Exploring the Thai Data Center Market: A Mega Trend Worth Watching

Analysis by SCB EIC

- The COVID-19 pandemic has been a significant catalyst for businesses to adopt technology more extensively, with the data center business being one of the beneficiaries, supported by:

1. Changing consumer behavior towards a new normal, leading to increased reliance on online platforms for daily activities, resulting in a higher demand for data.

2. Digital transformation, or the integration of technology into business operations at the organizational level, which is expanding rapidly. 3. Government agencies are likely to push for the development of a central cloud infrastructure project, supporting Thailand's goal to become a digital hub in ASEAN. - EIC estimates that the value of Thailand's data center market is projected to grow at a 20% CAGR from 2020 to 2022, reaching approximately 32 billion baht, primarily driven by the growth of public cloud services. It is expected that from 2020 to 2022, public cloud will expand at a high rate of 24% CAGR, reaching 26 billion baht, as users can save on IT equipment investment and have more flexibility in scaling usage compared to colocation or private cloud, which is expected to grow at 6% CAGR to 6 billion baht during the same period.

- However, the relatively high initial investment and competition from international players pose significant challenges for Thai operators. Therefore, operators should adapt to maintain growth rates and improve profitability in the future, such as:

1) Implementing modular data centers,

2) Focusing on public cloud services,

3) Collaborating with related businesses to create synergy in service delivery.

Continuously growing data centers are increasingly being designed and developed into modular data centers, as this format can save costs, time, and provide flexibility for expansion. Data centers, which are responsible for receiving, storing, processing, and transmitting data, consist of three key components: 1) Site infrastructure capital, which includes the building where various systems are installed, such as electrical and air conditioning systems. Currently, investments in constructing data center buildings are shifting from traditional structures that complete foundational systems before installing servers and equipment to modular data centers (MDC), which are like ready-made subunits that can operate independently. As demand increases, additional modules can be added, reducing construction delays and excessive initial investments, allowing for rapid expansion. 2) IT capital, which includes processing and data storage equipment such as storage devices, large processors, operating systems, racks, and internet connectivity devices. 3) Human capital, responsible for managing and overseeing systems in accordance with international standards set by institutions such as the Uptime Institute, Telecommunications Industry Association (TIA), Building Industry Consulting Services International (BICSI), and International Organization for Standardization (ISO), as well as personnel coordinating with clients and stakeholders.

In addition to building data centers for internal use, leasing services have created diverse business models for data center providers, offering options for businesses that need data center services. Leasing services are divided into two types: 1) private cloud or colocation services, and 2) public cloud services. The provision of private cloud (colocation) and public cloud services differs in the scope of services provided by data center providers. In the case of private cloud (colocation), the provider supplies the space for basic equipment placement, such as racks and connectivity cables, while the user invests in IT assets like servers and operating systems. Users pay monthly rental fees for the space used. In contrast, for public cloud services, the provider prepares all space and equipment, including IT assets, with users paying for services either through a subscription model or based on actual usage, allowing for flexibility in scaling usage as needed.

Public cloud services can be further divided into three subcategories based on the level of service provided:

- Infrastructure as a Service (IaaS) refers to IT infrastructure services that support data storage and computer networking on the cloud, with service fees calculated based on actual usage (pay per use). Examples of providers include Azure IaaS services, AWS EC2, Google Compute Engine, Rackspace, and INET.

- Platform as a Service (PaaS) refers to platform services for developing applications or software that operate on the cloud, with providers supplying necessary components for application or software development, such as web servers, databases, and development runtimes, with fees based on actual usage (pay per use). Examples include AWS Elastic Beanstalk, Windows Azure, Google App Engine, Oracle Cloud, IBM Cloud, and Alibaba Cloud.

- Software as a Service (SaaS) refers to software services available on the cloud, with fees typically structured as monthly or annual subscriptions. Examples include Office365, Google Docs, Salesforce, Docusign, and Zoom applications.

However, when using public cloud services, users may have concerns about data security due to shared storage devices with other organizations, leading many organizations to increasingly adopt hybrid cloud services, which combine private and public clouds. Hybrid clouds offer advantages in terms of lower initial investment compared to private clouds and can alleviate data security concerns, allowing users to store sensitive data on private clouds while keeping general data on public clouds.

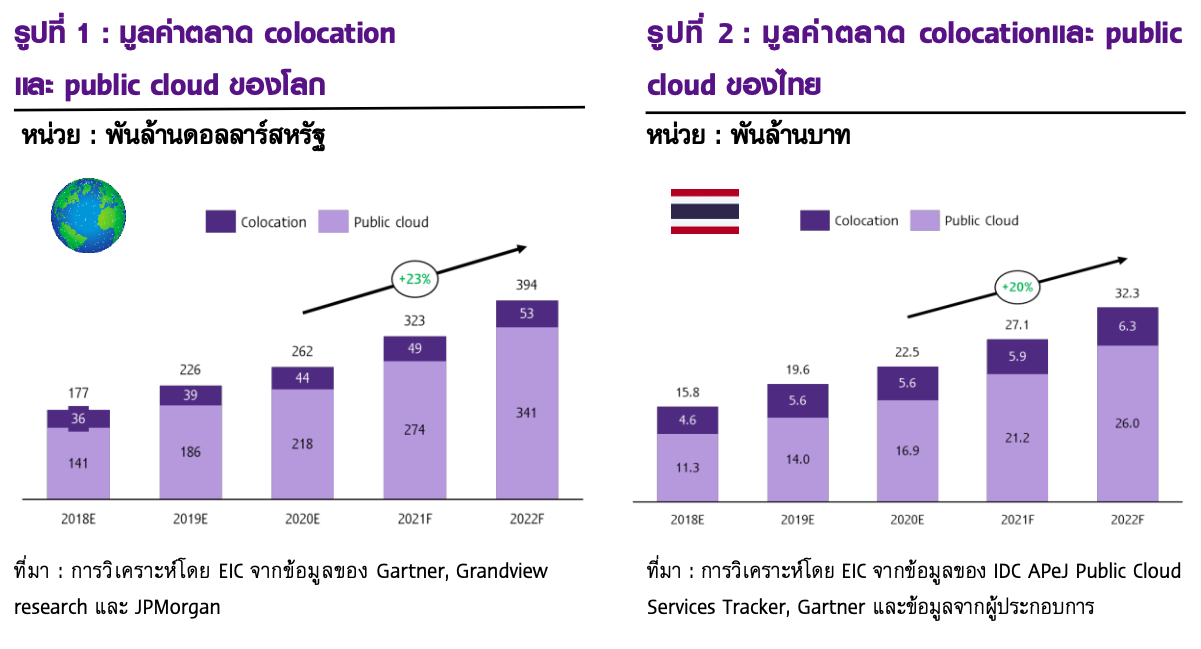

The global data center service market is expected to continue growing at approximately 23% CAGR from 2020 to 2022, driven by the rapidly expanding public cloud market, which effectively meets the needs of enterprise operations under the new normal. The total value of the data center market in 2022 is projected to be around $390 billion (approximately 12 trillion baht). Historically, the data center service market has seen an average growth rate of 22% CAGR from 2018 to 2020, supported by the continuous increase in data usage driven by advancements in digital technology and the rising accessibility of smartphones and high-speed internet among consumers. This growth rate is expected to accelerate due to the COVID-19 pandemic, which has significantly prompted organizations to adopt cloud technology for business operations. This trend is anticipated to continue in the future, as cloud technology can help organizations reduce IT costs and facilitate employee work from anywhere at any time through various software applications, such as customer relationship management (CRM) software, teleconferencing software, online document management, and e-signature solutions, based on data compiled from leading research institutions studying data center business trends.

Internationally, EIC estimates that the colocation market will grow at a slower rate than the overall data center market, projected to grow at around 8% CAGR to reach $52 billion from 2020 to 2022, due to some customer pressure to switch to public cloud services as part of organizational adjustments to reduce operational costs. Meanwhile, the public cloud market is expected to grow significantly at 25% CAGR, reaching $340 billion in 2022.

The value of Thailand's data center service market is expected to grow at a slower rate than the global market, with projections indicating a 20% CAGR increase from 2020 to 2022, reaching approximately 32 billion baht. This marks an acceleration from the average growth rate of about 19% CAGR from 2018 to 2020. The colocation market is expected to grow at around 6% CAGR, reaching 6.3 billion baht in 2022, a growth rate lower than the global market (8% CAGR), due to Thailand's economic conditions in 2021-2022, which are expected to recover more slowly than the global economy due to the impacts of a new wave of COVID-19. This has led some businesses to delay IT asset investments or shift towards using public cloud services due to lower initial investment costs. Meanwhile, Thailand's public cloud market is expected to grow close to the global market (25% CAGR), projected to expand at around 24% CAGR, reaching 26 billion baht in 2022, driven by increased adoption of cloud technology within organizations.

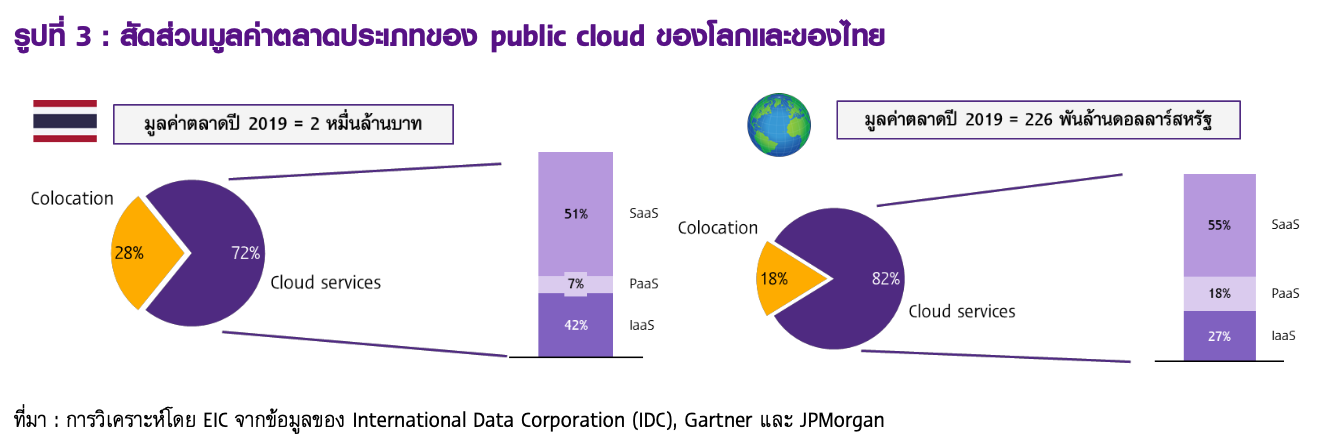

Additionally, considering the market value of data centers in 2019, the value of the public cloud market was at 72%, which is still lower than the global market share of around 80%, indicating significant opportunities for the expansion of Thailand's public cloud market in the future. This aligns with the market trend, where the growth rate of public cloud is expected to surpass that of colocation. Notably, over 93% of public cloud service offerings are IaaS and SaaS, while the market value of PaaS accounts for only 7%. EIC anticipates that two main groups of Thai providers, namely IaaS providers (mostly the same as colocation providers) and SaaS providers (mostly startups developing cloud-based software), will be crucial drivers for the future of Thailand's data center and cloud business. Although the PaaS market is expected to grow alongside the public cloud market, most providers in Thailand are still large foreign technology companies such as Amazon, Google, Microsoft, and Alibaba.

The growth of both colocation and public cloud is supported by three factors stemming from the demand for data from consumers, businesses, and government agencies:

1) Consumer sector: Data usage is expected to continue growing alongside the expansion of Cloud Gaming, Over-the-top platforms (OTT), social media, and e-commerce. This growth reflects the changing consumer behavior towards increased reliance on online platforms for daily activities, as evidenced by the average mobile data usage in Thailand, which has grown at an average of 38% CAGR (1H2019-1H2021) to 20.3 GB per number per month in the first half of 2021. Similarly, the number of fixed broadband internet users in Thailand grew by approximately 14% year-on-year, reaching 11 million in 2020.

2) Business sector: The COVID-19 pandemic has accelerated businesses' adoption of technology for operations (digital transformation), including technologies like Artificial Intelligence (AI), Big Data analytics, automation systems, and cloud computing. This will significantly increase data usage among businesses. The Digital Economy Promotion Agency (DEPA) estimates that the market value of big data analytics in Thailand is expected to grow at 12% CAGR (2020-2022), reaching approximately 19 billion baht in 2022. Additionally, foreign research forecasts indicate that the global market value of SaaS Customer Relationship Management (CRM) and Enterprise Resource Planning (ERP) operating on the cloud is expected to grow at average rates of 14% CAGR and 17% CAGR, respectively, from 2021 to 2025.

3) Government agencies: The government has projects to develop a central cloud infrastructure for public data (Government Data Center and Cloud Service: GDCC) to support the digital storage of public data and promote Thailand as a digital hub in ASEAN by providing tax incentives (BOI) to data center providers.

While the data center business shows promising growth, there are still significant challenges to watch out for, including high initial investment costs and competition from international players. The nature of the business requires substantial infrastructure investment to support server and equipment operations, resulting in high initial investments and fixed costs due to the need for construction, systems work, racks, maintenance staff, and servers for customer service. According to accounting systems, it takes time to amortize all expenses, impacting the profitability of providers in the early stages of business operations, as occupancy rates are still relatively low. Additionally, increasing competition from foreign providers is another factor to monitor, potentially leading to market share competition through diverse service strategies that meet varying customer needs, trust in user experience and recognized expertise, and price competition due to the larger budgets of major companies. Notable foreign providers planning to expand into Thailand include STT-GDC in partnership with Fraser Group, Huawei, NTT, Supernap, Tencent Cloud, and KT Corporation.

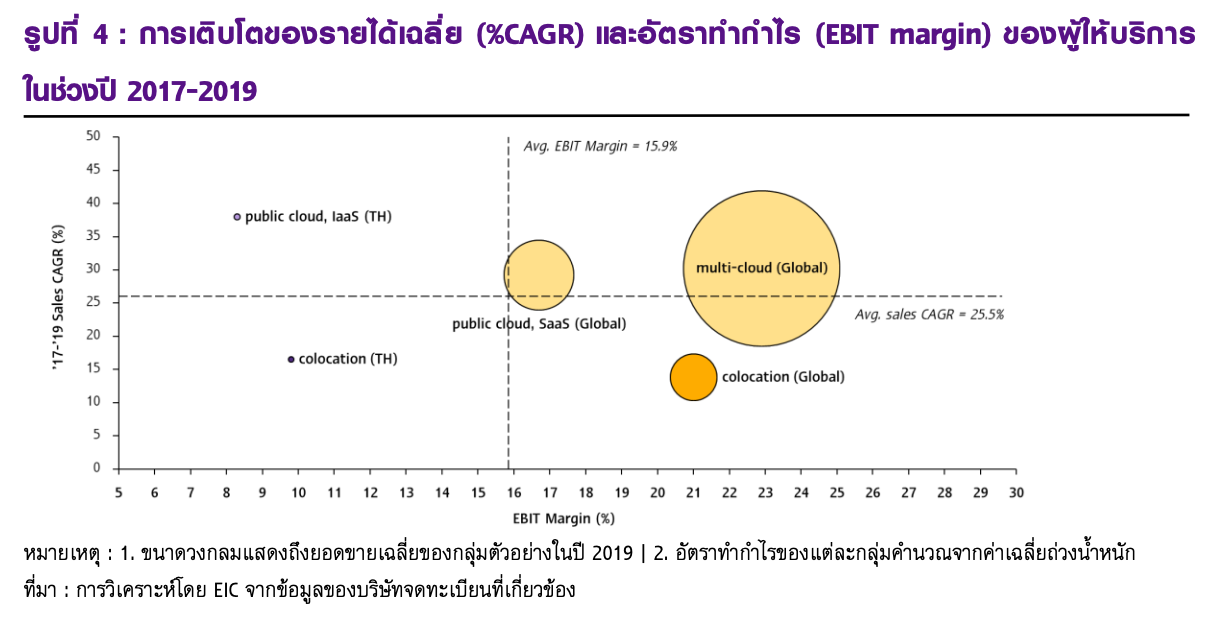

Regarding the performance of Thai data center providers over the past three years (2017-2019), there has been continuous growth. However, compared to global providers, the profit margins of Thai providers remain lower. A study of a sample of 20 data center providers (both Thai and foreign) found that from 2017 to 2019, the average revenue growth of the group was 25% CAGR, indicating strong business expansion. Thai colocation providers had an average revenue growth of 16% CAGR, similar to foreign providers at around 14% CAGR, while the revenue of Thai public cloud providers grew at an average rate of about 38% CAGR, outperforming foreign SaaS and multi-cloud providers (covering IaaS, PaaS, and SaaS) at around 29% CAGR and 30% CAGR, respectively, due to the smaller revenue base of Thailand's cloud market. Furthermore, in the past 3-4 years, digital technology has played an increasingly significant role in Thailand. Additionally, the revenue of both Thai and foreign public cloud providers has grown better than colocation, aligning with overall market conditions. However, when considering profit margins (EBIT margin), it is found that on average, Thai providers have lower profit margins than foreign providers, with Thai colocation providers having a profit margin of around 10%, lower than the 22% profit margin of foreign providers. Similarly, Thai public cloud providers have a profit margin of 8%, lower than the 17% and 23% profit margins of foreign SaaS and multi-cloud providers, respectively, due to economies of scale, where global players have advantages in higher revenue bases, allowing for better cost management under a high fixed cost structure.

In the future, EIC expects that the revenue and profit margins of Thai providers will gradually improve as the market expands and economies of scale improve from a larger revenue base. This is especially true for public cloud providers, where the market is experiencing high growth, while colocation providers may face pressure from some users switching to public cloud services, resulting in lower growth rates. Increased competition from foreign providers will be a key factor to monitor in the medium term.

EIC presents three adaptation strategies for operators to prepare for the anticipated increase in competition in the future:

1. Implementing modular data centers will help reduce initial investment costs and improve cost management due to the flexibility in expanding service areas.

2. Increasing focus on public cloud services to cater to the growing public cloud market in the future. Additionally, public cloud services have better profit margins per rack than colocation.

3. Business collaborations to enhance options and create synergy in service delivery, such as partnering with System Integrators (SI) that offer cyber security solutions, which will increase customer confidence in using public cloud services, as well as collaborating with foreign providers to offer platform as a service (PaaS), where currently there are few Thai operators providing such services.

The growth of the data center business also benefits other businesses in the supply chain, with EIC identifying:

1) IT equipment manufacturers

2) Construction contractors

3) Connectivity service providers as three groups significantly benefiting from this growth.

1. IT equipment manufacturers benefit directly from the production and distribution of IT equipment, which is a core component of data centers, such as hard disks, switches, routers, and cables. Gartner, a leading global technology research firm, estimates that global spending on data center systems and equipment will grow by about 8% year-on-year in 2021, reaching approximately $237 billion.

2. Construction contractors benefit from the increased demand for data center construction alongside market growth. The construction and installation of mechanical & electrical (M&E) systems for data centers are more complex than for general buildings and require specialized expertise in design and construction to ensure data centers operate efficiently according to standards. As a result, data center construction contractors have higher profit margins than general contractors, with studies showing that data center contractors have an average EBIT margin of around 20%, compared to 5%-10% for general contractors.

3. System integrators act as intermediaries connecting IT equipment and software manufacturers with users through various roles, including IT equipment distribution, software installation, consulting, and system management, to ensure data center and cloud computing operations effectively meet user needs. EIC anticipates that system integrators, often collaborating with foreign IT companies such as CISCO, Oracle, IBM, and Salesforce, will significantly benefit from the growth of the data center business, especially among providers of cloud service solutions and cyber security, which are experiencing high growth alongside the expansion of public cloud usage in organizations.

In summary, the data center business is another future-oriented industry worth watching, with a strong growth trajectory driven by increasing data usage from three sectors: consumers, businesses, and government agencies, which positively impacts providers in terms of revenue growth and improved profit margins. However, challenges related to high initial investment costs and competition from foreign companies necessitate that operators adapt to these factors moving forward.

Analysis by >>> https://www.scbeic.com/th/detail/product/7756

Author: Olan Ueawithayasuporn ([email protected])

Analyst

Economic Intelligence Center (EIC)

Siam Commercial Bank Public Company Limited

EIC Online: www.scbeic.com

Line: @scbeic