The Transformation of the Thai Retail Market Over the Past 30 Years

The Transformation of the Thai Retail Market Over the Past 30 Years

Bangkok, August 15, 2018 – Retail space is one of the most complex types of real estate to develop, as consumer tastes and demands are constantly changing.

The retail space market in Thailand has undergone significant changes over the past 30 years since CBRE opened its office in Bangkok, with transformations accelerating, particularly with the growth of the e-commerce market.

Thirty years ago, the retail landscape in Bangkok consisted of only a few shopping malls and centers, such as Central Plaza Ladprao, which was completed in 1982, Amarin Plaza in 1985, and Siam Center, which has been around since 1973, while other retail spaces were mainly comprised of shophouses and fresh markets.

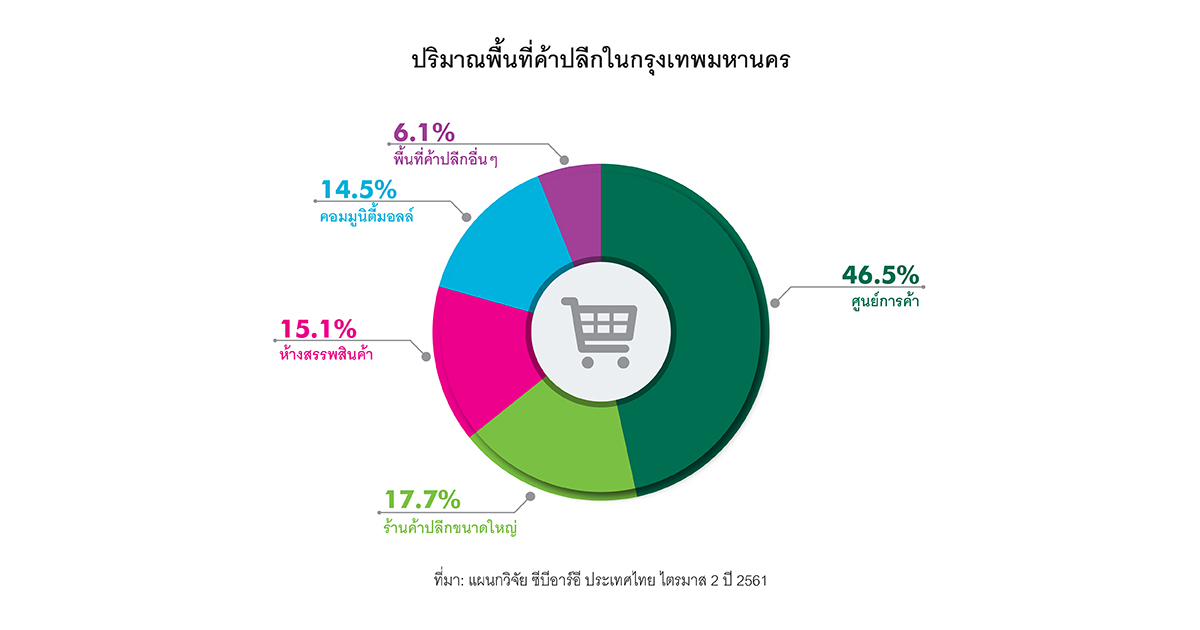

According to a survey by CBRE's research department, Bangkok now has nearly 7.5 million square meters of new retail space, divided into 46.5% shopping centers, 17.7% large retail stores, 15.1% department stores, 14.5% community malls, and 16.1% other retail spaces. There has been rapid growth and change in the types of retail formats and tenants.

Over the past 30 years, we have witnessed a shift from traditional retail stores in fresh markets and shophouses to modern retail spaces, ranging from convenience stores and community malls to large shopping centers like Central Plaza Westgate.

New retail formats have spread across Thailand, with many provincial cities featuring modern shopping centers. The first 7-Eleven convenience store in Thailand opened in 1989, and by 2018, there were a total of 10,268 branches. The first large retail store, Makro Ladprao, located in Bang Kapi district, opened in 1989. Currently, Big C, Tesco Lotus, and Makro have a combined total of over 450 branches in Thailand.

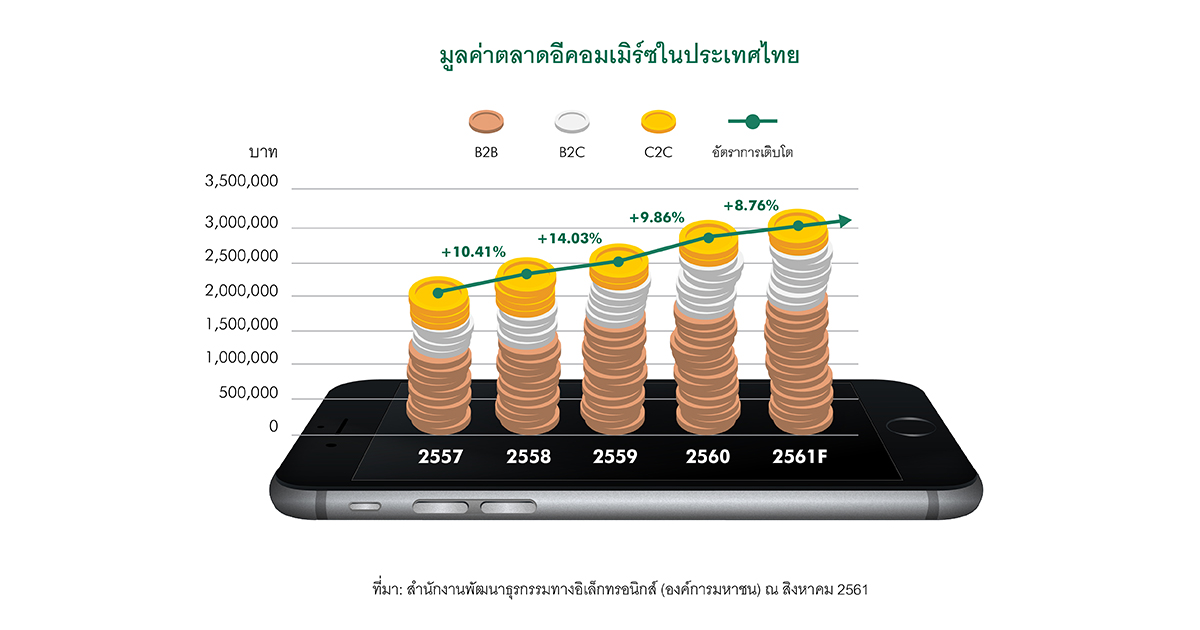

The Thai retail market, like others around the world, faces new challenges from e-commerce. In the UK, e-commerce sales are projected to reach 18% of total retail sales in 2018, while in the US, it stands at 9.5%.

In Thailand, e-commerce sales have not yet reached 1% of total retail sales but are expected to grow rapidly as the e-commerce model and infrastructure, including payment systems and distribution, continue to develop.

Retailers must adapt to provide the best service to customers both in-store and online. Retail space developers need to enhance customer experiences through thoughtful design, events, diverse tenants, and customer service.

Retail space owners must create unique environments that online retailers cannot replicate, such as allocating space for pop-up stores and sharing data with tenants to improve marketing.

"Online" will not replace all "stores," but it will require retailers and retail space developers to adapt. "Simply building aesthetically pleasing structures and filling them with well-known brands will no longer suffice," said Ms. Jariya Thamtrongkitkul, head of the retail space department at CBRE Thailand. "Many retailers are trying to leverage Omni-Channel strategies by integrating both online and offline channels to promote each other."

The continuous change in consumer behavior means that developing retail spaces is more complex than developing office spaces. It requires experienced management, innovative creativity, and ongoing improvements. Retail space owners need to regularly engage with consumers and tenants to understand rapidly changing trends and demands.High levels of commitment and expertise are essential, and unlike hotels, there are very few experts available to manage retail spaces in Thailand.

Even as the economy improves, retailers, retail space owners, and project developers still face significant challenges in adapting to the changing landscape brought about by e-commerce.

"Shopping centers are one of the most successful business formats and are not going anywhere, but competition with e-commerce necessitates the evolution of retail formats to survive," Ms. Jariya concluded.