Housing Market Situation 2022-2023 by Dr. Prasart Tangmattatham

The economic situation in 2021 improved in the second half due to the reopening of domestic tourism. In 2022, the economy expanded further with the entry of foreign nationals into the kingdom, initially under control in the first half and freely in the second half. The economy received a boost in the last two months of 2022 from Thailand's hosting of APEC 2022.

Various indicators are used to assess the housing market situation. Building permit applications serve as a leading indicator, while the number of housing sales contracts is a current indicator, and property transfer data is a lagging indicator. Therefore, to evaluate the current market situation, we primarily look at sales conditions, which still have two usable variables as follows:

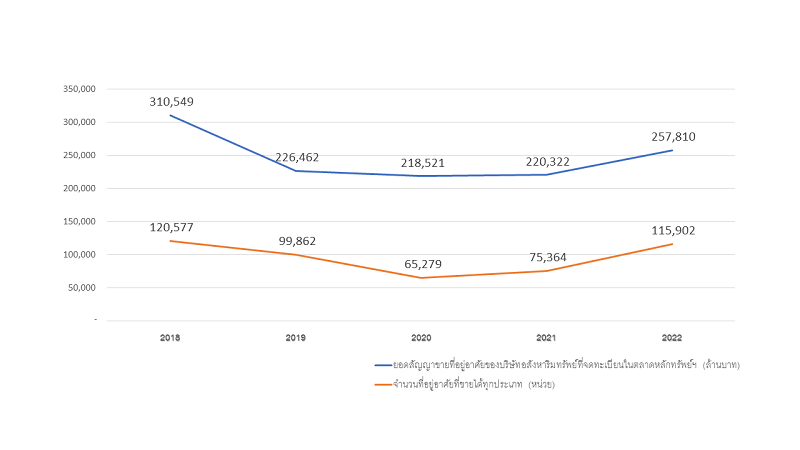

The graph shows two lines: the lower line indicates the number of sold housing units, while the upper line represents the sales volume of 10 registered real estate companies on the stock exchange. Both lines illustrate that the number of sold units and the monetary volume of contracts hit their lowest in 2020, improved in 2021, and expanded significantly in 2022. Specifically, approximately 110,000 units were sold in 2022, up from about 75,000 units in 2021. The monetary sales volume of registered companies increased from around 220 billion baht in 2021 to approximately 260 billion baht in 2022. Although both figures are based on different foundations, they clearly show a positive trend.

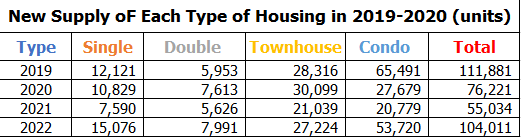

Regarding supply, new housing launched for sale in 2022 began to return to normal levels, with a total of about 100,000 units across all types. The most significant growth was seen in condominiums, increasing from about 20,000 units in 2021 to approximately 54,000 units in 2022. The supply of single-family homes also increased to around 15,000 units from the usual 10,000-12,000 units. This reflects the confidence of developers that purchasing power in the market has risen sufficiently to support normal marketing activities, similar to pre-COVID times. Detailed statistics of new housing offered for sale by type and year are presented in Table 1.

Looking back at the monetary sales figures of registered companies, it is evident that even the impact of the severe lockdown due to COVID in 2020 was relatively minor, with only about a 1% decrease from normal levels. A closer examination reveals that the primary consumer group that helped prevent a significant drop in housing sales due to COVID's impact on income consists of individuals aged 26-30, rather than the previously dominant group aged 36-40. This younger group has recently entered the workforce and has not been significantly affected by the economic downturn. Additionally, the current housing finance system facilitates home purchases with much lower monthly payments than before.

The overall economic situation relevant to the housing market includes the overall growth rate of the economy in 2023, which is expected to be at least equal to that of 2022, or around 3.4%. Positive factors likely to contribute beyond 2022 include the tourism sector and private sector investment. Private consumption continued to grow at a high rate in the third quarter of 2022 and should maintain this level in 2023. Negative factors include high oil prices, which have resulted in a negative trade balance for the foreign trade sector, unlike previous years. This factor is also related to inflation. However, housing prices have already adjusted due to material and labor costs since the fourth quarter of 2022, so the remaining impact in 2023 is expected to be minimal. Although there will be some increase in interest rates for housing loans due to the global rise in interest rates in 2023, it is anticipated to be less than half a percentage point for the first three years of repayment.

Considering all factors, overall housing demand is expected to remain at no less than 120,000 units in 2023. The supporting supply factors include the introduction of a large number of new condominium products into the market, which will drive developers to market aggressively to maintain their performance as much as possible. The younger consumer group is likely to be the target for these products. Single-family homes are another type of supply that will support the overall housing market well. In an economic environment with moderate growth but high inflation, entry-level products for older consumers who have just started working will still face challenges.