Industrial Market in the Second Half of 2025

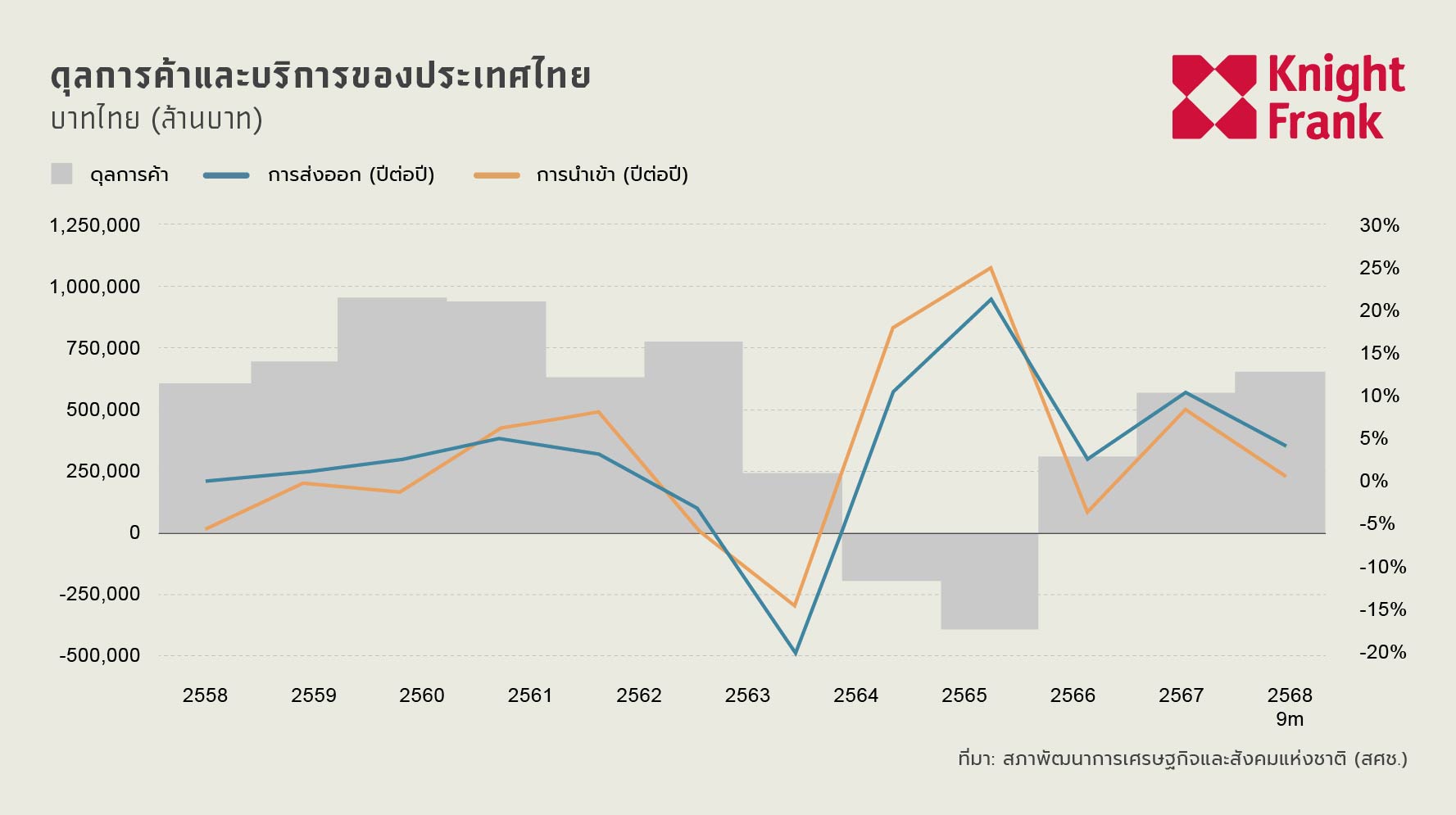

The Thai economy significantly slowed down in the third quarter of 2025, with the real Gross Domestic Product (GDP) growing by only 1.2% compared to the same period last year, down from 2.8% in the previous quarter. This slowdown reflects weakened domestic momentum, although the economy continues to benefit from foreign demand and a persistent trade surplus.

Exports remain the main engine of growth, increasing by 11.5% compared to the same period last year, reaching $86.2 billion, equivalent to 2,783.3 billion baht. This growth is primarily driven by the high-tech manufacturing sector, including computers and electronic components (+125.0%), telecommunications equipment (+55.2%), and integrated circuits (+31.7%). However, following the implementation of U.S. retaliatory tariffs, overall growth rates began to slow down as businesses adjusted their production and raw material sourcing strategies across several key industries.

The structure of the domestic industrial sector clearly reflects the differences between investment and consumption, with private investment growing by 4.2%, supported by investments in machinery and equipment, particularly industrial machinery and vehicles. Meanwhile, the overall economy faced a significant decline in inventory, decreasing by 136.371 billion baht. The relationship between investment in machinery and the decline in inventory indicates that businesses are depleting existing stock in the short term while simultaneously increasing production capacity to prepare for new production cycles in the future.

Conversely, public investment contracted by 5.3%, while the momentum of private consumption remained weak, despite growing by 2.6% compared to the same period last year for the second consecutive quarter. However, in value terms, private consumption decreased to 2,806,651 million baht, reflecting household caution and a declining consumer confidence level, which continues to exert pressure on domestic economic growth.

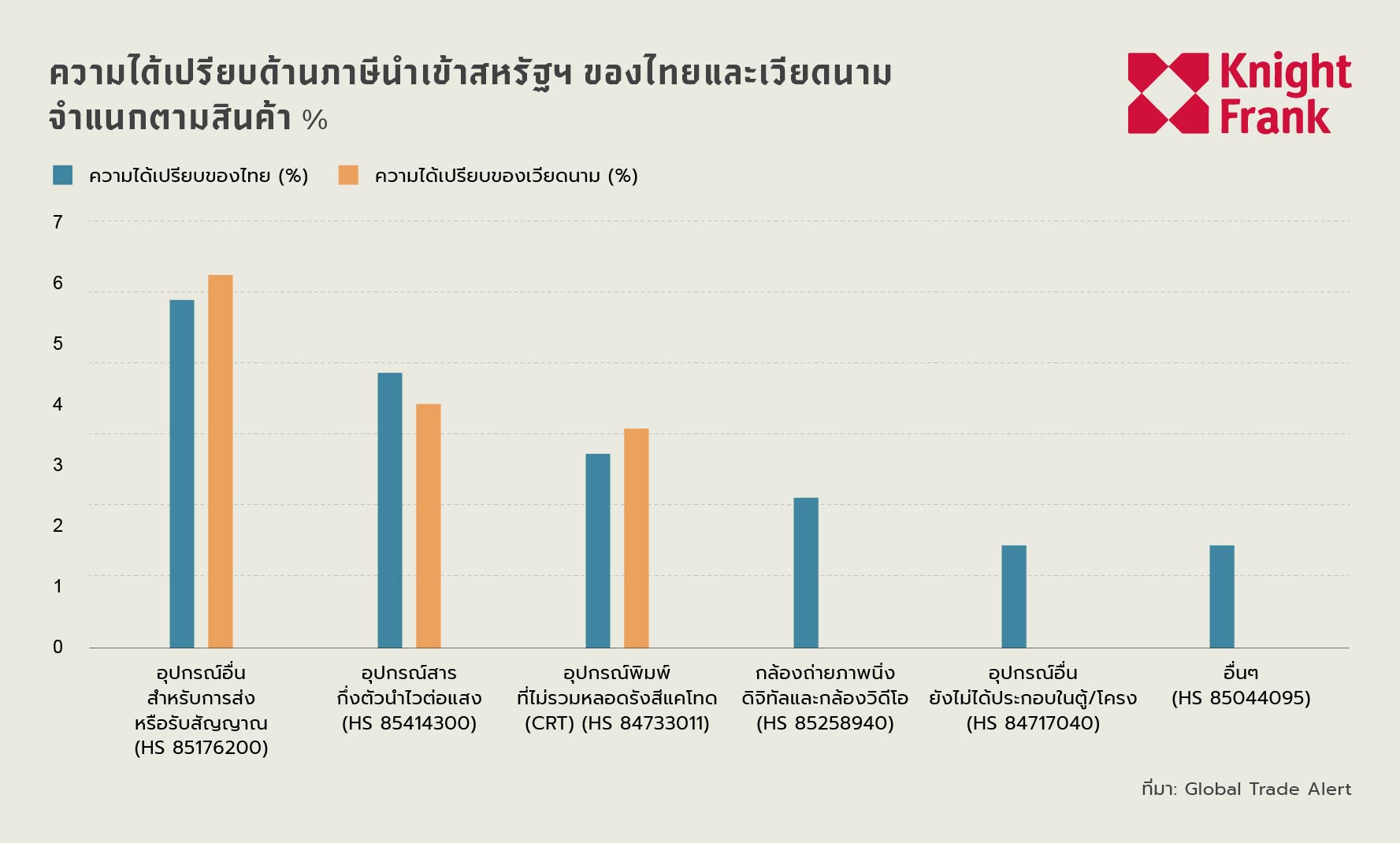

Currently, Thailand's export sector accounts for approximately 10% of GDP through the U.S. market, benefiting from tax rate advantages compared to regional competitors. This competitive position has allowed Thailand to increase its market share of U.S. imports across several key product categories.

In the telecommunications equipment category (HS 85176200), Thailand's performance stands out significantly. Despite Vietnam being classified in the “Green Zone,” Thailand's share of U.S. imports increased from 4.1% to 11.9% during the trade war transition, a rise that outpaced Vietnam's increase of only 6 percentage points during the same period, reflecting Thailand's role as a rapidly growing alternative for U.S. technology companies seeking to diversify away from China in the networking equipment sector.

A similar pattern is observed in the computer parts category (HS 84717040), where U.S. imports from Thailand have shown consistent resilience throughout Trade War 2.0, while imports from China have continued to decline, reflecting Thailand's increasing role as a stable and reliable supplier in the global technology supply chain.

In the category of transformers and energy equipment (HS 85044095), the adjustment of U.S. sourcing is also evident, with the U.S. significantly reducing imports from China while increasing imports from Thailand by 3.7% during Trade War 2.0, further reinforcing Thailand's role as a beneficiary of changes in trade and industrial policies.

In addition to quantitative changes, Thailand has also benefited from tax advantages in several subcategories of technology and electronics products that Vietnam does not enjoy, such as digital still and video cameras (HS 85258940), unassembled computer parts (HS 84717040), and other electrical and energy equipment (HS 85044095). The tax gaps for these specific products further enhance Thailand's competitive capabilities in the U.S. market and provide additional cost incentives for U.S. operators to source goods from Thailand rather than Vietnam.

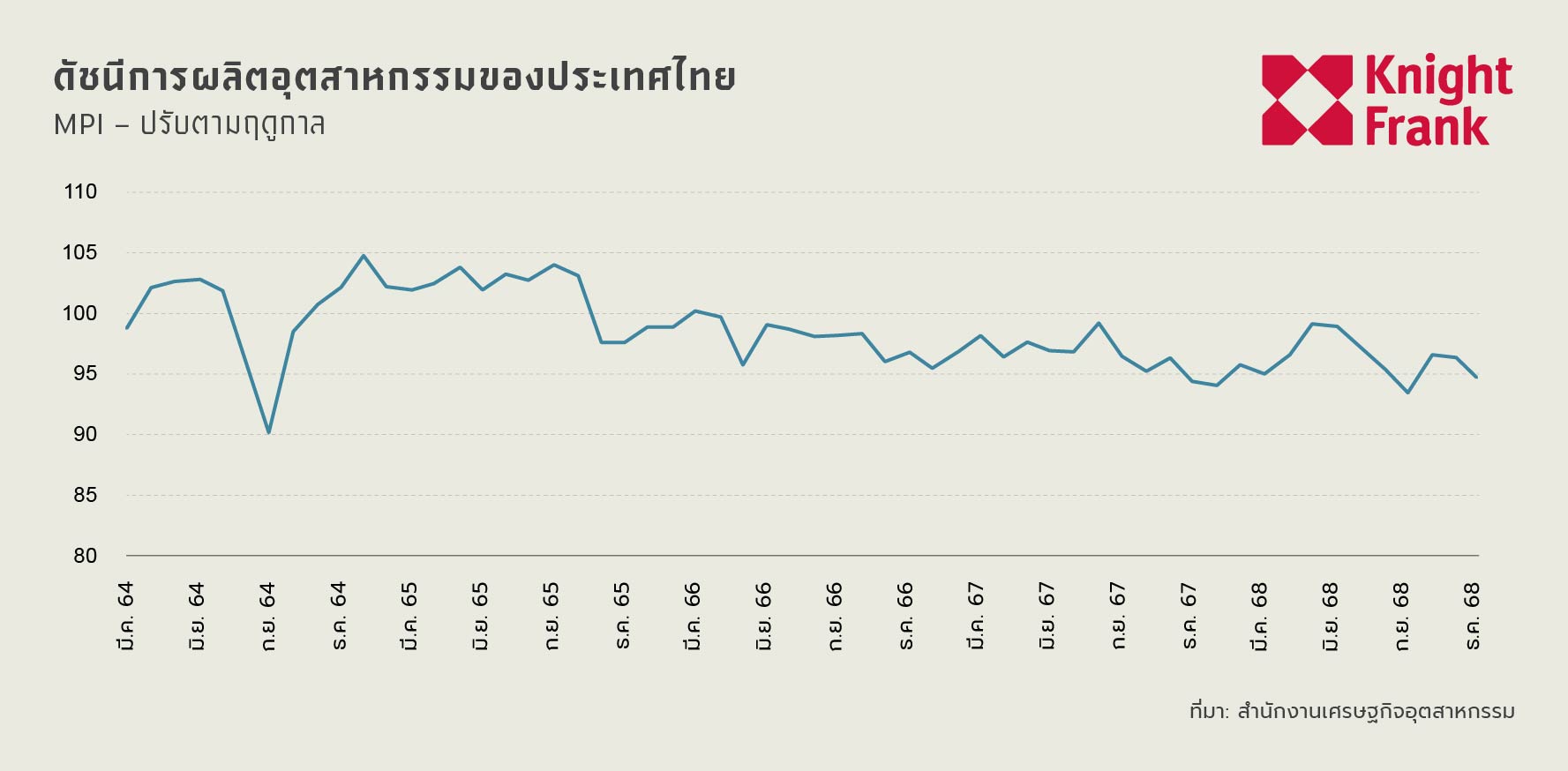

The manufacturing sector remained stable in the first half of the year, with the average MPI at 97.0, supported by a recovery in June and stable production in the food and electronics sectors. However, momentum weakened in the second half of the year, with the MPI dropping to 95.4, contracting by 0.5% compared to the same period last year.

In the third quarter, the performance of each industry varied significantly. The steel industry was the standout, with the MPI increasing by 13.9% due to a significant rise in hot-rolled steel production (+42.1%) and rebar (+21.2%), supported by lower production costs from a stronger baht.

The technology industry showed mixed results, with electronics production declining slightly by 1.3% compared to the same period last year, while hard disk drive production increased by 10.5% due to continued strong demand in the AI sector and investment in data centers. Appliance production increased by 3.0%, with transformers being the main driver (+32.2%).

Conversely, petroleum and automotive production decreased, partly due to refinery maintenance shutdowns and temporary production halts in the automotive sector.

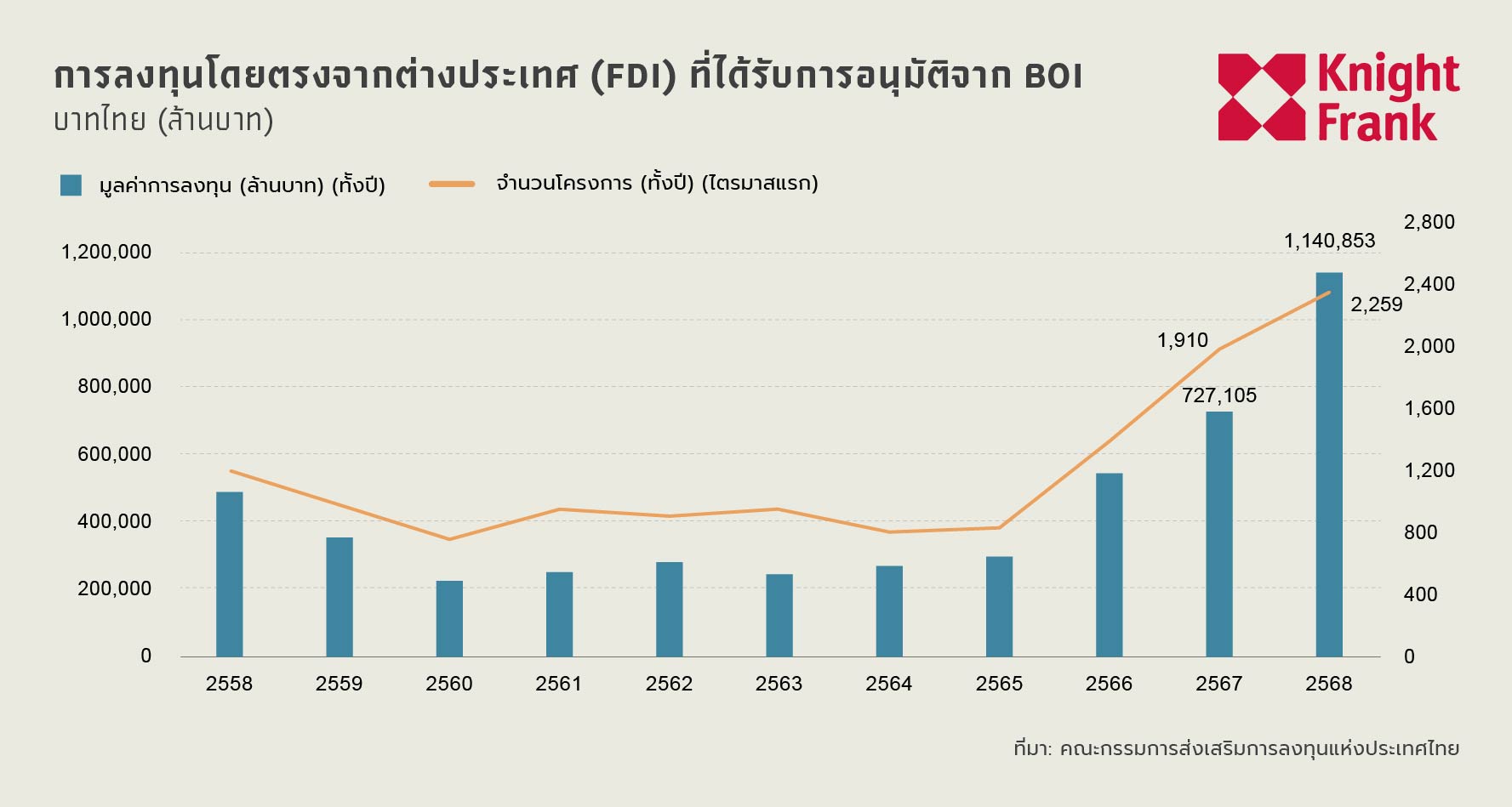

By the end of 2025, the value of approved foreign direct investment (FDI) increased from 1,063 projects worth 629.6 billion baht in Q2 to 2,259 projects with a total value of 1.14 trillion baht, representing an increase of 1,196 projects and an increase of 413.8 billion baht in approved investment during the second half of the year.

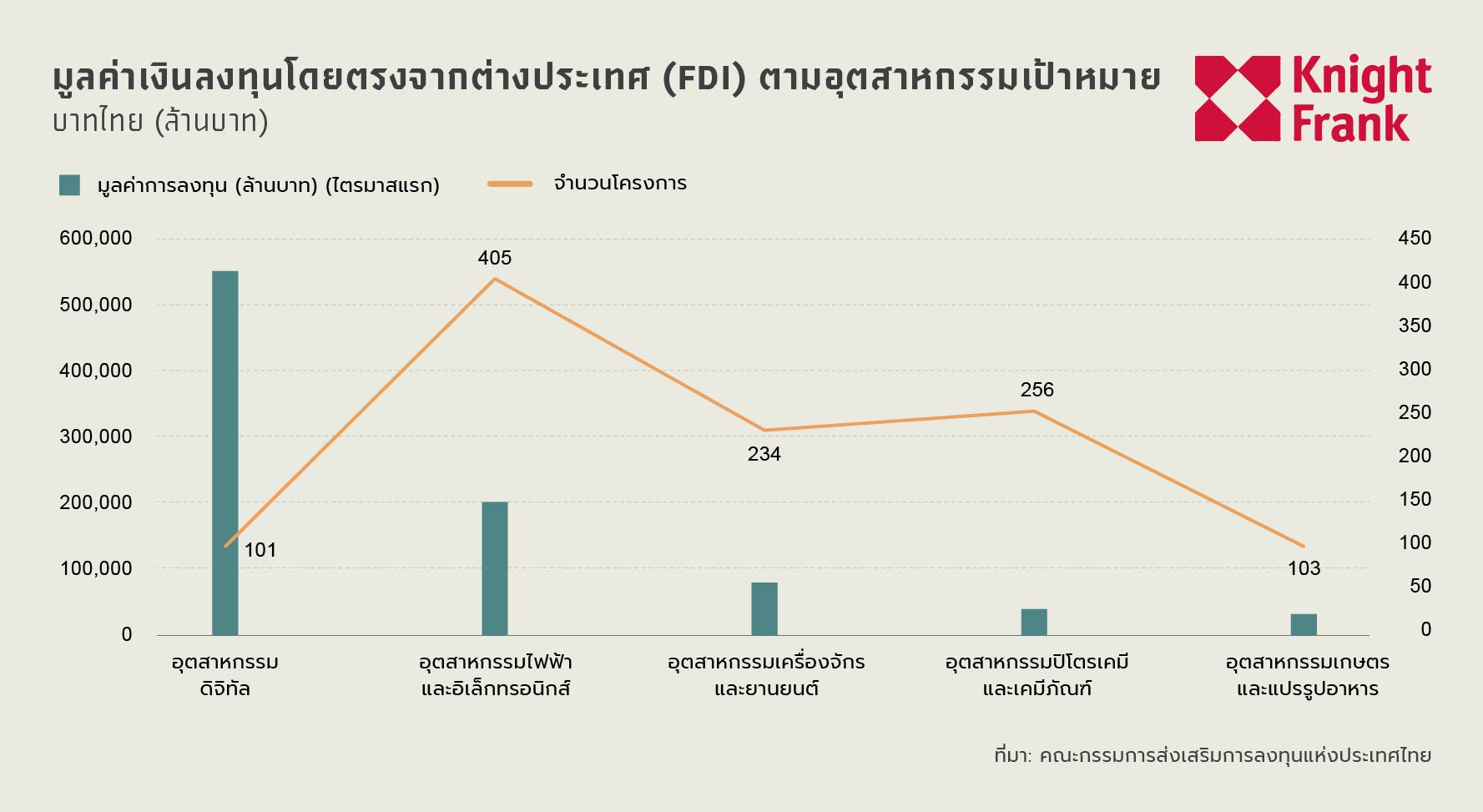

In terms of structure, the machinery and automotive sector had the highest number of approved projects at 440, while the digital sector had significantly higher investment intensity and accounted for the largest share of total investment value, despite having fewer projects.

When considering by industry, the metals and materials sector experienced the fastest growth, with investment value increasing from 32.8 billion baht in Q2 2025 to 81.8 billion baht in Q4 2025, representing a 149% increase. Meanwhile, the digital sector saw the highest inflow of investment in value terms, rising from 322.2 billion baht to 553.0 billion baht (+71.6%) and becoming the main driver of FDI growth in 2025, resulting in the digital sector having the highest investment value, followed by the electrical and electronics sector (204.4 billion baht) and machinery and automotive (119.3 billion baht), reflecting a transition towards a technology-focused and high-investment industrial structure.

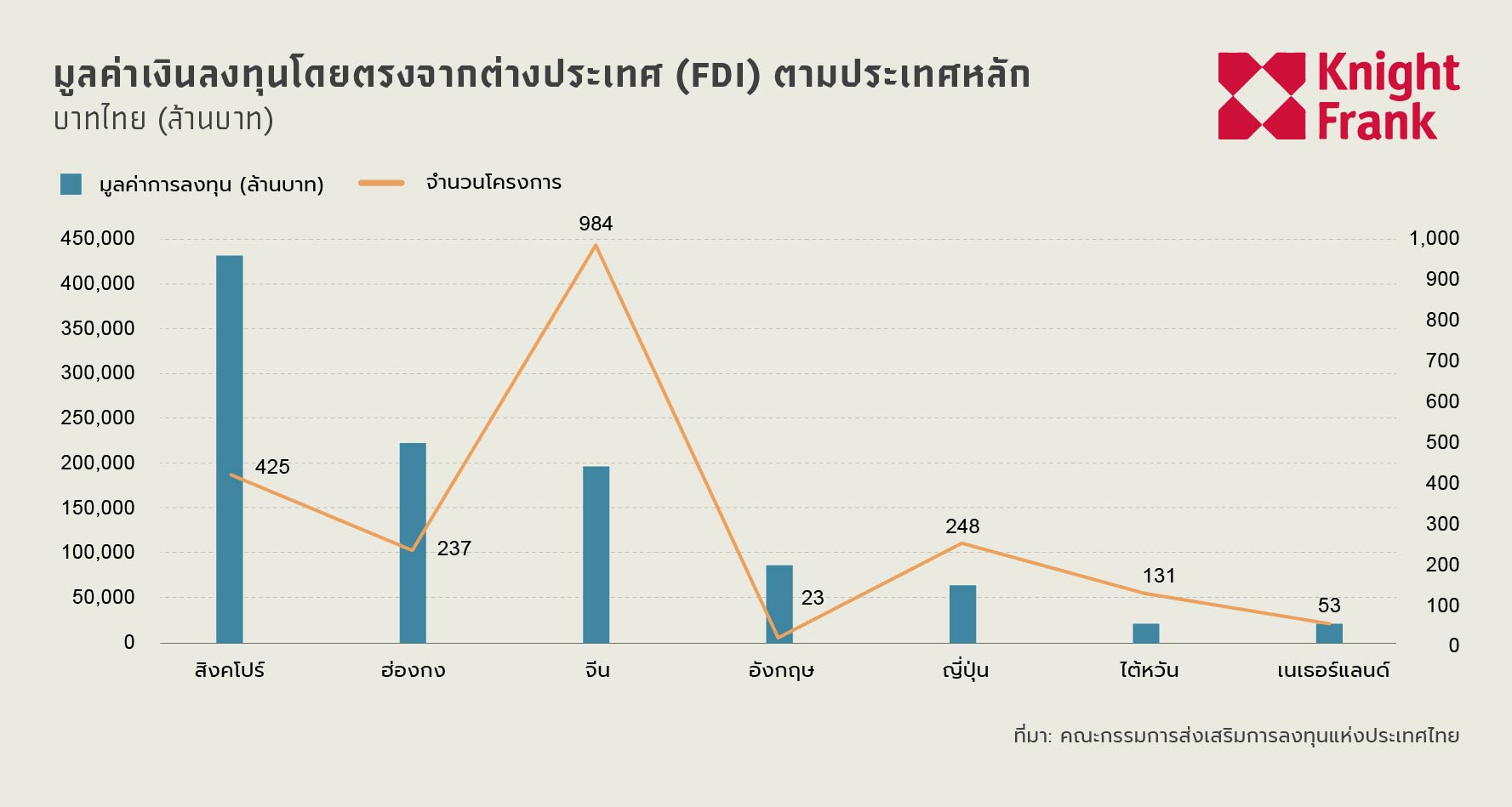

Geographically, Singapore remains the top source of foreign investment, with an investment value of 433.019 billion baht, followed by Hong Kong and China, with China having the highest number of projects at 984. Meanwhile, Western countries and regional partners, such as the United Kingdom, Japan, and the United States, continue to play a significant role, reflecting global investor confidence. This trend indicates investor confidence in the shift towards high-value digital and electronic infrastructure and Thailand's role as a strategic hub for advanced manufacturing and data services in the region.

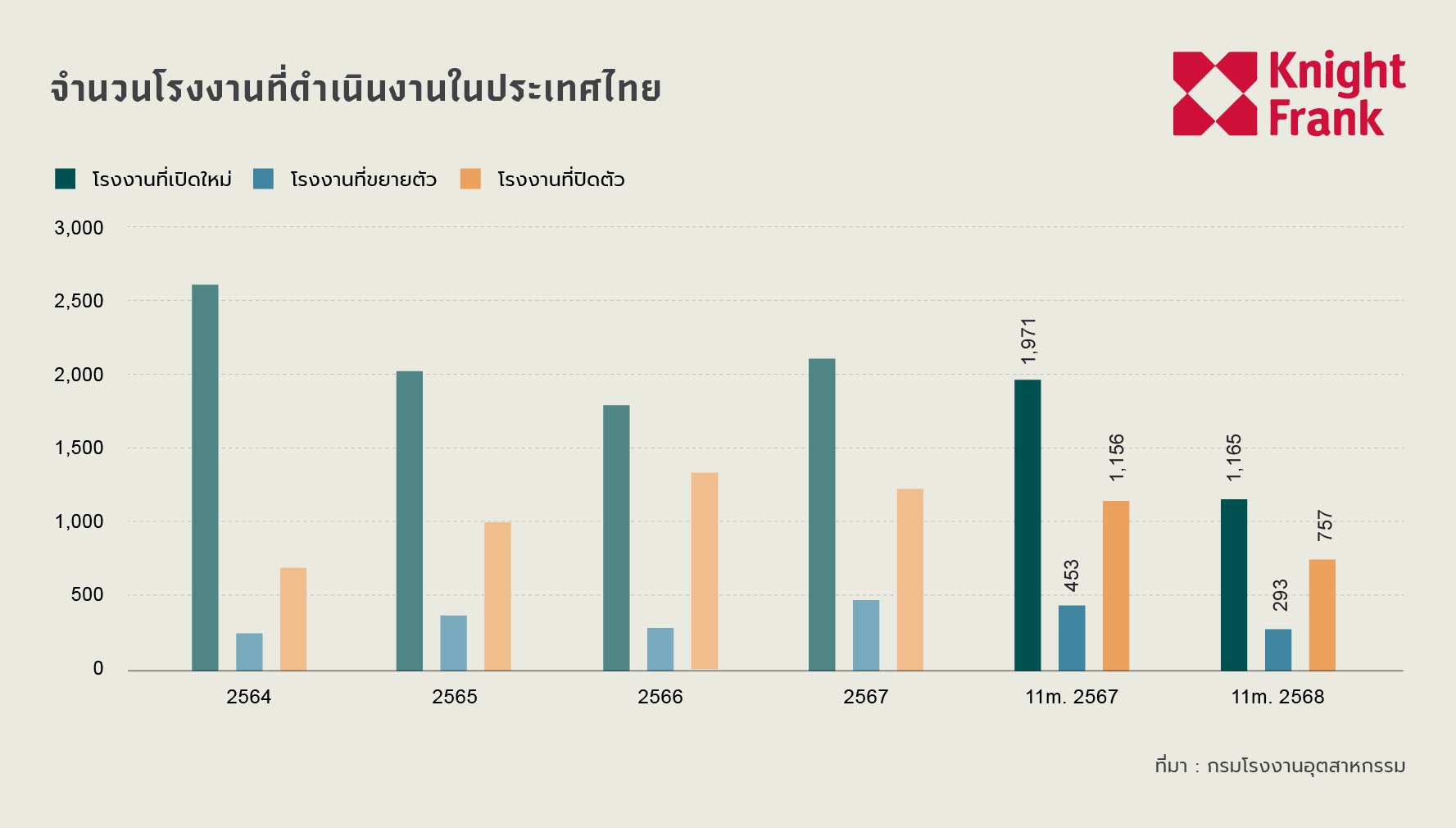

In the first 11 months of 2025, the Thai industrial sector entered a cautious adjustment phase, with the number of new factories opening down by 41% to 1,165, while factory expansions decreased by 35% to 293, reflecting weakened investor confidence. However, business closures decreased significantly by 34.5% to 757, indicating improved business survival rates. Although new investments have clearly slowed compared to the peak between 2021 and 2024, the industrial sector still recorded a net positive growth of 408 factories, reflecting a “wait-and-see” attitude where existing operators prioritize stability over aggressive expansion.

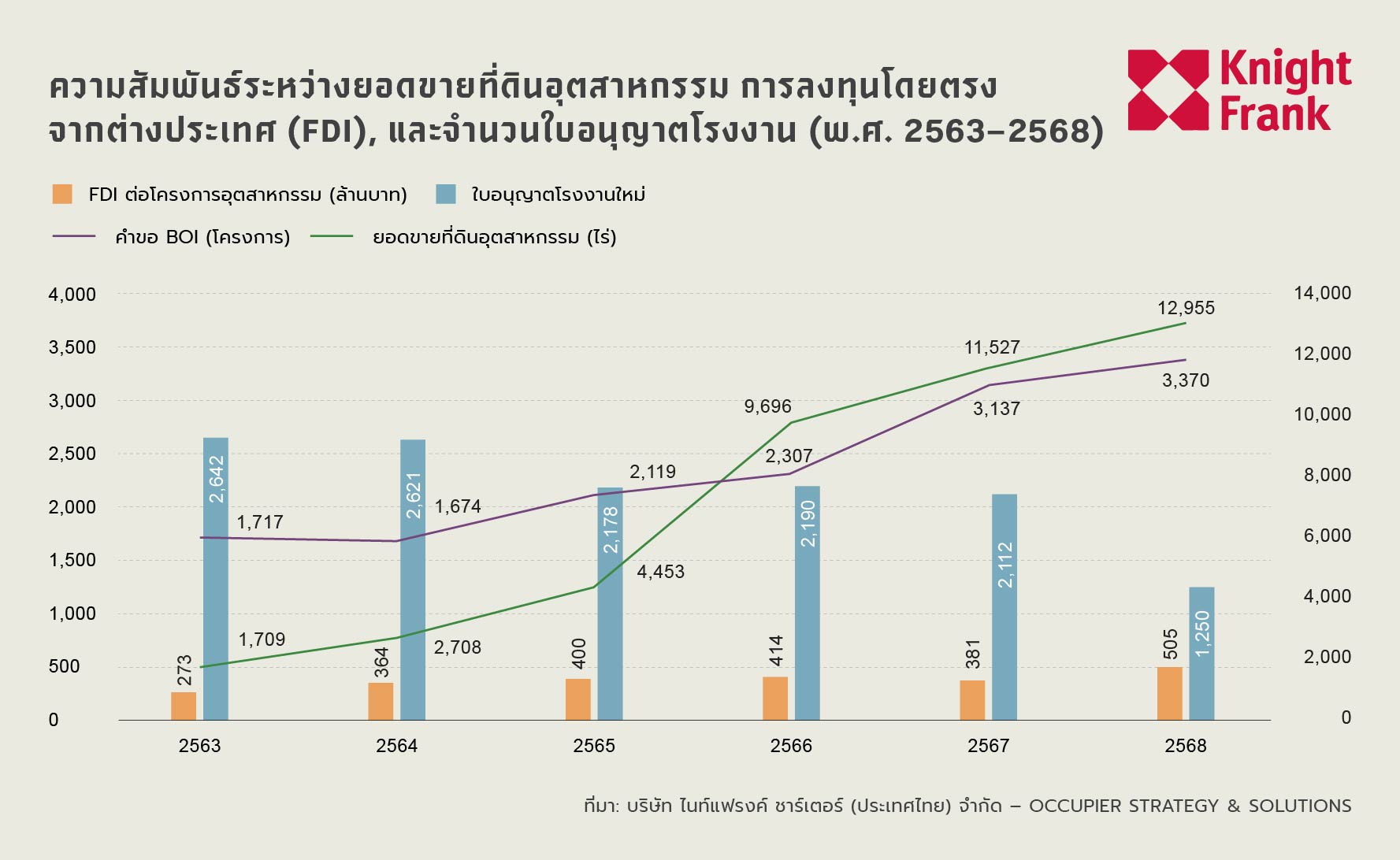

The structure of Thailand's industrial sector is transitioning towards a model with fewer but larger projects requiring higher investment, with industrial land absorption increasing from 4,684 rai in the first half of 2025 to 12,955 rai by the end of 2025, while the average FDI value per project increased to approximately 505 million baht, reflecting a shift towards high-value investments, even as the number of new factories decreases.

This trend is most evident in the digital sector, which attracts significant investment, while the electrical and electronics industry continues to expand due to demand for advanced components linked to AI and data storage technology, maintaining a high level of approved projects. Meanwhile, the machinery and automotive sector focuses more on upgrading production capacity and technology improvements rather than establishing new factories.

At the same time, the number of new factory licenses has decreased to approximately 1,250 in 2025, reinforcing the transition from “quantity” to “quality” in industrial development. This difference reflects that large-scale, high-investment projects, especially in digital infrastructure, often require significant land and investment but do not necessarily need to apply for traditional factory licenses, resulting in increased land absorption and FDI flows, even as the number of factory licenses declines.

Serviced Industrial Land Plots (SILP) Supply

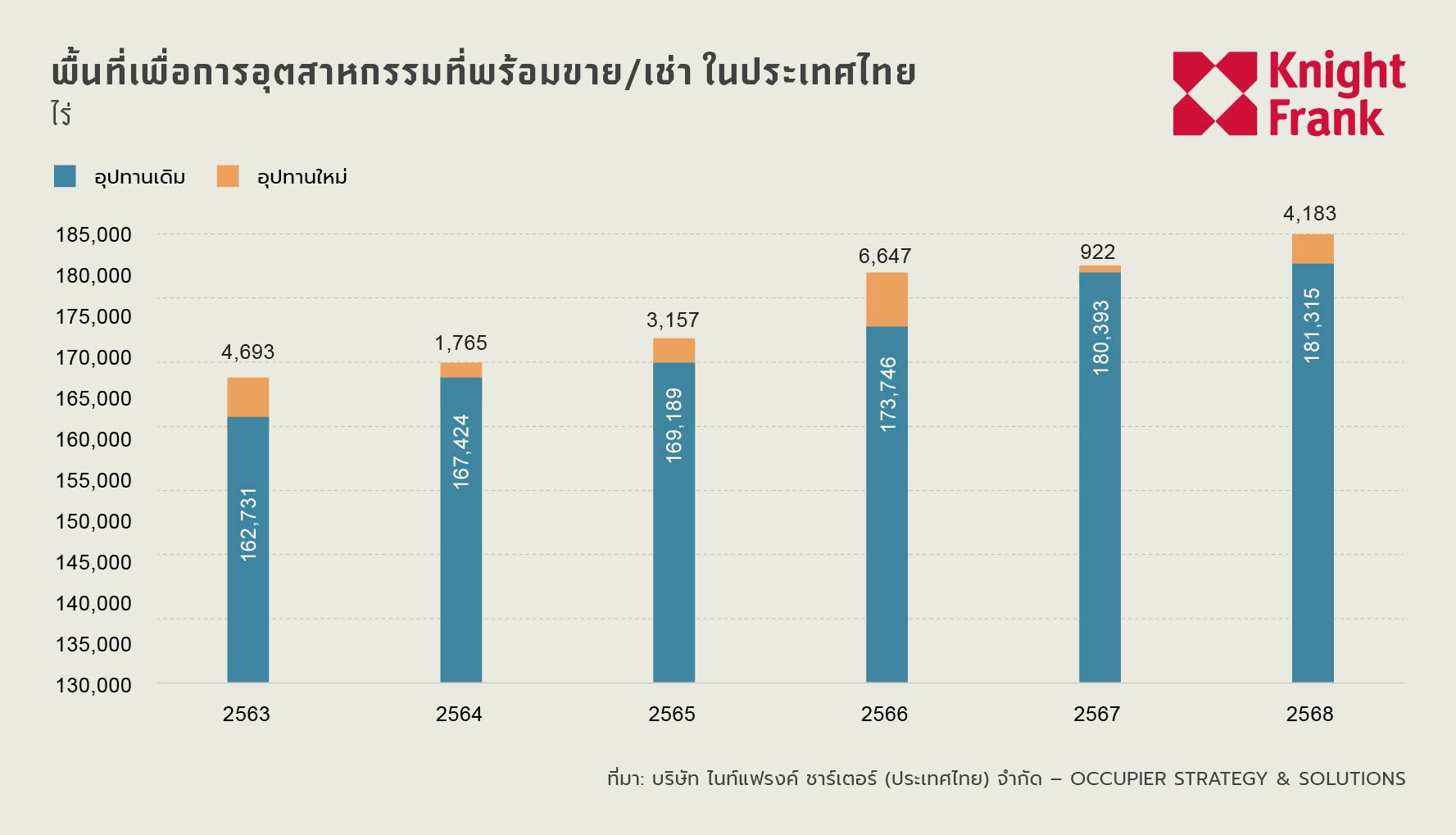

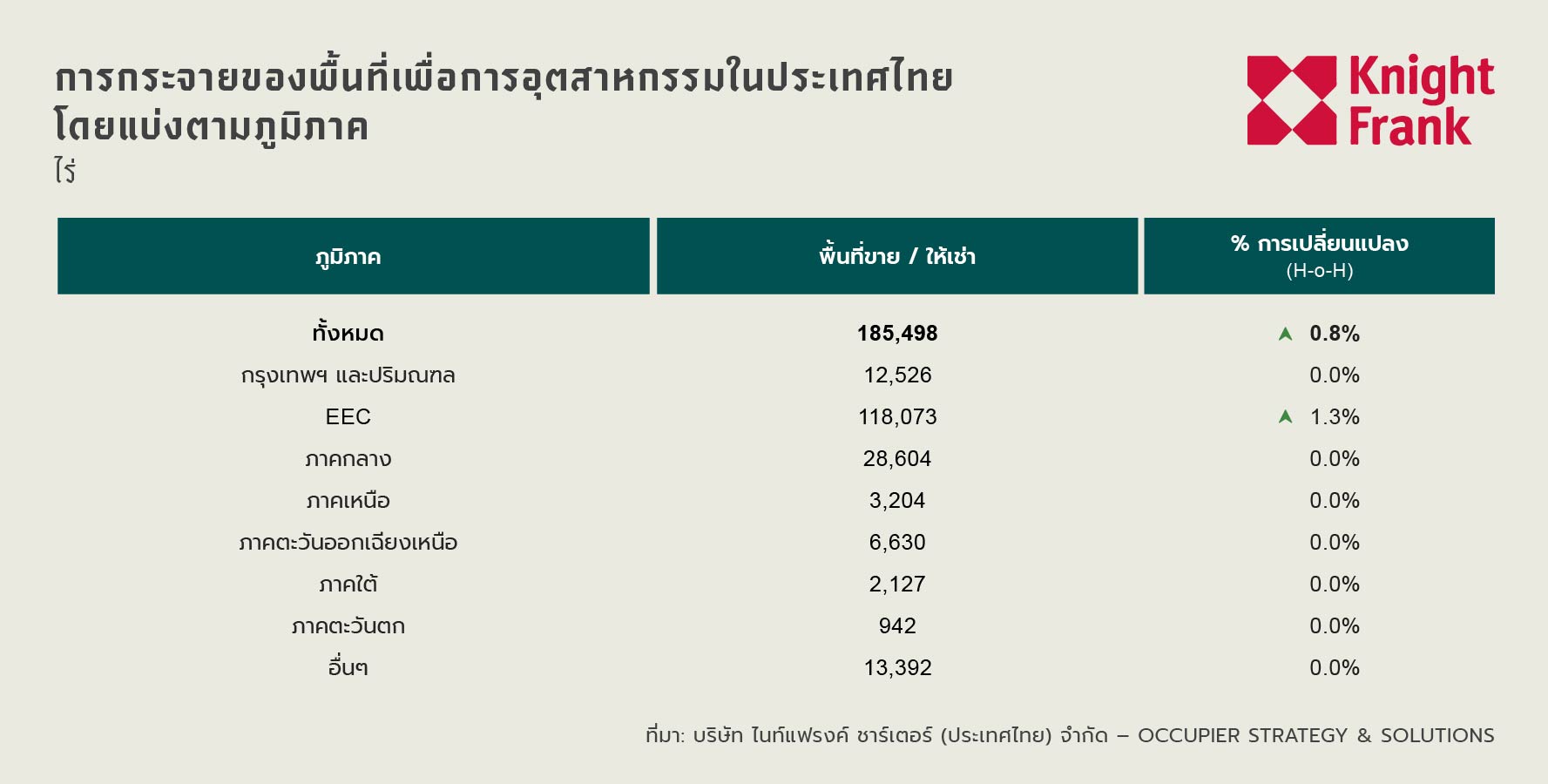

In the second half of 2025 (H2 2025), the total supply of serviced industrial land with utilities available for sale or lease increased by 0.8% compared to the previous half-year (H-O-H) to 185,498 rai. This expansion mainly comes from increased areas in existing industrial estates. However, during this period, several large new projects were launched, with significant projects starting operations in the second half of 2025, including WHA Eastern Seaboard Industrial Estates 4, WHA Industrial Estate Rayong Phase 3, and TFD Industrial Estate Phase 2.

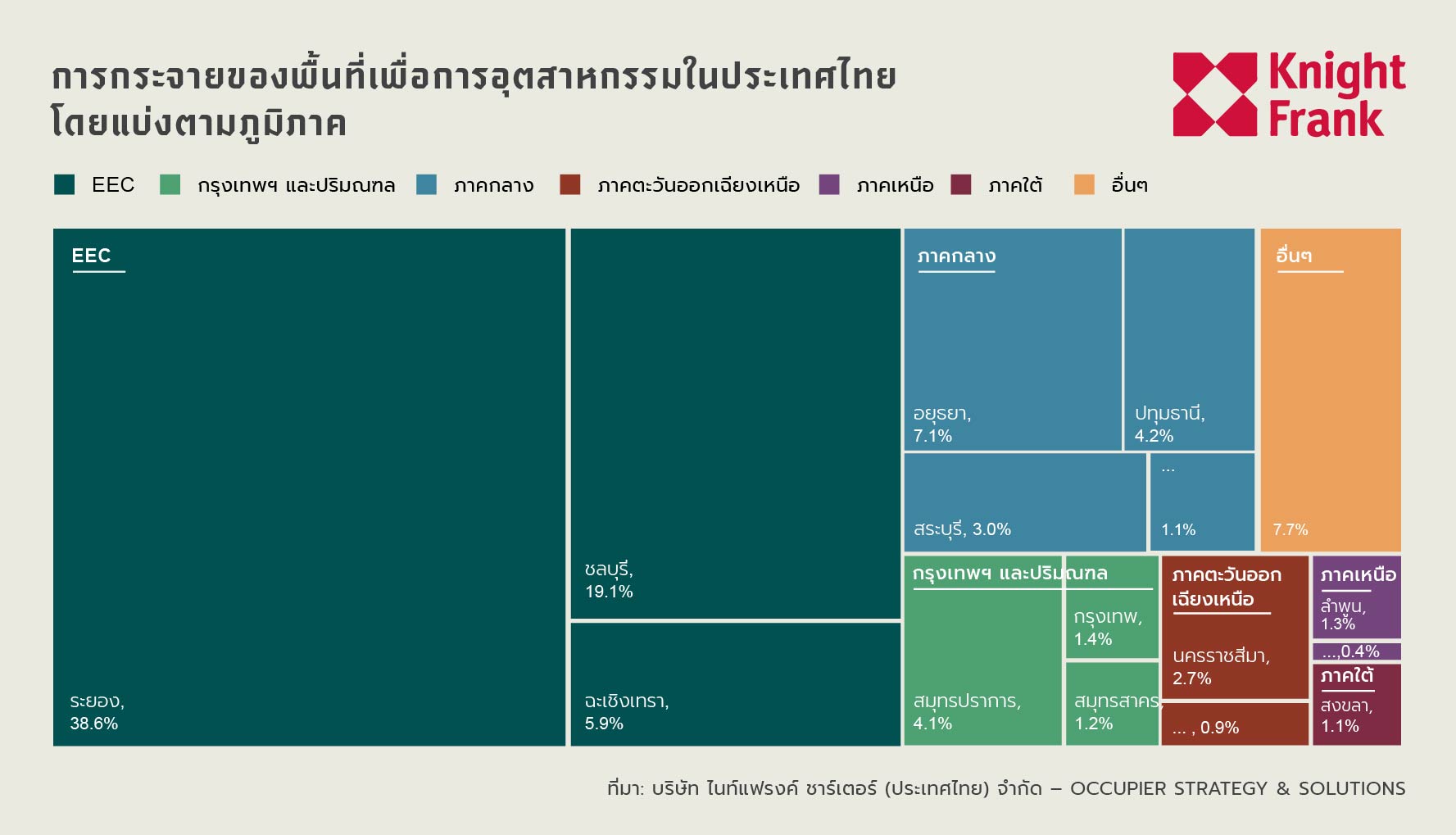

In terms of regional distribution, the Eastern Economic Corridor (EEC) remains the main mechanism of the market, accounting for a high proportion of 63.6% of the national SILP supply by the end of 2025. The total area available for sale in the EEC is 118,073 rai, an increase of 1.3% H-O-H. This growth is driven by increased supply in Rayong and Chachoengsao provinces, which together push the region's performance higher, with Rayong remaining the country's main market with a share of 38.6%, while Chachoengsao has a share of 5.9%. Chonburi province, an important industrial base, maintains a stable supply share of 19.1% throughout this period.

The Central region remains the second-largest market group, accounting for 15.4% of the market, equivalent to 28,604 rai, while the Bangkok Metropolitan Region (BMR) remains strategically important, with a total area of 12,526 rai or 6.7% of the national market. In contrast to the growth in the EEC, supply levels in other regions, including BMR, Central, Northern, Northeastern, Southern, and Western regions, remained unchanged during this period, resulting in a net new supply of only 1,470 rai in H2 2025, reflecting a cautious and selective development approach by project developers, with new investments still concentrated in high-demand locations rather than broad market expansions.

Demand

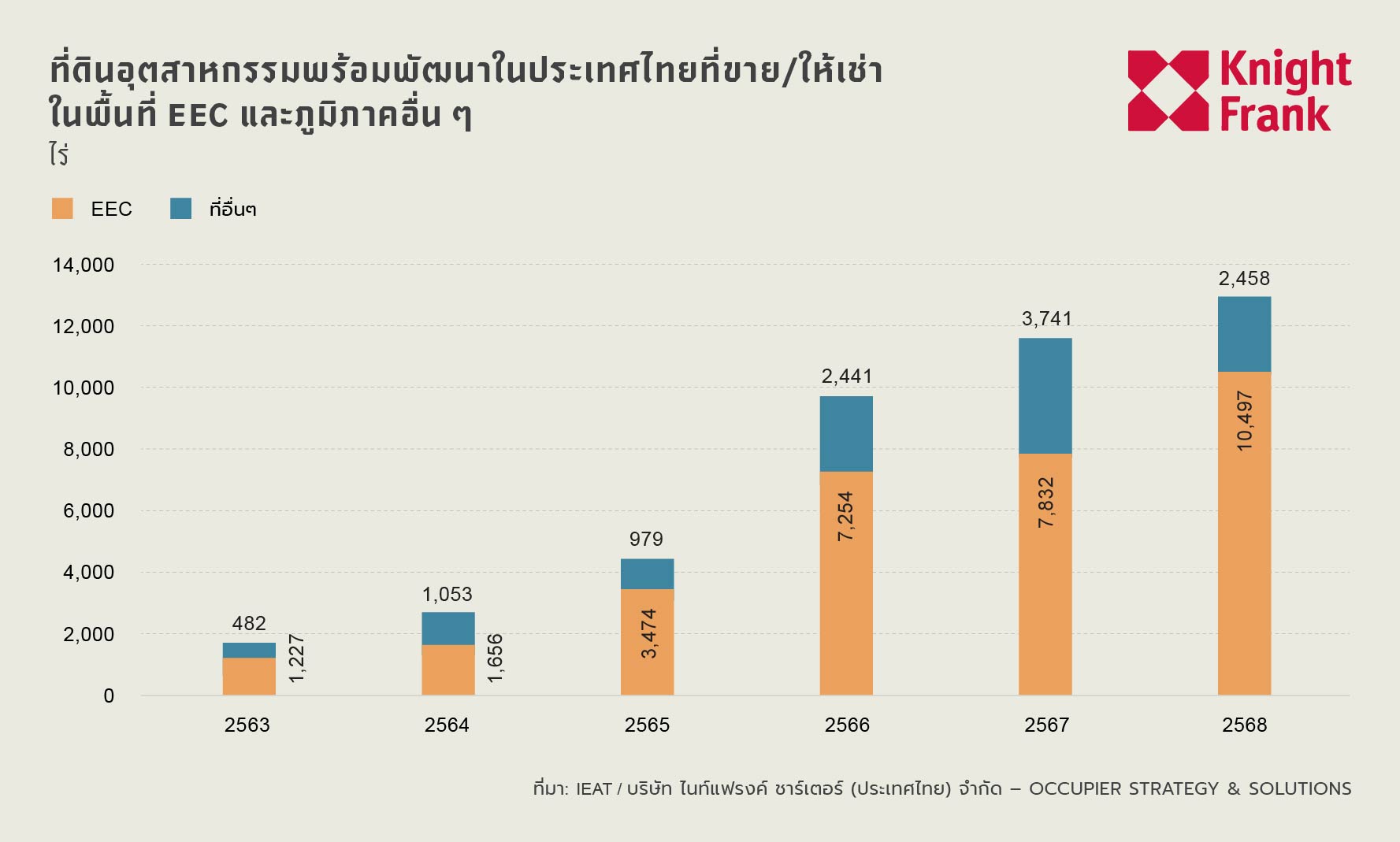

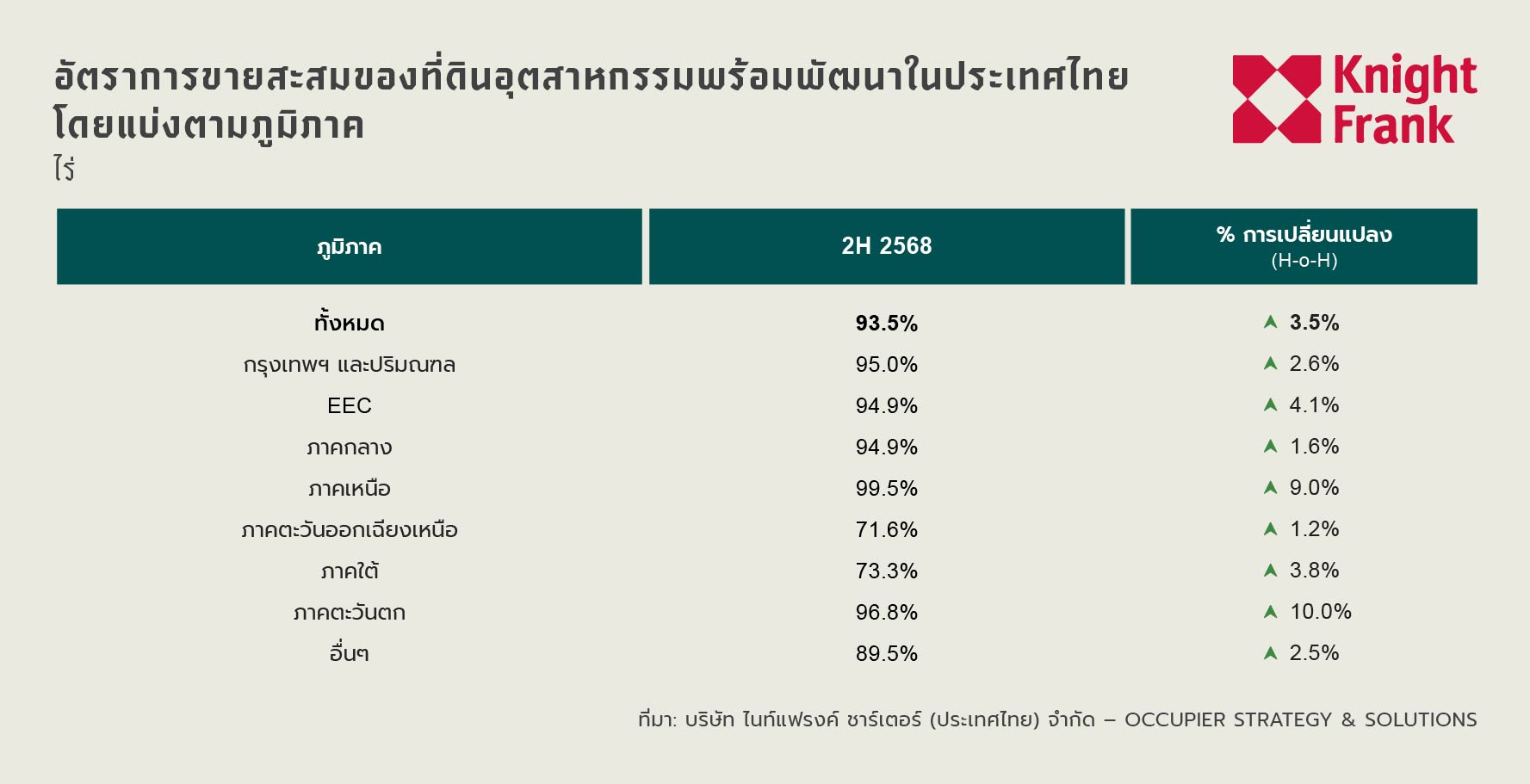

In the second half of 2025, the Thai industrial sector reached a historical peak, with demand for serviced industrial land increasing to unprecedented levels. Total sales and leases for the year surged to 12,955 rai, significantly up from 11,573 rai in 2024. This growth is driven by the Eastern Economic Corridor (EEC), which utilized a total of 10,497 rai.

The strong demand for land absorption this year has pushed the national cumulative sales rate up to 93.5%, reflecting a tight market situation in all regions, particularly in the North, which is approaching full saturation at 99.5% after a 9.0 percentage point increase H-O-H. The West also saw a rapid increase of 10.0 percentage points to 96.8%, while the Bangkok Metropolitan Region, EEC, and Central region all remain at limited levels of around 95%. These figures reflect a significant decrease in remaining space in the country’s main industrial centers. For manufacturing operators, H2 2025 will be a time of intense competition for the remaining space, signaling that the market is nearing full absorption, which may require future expansions to consider secondary areas more.

Asking Prices

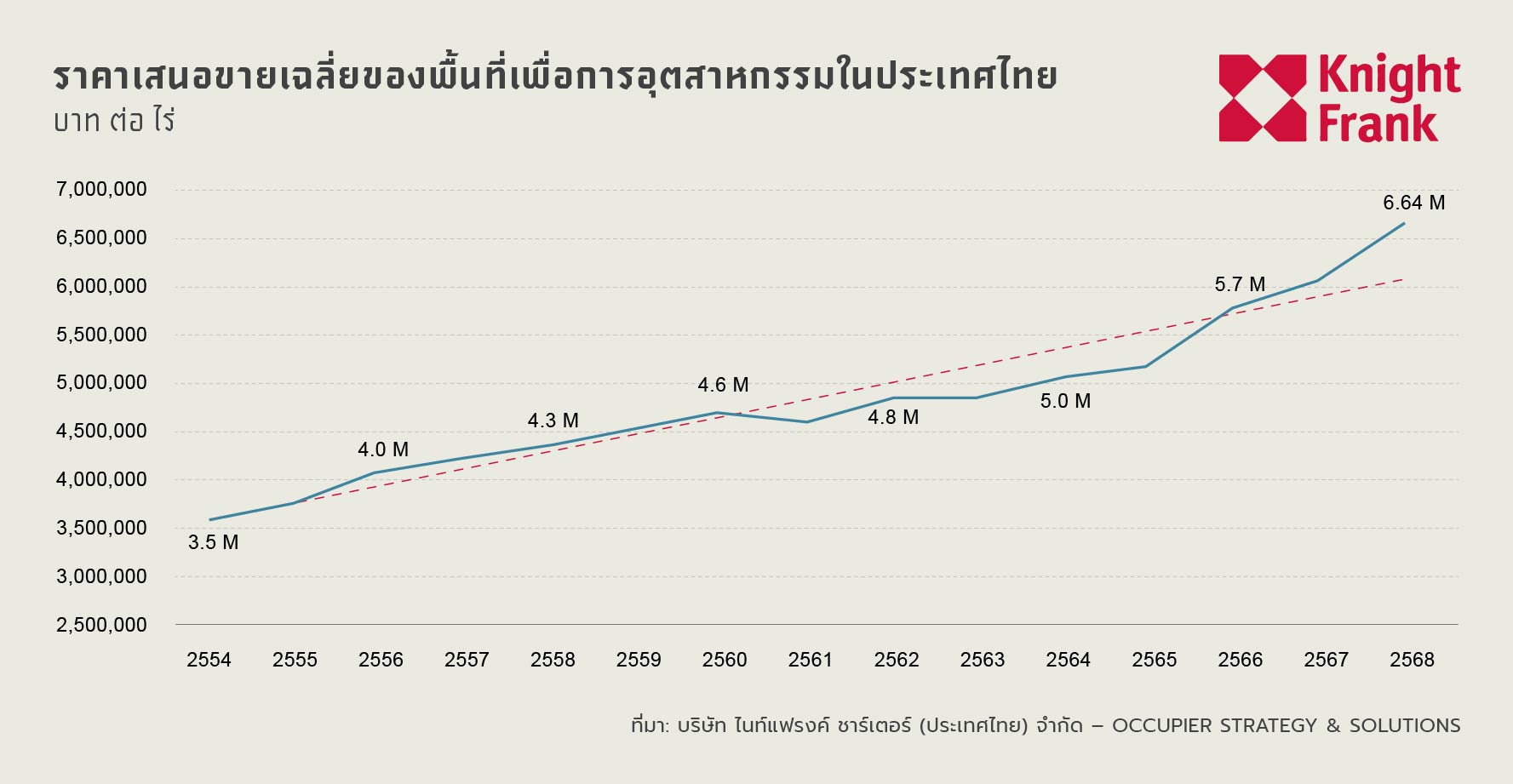

In 2025, the average asking price for serviced industrial land in Thailand is approximately 6.6 million baht per rai, the highest level during the study period, reflecting an acceleration in land price increases during the late cycle, particularly since 2023. Despite a more selective investment environment, the continuous increase in 2025 reinforces the structural strength of demand for well-located industrial land with complete utilities.

In the long term, asking prices have consistently increased since 2011, when the average price was around 3.6 million baht per rai. When calculated in index form, with 2011 as the base year (=100), land values increased to approximately 186 in 2025, reflecting an increase in accumulated capital value of nearly 90% over the past 14 years. This long-term upward trend indicates the effectiveness of land banking strategies and confirms the role of serviced industrial land as a highly flexible asset that can maintain value and generate returns from price increases in all economic cycles.

Market data for 2025 reflects a strong upward trend in serviced industrial land in Thailand, with the average asking price rising to 6.65 million baht per rai, an increase of 9.84% compared to the previous year. This growth is most pronounced in the EEC, where prices surged by 36.18% to 8.18 million baht per rai, while the Bangkok Metropolitan Region remains the highest-value market, with an average price of 14.00 million baht per rai.

When considering the price distribution range, there is a clear valuation premium in central areas, with the Bangkok Metropolitan Region having prices as high as 16.0 million baht per rai, while the EEC shows a wide price range from 4.8 million to 15.0 million baht per rai, reflecting diverse opportunities for long-term capital appreciation. For investors, these figures confirm that acquiring strategically located land in Thailand's main industrial centers continues to offer high value growth potential, along with strong risk-adjusted returns.

Ready-Built Factories (RBF) Supply

Supply

In the second half of 2025 (H2 2025), the ready-built factory market saw only a slight supply expansion of approximately 11,000 square meters, as project developers continued to adopt a cautious strategy despite high demand. This limited growth reflects a shift towards constructing only on a case-by-case basis with pre-leased tenants, resulting in a national occupancy rate increasing to 98.4% and creating a highly tight market situation in Thailand's main industrial areas.

The Eastern Economic Corridor (EEC) remains the main industrial hub, accounting for 47.7% of total net leased area, followed by the Central region and the Bangkok Metropolitan Region, with shares of 26.3% and 26.1%, respectively. The Bangkok Metropolitan Region is the only area with increased supply during this period, due to the completion of ready-built factories totaling 11,000 square meters in Samut Prakan province, while other regions saw no changes in supply volume. This distribution reflects the continued concentration of available industrial space in the country’s main logistics corridors.

Demand

The ready-built factory market reached a significant turning point in the second half of 2025, with available space in the main centers being nearly fully absorbed. The national occupancy rate reached a record high of 98.4%, driven by a strong inflow of foreign direct investment across various industrial sectors.

Regionally, the Eastern Economic Corridor (EEC) approached near-full utilization at 99.94%, leaving almost no ready-built factory space available for new operators. Meanwhile, the Bangkok Metropolitan Region and Central region had occupancy rates exceeding 96% and 97%, respectively. Given that total supply remained stable at approximately 3.3 million square meters, project developers are increasingly turning to Built-to-Suit models, constructing factories only after securing long-term lease agreements. The imbalance between demand and supply at the end of 2025 has put significant upward pressure on rental rates, reinforcing the “Landlord’s Market” that will continue into the following year.

Rental Rates

The severe supply shortage has pushed the average rental rate for ready-built factories up to 202.9 baht per square meter, an increase of 1.73% compared to the previous year. Regionally, the EEC has the highest rental rate at 217.1 baht per square meter, due to near-full utilization. The Central region follows at 193.0 baht per square meter, while the Bangkok Metropolitan Region stands at 186.8 baht per square meter. This rental increase clearly reflects the landlord market conditions, with demand from the electric vehicle (EV) and electronics sectors growing faster than the available ready-built factory space.

Market Analysis and Outlook

The Thai industrial real estate market in the second half of 2025 is no longer driven solely by traditional manufacturing relocations but is undergoing a deep restructuring towards high-investment industrial activities that rely more on infrastructure and are spatially concentrated. Trade policies, particularly differences in tax rates in the U.S. market, have become a key catalyst for this transition, occurring amid a macroeconomic context of slowing growth, with GDP growth dropping to around 1.2% compared to the same period last year in Q3 and a decline in inventory reflecting cautious producer behavior, yet with preparations in place.

Tax measures are not only changing the direction of production flows but are also altering the design of supply chains and production structures of multinational companies. Under the risks of tariffs, rules of origin, and policy uncertainties, multinational corporations are likely to choose to invest in fewer but larger and more technically specialized projects instead of expanding numerous factories. This trend helps explain the simultaneous occurrence of record-high land absorption, near-full occupancy rates, rising prices, and a decrease in the number of factory licenses, which is not a contradiction but a sign of the transition from a phase of quantitative expansion to one driven by investment efficiency and asset quality.

In terms of industry, this trend is evident in the electronics, digital infrastructure, electrical and energy equipment, and advanced materials sectors, while traditional industries such as automotive and petroleum still show weaker momentum.

On the supply side, project developers are responding to uncertainties similarly by reducing speculative development and focusing on post-contract construction and Built-to-Suit projects, resulting in a structural decrease in supply flexibility, even as underlying demand remains strong. Thus, the tight market situation arises more from supply constraints than from strong demand.

This trend is reflected in land sales and occupancy rates nearing record highs, with national industrial land sales in 2025 exceeding 12,955 rai and occupancy rates for ready-built factories approaching full utilization.

The Eastern Economic Corridor continues to be the center of this transition, as it can meet the infrastructure, regulatory, and logistics needs that modern investments require. However, the near-saturation condition of the EEC is beginning to function not as a growth engine but as a filter for investments, with capital flowing only to high-quality assets and locations, further widening the gap between premium areas with ready infrastructure and older or less serviced areas. At the same time, we are beginning to see a selective distribution of demand to the Central and Western regions, while peripheral markets remain sluggish.

Looking ahead, industrial demand is likely to remain strong but will be more selective due to the ongoing distribution of supply chains, the transition to digitalization, and energy investments. The main risks in the market are no longer related to economic slowdown but to long-term structural constraints, particularly regarding energy, infrastructure readiness, permitting processes, and policy stability, which may limit actual supply even as demand remains.

Therefore, the growth of land and rental prices is likely to continue, but it will not be uniform, reflecting scarcity and quality differences rather than broad increases. The market is entering a phase where asset quality, strategic positioning, and project execution risks are more important than size, while the risks of misallocating investments may be more significant than vacancy rate risks, as evidenced by current pricing patterns where value increases are concentrated in well-located assets with ready infrastructure, reflecting quality and characteristic premiums rather than equal increases across the market.

Marcus Berthenshaw Partner – Head of Industry Strategy & Solutions, Knight Frank Thailand commented: "What we are witnessing is not a slowdown in the Thai industrial market but a deep restructuring of the market. Investment is moving towards a model that requires higher investment per project, relies more on infrastructure, and is more selective. The difference between record land absorption and the reduced number of new factory licenses reflects the transition from quantitative expansion to an allocation of investment focused on asset quality."

As multinational companies restructure their supply chains to respond to the imbalances of tax measures and trade policy uncertainties, Thailand is emerging as a key strategic point for advanced manufacturing, digital infrastructure, and energy industries. However, the market is entering a more disciplined phase, where the decisive factors in investment decisions are no longer the size of the project but the quality of the asset, the readiness of the electrical system, and logistics potential.

Looking ahead to 2026, demand is expected to remain strong, but competition will intensify for truly well-supported infrastructure locations. The main risks in the market are not related to vacancy issues but to project execution capabilities and supply constraints, particularly regarding electricity generation capacity, permitting processes, and policy stability, all of which reflect that the Thai industrial real estate market is entering a new cycle characterized by more institutional features and focusing on asset quality as the core.”