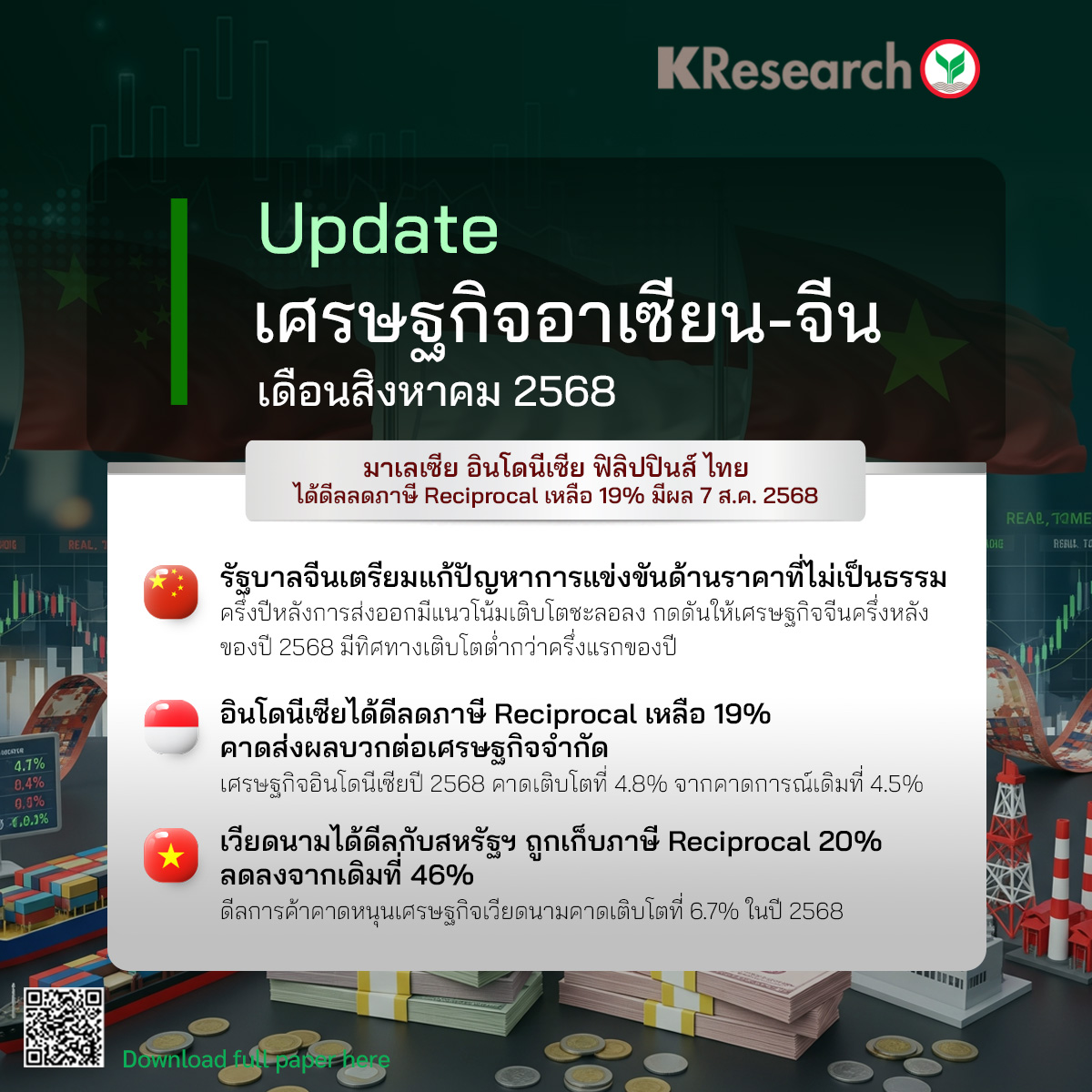

Monitoring ASEAN in the Second Half of 2025: How the Reciprocal Tax is Changing the Global Trade Game

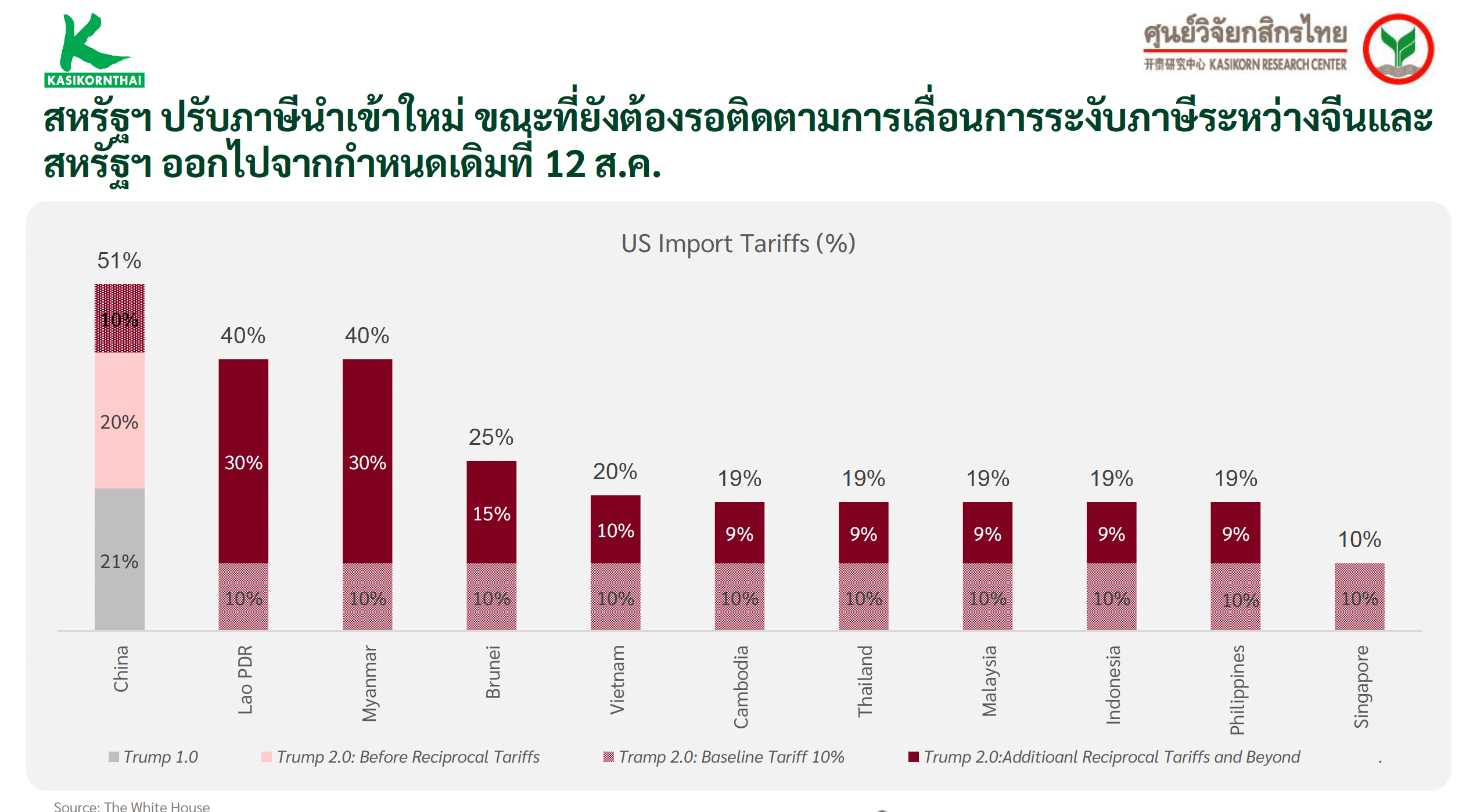

In the second half of 2025, the economies of ASEAN and China are facing renewed pressure from the reintroduction of the Reciprocal Tax by the United States, which impacts the export chains across the region. Despite negotiations to reduce taxes in some countries, exports and investments are beginning to show signs of slowdown.

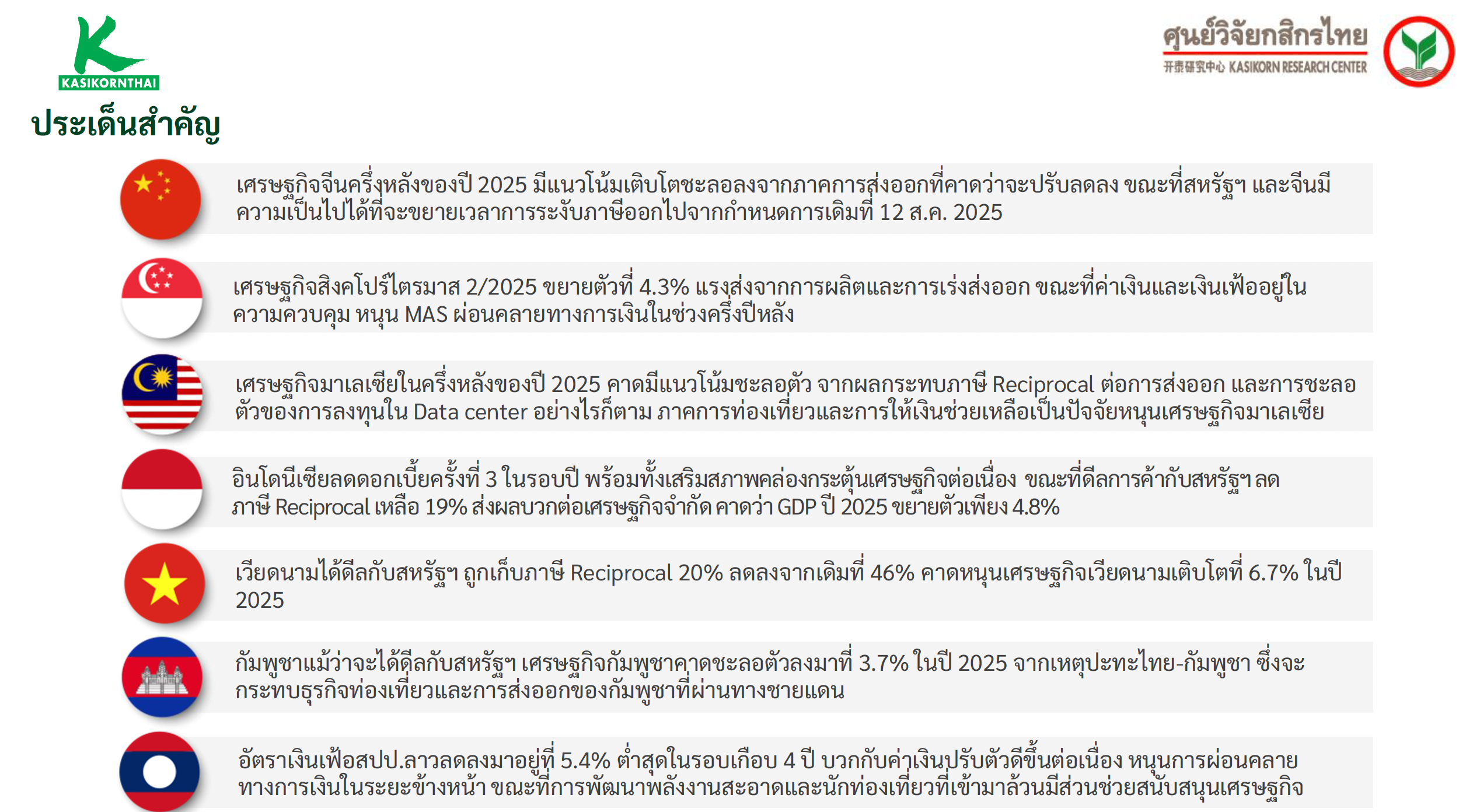

1. China: Internal Slowdown Affects the Entire Region

Although in the first half of the year, China experienced growth from manufacturing and exports, GDP is expected to slow to 4.8% in the second half due to pressures from deflation, intense price competition (involution), and a still-recovering real estate sector. At the same time, overcapacity issues in the Solar and EV industries are squeezing industrial profits and employment conditions.

2. Indonesia: Deal with the U.S. Eases Pressure, but Economy Remains Fragile

Indonesia managed to negotiate a reduction of the Reciprocal Tax to 19% and opened its market to nearly all U.S. imports. However, the economy is still growing at only 4.8% due to falling nickel prices affecting revenues, leading to a weakened rupiah and the sharpest contraction in FDI in Q2/2025 in five years. This is despite the central bank's efforts to stimulate the economy through interest rate cuts and increased lending.

3. Singapore: Exports Recover, but Caution is Needed

GDP in Q2/2025 grew by 4.3%, exceeding expectations due to electronics manufacturing and exports, particularly to Hong Kong and South Korea. However, the impending end of the U.S. tax suspension poses risks of a slowdown in the second half, while the MAS (Monetary Authority of Singapore) begins to ease monetary policy and inject 1.1 billion Singapore dollars to restore confidence in the capital market.

4. Malaysia: Tourism Boosts Economy

Malaysia negotiated a reduction of the Reciprocal Tax to 19%, similar to its neighbors, and is benefiting from a tourism sector that has grown by +20% YoY in the first five months of the year. However, investment in Data Centers is beginning to slow due to rising electricity costs, while the central bank is likely to cut interest rates to support the economy.

5. Thailand: Vulnerable Due to High Export Dependence

Thailand also reduced the Reciprocal Tax to 19%, but its high dependence on exports (accounting for 57.1% of GDP) makes the economy fragile during a global slowdown, with GDP forecasted to be only 4.1% in 2025.

Conclusion: Opportunities and Risks in the Second Half

The Reciprocal Tax is becoming a “game changer” in the global trade arena. While some countries have managed to negotiate more lenient terms, the structural impacts are inevitably dragging down economic growth in Asia.

Opportunities lie in adapting to a stronger domestic economy, accelerating technology development, and increasing reliance on domestic consumption.

Risks stem from geopolitical uncertainties, fluctuating U.S. policies, and domestic issues such as household debt, energy, and income distribution.

Discussion

Follow breaking news Investment property articles on Facebook, click here.