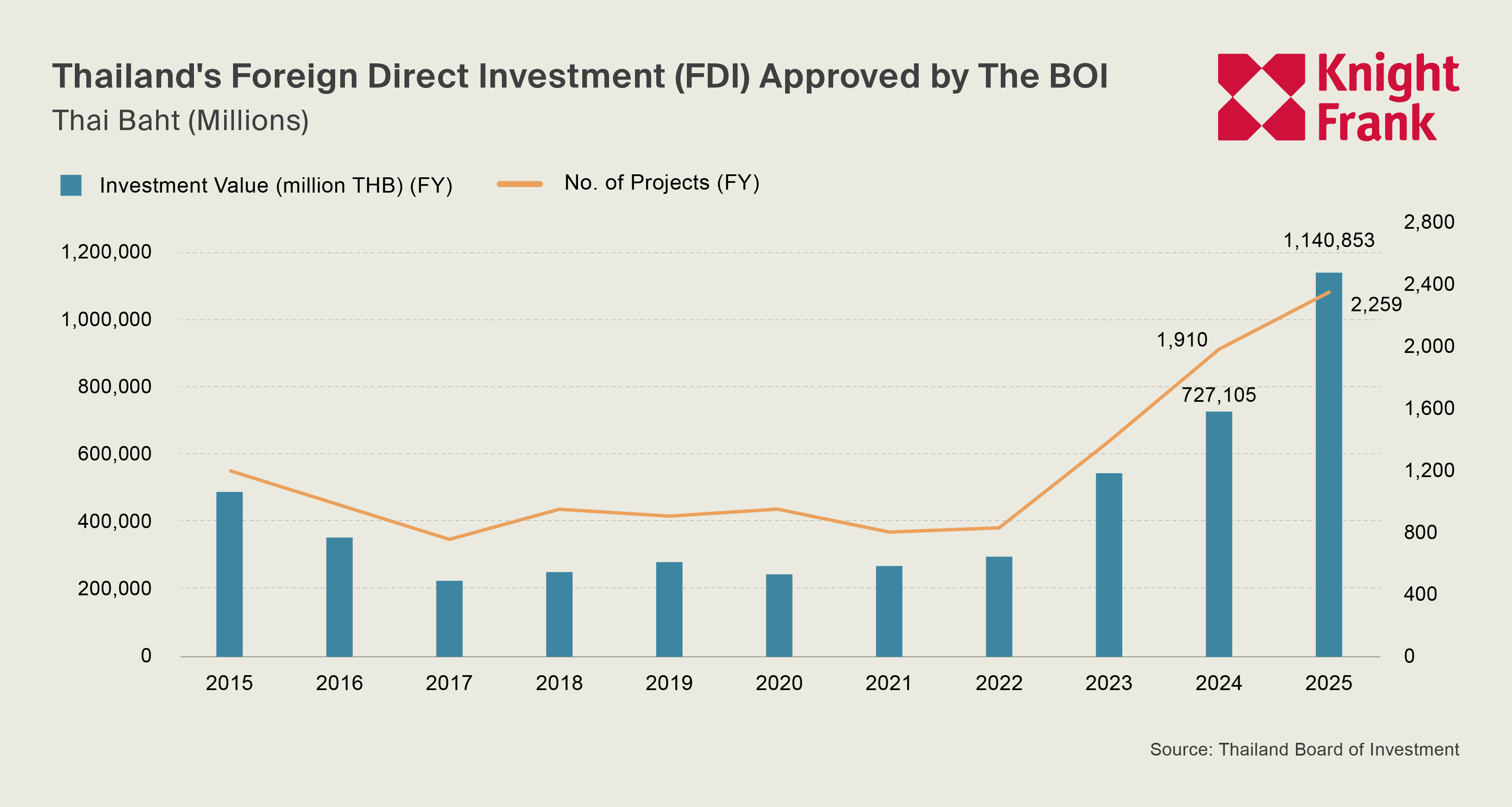

The Aftermath of the Trade War Accelerates FDI Inflows into Thailand, Reaching 1.14 Trillion Baht as EEC Approaches Saturation

The manufacturing and industrial real estate market in Thailand is entering a new structural phase in the second half of 2025, characterized by record-high foreign direct investment (FDI), unprecedented absorption of industrial land, and near-full utilization of ready-built factory space, according to the latest Manufacturing Market Report for the Second Half of 2025 by Knight Frank Thailand.

Despite a slowdown in macroeconomic momentum, with real GDP growth dropping to 1.2% compared to the same period last year in Q3 2025, Thailand's industrial sector continues to outperform the overall economy, driven by strong foreign demand, a consistent trade surplus, and a rapid restructuring of supply chains amid the global trade context and international tax measures.

FDI Reaches 1.14 Trillion Baht, with Digital Investment as the Main Driver

By the end of 2025, Thailand has accumulated 1.14 trillion baht in foreign direct investment promoted by the BOI, covering 2,259 projects. Notably, in the second half of the year, the number of projects increased by 1,196, with approved investment value rising by 413.8 billion baht. Meanwhile, the average investment value per project has increased to approximately 505 million baht, reflecting a clear transition towards larger and higher-capital investments.

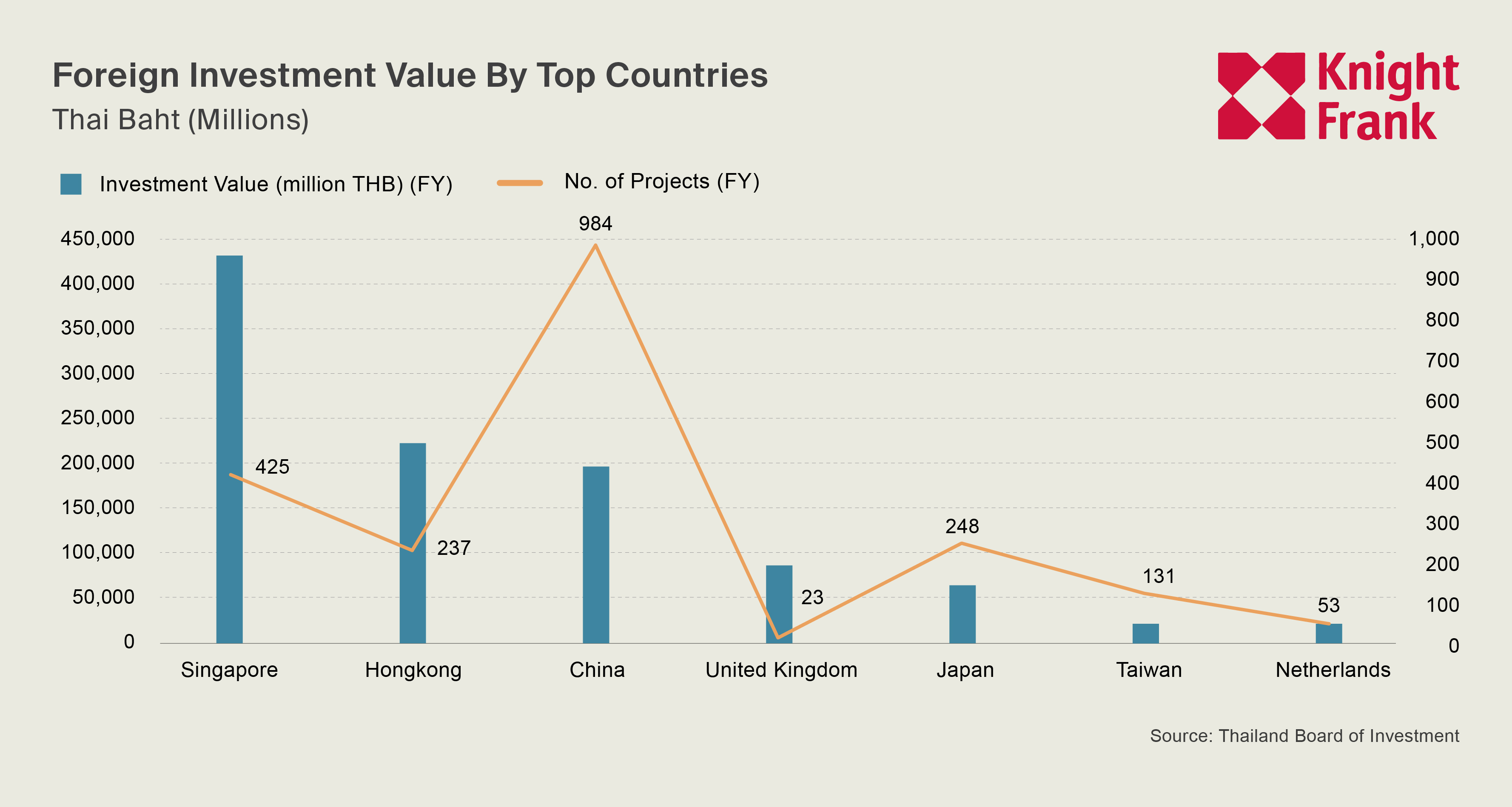

Geographically, Singapore remains the largest source of foreign investment in Thailand, with an investment value of 433,019 million baht, followed by Hong Kong and China, with China having the highest number of investment projects at 984. Meanwhile, investors from Western countries and regional nations, such as the UK, Japan, and the USA, continue to play a significant role, reflecting global investor confidence. This trend indicates a shift towards high-value digital and electronic infrastructure and Thailand's emergence as a strategic hub for advanced manufacturing and information services in the region.

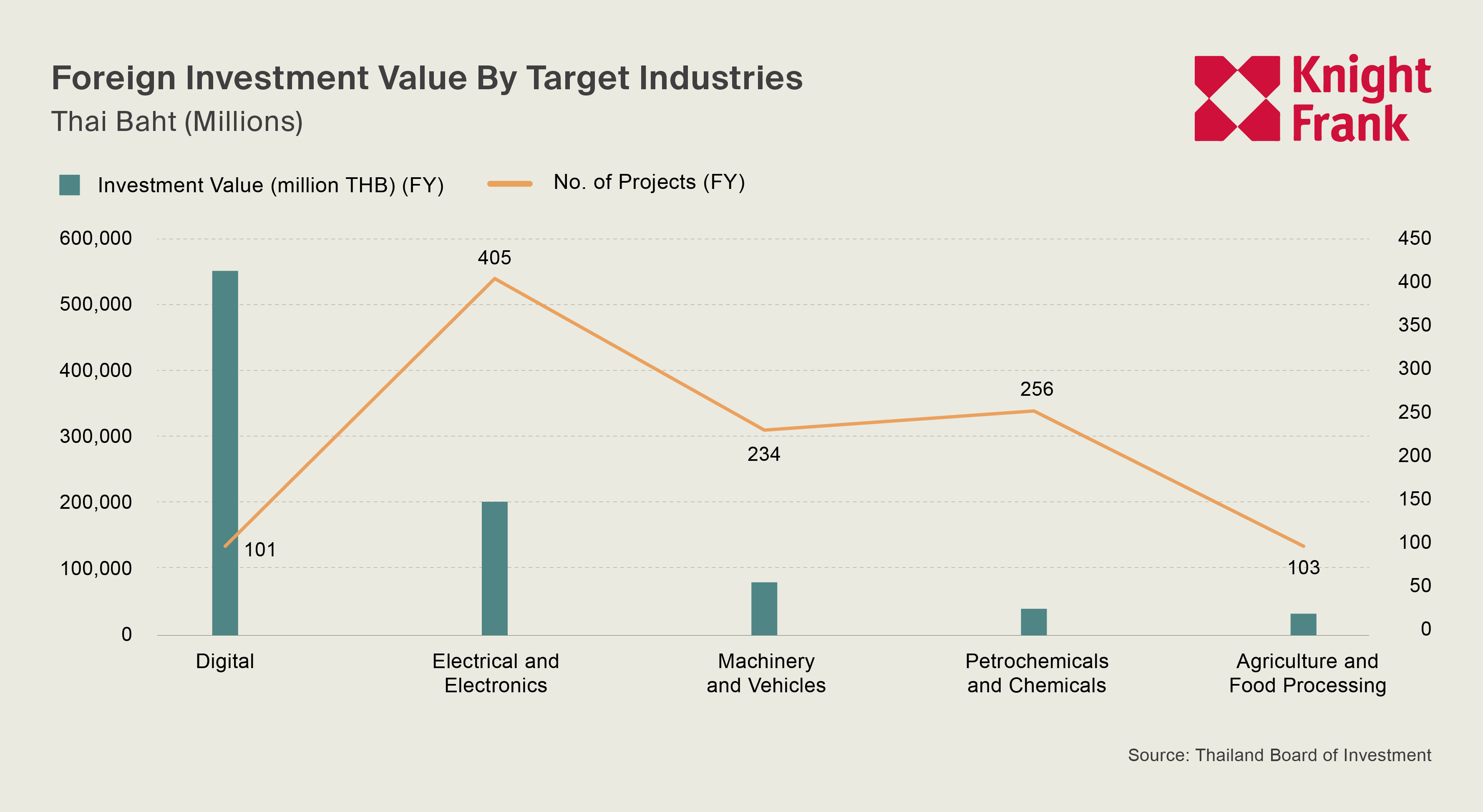

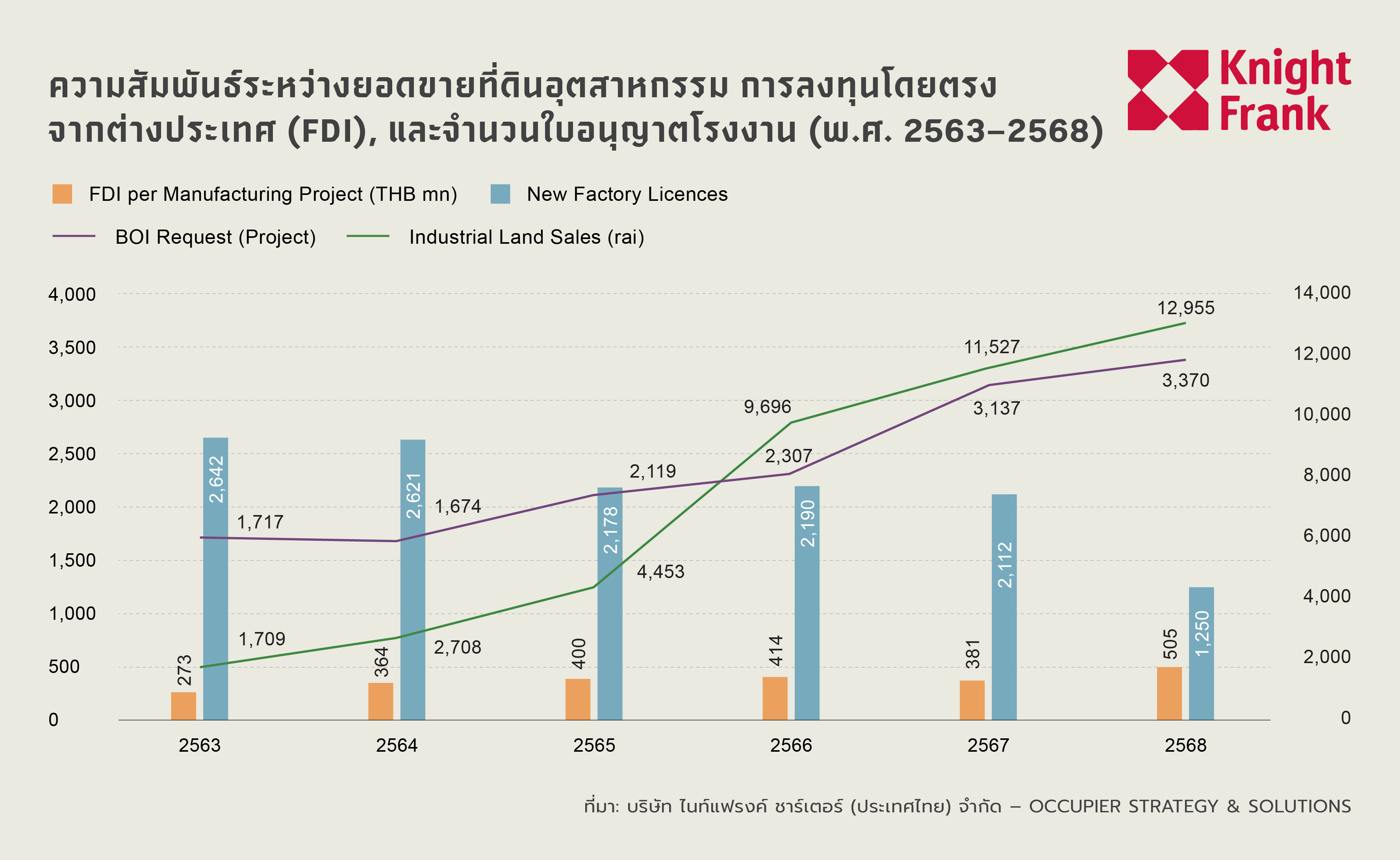

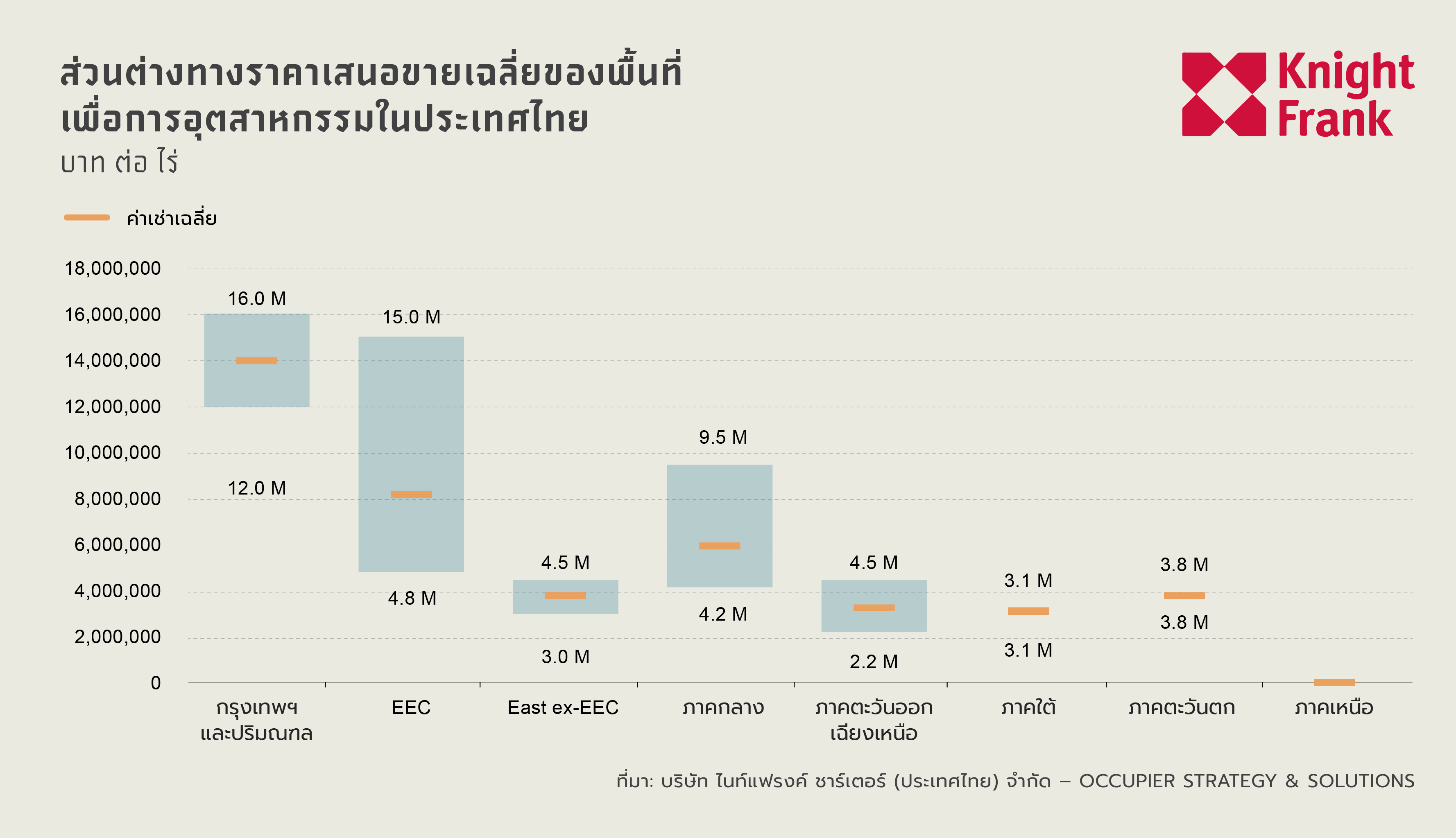

The industrial landscape in Thailand is transitioning towards fewer but larger and higher-capital investments, with industrial land absorption rapidly increasing from 4,684 rai in the first half of 2025 to 12,955 rai by the end of the year. The average FDI value per project has risen to approximately 505 million baht, reflecting a focus on high-value investments, even as the number of new factories declines.

This trend is most evident in the digital industry, alongside the continuous expansion of the electrical and electronics sector, driven by demand for advanced components related to AI technology and data storage systems. Meanwhile, investments in machinery and automotive sectors are focused on upgrading production capacity and improving efficiency rather than developing new projects.

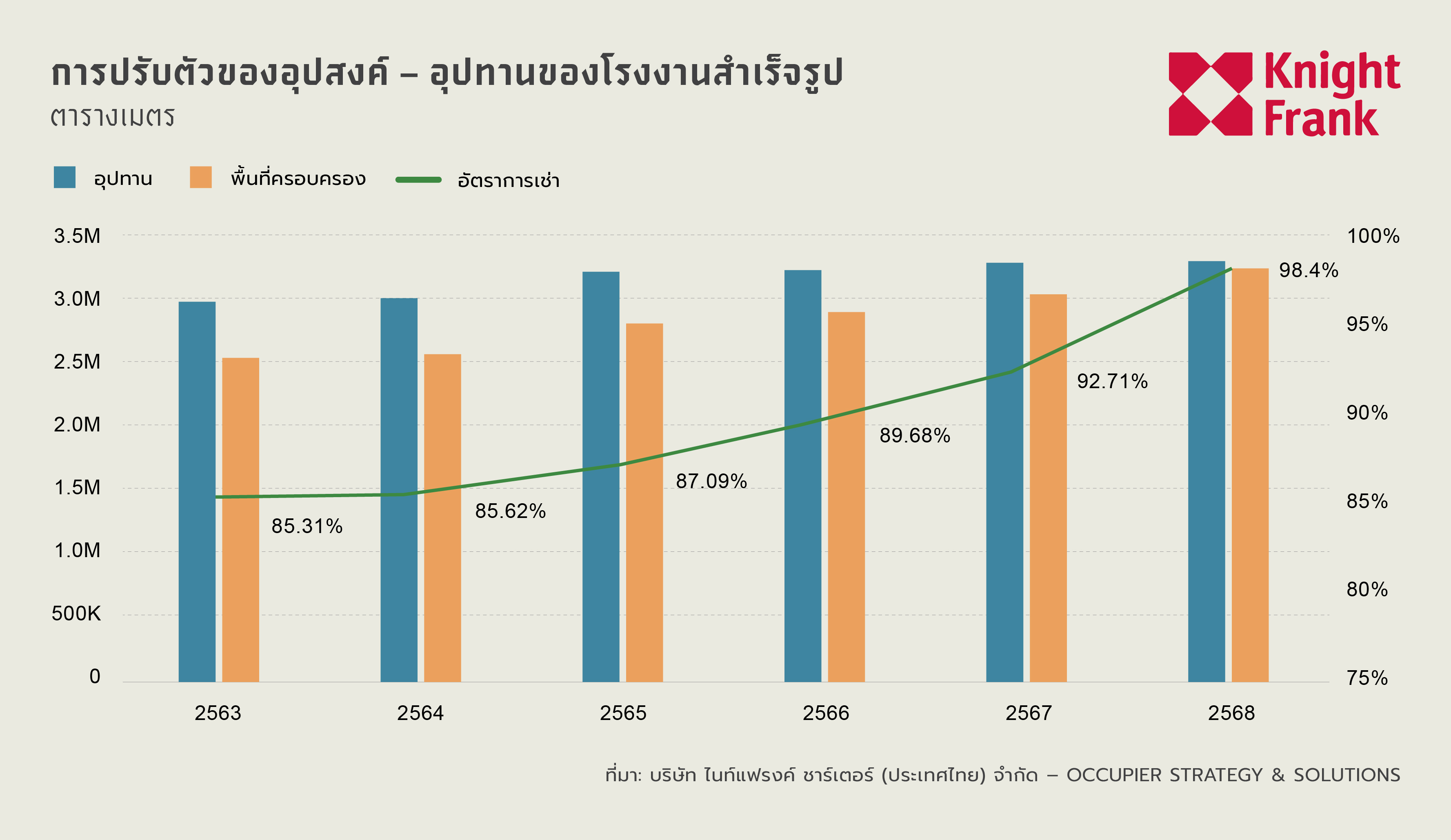

At the same time, the number of new factory licenses has decreased to approximately 1,250 in 2025, reinforcing the transition from quantity-driven development to high-quality large-scale projects requiring significant investment, particularly in digital infrastructure, which often demands substantial land and capital but does not necessarily require traditional factory licenses. This has allowed for increased land absorption and FDI inflows, even as the number of factory licenses declines.

Demand for Industrial Land Soars to Historic Highs

The demand for serviced industrial land plots (SILP) has surged to unprecedented levels in 2025, with total sales and leases reaching 12,955 rai, significantly up from 11,573 rai in 2024. The Eastern Economic Corridor (EEC) accounts for a substantial 10,497 rai of land usage, underscoring the area's role as a key mechanism for Thailand's industrial sector.