What is Real Yield? Why Investors in Stocks and Gold Need to Know!

Understanding "Real Yield": What is it and why is it important for investors to pay more attention to Real Yield and Breakeven Inflation when analyzing stock and gold price trends?

In 2020, traditional fundamental analysis became less effective. Stock indices did not rise in line with profit growth; in fact, they often moved in the opposite direction. For instance, in the U.S., profit estimates were revised downwards, yet stock indices continued to rise. Similarly, valuation analysis proved ineffective as we encountered a year where valuations were high, fundamentals were poor, yet stock indices kept climbing, and the market's P/E Ratio continued to increase.

In a market driven by the influx of money, there are indicators that work exceptionally well for analyzing stock and gold prices, namely "Real Yield" and "Inflation Expectation." The formula for Real Yield is:

Real Yield = Nominal Bond Yield – Breakeven Inflation

Real Yield reflects the actual return investors receive from government bonds after accounting for inflation. Therefore, if Real Yield decreases, the attractiveness of government bonds diminishes, prompting capital to flow out of bonds and into other asset classes.

What many central banks are doing today is injecting money into the system, which raises inflation expectations while using QE measures to keep government bond yields low, resulting in a decrease in Real Yield. Consequently, investors will shift their money from government bonds to other assets like stocks or gold.

However, instead of the typical scenario where a rush to sell government bonds would lead to an increase in Nominal Bond Yield, the FED continues to inject money by purchasing government bonds to keep Bond Yields low, which is a mechanism of QE that causes Real Yield to decrease. In this environment where banks become the hosts of the capital market, investors should pay more attention to Real Yield and Breakeven Inflation when analyzing stock and gold price trends.

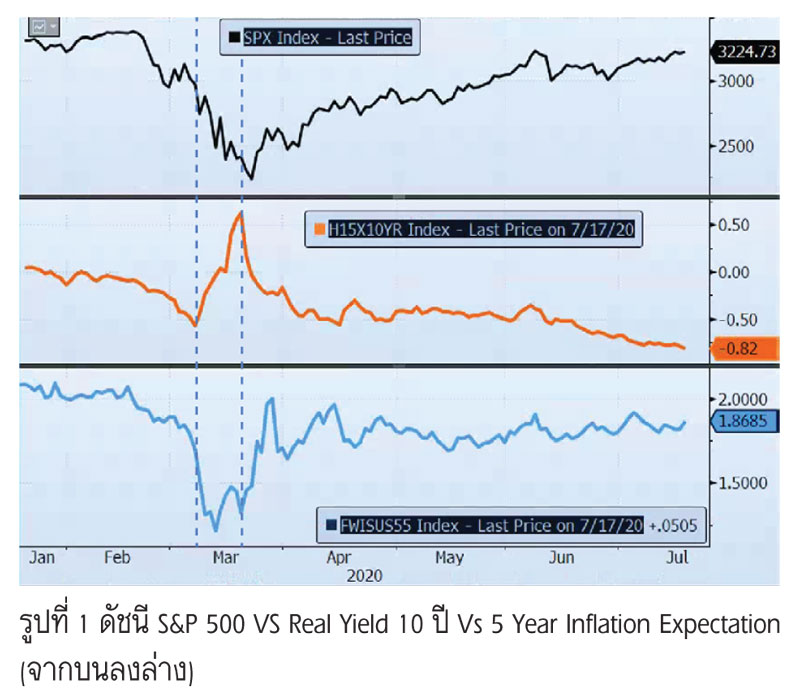

Looking back at the COVID-19 events, we can see that in March 2020, when the market panicked due to the COVID-19 crisis, Real Yield sharply increased in a short period, while inflation expectations plummeted, reflecting a severe liquidity shortage in the financial system, and the S&P 500 index fell drastically.

When the FED decided to implement QE, followed by Unlimited QE, Real Yield decreased significantly since late March 2020, falling into negative territory. This led to QE capital flowing into various assets, as evidenced by the S&P 500 index, which continuously rose from April to June 2020, despite poor economic fundamentals and corporate performance.

When we examine the relationship between gold prices and Real Yield, we find a very clear correlation this year. Particularly, when Real Yield decreased from -0.40% to -0.6%, gold prices surged from around 1,700 to 1,800 after being stagnant around 1,700 for nearly three months. The theoretical explanation is similar to that of stocks: as Real Yield becomes more negative, investors move their money from bonds to other investment assets, including gold.

In normal conditions, money flows between risk assets like stocks and lower-risk assets like gold and bonds. In an economic expansion, money flows from bonds to stocks, while in a downturn, it flows from stocks to bonds. In a crisis, money flows from stocks to safe-haven assets like gold.

However, in a situation where central banks have special tools to inflate the money supply in the global financial system, the result is the purchase of government bonds, which raises bond prices. At the same time, increasing the money supply raises inflation expectations and lowers Real Yield, causing other assets like gold and stocks to rise simultaneously. Recently, we have seen that major assets—stocks, bonds, and gold—move in the same direction, making the use of Real Yield very helpful for investment analysis.

If Real Yield continues to decrease, it reflects the FED's clear intention to have QE money flow from bonds to various assets and the real economy. Conversely, if Real Yield begins to trend upwards, it indicates that QE money is starting to decrease, and investors should reduce their exposure to risky assets accordingly.

SOURCE: www.bangkokbiznews.com