EIC Assesses Higher Chances of Policy Rate Cut This Year After MPC Votes to Maintain Rate Unanimously

• The MPC voted 4 to 2 to maintain the policy rate at 0.50% per annum. Although the MPC assessed that the economy has been more adversely affected by COVID-19 than previously estimated, reflected in the downward revision of this year's economic growth forecast to 0.7% and 3.7% for next year (down from 1.8% and 3.9% respectively), the majority of the committee still believes that monetary measures will be more effective than reducing the already low interest rate. Meanwhile, two members suggested a 0.25% cut in the policy rate to support the economy and address increasing economic risks.

• The MPC assessed that liquidity in the financial system remains high, but its distribution is not widespread due to increasing credit risks, particularly for SMEs and households. Additionally, the Thai economy will face significantly increased downside risks, which will impact private consumption, income, and employment.

• EIC predicts that the MPC will maintain the policy rate at 0.5% throughout 2021 and 2022, assuming that the economy follows the latest baseline scenario where the outbreak is controlled by early Q4 this year. The MPC is likely to keep the interest rate unchanged to preserve policy space and focus on adjusting monetary measures to distribute liquidity more effectively. However, the likelihood of a single rate cut this year has increased (30% probability) due to the downside risks from the Delta variant outbreak, coupled with slow vaccination rates, which may lead to prolonged outbreaks and control measures, further impacting recovery and economic scars. This could prompt the MPC to decide to cut the rate by another 0.25% this year to provide additional economic support. Key factors to monitor include outbreak control, vaccination progress, and the adequacy of fiscal measures.

• Overall, EIC believes that further cuts in the policy rate may help reduce debt burdens but will have a limited economic stimulus effect given that interest rates are already very low and the economy is primarily affected by reduced income from lockdown measures and concerns over the outbreak. Therefore, accelerating vaccination to control the outbreak, fiscal measures to compensate for lost income, and adjusting monetary measures to distribute liquidity more broadly will be more effective.

• EIC anticipates that the government will consider adjusting existing monetary measures and may introduce additional measures to accelerate liquidity distribution and reduce the debt burden of those affected by the outbreak, as communicated by the MPC. In terms of rehabilitation loan measures and debt suspension measures, adjustments to conditions and reductions in various restrictions may be seen, especially in terms of reducing credit risk and lowering financial costs for SMEs affected by the outbreak to support their access to credit, which, although improving, is still not sufficiently widespread.

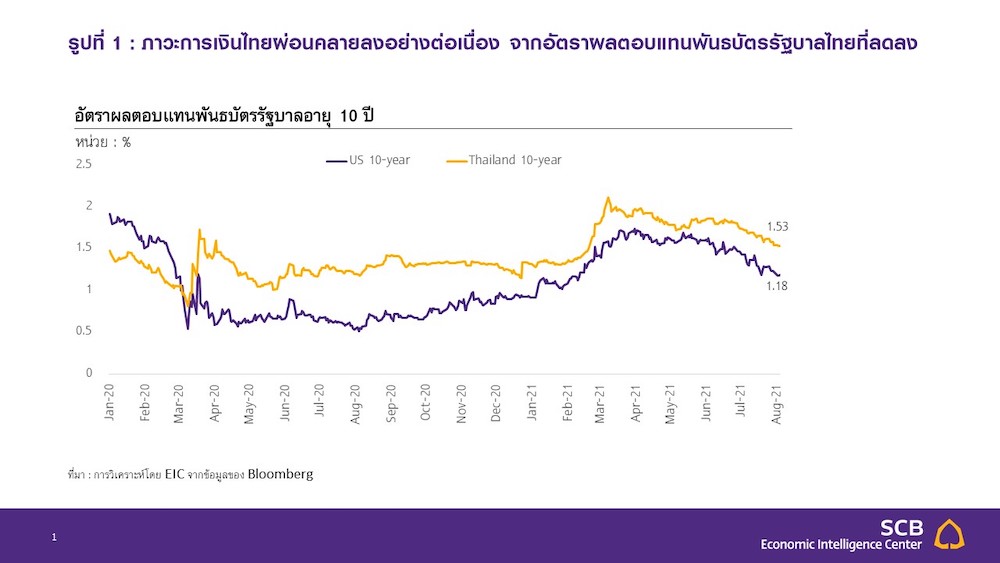

• In the financial market, the Thai financial condition continues to ease, as evidenced by the decline in Thai government bond yields over the past month. This follows the decrease in US government bond yields, while the Thai baht has depreciated more than other currencies in the region due to concerns about the outbreak situation and the ongoing current account deficit.

The MPC revised down its economic forecast for Thailand due to greater-than-expected outbreak impacts, but voted 4 to 2 to maintain the policy rate at 0.50% per annum. The majority of the committee believes that monetary measures are more effective than interest rate cuts, while two votes suggested a 0.25% cut in the policy rate for additional economic support. The committee assessed that the Thai economy in 2021 has been more adversely affected by the COVID-19 outbreak than previously estimated and still faces significant downside risks. The most critical challenge for the Thai economy is to accelerate outbreak control and vaccine distribution to restore public confidence and enable economic activities and income to expand again. Meanwhile, fiscal and monetary measures must urgently assist those affected more precisely and timely. The committee believes that economic risks remain high.

Assistance must be accelerated through liquidity distribution and reducing the debt burden of affected groups, with the majority of committee members believing that monetary measures will be more effective than the current low interest rate. Therefore, they recommend maintaining the policy rate, while two members suggest reducing the interest rate as a supplementary measure to support the economy and address the high-risk economic outlook ahead.

• The Thai economy is projected to grow by 0.7% and 3.7% in 2021 and 2022, revised down due to the prolonged and more severe impacts of COVID-19 than previously estimated, as well as significant impacts on private consumption this year and a substantial decrease in foreign tourist trends next year due to delayed reopening policies and reduced foreign tourist confidence. The Bank of Thailand has revised down its foreign tourist forecast to 150,000 in 2021 and 6 million in 2022 (from 700,000 and 10 million respectively).

• The labor market has become increasingly fragile due to the third wave of outbreaks, especially in the service sector and among self-employed individuals. It was found that in Q2 of this year, the number of virtual unemployed increased for the first time in a year, with more workers returning to their hometowns and a rise in long-term unemployment. Furthermore, the recovery of private sector employment outside agriculture has a W-shaped pattern, where severe and prolonged outbreaks will delay recovery further. However, the Thai economy still has additional support from increased government spending trends from the latest borrowing decree and strong export growth, although some manufacturing sectors have been affected by outbreaks in factories and temporary raw material shortages.

• General inflation rates are expected to remain close to previous levels. Medium-term inflation forecasts remain anchored within target ranges.

• Nevertheless, the Thai economy still faces significant downside risks from outbreaks both domestically and internationally, which are likely to worsen, impacting private consumption, income, and employment, in addition to the effects on the number of foreign tourists, which the committee will closely monitor.

The MPC assessed that liquidity in the financial system remains high, but its distribution is not widespread due to increasing credit risks, particularly for SMEs and households affected by the outbreak. The rehabilitation loan measures introduced have helped SMEs access credit more effectively. Regarding exchange rates, the baht has depreciated against the US dollar more than regional currencies due to domestic factors.

The MPC stated that government measures and policy coordination are crucial for economic recovery, with public health measures needing to accelerate the procurement and distribution of effective vaccines to prevent prolonged outbreaks. Fiscal measures should urgently support and sustain the economy by adequately addressing the labor market and vulnerable business sectors in a timely manner. Monetary policy must continue to support overall financial conditions, while financial and credit measures should be improved for greater effectiveness by rapidly distributing liquidity to affected parties and reducing debt burdens, such as rehabilitation loan measures, debt suspension measures, and other measures from specialized financial institutions, alongside pushing financial institutions to improve debt restructuring to achieve broader results aligned with borrowers' long-term repayment capabilities.

The MPC continues to prioritize supporting economic recovery within the framework of monetary policy aimed at maintaining price stability while ensuring sustainable and full economic growth and financial system stability, and will monitor key factors affecting economic trends, including vaccine distribution and effectiveness, outbreak situations both domestically and internationally, and the adequacy of fiscal and monetary measures. They are prepared to use appropriate monetary policy tools if necessary.

EIC expects that the Bank of Thailand will maintain the policy rate at 0.5% throughout 2021 and 2022, but the chances of a single rate cut this year have also increased. EIC assesses that under the baseline scenario, the MPC is likely to keep the policy rate at a historic low until the end of 2022, as the latest economic forecast from the MPC still assumes that the outbreak situation may improve and lockdown measures can be eased in early Q4 this year, which would reduce the necessity for a rate cut this year. Additionally, the majority of committee members believe that the benefits of reducing the policy rate in the current situation will be limited, as the main issue is the distribution of liquidity to SMEs and households rather than financial cost issues. Furthermore, the MPC must weigh the side effects of reducing the interest rate closer to zero, such as 1) further reduced interest rates may lead some groups reliant on interest income, such as the elderly, to save more and reduce spending, 2) policy space will further diminish and be insufficient to support cases where the economy worsens, and 3) significant rate cuts may lead to increased debt accumulation, making future rate hikes more difficult, potentially leading to long-term financial system stability risks from excessively high debt levels, search for yield behavior, and underpricing of risk.

However, the significant downside risks to the economy, particularly the outbreak that may last longer than expected, will make the chances of a single rate cut this year reasonably likely (around 30%), due to the Delta variant outbreak, which has a much higher transmission rate than previous strains. Especially in a situation where vaccination rates remain low, the current lockdown measures may not be effective enough to control the outbreak by early Q4 as per the baseline scenario. If downside risks materialize, whether through a more severe and prolonged outbreak than expected, the impact of lockdown measures on private consumption and investment being more severe than estimated, or government support measures being less effective than anticipated, the majority of the committee may need to resort to policy measures through

additional rate cuts to support the economy by reducing interest debt burdens and supporting debt restructuring for households and SMEs. This would also help ease financial conditions and reduce the interest payment burden on the government from rising public debt in the future. In addition to considering rate cuts, the MPC may consider extending the duration of the reduced contribution rate to the FIDF fund, which was implemented last year, and may also consider further reducing the contribution rate.

The Bank of Thailand will consider adjusting existing monetary measures and may introduce additional measures to accelerate liquidity distribution to affected groups from the outbreak to be more widespread and sufficient, as communicated by the MPC. Overall, although the Bank of Thailand has collaborated with relevant agencies to adjust monetary measures to assist SMEs more effectively, including rehabilitation loan measures and debt suspension measures, the progress of these projects has been slow and not sufficiently widespread. As of July 27, 2021, 27,219 beneficiaries have received assistance through rehabilitation loan measures, accounting for only 3.5% of the total registered SMEs in the country, which number around 770,000. Additionally, the approved loans through the program amount to only 82 billion baht out of a total budget of 250 billion baht, making it highly likely that new loans in the SME sector will continue to contract this year. For the debt suspension project, participation has also been low, with only 18 beneficiaries, reflecting that the conditions of the measures and regulations from relevant agencies may still pose obstacles to business participation in the projects. This presents a significant challenge for the government to urgently consider adjusting conditions and reducing obstacles to enhance the effectiveness of liquidity distribution. For the SME loan project, the government may need to consider mechanisms that involve greater participation and reduce credit risks, such as lowering credit insurance fees, increasing the proportion of compensation for loan portfolio losses, or declaring government risk acceptance in the form of loan guarantees at sufficiently high ratios. This is to support liquidity distribution to SMEs severely affected by the COVID-19 crisis. In terms of the financial market, the Thai financial condition continues to ease, as evidenced by the decline in Thai government bond yields over the past month, following the decrease in US government bond yields and domestic risk factors. Currently, the yield on 10-year Thai government bonds stands at 1.53%, down 21 bps since early July, while the yield on 10-year US government bonds is at 1.18%, down 28 bps during the same period.

The yield on US government bonds has continuously decreased in July 2021, which contrasts with US economic data, including non-farm payroll figures and inflation rates that have been rising steadily. The decline in US government bond yields is attributed to three main factors:

1) Concerns about the economic impact of the Delta variant outbreak of COVID-19, as the daily new COVID-19 cases in the US and the number of hospitalizations have rapidly increased in the past week, primarily among unvaccinated groups. The resurgence of COVID-19 has led investors to worry about the uncertainty of the economic situation in the near future, prompting them to avoid risky assets and buy safer assets more.

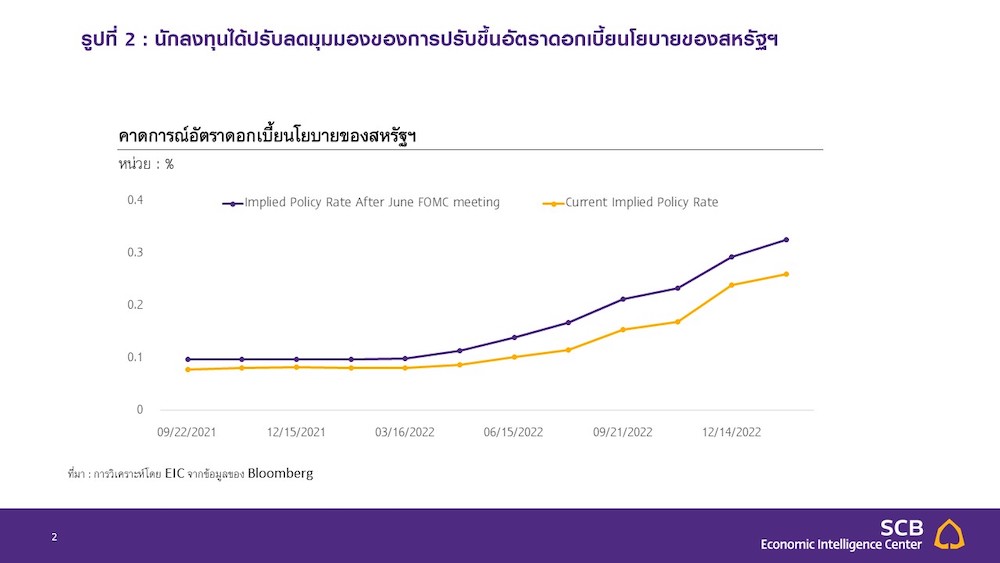

2) A reduction in market outlook regarding the likelihood of a tightening monetary policy in the US, with the latest forecast for the US policy rate being lower than the predictions made in June. This reflects a reduction in investors' outlook on the chances of a rate hike. Additionally, investors have lowered their medium-term inflation forecasts, viewing the rising inflation as a temporary factor, which differs from the perspective in the first quarter, where investors believed inflation would remain high due to large-scale economic stimulus measures and rapid vaccine distribution in the US.

3) Supply-side constraints that are likely to be more severe and prolonged than expected pose significant risks to global economic growth, including the US economy in the near future. Delays in production and low inventory levels have resulted in longer delivery times and increased price pressures, with many factories worldwide having to temporarily shut down production lines. Moreover, the US labor market has not yet recovered to pre-COVID-19 crisis levels, even as unemployment benefits measures begin to expire in some states.

The yield on Thai government bonds has decreased in line with the decline in US government bond yields and domestic risk factors. The outbreak of the virus in the country and the implementation of stricter outbreak control measures have worsened the outlook for the Thai economy, leading to lower investor confidence and additional pressure on Thai government bond yields.

Figure 1: Thai financial conditions continue to ease as evidenced by declining Thai government bond yields.

Source: Analysis by EIC from Bloomberg data

Figure 2: Investors have revised down their outlook on the likelihood of US policy rate hikes.

Source: Analysis by EIC from Bloomberg data.

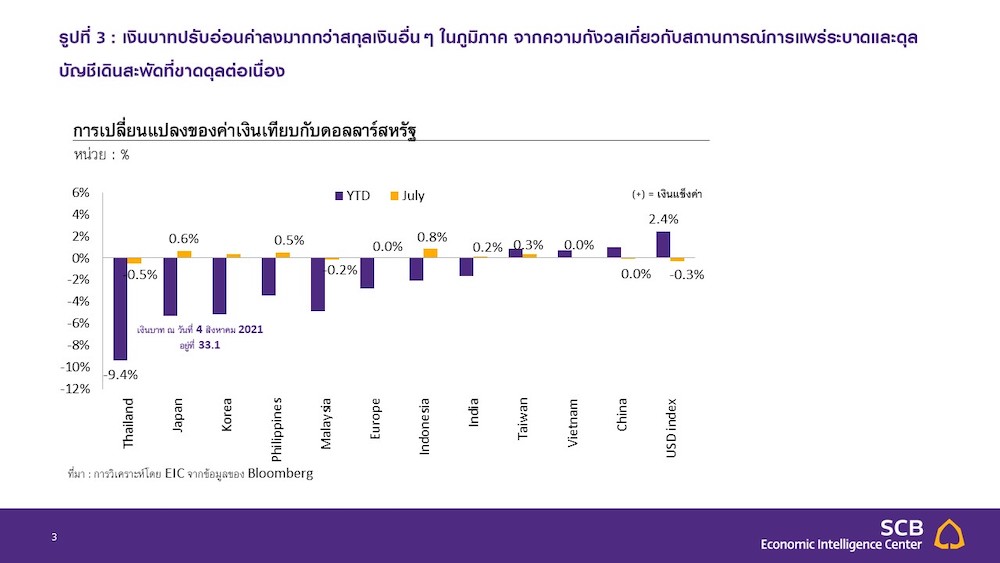

The baht has depreciated more than other currencies in the region due to concerns about the outbreak situation and the ongoing current account deficit. Currently, the baht is at 33.1 baht per US dollar, depreciating by 9.4% since the beginning of the year, which is a greater depreciation than that of other regional currencies. (Figure 3) In the short term, the baht is likely to remain weak due to

1. The prolonged and intensified Delta variant outbreak of COVID-19, which has affected investor confidence, leading to capital outflows from Thailand in July, both in the bond and equity markets. Concerns about outbreaks in several countries have prompted investors to buy more US dollars, resulting in the dollar appreciating against other currencies.

2. Thailand's ongoing current account deficit, with a deficit of 164 billion baht in Q2 of this year, the lowest level since 2013. This deficit has arisen from service deficits due to increased shipping costs, while Thailand's trade balance remains in surplus. Additionally, the stagnation of tourism has reduced the demand for holding baht, leading to a rapid depreciation of the baht.

However, if the outbreak situation improves as expected in Q4 this year, it will be a factor that helps the baht appreciate slightly towards the end of the year. If the increased shipping costs from previous supply chain disruptions ease in the remaining part of the year, it will reduce Thailand's service deficit. Furthermore, if the government can control the outbreak situation and investor confidence increases, it will boost the demand for baht, leading to a potential appreciation. EIC expects the baht to be in the range of 32.5-33 baht per US dollar.

Figure 3: The baht has depreciated more than other currencies in the region due to concerns about the outbreak situation and ongoing current account deficits.

Source: Analysis by EIC from Bloomberg data.

Analysis by SCB EIC >>> https://www.scbeic.com/th/detail/product/7720

Authors of the analysis:

Wachirawat Banchuen ([email protected]) Senior Economist

Nichanan Logewitool ([email protected]) Analyst

Economic Intelligence Center (EIC)

Siam Commercial Bank Public Company Limited

EIC Online: www.scbeic.com