Kasikorn Research Center Reveals Credit Bureau Data Reflecting the Quality of Business Loans, Benefiting from Debt Restructuring

Kasikorn Research Center examines business debtor accounts from the database of National Credit Bureau Co., Ltd. (NCB) for Q1/2025, finding that smaller businesses face a more pronounced increase in non-performing loans (NPLs) compared to other groups. Meanwhile, the benefits from debt restructuring under the Responsible Lending (RL) criteria and proactive debt quality management by financial institutions have led to a decrease in the proportion of overdue debts of 1-30 days, or Stage 1, since mid-2023. This emphasizes that sustainable solutions to the problem of poor-quality business debt require favorable macroeconomic conditions to help Thai businesses remain competitive and profitable in the long term.

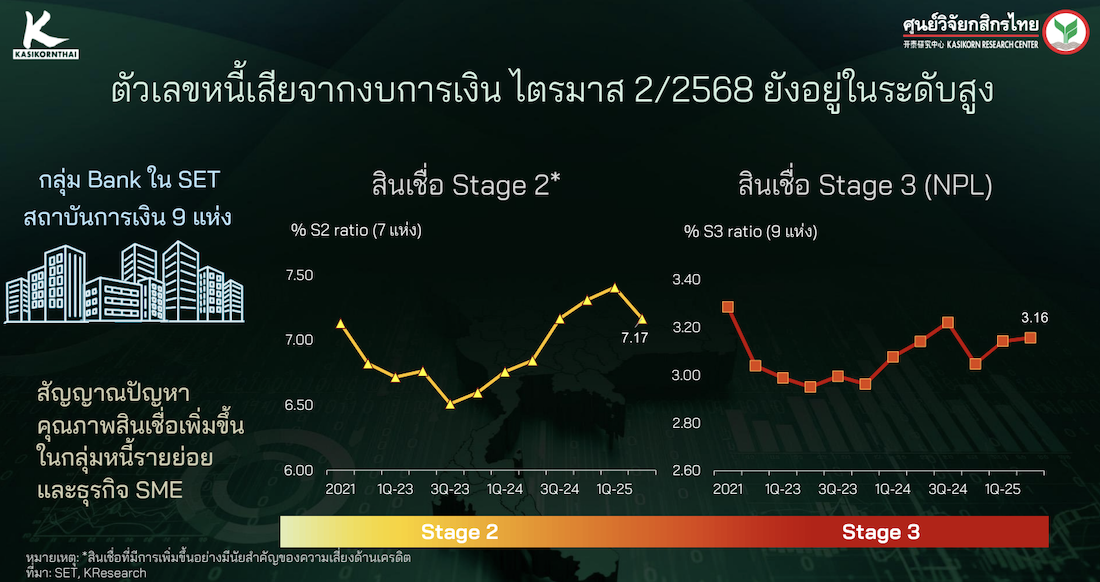

Ms. Thanyalak Watcharachaisurapol, Deputy Managing Director of Kasikorn Research Center Co., Ltd., stated that in Q2/2025, the overall picture of bad debts in the nine commercial banks listed on the stock exchange showed a slight increase in NPLs compared to the previous quarter. However, a deeper analysis of the business debtor accounts from the National Credit Bureau Co., Ltd. (NCB) for Q1/2025 reveals that while the trend of problematic debts (Stage 2 and Stage 3) has stabilized since late 2023, it has slightly increased from Q2/2024, which marks one year since the country reopened after COVID. Additionally, smaller businesses are experiencing a more significant increase in NPLs, with the Super Micro group having an NPL ratio of 14.81% of total loans, followed by Micro at 12.11% and small businesses at 9.75%. In contrast, medium and large businesses have NPL ratios of 6.51% and 1.37%, respectively. Nevertheless, the measures for debt restructuring under the Responsible Lending (RL) criteria and proactive debt quality management by financial institutions have resulted in a decreasing trend in overdue debts of 1-30 days since mid-2023.

Mr. Kritsada Kaewhirun, Senior Researcher at Kasikorn Research Center Co., Ltd., revealed that data on debt quality classified by business type shows that businesses linked to domestic and international purchasing power, such as manufacturing and accommodation, are concerning, particularly large businesses with high overdue debts exceeding 30 days. Meanwhile, small and micro SMEs are beginning to show increasing overdue debts. In contrast, businesses linked to domestic purchasing power, such as wholesale and retail, have seen a decline in debt quality among small and micro SMEs, which is now extending to medium-sized businesses. The construction and real estate sectors are also experiencing negative trends affecting large businesses. Given the rising uncertainty in the economy, stemming from the impact of U.S. import tax increases affecting exports and sluggish domestic purchasing power, the ability of various business types to repay debts may decline further in the remaining quarters of this year.

Dr. Kanjana Chokpaisansilp, Research Executive at Kasikorn Research Center Co., Ltd., stated that the classification of business loan accounts based on debtor repayment behavior over the past year has resulted in four groups: Normal (Good), Newly Impaired, On-Off, and Distressed. It was found that 95% of business loan accounts are still classified as Normal, but the proportion of accounts in this category has been gradually decreasing since the post-COVID period. Meanwhile, the On-Off and Distressed groups have increased. This reflects the impact of multiple economic challenges affecting the profitability of Thai businesses.

Smaller businesses are seeing a decreasing proportion of accounts classified as Normal over time. Moreover, while debt restructuring helps delay the transition to bad debt, it is most effective in reviving businesses when initiated as soon as signs of overdue payments appear, rather than after they have become NPLs. The chance of recovering NPLs to a better classification (within one year after restructuring) is less than 10%.

Kasikorn Research Center further suggests that the Thai government should implement debt management measures tailored to the repayment characteristics of each customer group. This could include enhancing policies to support temporary adjustments to repayment terms for regular customers who have not defaulted and recognize early signs of business issues. Additionally, a new Asset Warehousing project could be prepared as a proactive measure before debtors become NPLs. Once a debtor becomes an NPL, promoting out-of-court workouts, such as asset transfers to settle debts, should be encouraged, with the government supporting this by reducing related fees, such as transfer fees for properties and land.

Furthermore, as the duration of overdue payments increases, the likelihood of falling into deeper debt levels rises compared to the chance of recovery to good debt status. Therefore, if the legal process for case consideration is expedited, it could help both debtors and creditors achieve clarity more quickly, allowing debtors to restart their businesses sooner. Options should also be provided for debtors to prioritize selling their assets, which would give them a chance to recover quickly and regain ownership of their original assets. However, these various debt resolution approaches are only temporary fixes. To truly address the persistent issue of poor-quality business debt, favorable macroeconomic conditions are necessary to ensure that Thai businesses can compete and achieve long-term profitability, leading to sustainable management.