets (EM).

EIC found that businesses at high risk of default are primarily in sectors severely affected by lockdowns, such as aviation, hotels and tourism, retail, and energy. Additionally, Fitch Ratings data indicates that the number of companies globally downgraded in credit ratings has rapidly increased during Q2 2020, nearing levels seen during the global financial crisis, reflecting the financial vulnerability of businesses due to the economic contraction from COVID-19.

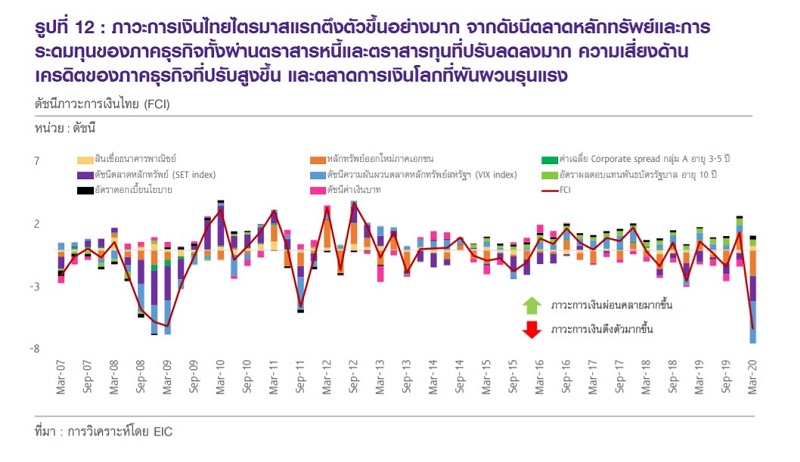

Regarding Thailand's financial situation, the rapid spread of COVID-19 in March-April 2020 indicated that Thailand's financial conditions tightened significantly, approaching levels seen during the 2008-2009 crisis in the first quarter of 2020.

The tightening of Thailand's financial conditions this time resulted from a significant decline in stock market indices and corporate fundraising through debt and equity instruments, increased credit risk in the business sector, and severe volatility in global financial markets. However, government and Bank of Thailand measures have somewhat eased financial conditions in certain aspects, such as lowering policy interest rates to the lowest levels in history, managing government bond yields, and supporting government lending, along with the depreciation of the baht this year, which has contributed to easing financial conditions.

Measures to assist mutual funds affected by liquidity shortages in financial markets have helped reduce panic in the money market. The MFLF measure has increased liquidity for debt mutual funds affected by the severe panic of investors, resulting in rapid redemptions in some high-quality debt funds.

Although in the first half of the year, the Bank of Thailand has reduced the policy interest rate to the lowest level in history at 0.5% and implemented several unconventional measures, EIC assesses that if Thailand's financial conditions tighten again or if financial stability risks flare up, the Bank of Thailand still has the capacity to implement monetary policies to support the economy and maintain the stability of Thailand's financial system.

Monetary policy tools that the Bank of Thailand can still utilize in the future include:

- Reducing the contribution rate to the FIDF fund, with the latest measure reducing the contribution rate from 0.46% to 0.23% for two years. The Bank of Thailand can further reduce the contribution rate, which should lead to lower borrowing rates for commercial banks without significantly impacting deposit interest rates.

- Further reducing the policy interest rate by 25 bps to 0.25%. In EIC's base case scenario (2020 GDP growth -8.0% YOY), the policy interest rate is expected to remain at 0.5% for the remainder of the year. However, in a worse case scenario (2020 GDP growth -11.2% YOY), EIC estimates that the MPC may reduce the policy interest rate again to 0.25%.

- Increasing the volume of Thai government bond purchases to keep Thai government bond yields low and in line with policy interest rates.

- Expanding the scope and types of assets that the Bank of Thailand can purchase, such as allowing the BSF fund to buy bonds in the secondary market, whereas currently, the BSF only purchases bonds in the primary market. The Royal Decree on Financial Stability and Economic Security of 2020 grants the Bank of Thailand the authority to purchase bonds in the secondary market in cases of severe liquidity issues in the bond market and urgent needs for financial stability.

- Expanding low-interest loan measures to cover a broader range of businesses and increasing compensation for financial institutions in cases of borrower defaults. The Bank of Thailand may increase the loan limit per borrower, expand the types of businesses eligible for loans, or increase compensation for financial institutions from the current level of 60%-70% of the amount that financial institutions must set aside from the total debt of borrowers multiplied by the ratio of new debt to total debt to incentivize financial institutions to participate in the program.

- Increasing the types of assets that commercial banks can use as collateral when applying for loans from the Bank of Thailand, such as allowing commercial banks to use various types of loans, including housing loans, car loans, and personal loans, to convert assets into securities (Asset-backed security) and use them as collateral for loans from the Bank of Thailand, similar to the Mutual Fund Liquidity Facility (MFLF) case.

Investment Return Outlook

EIC expects that the yield on short-term Thai government bonds with a maturity of 1 year at the end of 2020 will be in the range of 0.4-0.5%, based on the expectation of maintaining the policy interest rate at 0.5% for the remainder of the year.

For the expected yield on long-term Thai government bonds with a maturity of 10 years at the end of 2020, it is projected to be 0.90-1.00% (down from the previous forecast of 1.65-1.75%). As of May 26, 2020, the yield on 10-year Thai government bonds was 1.04%, down 43 bps from the beginning of the year. In the future, the yield on long-term Thai government bonds is expected to remain low due to external factors, including pressure from long-term U.S. government bond yields and expected low inflation levels this year.

References: Economic Intelligence Center (EIC)

International Monetary Fund (IMF)