Low Thai Interest Rates: The Impacts

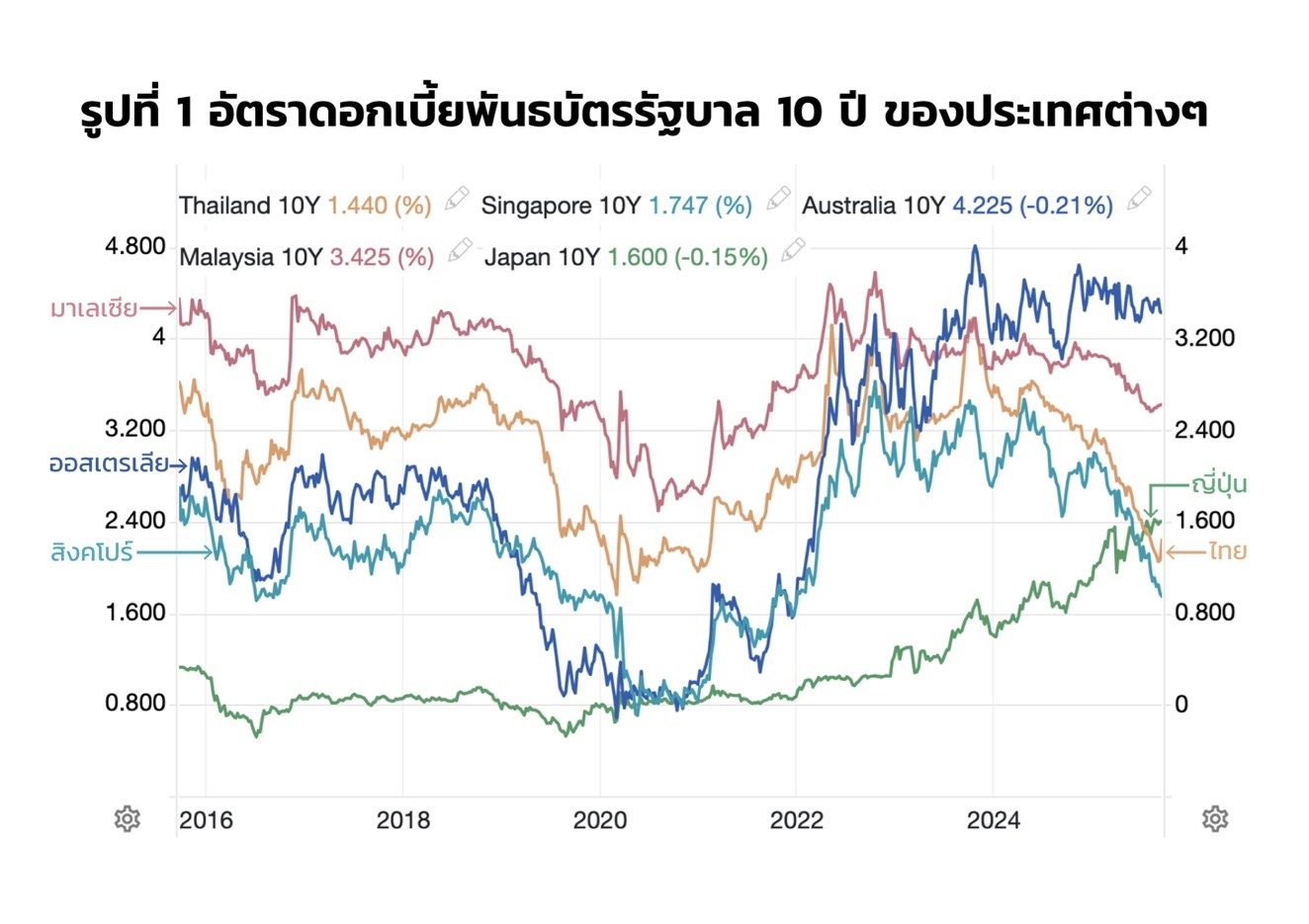

When comparing the 10-year government bond interest rates of major countries with that of Thailand, the results are as shown in Figure 1. Currently, Australia has the highest rate, followed by Malaysia, Singapore, and even Japan, all of which have higher interest rates than Thailand.

Why do interest rates in one country exceed those of another? The content of economics courses rarely addresses this question. It may be mentioned that countries with high savings rates tend to have lower interest rates, but that’s about it. However, if we compare the savings rates of the aforementioned countries against their GDP, we find that Australia has 23%, Singapore 40%, Thailand 24%, Malaysia 24%, and Japan 30%. This data does not adequately explain the comparative interest rates mentioned earlier.

In reality, the differences in interest rates between countries have deeper origins that economics courses have yet to fully explain.

This article attempts to start from issues related to the money supply, which leads to the varying levels of interest rates. Related topics include the financial statements of central banks and the financial system. However, what students of financial economics often overlook is the balance of payments of a country, which is a source of input that impacts the financial statements of financial institutions. This article will first discuss financial statements and then proceed to the balance of payments.

Table 1

Proportion of Monetary Base and Money Supply Compared to Total Assets of Central Banks

|

Country |

Monetary Base |

Money Supply M1 |

|

Thailand |

29% |

35% |

|

Singapore |

11% |

34% |

|

Australia |

101% |

425% |

|

Malaysia |

49% |

107% |

|

Japan |

87% |

150% |

Source: Financial Statements and Money Supply M1 of Various Countries

Thailand began accumulating foreign reserves again after the 1997 financial crisis. Although Thailand may not have a significant surplus in its balance of payments each year, it has gradually accumulated reserves, even in years when it experienced a deficit. The influx of foreign currency has led the Bank of Thailand to issue bonds to absorb excess money in the market to a reasonable level. When looking at the ratios of the monetary base and money supply M1, it can be seen that they are not significantly different, indicating that the money supply primarily arises from the monetary base.

Singapore is a country with significant international trade and a surplus every year. Its capital account consistently sees more inflows than outflows. However, it is noteworthy that Singapore tries to invest its money abroad to prevent excessive foreign currency in the system, which incurs some costs. Therefore, the money supply in Singapore is not largely derived from the monetary base but rather from the financial resources of the private sector.

Australia has the lowest savings rate among the five countries. If we look at the current account balance, it has been negative for a long time until it recently turned positive in the last decade. However, the capital account has consistently seen inflows exceeding outflows, primarily in the form of direct investment and securities investment. Financial institutions and businesses are the largest sources of capital inflow. Thus, the money supply is more influenced by the financial sector than the central bank, as evidenced by the ratio of money supply M1 to the total assets of the central bank.

Malaysia has a somewhat positive component in its balance of payments, primarily in trade balance. Other components are generally unstable and mostly negative, leading to an overall unstable balance of payments.

Japan's savings rate is surprisingly lower than Singapore's. The Bank of Japan creates money by holding government/private bonds and shares of private companies. Japan has consistently had a positive current account due to trade and primary income, but it also invests heavily abroad through direct investment and securities. Therefore, the money supply is more derived from domestic assets than foreign ones.

The details of each country mentioned above show that Thailand has liquidity in its monetary system (not the financial system) that allows for easy money supply expansion, simply by reducing the liquidity absorption caused by foreign currency. Not to mention extreme cases like Australia, where even the money supply relies heavily on borrowing or direct investment. Due to Australia's capital shortage, even the highest-rated companies must borrow at interest rates not lower than 3 percentage points above the central bank's policy rate. In contrast, well-rated Thai companies can issue bonds at only 0.5 percentage points above the policy rate, which translates to 6%+ compared to 2%+. The more a country relies on foreign capital, the more domestic interest rates will fluctuate according to foreign interest rates. Malaysia exhibits this characteristic, while Singapore may adjust its money supply according to its trade and financial conditions. Japan's central bank adjusts according to the needs of the private sector.

The size of the bond market in the countries mentioned is as follows: Japan $11 trillion, Australia $1.5 trillion, Singapore $0.5 trillion, Malaysia $0.5 trillion, and Thailand $0.5 trillion, with the proportion of foreign investor holdings as follows: Japan 12.5%, Australia 60%, Singapore undisclosed, Malaysia 60%, Thailand 25%. These figures clearly show that foreign investors primarily consider yield rates when deciding how much to invest. Thailand's market has the lowest yield, thus attracting the least foreign investment. However, the market's liquidity is sufficient to maintain low-interest rates, benefiting domestic investment by keeping business costs low. The state of the domestic money market can be considered at an optimum level, and it should be noted that this condition arises from long-standing trends in the balance of payments and the financial system of the country.

Liquidity in the money market, determined by monetary policy and general economic conditions, is also related to the international money market where investors will invest. An observable example is the interest rates and capital volumes in the bond market, which fluctuate according to global markets.

Sources of funding in Thailand can be divided into three main parts: the capital market and the bond market are roughly equal at about 17 trillion baht, and the bank lending market is around 13 trillion baht. The bond market has about 25% of trading volume from foreign investors, while the stock market has about half of its trading volume from foreign investors. Therefore, the conditions of the money and capital markets affect the domestic market but not to the extent of 100%. Theoretically, money flowing into the Thai bond market may fluctuate with exchange rates or international interest rates, but the average monthly outright trading volume of bonds has been steadily increasing since the 1997 Thai financial crisis, from 234,767 million baht in 2005 to 1,808,279 million baht in 2025, or an average rate of 8.5% per year. The correlation with those variables is not very clear, but the increasing volume has kept Thai bond interest rates relatively low during the years 2016-2021, including the current year 2025.

The characteristics of the Thai money and capital markets are determined by the structure of the balance of payments and the policies of the Bank of Thailand, resulting in a reasonably liquid financial system compared to other countries. Interest rates in the market are relatively low, even compared to developed countries, but certainly not compared to Japan, as Japan has a monetarist financial system where banks do not hold foreign reserves but instead hold government and private sector assets. Additionally, Japan has a low proportion of Japanese bonds held by foreign investors at only 12.5%, so there is less concern about foreign market manipulation. Thailand has higher interest rates than Japan but lower than many other countries. Furthermore, there are avenues for risk diversification by connecting with international markets. Currently, Thailand is experiencing an increasing and more frequent deficit in the financial account, but the amount of the deficit remains very low, allowing Thai companies opportunities for business growth abroad as a substitute for the declining growth rate of the domestic economy.