Krungsri Research Predicts BoT to Maintain Policy Rate at 0.50% Throughout the Year

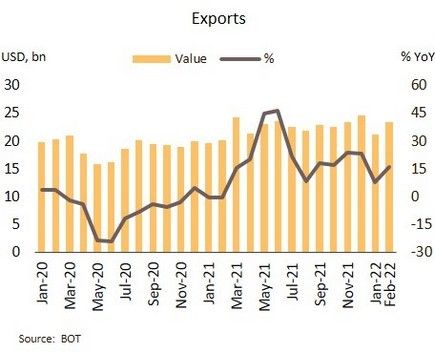

Krungsri Research indicates that the economy in February was supported by strong export growth, while domestic spending saw a slight slowdown. The value of exports returned to double-digit growth (+16% YoY) due to improved foreign demand. Additionally, the number of foreign tourists increased from January, following the reopening of the Test & Go registration system at the beginning of February.

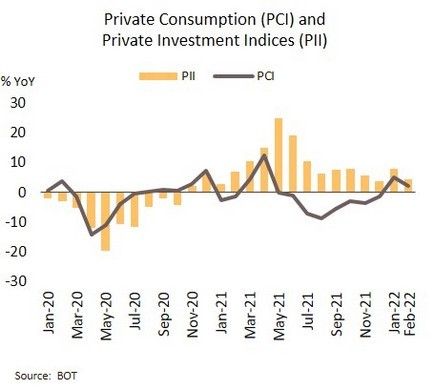

As for domestic spending, the private consumption index grew at a slower rate (+2.3% from 5.0%) due to a resurgence of COVID-19 cases in the country, along with rising energy and food prices, which dampened consumer confidence. However, government measures remain a positive factor supporting household spending. Similarly, private investment expanded at a slower pace (+4.3% from 7.8%) primarily due to a decrease in capital goods imports, while construction investment remained relatively stable.

Despite the Thai economy showing signs of recovery at the beginning of the year, there are still negative factors ahead. The high number of COVID-19 cases from the Omicron variant may pressure confidence and economic activity domestically. Externally, the ongoing conflict between Russia and Ukraine introduces uncertainty that could prolong into the second quarter, impacting the global economic recovery, particularly in Europe. This may affect (i) international trade due to decreased demand for goods and services, transportation issues, and supply chain disruptions for certain products affected by sanctions on Russia; (ii) rising energy and commodity prices, which impact production costs for businesses and the cost of living for citizens, thereby reducing household spending.

BoT has slightly revised down its economic forecast for this year but raised inflation expectations above the target range. Krungsri Research anticipates that the policy rate will remain steady at 0.50% throughout the year. In the Monetary Policy Committee (MPC) meeting on March 30, it was unanimously decided to maintain the policy rate at 0.50% to support the ongoing economic recovery. The MPC has revised its GDP growth forecast for 2022 to 3.2% from the previous 3.4% due to the impact of sanctions on Russia, which will affect the Thai economy through rising energy and commodity prices and a slowdown in demand from trading partners. The average inflation rate for this year has been revised up to 4.9% from the previous 1.7%, driven primarily by rising energy prices and cost pass-through in the food sector.

Although the average inflation rate for this year is expected to exceed the target range (1-3%), Krungsri Research still predicts that the MPC will keep the policy rate at a historic low of 0.50% until the end of the year. This is because the rising inflation is mainly due to supply-side pressures (cost-push inflation), while demand-side pressures (demand-pull inflation) remain low due to just starting income recovery. Most price increases are concentrated in energy and temporary cost pass-through in food. Medium-term inflation is expected to remain within the target range. The MPC stated, "Even though inflation is likely to exceed 5% in the second and third quarters of 2022, it will gradually decrease and return to the target range by early 2023." The MPC's statement emphasized the importance of supporting economic recovery, with the latest GDP estimate of 3.2% suggesting that economic activity levels may return to pre-COVID-19 pandemic levels by late this year or early next year.