Overview of the Bangkok Condo Market in 2017: Record High Launches in 10 Years, Luxury Segment Remains Strong; Watch for Investors and Buyers from Hong Kong, China, and Japan

- Future project trends must focus on integrating technology into the lifestyle as customers adapt to an aging society -

Bangkok - December 21, 2017: Nexus Co., Ltd. reveals that the Bangkok condo market in 2017 was vibrant, setting a new record with the highest number of units offered for sale in 10 years. Phra Khanong - Suan Luang remains popular with the highest number of projects launched, while Pathum Wan - Ratchathewi saw price increases of up to 16%. It is expected that in 2018, growth will continue with supply increasing by at least 10%. The future housing trend is moving towards a state of "transformation" due to various factors, including foreign investment, rapid growth of CLMV, Thailand's transition to an aging society, and the increasing role of technology in project development.

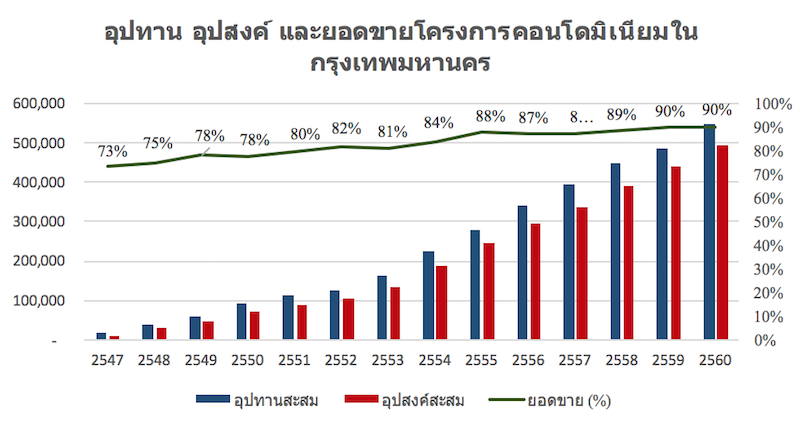

Ms. Nalinnarat Charoensupong, Managing Director of Nexus Property Marketing Co., Ltd., revealed the condominium market research results in Bangkok for 2017 and projected trends for 2018, stating that 2017 was a year of fierce competition among condominium developers in Bangkok, with new supply from both large and small developers reaching 62,700 units from 128 projects. This was the year with the highest number of units entering the market in the past 10 years. The significant increase in condominium supply was due to both large and new developers continuing to develop projects, including many large-scale developments, resulting in a total market of 550,000 units, with new launches exceeding the average of the past five years by 15% (the average number of new units launched from 2013 to 2017 was 53,600 units per year). Projects continue to expand into areas surrounding the city center, with the top three locations for increased supply being: 1. Phra Khanong - Suan Luang with 14,400 units or 23%, 2. Phaya Thai - Ratchadapisek with 13,200 units or 21%, and 3. Thonburi - Phetkasem with 8,900 units or 14%, accounting for over 58% of all newly launched condominiums.

Regarding the expansion of project development, it is well known that over the past five years, the condominium market has significantly expanded from the city center. The area with the highest growth rate for condominiums is Thonburi - Phetkasem, which grew by 107%, followed by Tiwanon - Rattanathibet at 76% and Chaeng Watthana - Pak Kret at 68% compared to 2016.

Demand

The overall demand in 2017 continued to grow well, with new sales in the market at 57,300 units, which is 14% higher than the average sales rate of the past five years (the average sales rate from 2012-2016 was 50,400 units per year). However, when considering the overall sales rate of condominiums in the market, it remained stable at 90% (total accumulated sales of condominiums increased to 496,100 units), leaving approximately 53,900 units available for sale in the market.

In 2017, newly launched condominiums had an average sales rate of 62%. The top three locations with the highest sales of units were: 1. Phra Khanong - Suan Luang, 2. Phaya Thai - Ratchadapisek, and 3. Pathum Wan - Ratchathewi, with Phra Khanong - Suan Luang remaining a popular area with a large number of new units launched each year and a continuously increasing sales rate. The Pathum Wan - Ratchathewi area had the highest sales rate for new units at 88%.

Source: Nexus Research, December 2017

Prices

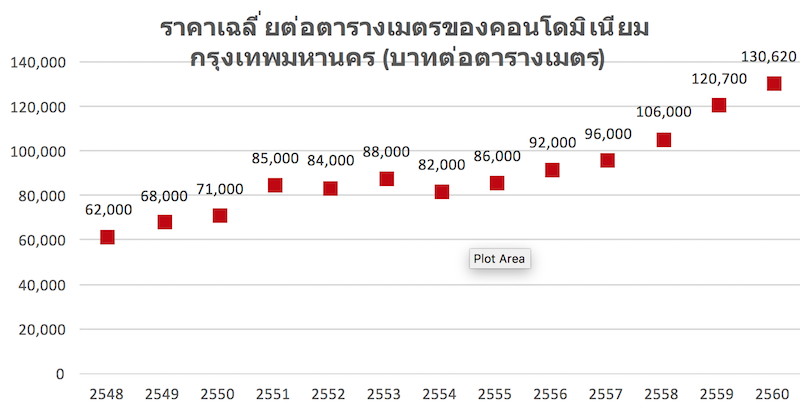

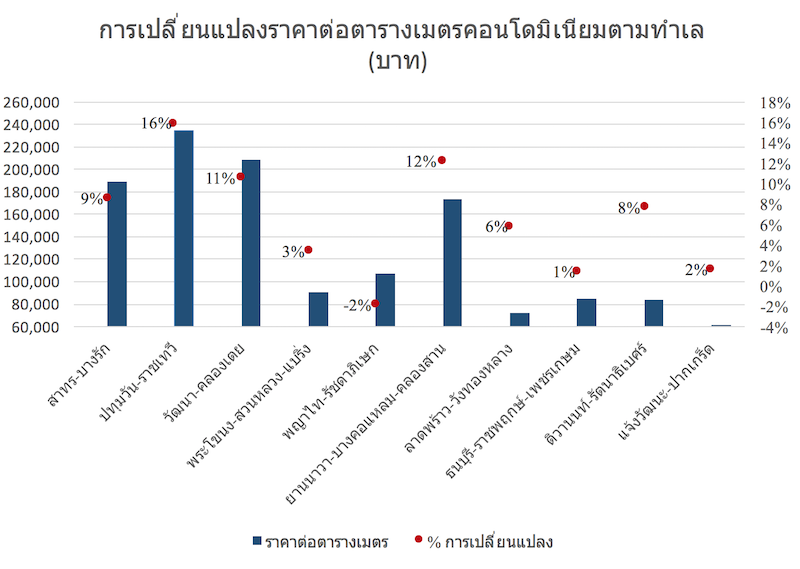

In 2017, the average selling price of condominiums in Bangkok increased at a slower rate, rising by 8% from 2016, with an average price of 121,000 THB per square meter increasing to 130,600 THB per square meter in 2017. This rate of increase is close to the average growth rate of condominium prices over the past five years, which was an average of 9% per year. However, upon closer examination, it is found that the areas with the highest price increases for condominiums are in the Pathum Wan and Ratchathewi districts, where prices increased by 16% to 234,000 THB per square meter. This is due to the high demand for units in this location, rising land costs, and a limited supply of new units in this area over the past few years. In the city center, prices increased by 12% to 210,700 THB per square meter, following the same trend. The Yan Nawa and Klong San districts, which have good sales, also saw price increases of 12%. For projects in the outer Bangkok area, prices increased only slightly, around 5%.

Source: Nexus Research, December 2017

Source: Nexus Research, December 2017

Regarding the forecast for the condominium market in 2018, Ms. Nalinnarat stated that in terms of supply, it is expected to increase by at least 55,000 units or 10%. The inner Bangkok and areas surrounding inner Bangkok will see the most new supply, while outer Bangkok will have fewer new projects but with a relatively high number of units per project. Demand for units is expected to continue to grow at a rate similar to that of supply, resulting in approximately 58,000-60,000 units remaining in the market in 2018.

For condominium prices in the inner Bangkok market in 2018, it is expected to increase by at least 11%, while prices in the inner Bangkok and outer markets will rise by about 5-6%, resulting in an overall average price increase of at least 8%.

In 2018, there will be a trend towards developing condominiums in all segments into smaller buildings of 7-8 stories, as land along major roads becomes scarce and prices continue to rise. When considering the movements in the condominium market, segmented by price, it can be divided into five segments: 1) Super Luxury Market, 2) Luxury Market, 3) High-End Market, 4) Mid-Range Condos, and 5) City Condos.

For the Super Luxury and Luxury markets, it is observed that both large and new developers continue to show interest in this market. Price trends are expected to continue to rise, while the buyer group will expand to include foreign markets, with foreign buyers investing for both rental and second home purposes. The entry of foreign investors not only as buyers but also as joint venture partners will enhance buyer confidence.

In the High-End market, most project developers will still be large companies seeking to acquire land near the city center's mass transit. However, the limited buyer pool in this market will affect sales. The Mid-Range condo market remains focused on projects near the city center and mass transit, catering to buyers with stable incomes seeking actual residences, necessitating developers to create products that truly meet this demographic's lifestyle. For the City Condo market, price conditions remain a key factor in buyers' decisions, so developers must manage costs effectively to achieve good selling prices while considering payment terms and financing options that do not overly burden buyers.

Forecasting Future Real Estate Market Trends in the Short and Medium Term

Ms. Nalinnarat forecasts the short and medium-term housing market trends, stating that the outlook for real estate will primarily be based on the projected economic growth rate (GDP) of the country, which the government has set at around 4% for 2017-2020. This figure is expected to reflect positive growth in various sectors of the economy. However, when looking deeper into the real estate segments, we must also consider various internal and external risk factors that could significantly impact the growth of the real estate market. These factors include economic developments in neighboring countries, as in the next 10 years, countries in the CLMV region may catch up with Thailand. As these countries develop and continue to grow, the investment capital that previously flowed into Thailand may be distributed to neighboring countries. The purchase of real estate in Thailand by foreigners may begin to decrease as more options become available in neighboring countries. Additionally, in the coming years, Thailand will transition into an aging society, which will necessitate changes in housing to accommodate the lifestyles of the elderly. Rapid technological advancements that affect people's lifestyles will also influence housing trends. All of these factors can be summarized into three main trends regarding future housing: investment trends, housing trends, and location.

Trend 1: In terms of investment, developers will increasingly focus on developing long-term leasehold projects on large, potential land owned by government agencies, creating mega projects that integrate land use. Buyers are also showing more interest due to lower costs. Additionally, we will see the development of mixed-use projects to diversify risks and reduce business competition. The foreign market will continue to play a significant role, both in large and small investments, with foreign companies interested in partnering with Thai developers on various projects, bringing in investment capital and technology. Foreign joint ventures are coming from various countries, including Japan, China, and Hong Kong, while foreign individual investors purchasing units for long-term investment and rental continue to increase.

Trend 2: In terms of future housing, demographic factors indicate that Thailand is moving towards an aging society. Therefore, markets for senior homes or elderly care will emerge to meet the needs of Thai society, and these products will continue to develop. The challenge will be to make these products acceptable and adaptable to Thai lifestyles. At the same time, technology that quickly integrates into lifestyles will require developers to create housing that meets these changes, such as homes equipped with technology. Additionally, the concept of truly livable homes, such as small units with large communal spaces, sustainable housing with quality construction, and socially and environmentally friendly homes that provide a relaxing living environment for long-term residents.

Trend 3: In terms of location, which remains a crucial factor influencing housing trends, interesting locations for the condominium market can be divided into three main groups: the first group is central urban locations, which will increasingly be defined as smaller centers (Nodes), such as Phrom Phong to Thong Lor, becoming a hub for luxury lifestyles with both high-end condominiums and upscale homes, as well as numerous chic restaurants and attractions. New business centers around Ratchada and Rama 9, the historical areas of Yaowarat and Charoen Krung, and luxury residential centers like Lang Suan and Ploenchit. The second group is locations near mass transit, which should be considered carefully, as the development of a good public transport system will significantly impact real estate growth. The most noteworthy area is Bang Sue, as the government is pushing for Transit Oriented Development (TOD) in this area. The ongoing extensions of the green, yellow, and orange subway lines are also of interest. Finally, the third group is riverside locations, such as Charoen Nakhon and Charoen Krung, which are becoming new shopping and lifestyle centers.

The growth of real estate is a chain reaction, a cycle interconnected throughout the system. As we observe changes in economic, social, cultural, and technological conditions rapidly evolving both nationally and globally, all of these are factors that developers must prioritize.

Thank you for the information from www.nexus.co.th