Economic Report July 2025: Thailand and the World Face Friction Amid Uncertainty

In the first half of 2025, the global economy continued to advance under pressure from geopolitical tensions, trade wars, and fluctuations in energy prices. Meanwhile, the Thai economy faced multiple risks, both from external factors and unclear internal political dynamics.

An Uncertain World: War, Tariffs, and Oil Prices

The conflict between Israel and Iran has caused significant volatility in global oil prices. Although Iran accounts for only 4.6% of global oil supply, the Strait of Hormuz, which is a route for over 20% of the world's oil exports, has become a vulnerable point that creates ripples in the energy market. If blocked, it would have a significant impact on global oil prices and exacerbate inflation in many countries.

In terms of trade, delays in negotiations between the U.S. and key trading partners have led to the imposition of reciprocal tariffs, affecting exports from Asian countries, particularly China, Thailand, South Korea, and Vietnam, all of which are facing ongoing pressure.

The U.S. and Europe: Strength Starting to Waver

While the U.S. economy has continued to grow in the first half of the year, the outlook for the second half carries risks from declining private sector demand and inventory accumulation. The Federal Reserve has signaled clearly that it will reduce interest rates twice this year to help the economy avoid recession.

At the same time, the Eurozone economy remains fragile due to high energy costs and the impact of U.S. tax measures that undermine consumer and business confidence.

Thailand in a Risky Situation: Improved Exports but Weak Tourism

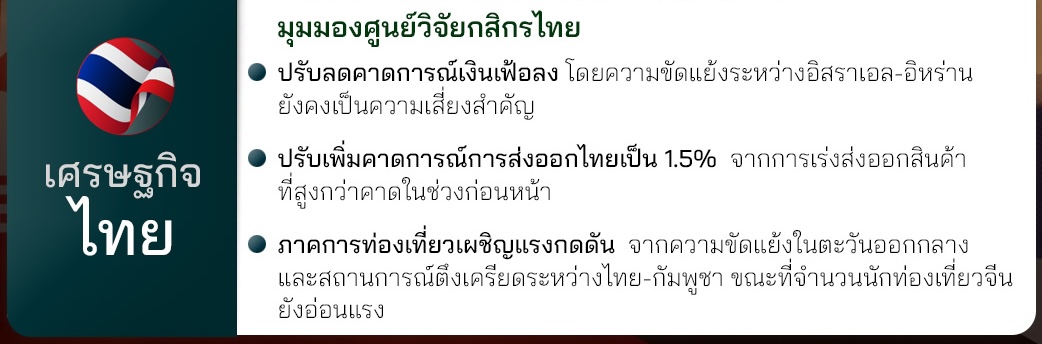

Although the Thai economy continues to grow to some extent, the overall picture remains fragile. Kasikorn Research Center has maintained its GDP forecast for 2025 at 1.4%, reflecting that the economic recovery is not strong enough.

The good news is that exports in the first half of the year grew better than expected, leading to an upward revision of the 2025 export target to 1.5%. However, Thailand still relies on a few key products and faces risks from U.S. tax measures that may impact the second half of the year.

In terms of tourism, which has been a significant driver of the economy, there has been a decline, with the number of foreign tourists in the first five months of the year down by 12.5% compared to the previous year, particularly from China and Malaysia.

Low Inflation but Not “Deflation”

The general inflation rate in Thailand is expected to be only 0.3% throughout 2025, the lowest level in several years, due to falling energy and fresh food prices. At the same time, the import of cheap goods from China continues to pressure domestic prices, especially for consumer goods, reflecting an economy that is still sluggish and domestic demand that has not fully recovered.

Domestic Politics: A Risk Factor to Watch

The unresolved internal political issues are another factor putting pressure on confidence and budget disbursement. The coalition government has only a slim majority in parliament, making it necessary for more stable politics to push through important legislation, including the budget for 2026. If further uncertainty arises, it could hinder economic growth in the future.

Conclusion: The Calm After the Storm Has Yet to Appear

The Thai economy in the second half of 2025 will face challenges from both external and internal factors. The recovering exports may slow down again due to tax pressures, tourism has not returned to full potential, and political uncertainty remains a critical condition.

In this context, both the public and private sectors must collaborate to enhance economic resilience, diversify risks, and proactively plan to prepare for potentially stronger headwinds in the future.

Discussion

Follow breaking news Investment property articles on Facebook, click here.