Cancellation of Japan's Negative Policy Interest Rate by Dr. Prasart Tangmattatham

By Dr. Prasart Tangmattatham

The Japanese economy expanded at a very high rate until it experienced a bubble burst due to excessively high real estate prices, leading to a severe contraction and negative growth since 1992. Since then, inflation has remained close to zero.

In this world, many central banks implement monetary policies targeting an inflation rate of 2% per year, adjusting the money supply and/or policy interest rates to achieve this goal. The Bank of Japan is no exception; it began lowering its policy interest rate from 6% in June 1991 to near zero by 1999, maintaining that level for the most part. Haruhiko Kuroda took office as the governor of the Bank of Japan in 2013 during Prime Minister Abe's administration, increasing the central bank's asset purchases by 80 trillion yen per month. However, Japan's GDP continued to grow at just over 1% per year, showing no signs of improvement. In 2016, the Bank of Japan decided to adopt a negative policy interest rate, following several European countries, maintaining a level of -0.1% until the Bank of Japan announced on March 19, 2024, that it would:

1) Cancel the negative policy interest rate

2) End yield curve control while still managing long-term interest rates

3) Cease or reduce asset purchases previously conducted.

One observation regarding the 2% inflation target is that inflation in Japan was too low at that time. Low inflation indicates that demand is less than supply, resulting in minimal economic growth. The secondary target, following inflation, is to focus on economic growth by increasing the money supply and/or lowering interest rates to boost borrowing for investment, which would subsequently lead to economic expansion.

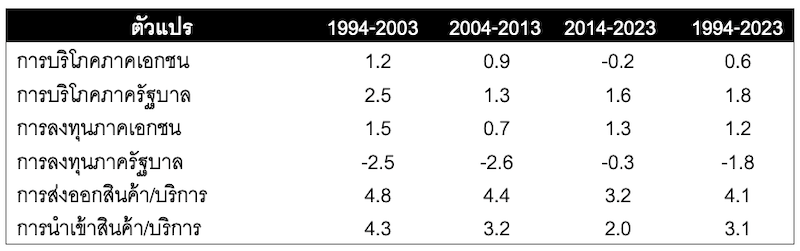

Table 1: Economic Growth Rates of Various Variables Over Different Periods in Japan (Unit: Percent)

Source: Calculated from data by the Japanese Prime Minister's Office

Table 1 shows the growth rates of various economic variables over different periods in Japan. Generally, consumption and private investment account for over 80% of the overall economic growth rate. When examining different periods of ten years, it is evident that the period following the bubble burst (1994-2003) saw the economy remain relatively stable but deteriorate progressively thereafter, culminating in the last decade (2014-2023). Therefore, the data in Table 1 suggests that increasing the money supply and maintaining a negative policy interest rate did not lead to any improvement in the economy.

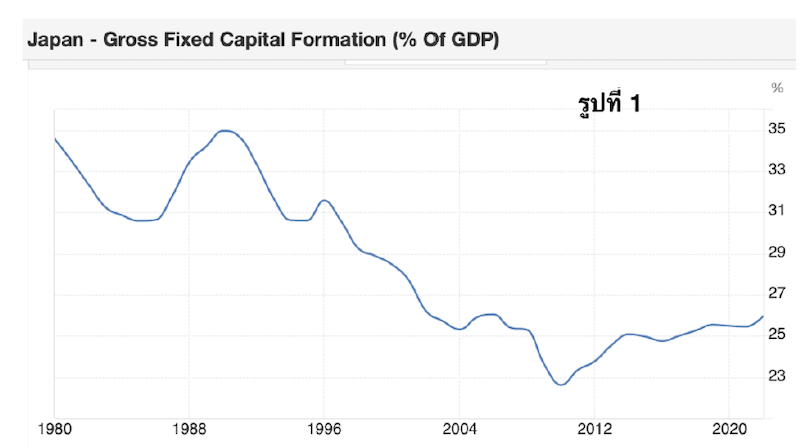

Figure 1 illustrates the investment-to-GDP ratio in Japan. This ratio declined during the Plaza Accord around 1985, when Japan had to invest overseas due to the appreciation of the yen, which also reduced domestic investment relative to GDP. Statistics on domestic and foreign investment in Japan from JETRO support this. Typically, investment drives economic growth in the year of investment and in subsequent years as the investment generates output, a phenomenon observed globally. Thailand and China have faced similar issues. Thus, a significant reason for the decline in Japan's economic growth is the loss of investment within the system. When investment is lost due to overseas ventures or a lack of domestic investment, monetary policy cannot stimulate investment domestically. This is particularly evident from the consistently negative growth rate of public investment in Japan, leading to reduced income for the populace and a decline in private consumption growth.

Now, returning to the reasons behind the cancellation of the negative policy interest rate by the Bank of Japan, the core inflation rate in Japan has exceeded 2%, the target set since 2022, and has remained above 2% this year. However, a deeper reason is the depreciation of the yen by about 40% over two years, which has significantly increased the prices of imported goods. Simultaneously, the weaker yen compared to other currencies has nearly doubled exports and increased business profits. This phenomenon leads to another economic variable: wages, which are influenced by four factors:

1) Business profits - very good

2) Labor tightness - which is as high as before the bubble burst

3) Long-term inflation - expected to remain around 2%

4) Others - differences across industries for factors 1) - 3), which vary each time.

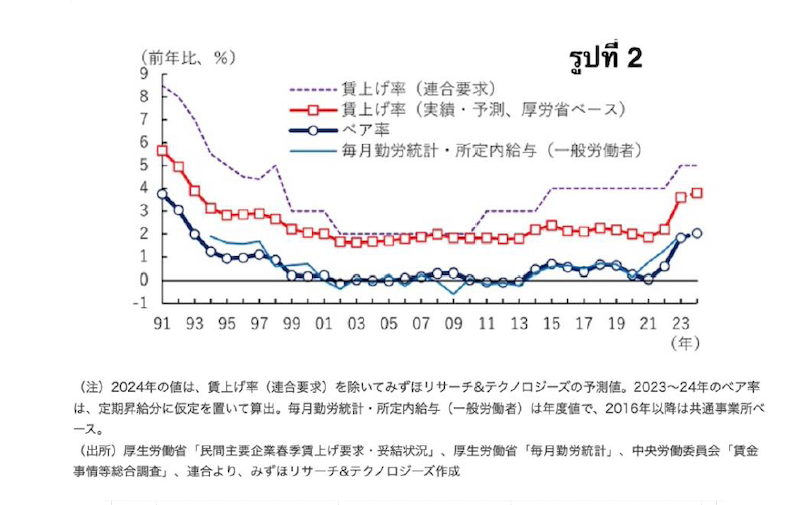

When these factors are combined, the conclusion is the wage adjustment rate shown in Figure 2. The black line represents the basic adjustment rate, which is the same across all industries, while the red line shows the average adjustment rate across all industries after considering the differences among them. This data is sourced from Mizuho RT Express, summarizing that the wage adjustment rate for 2023 is 3.8% and for 2024 is 3.4%, based on demands from labor representatives exceeding 5% for both years. It is noteworthy that the general wage adjustment rate during the period from 1999 to 2013 was nearly zero over ten years.

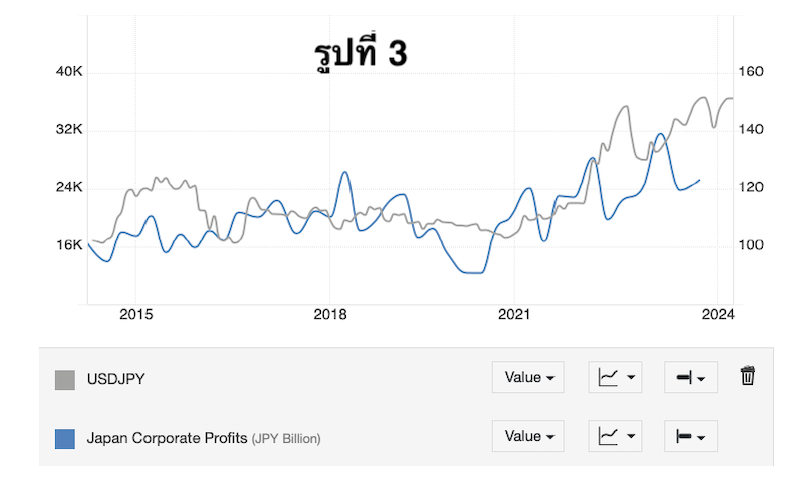

In this context, the causation direction stems from the difference in interest rates between Japan and the United States, leading to a weaker yen, improved business profits, higher inflation, and ultimately higher wage adjustments. The initial cause did not originate from monetary policy, whether through interest rates or the money supply. It should be emphasized that this time, the yen's exchange rate significantly impacted business profits, as shown in Figure 3.

While the Bank of Japan has canceled the negative policy interest rate, it has not disclosed future policies, leading to uncertainty. Speculation and guessing continue, and the policy interest rate lacks a clear direction. However, it is certain that the difference in interest rates between Japan and the United States remains relatively unchanged. The yen's exchange rate continues to be weak without significant changes, unless it follows a random pattern. Such conditions allow Japanese products to remain competitive, boosting exports, stimulating domestic investment, and increasing business profits, as reflected in various statistics.

Higher wage adjustments, increased domestic investment, and improved business profits all contribute to economic expansion. The balance of payments may improve, albeit slightly, but if the yen's value does not change significantly, the Japanese economy should reach equilibrium close to its current state.

Teikoku Databank conducted a survey of businesses of all sizes in January 2023, revealing that about 40% of businesses believe that the cancellation of Japan's negative policy interest rate will have negative effects, while around 60% think it will increase interest expenses. In reality, the latter opinion does not require a survey; it is common knowledge. However, the magnitude of the impact is a question that no one can answer. The actual impact may be minimal, and the likelihood of unclear effects on the exchange rate is low, thus not widely discussed.

Therefore, the cancellation of Japan's negative policy interest rate is unlikely to bring about significant changes beyond a slight improvement in economic burdens, maintaining the status quo until the U.S. policy interest rate is reduced around late 2024. Only then will the yen's value potentially improve. However, the benefits from a weaker yen will diminish, and Japan's economy is unlikely to expand significantly enough to push domestic inflation beyond current levels. The chances of the Bank of Japan raising the policy interest rate above the current level are therefore slim.

References:

Japan Cabinet Office Economic and Social Research Institute National Economic Accounting Division 1. Gross Domestic Product (Expenditure Side, Real: Chain Method)

Mizuho RT EXPRESS Research Department Economic Research Team Chief Economist Hiroshi Kawada “2024 Spring Labor Negotiation Wage Increase Rate Outlook”

Teikoku Databank Information Management Department “Survey on the Impact of Interest Rate Increases on Businesses” December 18, 2023

JETRO, "Balance of Payment Statistics" (Ministry of Finance, Bank of Japan) and "Foreign Exchange Rate" (Bank of Japan).