Banks Begin Gradually Adjusting Loan Interest Rates, Awaiting Impact on Borrowers

KASIKORN RESEARCH CENTER

• Following the Monetary Policy Committee's (MPC) decision to lower the policy interest rate by 0.25% to 2.00% on February 26, 2025, interest rates in the money and bond markets immediately decreased in accordance with the monetary policy transmission mechanism. The short-term money market interest rates (Tenor) of up to 1 year dropped by approximately 0.24-0.25%, while the yield on Thai government bonds with maturities of 1 month to 1 year decreased by 0.08-0.10% (as of March 3, 2025).

• The focus after this MPC meeting is on the announcement of interest rate adjustments by commercial banks, which began within one day following the MPC's decision, specifically regarding the reduction of single loan interest rates.

Major commercial banks in the D-SIBs group are gradually lowering their MLR, MRR, and MOR loan interest rates by approximately 0.10-0.25%, effective from the beginning of March 2025. As of now (March 4, 2025), there has been no adjustment to savings deposit interest rates, including those for 3-month, 6-month, 12-month, and 24-month fixed deposits for individual accounts.

• KASIKORN RESEARCH CENTER believes that the interest rate reduction will affect new loan contracts but will only alleviate the interest burden for current borrowers when their loans enter the reference interest rate adjustment period.

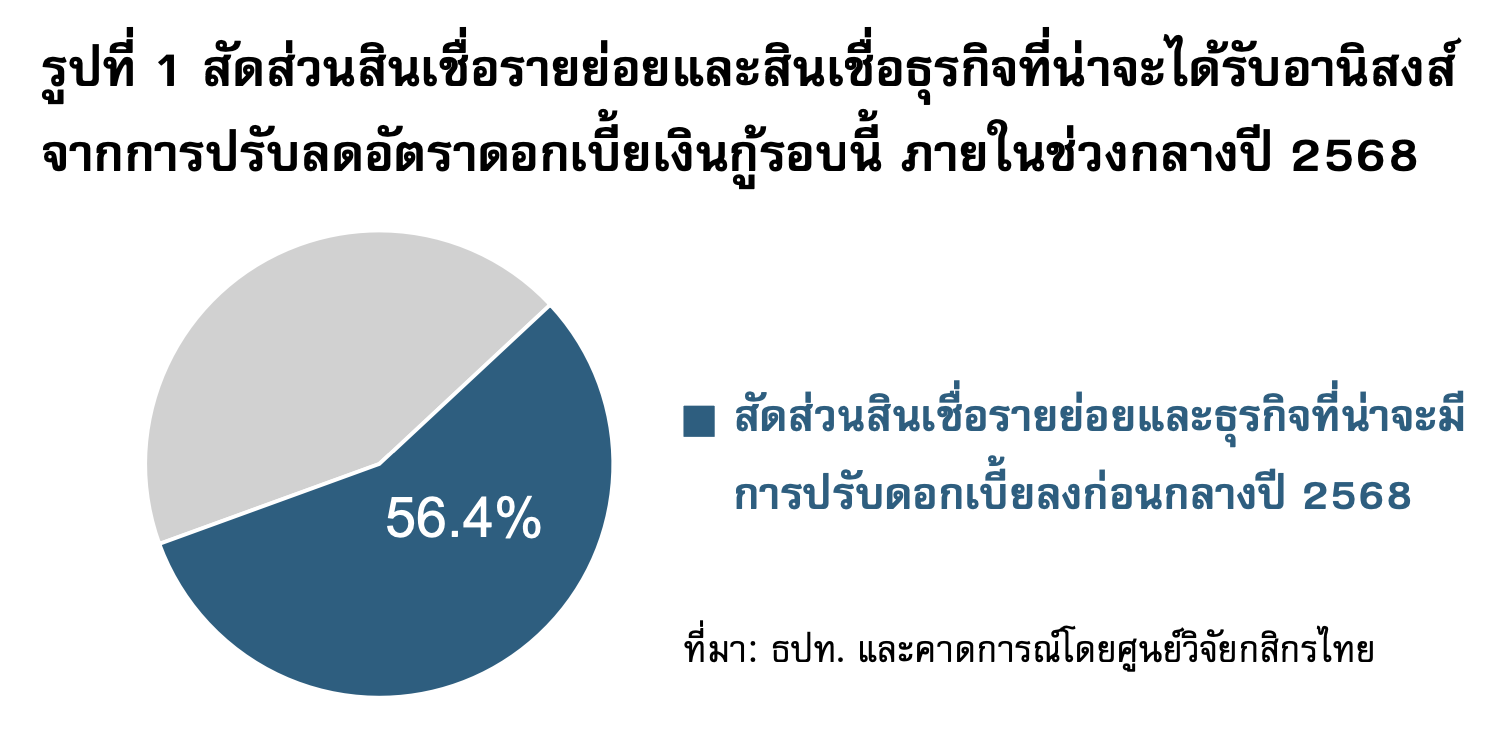

KASIKORN RESEARCH CENTER estimates that retail and business loans likely to benefit from the loan interest rate reduction in the middle of this year will account for approximately 56.4% of total loans in the Thai banking system (see Figure 1). The impact of this recent reduction in single loan interest rates is expected to decrease the interest burden for retail and business borrowers by around 7.3-7.5 billion baht, representing about 1.0-1.2% of the projected net interest income for 2025 (assuming the calculation of the reduced loan interest burden begins between March and December 2025).

• However, it is anticipated that the overall credit growth will remain limited. KASIKORN RESEARCH CENTER maintains its estimate for the growth rate of loans in the Thai banking system for 2025 at 0.6%, a slight recovery compared to the contraction of 0.4% in 2024. This is because, while interest rates are an important factor influencing credit trends, support from other factors, particularly the trend and timing of economic recovery affecting loan utilization, as well as the assessment of borrowers' risk and repayment capacity, will also be necessary. Therefore, two key factors to monitor for the remainder of the year are: 1) whether domestic interest rates will decrease further, and 2) the momentum of credit and the overall economic situation.

KASIKORN RESEARCH CENTER by Kanjana Chokpaisarnsilp, Research Executive