Examining the Housing Market: Challenges of Recovery Post-COVID-19

The COVID-19 pandemic has exacerbated an already weak housing market, which was affected by LTV measures in 2019, leading to a continuous contraction in 2020. This is reflected in two main areas: 1) A significant drop in demand due to reduced purchasing power and consumer confidence, resulting in lower sales and transfers; 2) A decrease in supply as developers postponed the launch of new projects, particularly condominiums, and shifted focus to developing more horizontal projects while also concentrating on clearing high stock levels.

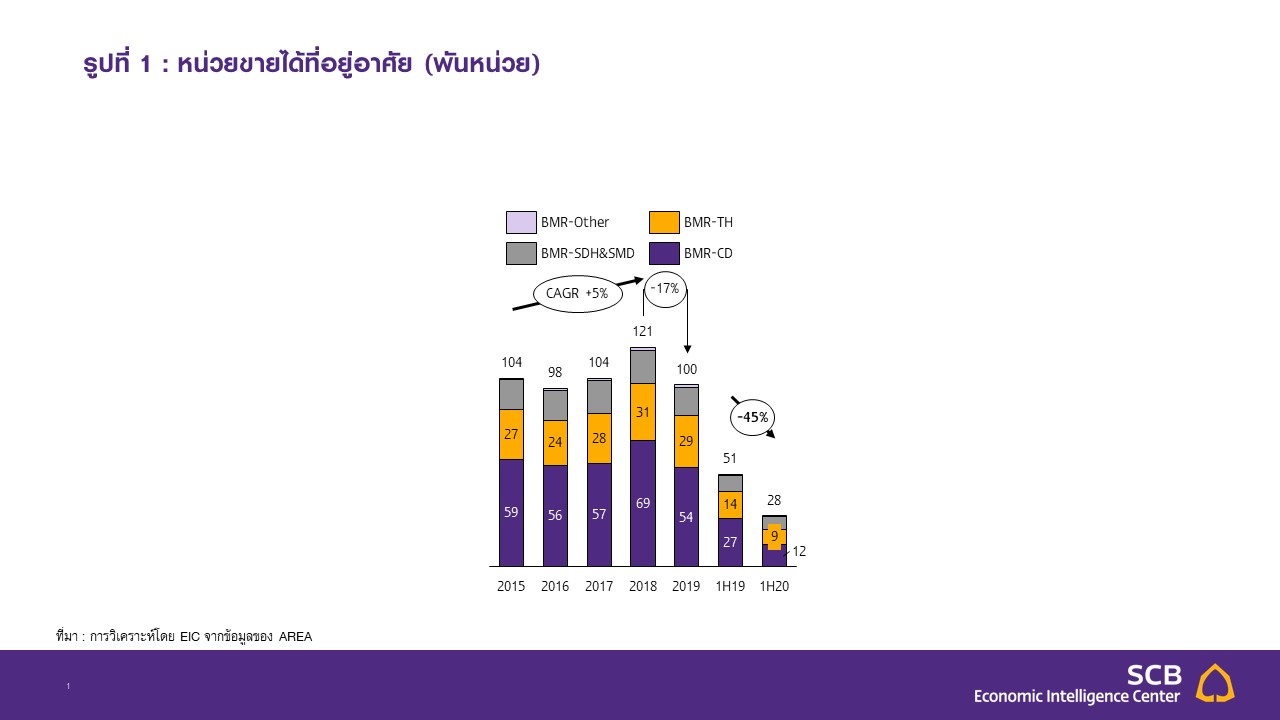

The COVID-19 outbreak further diminished housing sales in 2020, following the impacts of the LTV measures in 2019. Analyzing the housing market over the past period reveals a continuous stagnation due to a contracting economy and weakened foreign purchasing power, compounded by the LTV measures that came into effect in April 2019, which caused housing sales units in Bangkok and its vicinity to shrink by -17% YoY in 2019 and continued to decline in 2020. The COVID-19 pandemic intensified this contraction, as evidenced by AREA data showing a -45% YoY decrease in sales units in the first half of 2020 (Figure 1), driven by reduced purchasing power and the impact of lockdown measures that led consumers to delay outdoor activities. Additionally, foreign sales halted due to international travel restrictions and a slowing global economy. The significant drop in sales was also a result of the postponement of new project launches, with the sales rate in the first month of new projects consistently falling below the average of the past three years for both condominiums and horizontal projects, averaging 26% for condominiums, 13% for townhouses, and 8% for single and twin houses in the first half of 2020.

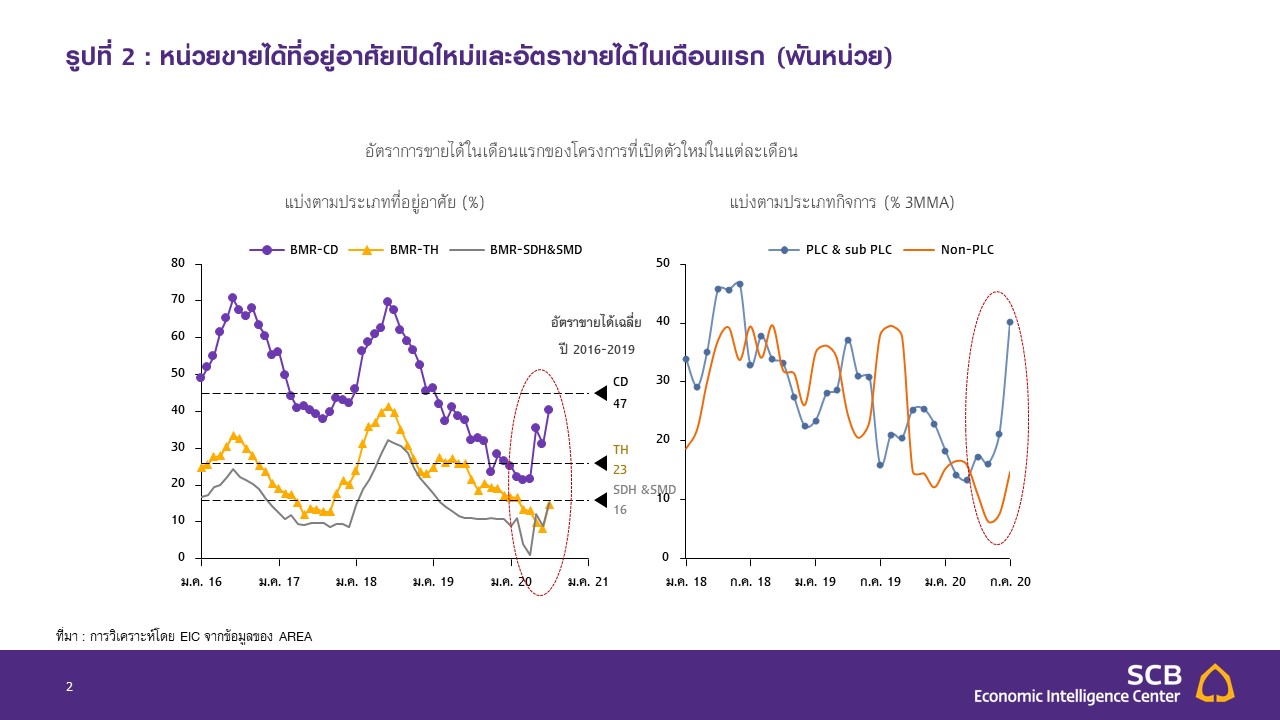

When comparing the first-month sales rates of newly launched projects in the first half of 2020 between listed companies and non-listed companies, it was found that listed companies had a higher average sales rate of 17% compared to 12% for non-listed companies (Figure 2). This was due to increased sales from both horizontal and condominium projects, as larger companies focused on penetrating the horizontal market while also working to clear condominium stock through various promotions, including enhanced online marketing efforts. The reputation of established brands contributed to improved sales, as reflected in the financial reports of some listed companies in the second quarter.

Figure 1: Housing Sales Units (thousands)

Source: Analysis by EIC from AREA data

Figure 2: Newly Launched Housing Units and First-Month Sales Rates (thousands)

Source: Analysis by EIC from AREA data

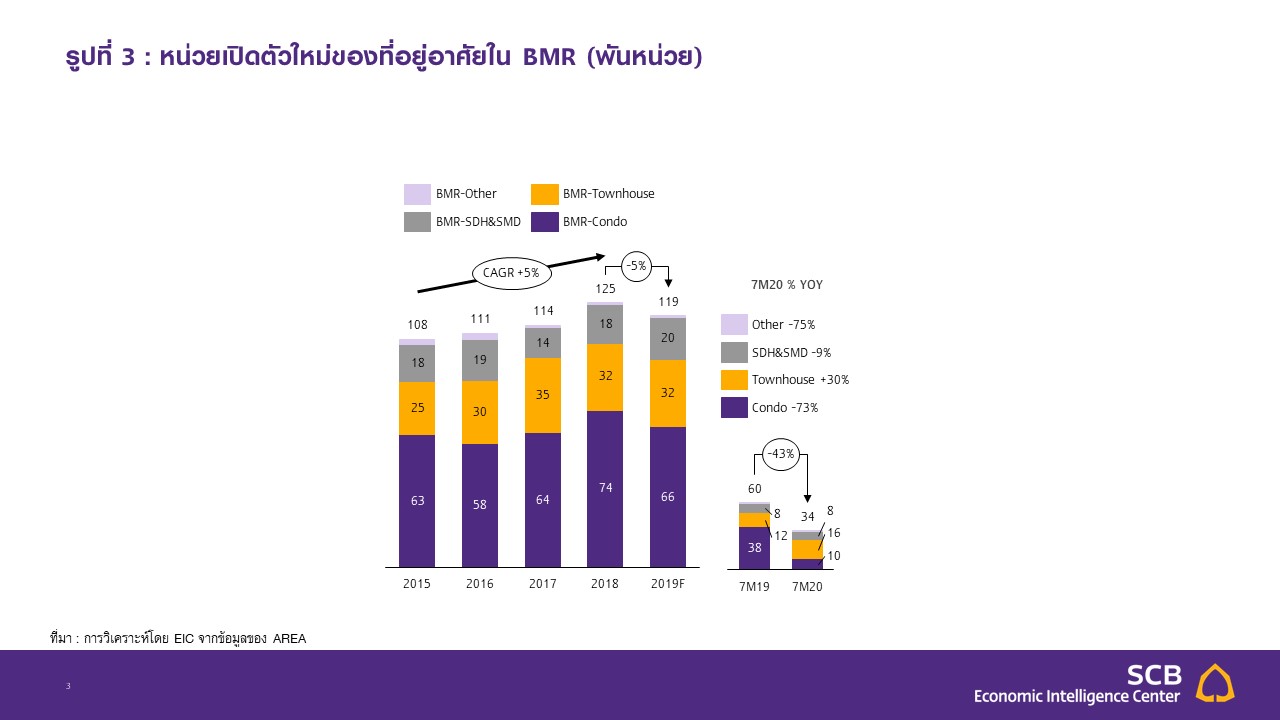

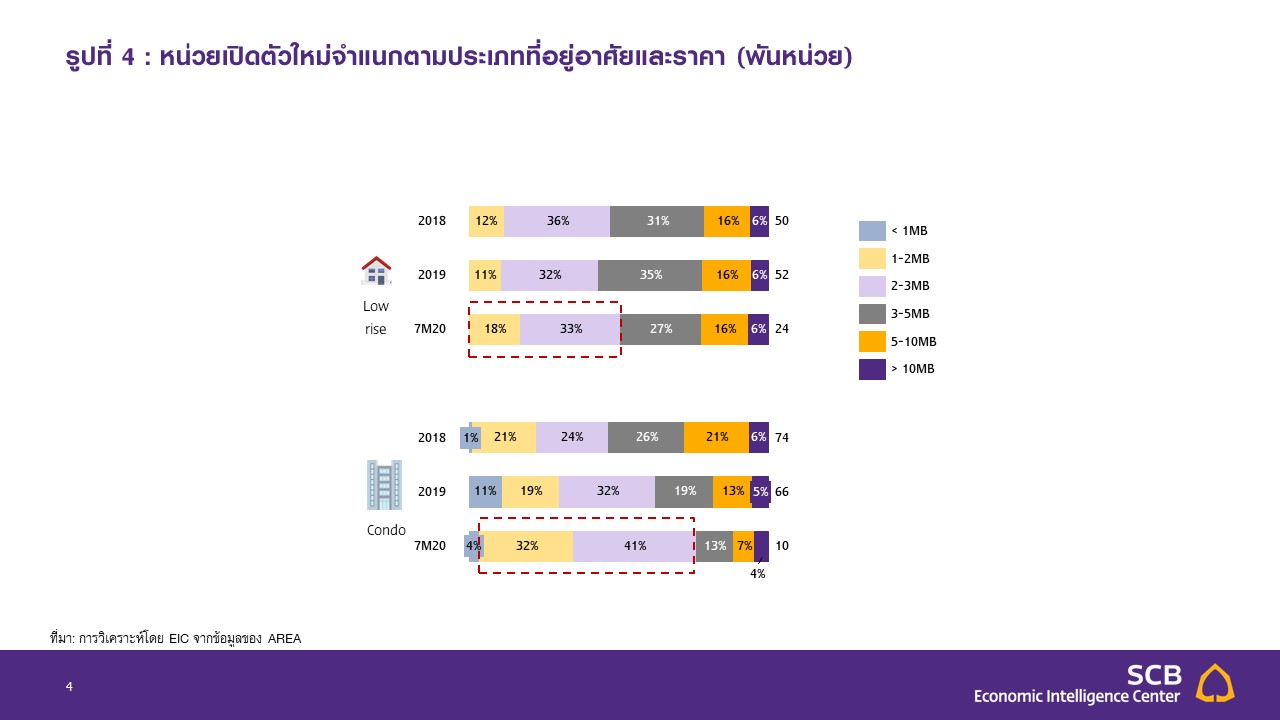

The ongoing decline in market conditions has led developers to delay the launch of new projects, particularly condominiums, while increasingly focusing on horizontal projects, especially townhouses, which have seen an uptick in launches. The sluggish market conditions in 2019 resulted in a continuous increase in unsold units, prompting developers to exercise greater caution in launching new projects. The COVID-19 pandemic has heightened this caution, as reflected in the postponement of new project launches, particularly in the first half of the year, which was impacted by lockdown measures. Consequently, the number of newly launched housing units in the first seven months of 2020 decreased by -43% YoY to 34,390 units (Figure 3), primarily due to a reduction in condominium projects, which still have a high level of unsold inventory. Developers have shifted focus to horizontal projects, targeting the real demand market by launching more affordable projects. If we look at new launches by price level and type of housing, it is evident that developers are increasingly focusing on horizontal projects, particularly townhouses, as reflected in the growing proportion of new units priced between 2-3 million baht (Figure 4). Furthermore, most new units are located along the subway lines, such as the blue, green, and yellow lines, and in areas surrounding Bangkok.

Figure 3: New Housing Launches in BMR (thousands)

Source: Analysis by EIC from AREA data

Figure 4: New Launches by Housing Type and Price (thousands)

Source: Analysis by EIC from AREA data

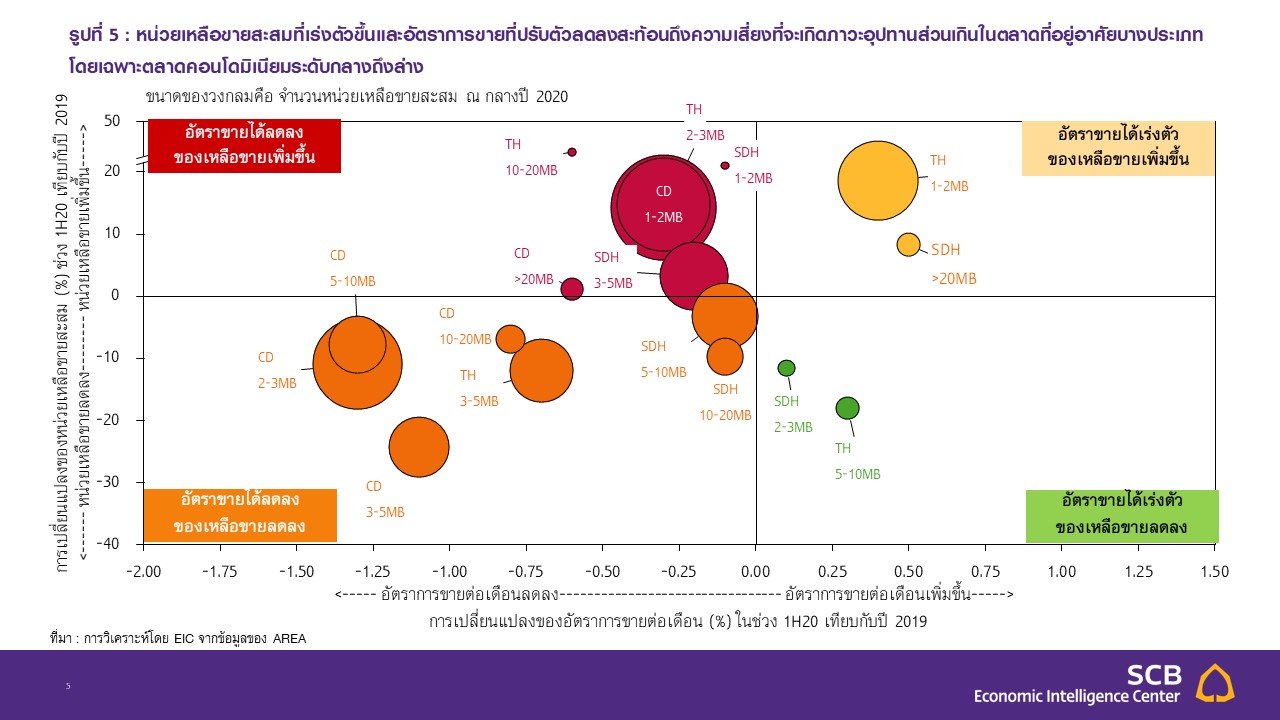

The issue of excess supply remains a concern, particularly for condominiums, where developers must focus on clearing stock, leading to intensified price competition, especially as condominium prices are expected to decline. Although developers have adjusted by significantly delaying new project launches, the level of unsold inventory remains relatively high, with unsold housing units in Bangkok and its vicinity at 221,000 units as of mid-2020, with over 41% being condominiums. Additionally, when examining unsold units by price level, it is found that the majority are priced below 3 million baht, with unsold condominium units priced below 3 million baht remaining high at around 63,000 units, accounting for about 70% of total unsold condominium units. Even though most developers postponed new project launches in the first half of 2020, leading to a decrease in unsold inventory for certain housing types, such as condominiums priced above 2 million baht, the monthly sales rate continues to trend downward, reflecting the market's risk of excess supply due to sales rates remaining lower than the decline in new launches. Furthermore, as developers increasingly focus on horizontal projects, the unsold inventory of some horizontal projects, such as townhouses priced between 2-3 million baht, is also accelerating (Figure 5). Therefore, it is essential to monitor the excess supply situation, particularly for housing priced below 3 million baht, which is expected to be significantly impacted by the economic slowdown, as it primarily targets the middle to lower-income segment that is anticipated to recover slowly from the effects of COVID-19.

Figure 5: Accelerating Unsold Inventory and Declining Sales Rates Reflecting the Risk of Excess Supply in Certain Housing Markets, Particularly Mid to Lower-End Condominiums

Source: Analysis by EIC from AREA data

The change in unsold inventory is calculated based on the change in unsold inventory as of mid-2020 compared to the unsold inventory at the end of 2019.

The change in the monthly sales rate is calculated from the average monthly sales rate of all housing units sold during mid-2020 compared to the sales rate in 2019.

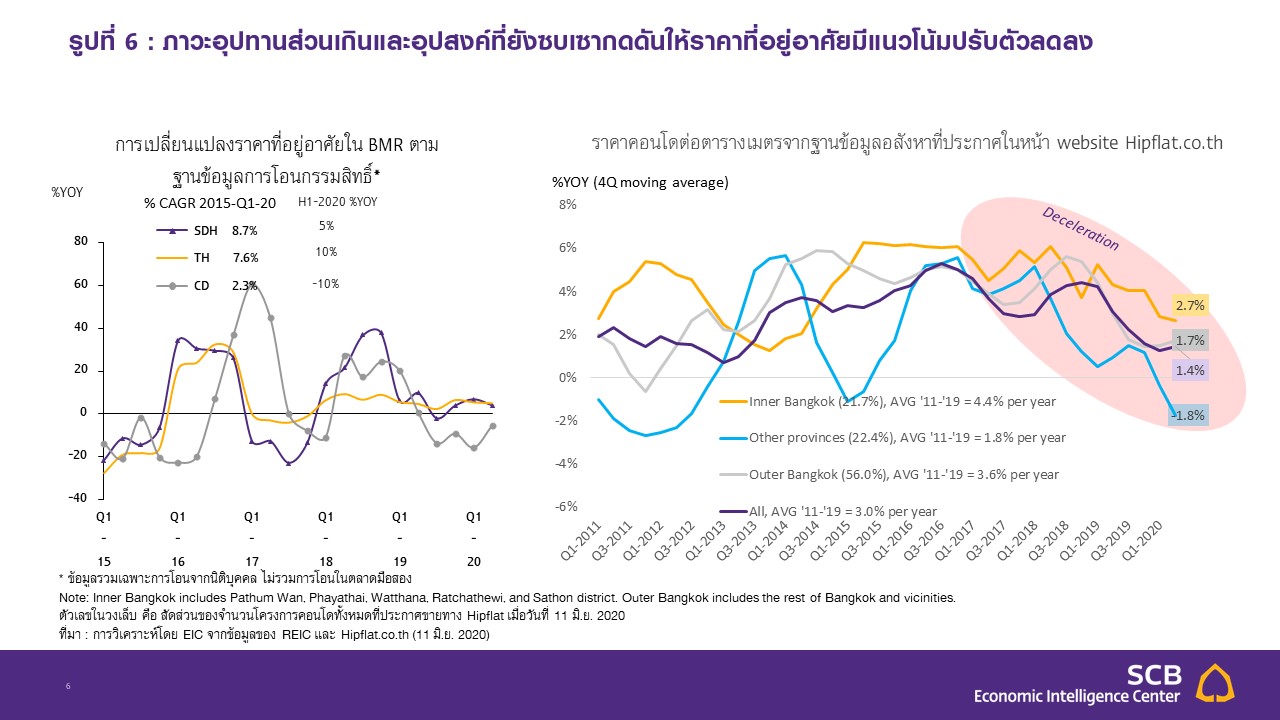

Figure 6: Excess Supply and Weak Demand Pressuring Housing Prices to Decline

Source: Analysis by EIC from REIC and Hipflat.co.th (June 11, 2020)

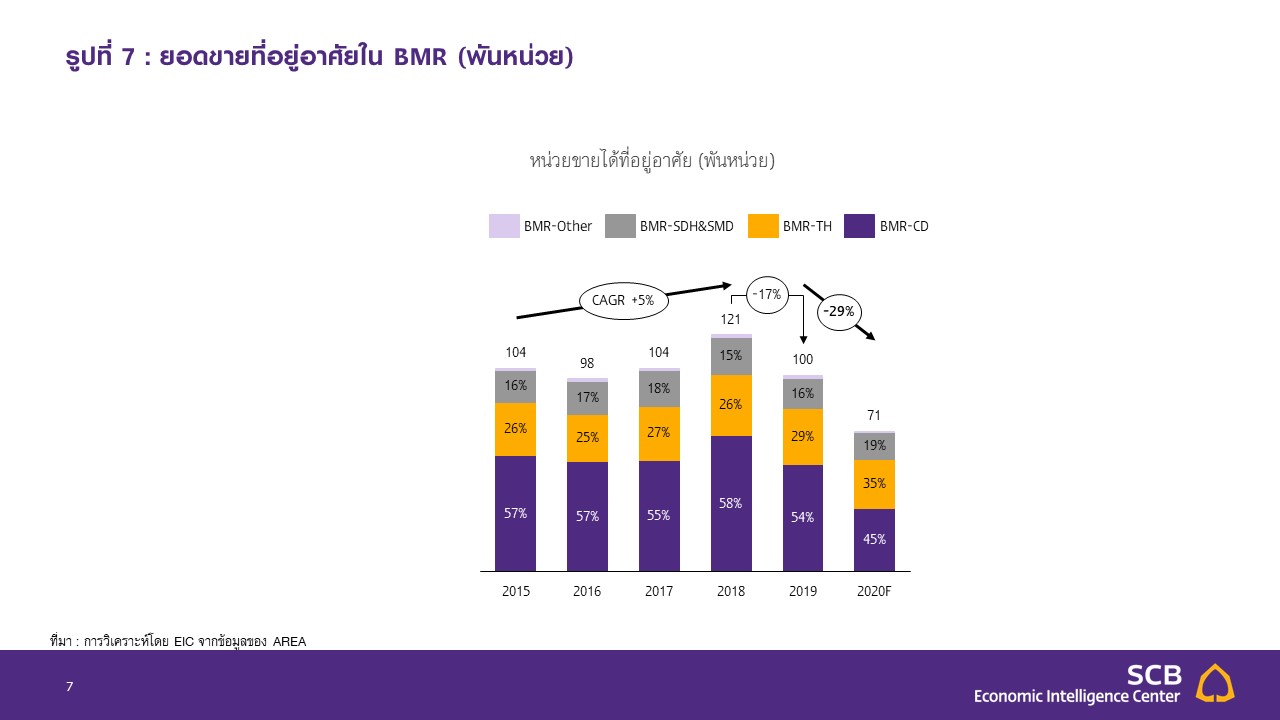

The market's significant contraction due to the impact of COVID-19 has led EIC to forecast that the number of housing sales units in 2020 will shrink by -29%. Although the recent COVID-19 situation in Thailand has improved, leading to significant relaxation of lockdown measures by the government, the severe economic impact has pushed the Thai economy into recession, with consumer purchasing power drastically reduced. EIC forecasts that the Thai economy will contract by -7.3% (as of June 2020), with economic recovery expected to be slow, particularly in the real estate sector, which requires time for consumer confidence to rebuild and for wealth accumulation to return to previous levels.

While some segments of real demand that were less affected may gradually recover following the easing of lockdown measures, as reflected in the improving sales of horizontal housing from major developers, EIC believes that overall housing sales for the remainder of the year will still recover slowly and remain stagnant, leading to a forecast of a -29% YoY decline in the number of housing sales units in 2020 (Figure 7), following a -45% YoY contraction in the first half of the year.

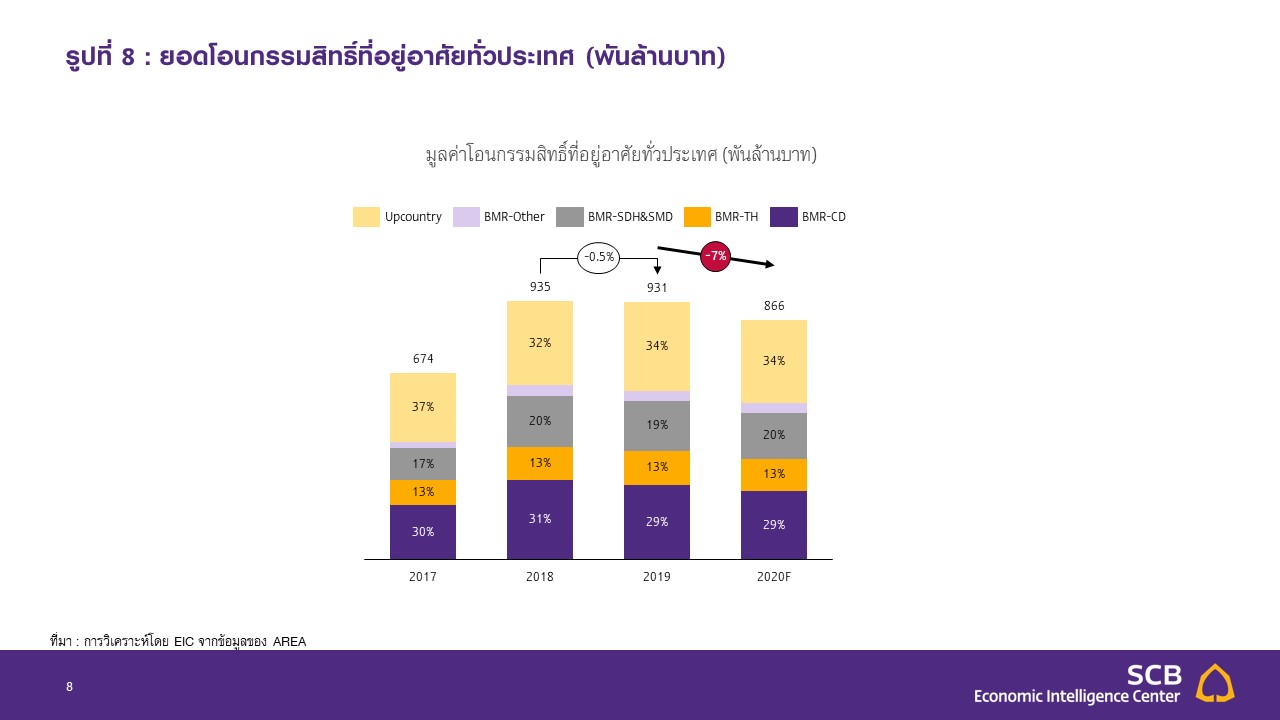

EIC predicts that the value of housing ownership transfers in 2020 will contract by -7% YoY, as the overall transfer of housing has been continuously declining since the LTV measures took effect in April 2019 and continued into 2020. The number of transfers and the value of housing transfers in Bangkok and its vicinity in the first half of the year shrank by -6.3% YoY and -5.2% YoY, respectively. The relatively less negative transfer figures are partly due to condominium transfers from sales contracts made 1-2 years prior, particularly in 2018, when condominium sales units reached 69,352. Condominiums constructed in that year began to be completed and ready for transfer in 2020, along with the government's market stimulus measures to mitigate the impact of the LTV measures, such as reducing transfer and mortgage fees.

Programs like "Good Homes with Down Payments" and low-interest loan measures from specialized financial institutions, which have been in place since 2019, continue to be effective into 2020. EIC believes that although the COVID-19 outbreak is beginning to ease, the severe economic contraction increases the likelihood of cancellations from the average of around 20-25% to 30-40% of total presales. Additionally, the lending practices of financial institutions remain strict, as reflected in the new housing loans issued in the first half of 2020, which contracted by -14% YoY, leading EIC to predict that the ownership transfers for the remainder of 2020 will continue to decline, resulting in an estimated total value of housing ownership transfers for the year 2020 to shrink by -7% YoY to 870 billion baht (Figure 8).

Figure 7: Housing Sales in BMR (thousands)

Source: Analysis by EIC from AREA data

Figure 8: Total Housing Ownership Transfers Nationwide (billion baht)

Source: Analysis by EIC from REIC data

The COVID-19 pandemic has significantly slowed down the residential real estate business, and recovery is expected to take a considerable amount of time. EIC forecasts that sales for developers will return to pre-COVID-19 levels by 2022 at the earliest, as COVID-19 has broadly impacted consumer purchasing power, not just targeting low-income groups. Although the pandemic situation is gradually improving, consumer purchasing power and confidence will require time to adjust before positively impacting the housing market. Additionally, the effects of the LTV measures mean that consumers will need time to accumulate wealth and down payments before returning to the housing market.

EIC estimates that housing sales will return to levels close to those of 2019, before COVID-19, in the second half of 2022, with the middle to upper-income segments leading the market recovery. Horizontal projects are likely to remain the primary market segment as they best meet the needs of real demand for housing, while lower-income segments are expected to recover slowly, similar to foreign sales, which are not anticipated to rebound in the near future due to the ongoing global economic slowdown.

Moreover, other factors that may impact the market should be monitored, such as government stimulus policies for real estate, low-interest loan policies from state financial institutions, progress on new subway projects, and land taxes. Although the government has significantly reduced land and property taxes by 90% in 2020, this is expected to have only a short-term effect, while the long-term burden of land taxes remains a consideration for both buyers and sellers in future project decisions.

Residential real estate developers should adjust their strategies to meet changing consumer behaviors and lifestyles, focusing on: 1) Online sales channels to facilitate buyers and serve as an important marketing tool; 2) New project development emphasizing value to align with reduced purchasing power while competing with the second-hand market, which is expected to see an increase in non-performing assets; 3) New lifestyle trends, such as the work-from-home trend, will lead consumers to prioritize both location and usable space when choosing housing; 4) Project development must respond to new consumer trends, such as health and hygiene considerations.

1) The COVID-19 outbreak has driven the adoption of technology and digital platforms in housing transactions, allowing consumers to compare multiple projects online without visiting each one. Technologies like AR and VR, along with live streaming, also help stimulate consumer interest.

2) In developing new projects, developers will emphasize value to align with reduced purchasing power and the ability to buy homes, while also competing with the expected increase in non-performing assets in the housing market due to COVID-19.

3) While location has traditionally been a key factor in housing selection, consumers may increasingly prioritize usable space as they spend more time at home. The work-from-home trend may lead consumers to seek homes with more usable space within the same budget, making townhouses, which offer more space than city condominiums but may be located slightly further away, more appealing, especially with the expansion of new subway lines improving accessibility.

4) Future project designs must address new lifestyle needs, such as creating adaptable spaces for work-from-home arrangements and energy-efficient designs, as residents spend more time at home. Developers should also prioritize safety and hygiene in living environments, incorporating touchless technology in common areas, such as key card access for doors and elevators.

SOURCE: techsauce.co/pr-news/shedding-the-housing-market-covid-19