The Piling Business Can Still Thrive Despite Covid Challenges

Analysis by KRUNGTHAI COMPASS

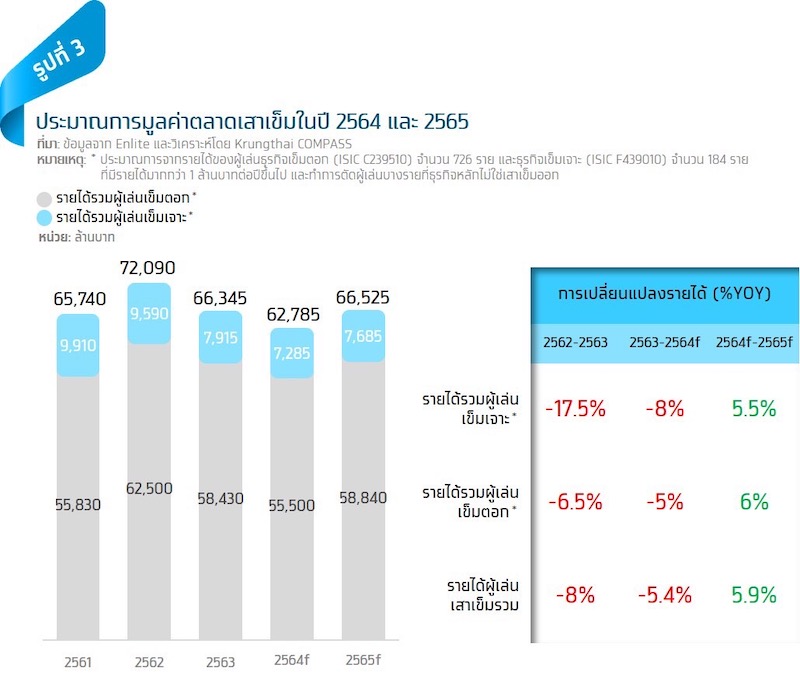

- Key Highlights: Krungthai COMPASS predicts that in 2022, the total piling market will be valued at approximately 66 billion baht, reflecting a 6% year-on-year recovery from 2021, which was the lowest level in several years. This includes: 1) the driven pile market, which is expected to grow by 6% year-on-year to about 58 billion baht, and 2) the bored pile market, which is projected to increase by 5.5% year-on-year to around 7.6 billion baht. This growth is supported by ongoing public construction and the recovery of private construction, particularly in residential projects.

- The total piling market value in 2021 is expected to decrease to about 62 billion baht, contracting by 5.4% year-on-year due to a decline in private construction and the closure of construction worker camps from June to July. This includes: 1) the driven pile market, which is expected to decrease by 5% year-on-year to about 55 billion baht, and 2) the bored pile market, which is projected to decline by 8% year-on-year to around 7.2 billion baht.

- Players should order steel materials in appropriate quantities to avoid future stock losses, as we anticipate that the average price of long steel in 2021 will rise by 25% year-on-year to about 20.4 baht per kilogram. However, the average price in 2022 is expected to decrease by 5% to 10% year-on-year to between 18.4 and 19.4 baht per kilogram. Ordering excessive amounts of steel in advance may lead to stock losses.

What is the Nature of the Piling Business?

The piling business can be divided into two types:

1) Driven pile business

2) Bored pile business

Both are driven by the construction industry, where driven pile operators sell pre-cast piles and may also provide pile driving services. Additionally, they may sell other concrete products such as utility poles and beams. Bored pile operators provide on-site casting services for piles, and some also offer related services such as diaphragm wall construction and bracing system dismantling.

The growth of the driven and bored pile market (total revenue from both types of operators) heavily depends on the value of public and private construction projects, as reflected by a high correlation coefficient of 0.75.

Generally, the driven pile business is highly competitive, while the bored pile business has moderate competition. According to the Herfindahl-Hirschman Index (HHI), the driven pile business has an HHI of around 110, indicating a highly competitive environment due to lower investment and technology requirements, leading to many operators in the same area. In contrast, the bored pile business has an HHI of about 1,765, indicating moderate competition, as it requires higher technology and investment, resulting in fewer players compared to the driven pile sector.

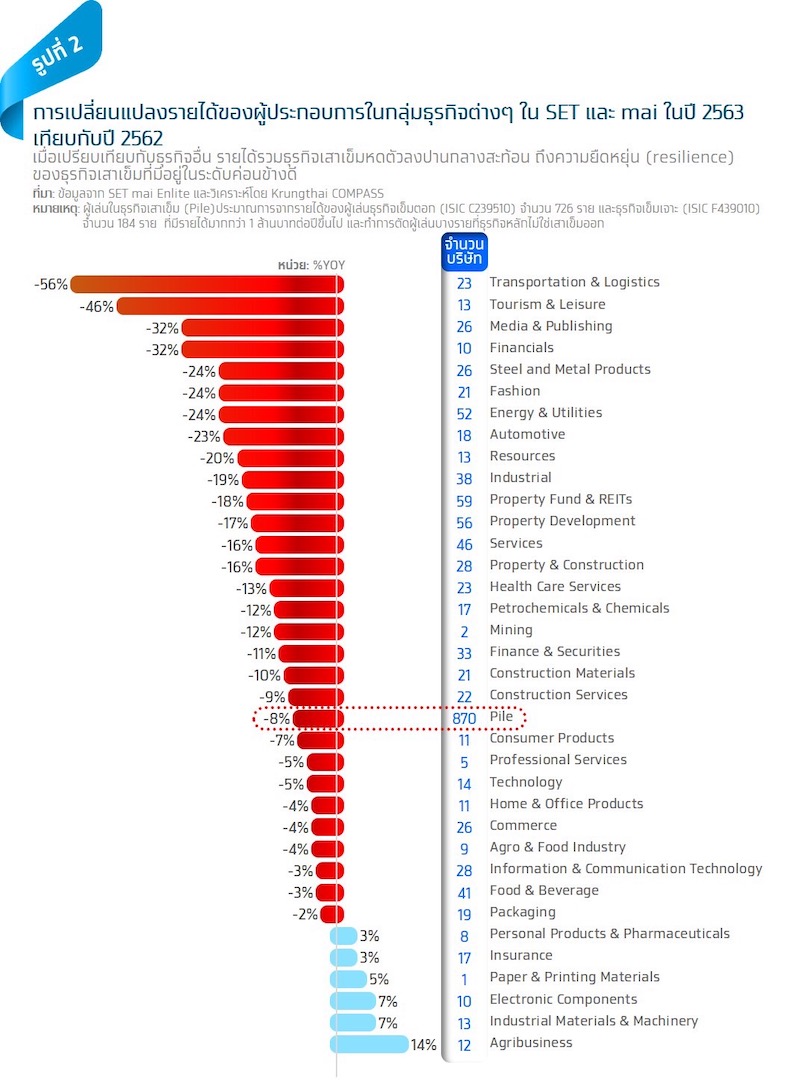

In 2020, the piling market contracted by 8% year-on-year to about 66 billion baht, which is a relatively small decline compared to other businesses facing the Covid-19 pandemic. This is because pile driving is a fundamental construction activity that still has demand and can continue to operate. Compared to other sectors, the total revenue of the piling business showed moderate contraction, reflecting a relatively good resilience in the face of economic volatility.

The contracting piling market in 2020 saw driven pile operators' revenue decrease by 6.5% year-on-year to about 58 billion baht, while bored pile operators' revenue fell by 17.5% year-on-year to around 7.9 billion baht. When considering the revenue of operators with earnings over 1 million baht, we found that driven pile operators experienced an average revenue contraction of only 6.5% year-on-year, while bored pile operators faced an average decline of 17.5% year-on-year. This is due to the nature of driven pile projects being primarily public and residential construction, such as single-family homes and townhouses, which could still proceed. In contrast, the significant drop in bored pile revenue was due to a slowdown in large-scale building projects that primarily use bored piles, such as condominiums and mixed-use buildings. Additionally, the backlog of work for both types of operators helped prevent revenue from falling further.

What is the outlook for the piling business in 2021-2022, and what are the driving factors?

Krungthai COMPASS expects that in 2021, the piling market will contract again by 5.4% year-on-year to about 62 billion baht, which would be the lowest point in several years due to a decrease in private construction. However, it will still receive support from ongoing public construction, preventing a deeper contraction. The closure of construction worker camps from June to July also hindered pile operators' ability to operate. This includes: 1) the driven pile market, which is expected to decrease by 5% year-on-year to about 55 billion baht, and 2) the bored pile market, which is projected to decline by 8% year-on-year to around 7.2 billion baht.

In 2022, we estimate that the total piling market will likely increase by 5.9% year-on-year to about 66 billion baht, driven by ongoing public projects from 2021 and the recovery of private construction, particularly in residential projects. This includes:

1) the driven pile market, which is expected to grow by 6% year-on-year to about 58 billion baht.

2) the bored pile market, which is projected to increase by 5.5% year-on-year to around 7.6 billion baht.

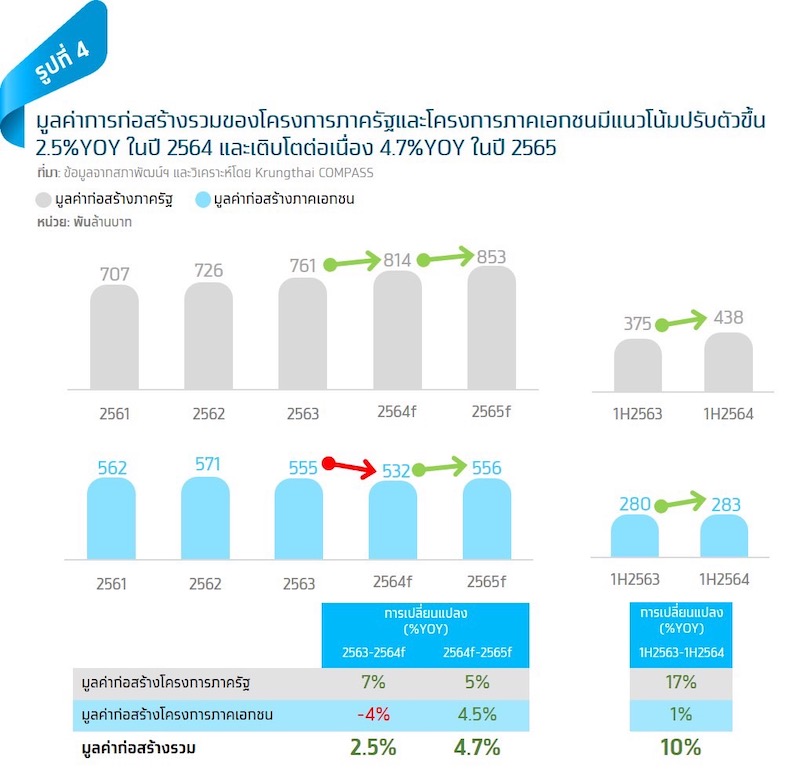

The pile market is expected to contract in 2021 due to a decrease in the value of private construction projects, but it will still receive support from the growth of public construction projects, which is expected to grow by about 7% year-on-year to 814 billion baht in 2021. In the first half of 2021, the value of public construction projects continued to grow by 17% year-on-year, reflecting the ability to conduct business despite the Covid-19 pandemic, along with a low base in the first half of 2020. Given this situation, we anticipate that the value of public construction projects in 2021 will continue to grow from the previous year, which will support the demand for piles and prevent a significant contraction.

In 2022, the value of public construction is expected to continue growing by about 5% year-on-year to 853 billion baht, alongside the recovery of private construction values, which will help improve the piling business.

The growth of public construction project values in both 2021 and 2022 is driven by two main components: 1) General public construction projects and 2) Mega transportation projects.

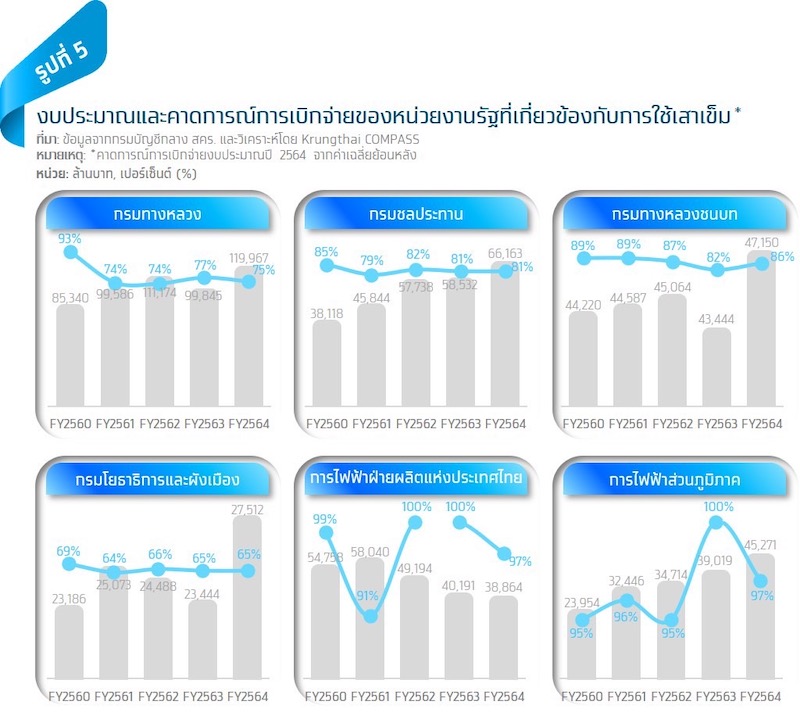

1) General public construction projects in the 2021 fiscal year saw key agencies related to construction receive higher investment budgets than in 2020. These projects include those related to transportation, such as roads, bridges, and general infrastructure related to water, such as dams and weirs. The investment budget in 2021 for four state agencies involved in these projects increased, including the Department of Highways, which rose by 20% year-on-year to about 120 billion baht, the Department of Rural Roads, which increased by 13% year-on-year to 66 billion baht, and the Department of Water Resources, which increased by 9% year-on-year to about 47 billion baht. We also estimate that in 2021, these agencies will likely disburse over 75% of their allocated budgets, which, combined with the higher budget and good disbursement rates, will positively impact the revenues of pile operators.

In the 2022 fiscal year, all four agencies received slightly reduced investment budgets but still at high levels. Agencies with increased budgets include the Department of Water Resources, which rose by 6% year-on-year to about 70 billion baht, and the Department of Public Works and Town & Country Planning, which increased by 9% year-on-year to about 29 billion baht. Meanwhile, transportation agencies saw reductions, with the Department of Highways decreasing by 8% year-on-year to about 110 billion baht and the Department of Rural Roads decreasing by 5% year-on-year to about 44 billion baht. Thus, in the 2022 fiscal year, the budgets of the four agencies slightly decreased by about 2.5% year-on-year to 255 billion baht, but still remained higher than the total investment budget in 2020 of 225 billion baht and in 2019 of 238 billion baht.

Additionally, this includes electrical system projects, such as utility poles, which are similar products to driven piles, where state enterprises like the Electricity Generating Authority of Thailand and the Provincial Electricity Authority continue to receive investment budgets.

2) Mega transportation projects are expected to commence construction in 2021 and 2022, such as the high-speed rail project connecting Bangkok and Nakhon Ratchasima (with a civil work value of 180 billion baht), which has mostly signed construction contracts, and the high-speed rail connecting three airports (120 billion baht). There are also projects currently in the bidding process, such as the dual-track railway from Den Chai to Chiang Rai and Chiang Khong (73 billion baht), the dual-track railway from Ban Phai to Mukdahan and Nakhon Phanom (55 billion baht), and the Purple Line extension from Tao Pun to Rat Burana (78 billion baht). These construction projects will create continuous demand for both driven and bored piles in 2021 and 2022, depending on the design characteristics of the construction projects.

However, the value of private construction projects in 2021 is still expected to contract by 4% year-on-year to 532 billion baht, but is anticipated to recover by 4.5% year-on-year to 556 billion baht in 2022, which will positively impact both driven and bored pile operators. In the first half of 2021, the value of private construction showed a slight increase of 1% year-on-year to 283 billion baht, reflecting ongoing private project construction. However, we found that this increase was primarily due to other private construction projects, not the main private construction sectors, including residential and non-residential construction.

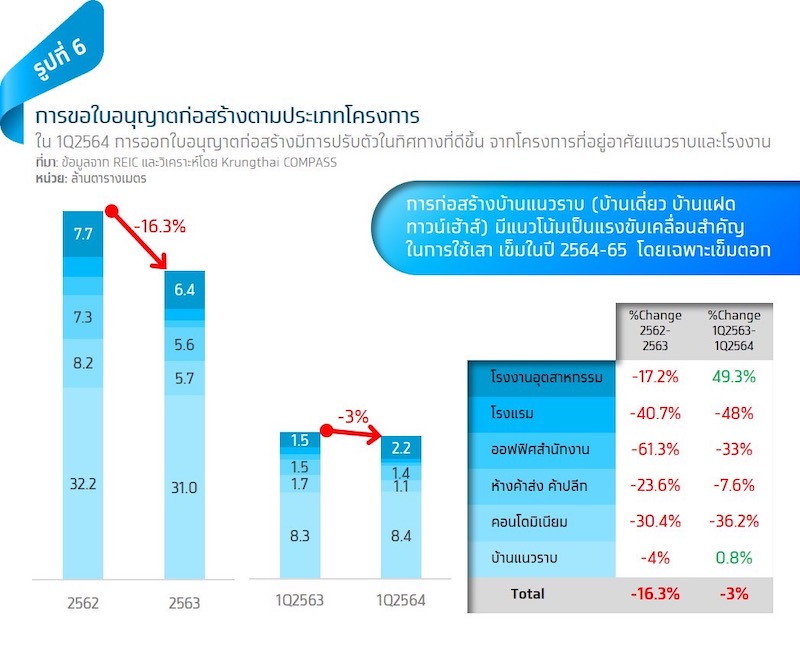

Although the issuance of construction permits for private projects decreased by 16.3% year-on-year in 2020 to 51.8 million square meters, in the first quarter of 2021, we began to see signs of improvement in construction permits, particularly for horizontal residential projects and factories. The issuance of construction permits for horizontal residential projects, which include single-family homes, duplexes, and townhouses, increased by about 1% year-on-year to about 8.4 million square meters. Notably, three regions saw continuous increases in the issuance of construction permits for horizontal residential projects in 2020 and the first quarter of 2021: the northeastern region increased by 9.7% year-on-year in 2020 and 11% year-on-year in the first quarter of 2021, the southern region increased by 5.7% year-on-year in 2020 and 2% year-on-year in the first quarter of 2021, and the western region increased by 8% year-on-year in 2020 and 14% year-on-year in the first quarter of 2021.

In the first quarter of 2021, the issuance of industrial factory construction permits significantly increased (over 150% year-on-year) in the eastern region, including Rayong, Chachoengsao, and Sa Kaeo. The construction of both residential and factory projects will positively impact the piling business, especially driven piles, which can be used for both residential and industrial construction.

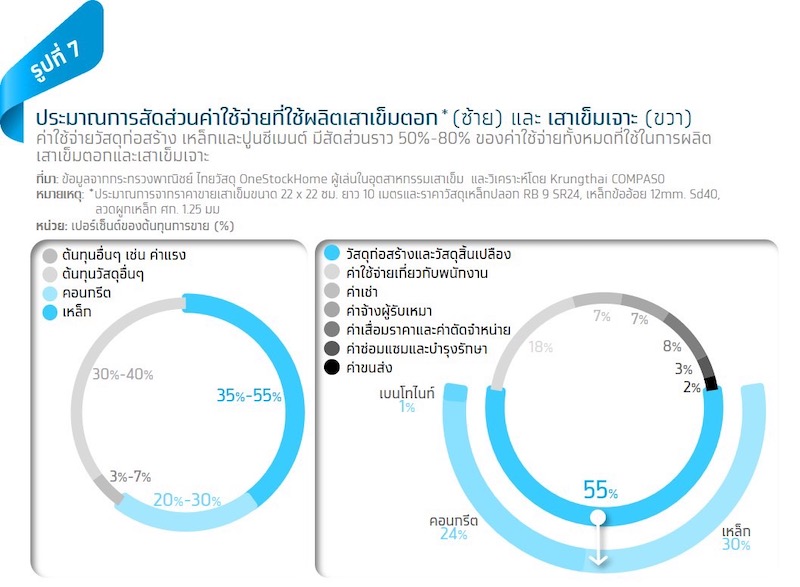

In the bored pile sector, construction material costs account for about 55% of total costs, with steel making up approximately 30%, concrete about 24%, and bentonite (a stabilizing agent for boreholes) around 1% of the total production costs for bored piles. Labor costs account for about 18% of the total production costs for bored piles.

The issuance of construction permits for these private projects serves as a leading indicator for the value of private construction and the demand for piles in the next 1-3 years, in line with the lifespan of construction permits. Additionally, as the government begins to relax Covid-19 control measures, it will help boost private sector confidence in undertaking new real estate projects, including new residential developments.

From our analysis, we found that if the price of long steel increases by 1%, it will result in a cost increase of about 0.3%-0.5% for pile operators, and if the price of cement rises by 1%, it will lead to a cost increase of about 0.2%-0.3%. This will pressure the gross margin down. Therefore, controlling the prices and supply of construction materials is a crucial issue that operators should closely monitor.

It is expected that the average price of long steel in Thailand in 2021 will rise by 25% year-on-year to about 20.4 baht per kilogram, which will increase costs for pile operators by about 7.5%-12.5%. The price of steel has been on the rise since late 2020, as demand for steel in China increased following the easing of the Covid-19 outbreak, coupled with production controls to reduce pollution in China and the cancellation of the 13% export tax rebate since May. This has led to a reduction in steel supply from China and an increase in steel prices there.

However, steel prices are expected to decrease in the remaining months of the year due to falling iron ore prices, which began to decline in August 2021 to around 150-160 USD per ton, nearing levels seen in January 2021. This will directly affect the prices of steel products in China, as Thailand imports about one-third of its steel consumption from China.

For 2022, we believe that the average steel price in Thailand will decrease by about 5% to 10% year-on-year, falling to between 18.4 and 19.4 baht per kilogram, which will positively impact the costs for pile operators. This is a result of the anticipated continued decline in average iron ore prices, as well as the rebalancing of supply and demand for steel products in China, where steel producers have adjusted their production to match steel demand, leading to a downward trend in Thai steel prices. This situation will likely improve the gross margins for pile operators.

However, the impact of construction material prices on the gross margins of operators still depends on several factors, such as purchasing construction materials in advance to lock in prices, which can help reduce volatility and material costs, and negotiating price adjustments for piles with project owners.

2) The Covid-19 pandemic may affect operators in various ways, such as delays in working hours and the transportation of piles, raw materials, equipment, and tools due to lockdowns, reduced labor supply due to infections, foreign workers unable to return to the country after returning home during the outbreak in the second quarter of 2020, the closure of worker camps, and the need for operators to maintain cleanliness and hygiene at job sites, camps, and vehicles, as well as closely and regularly monitoring these areas.

3) The disbursement of the annual investment budget for 2022 by the four main agencies related to construction is a key issue that operators should monitor, as it directly affects revenues from public construction work. Additionally, the recovery of the economy from the Covid-19 pandemic is a factor that will instill confidence in the Thai private sector to invest in residential and commercial real estate construction, as well as attract foreign investors to invest in Thailand, which will lead to future industrial factory construction.

Implications:

• Pile operators should adapt to take on more residential and public construction projects, especially in the northeastern, southern, and western regions where construction permits have been continuously increasing in both 2020 and the first quarter of 2021, as well as in the eastern region, which saw an increase in construction permits in the first quarter of 2021. Public construction projects are also likely to continue if there is no severe Covid-19 outbreak, as reflected in the high investment budgets of the four agencies related to construction and ongoing bidding for mega projects.

• Pile operators should be prepared to handle fluctuations in construction material prices, especially steel, which is expected to remain high in 2021 compared to average prices in 2020. Operators should consider entering into forward contracts to reduce price volatility for steel, which is a significant cost, and may need to diversify their sources of steel to mitigate supply chain disruptions in case of a severe resurgence of Covid-19 that prevents suppliers from producing and delivering on time. However, operators should order steel in line with actual demand, as average steel prices in 2022 are expected to decrease, and over-ordering may lead to stock losses.

• The government should consider appropriate measures to control the spread of Covid-19 to allow the piling business and other sectors in the construction industry to continue operations. The construction industry is one that can still operate despite the Covid-19 pandemic and is a vital sector that can help sustain the country's economy through this crisis. Therefore, the government should implement Covid-19 control measures that are suitable for businesses, such as restricting operations only at job sites and camps with infected workers or those at risk of infection, along with other easing measures, such as extending the time for transporting piles and other construction materials. Finally, the government should expedite vaccine distribution for personnel in the construction business, especially workers.