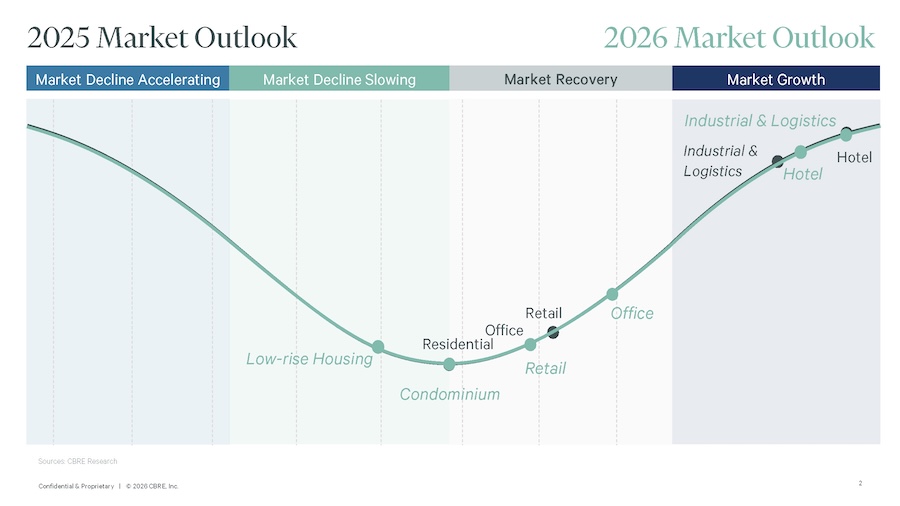

Trends in the Thai Real Estate Market for 2026: Strategies for Balancing 'Risk and Return' in a Changing Market

CBRE Thailand, a leading global real estate consulting firm, has released its comprehensive report on the trends in the Thai real estate market for 2026. CBRE predicts that this year will require project developers and investors to strategically balance 'risk and return' amidst a market environment that remains highly uncertain.

"The Thai real estate market continues to evolve, which means that property developers must plan strategically and be agile in their investments and developments," said Ms. Rungrat Veerapakarnkun, Managing Director of CBRE Thailand. "Our analysis indicates that while some sectors still face pressure, others are well-positioned for strong growth, supported by changing consumer behaviors, government stimulus measures, and global trends. Therefore, adaptability and innovation are key to success."

Retail Market: Focus on Creating Experiences to Cater to Cautious Consumers

In the retail market in Bangkok, which ranges from large shopping centers in the city center to projects targeting surrounding residents, developers continue to invest in new projects and upgrade existing ones to meet the evolving lifestyles of consumers.

However, in 2025, the total retail space reached 8.25 million square meters, with an additional 300,000 square meters expected to be completed in 2026. It is anticipated that the increase in new retail space will outpace tenant demand, resulting in an average occupancy rate dropping below 90%.

Approximately 75% of this new retail space will be concentrated in the outskirts of the city center (midtown) and suburban areas, shifting the competitive landscape towards residential neighborhoods where consumers tend to be more price-sensitive.

Ms. Chotika Thangsirithap, Head of Project Development Consulting and Market Research at CBRE Thailand, noted that "The interest of foreign brands in Bangkok, particularly in the food and beverage (F&B) and fashion sectors, underscores the city's attractiveness as a destination for experiential spending. In 2025, the largest share of new foreign brands entering the market came from China (20%), followed by Japan and Europe (18% each)."

Hotel and Service Business Market: Competition Accompanied by Niche Growth

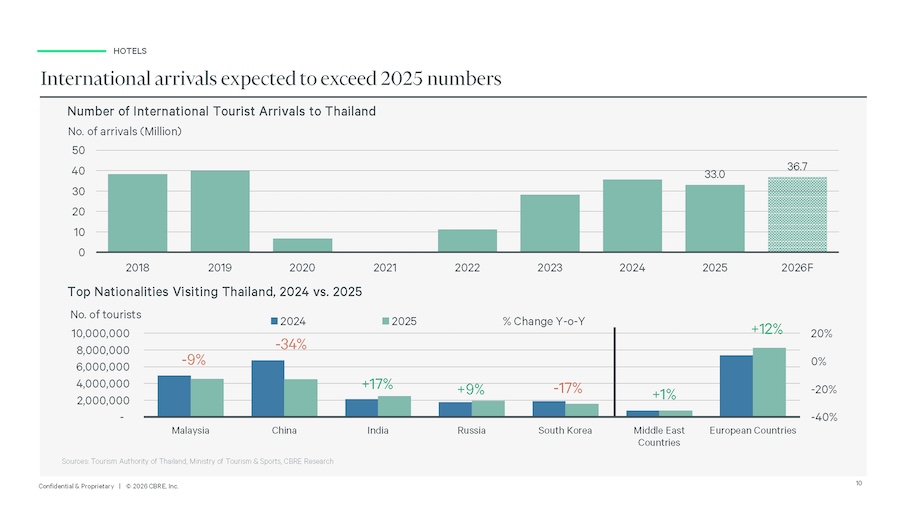

Although 2025 was a challenging year with fewer than 33 million international tourists, Thailand still has strong potential to attract visitors seeking medical treatment, wellness services, and leisure, provided that conditions stabilize and the tourism atmosphere improves.

Thailand has high potential to attract high-spending tourists in the expanding medical, wellness, and MICE (Meetings, Incentives, Conventions, and Exhibitions) markets. Additionally, building confidence in safety and providing valuable experiences for short-haul international tourists will also be crucial. The Tourism Authority of Thailand (TAT) has projected the number of tourists to reach 36.7 million, with these factors being key to achieving this goal.

"In 2026, Bangkok is expected to see an increase of over 4,300 hotel rooms, primarily in the upscale and luxury segments, although midscale accommodations will still account for the largest share at 43%. The influx of new rooms will intensify competition but is expected to positively impact occupancy rates, projected to grow by up to 2 percentage points, and average revenue per available room (RevPAR) is expected to increase by 3-4%. However, the increase in average daily rates (ADR) from sold rooms may be somewhat limited due to new supply, a strengthening currency, and regional competition. Nevertheless, the rise of upscale and luxury projects is likely to benefit the overall ADR," Ms. Chotika added.

Hotel operators are now focusing on metrics beyond just occupancy rates and ADR, shifting towards diversifying revenue streams through expanded service offerings and more efficient cost management.

Condominium Market: Emphasis on Quality Over Quantity

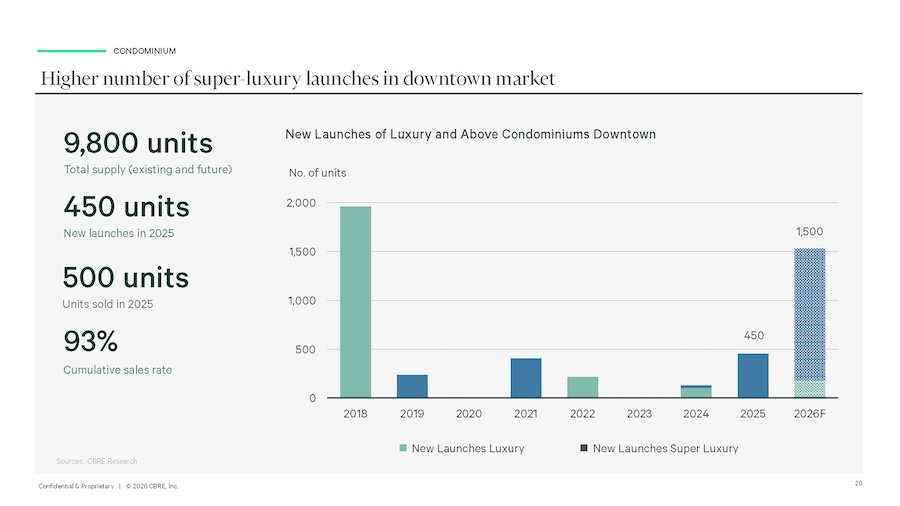

The balance between risk and return in the condominium market is expected to continue in 2026. Ms. Rungrat stated, "CBRE anticipates an increase in new luxury and super-luxury projects, supported by a high sales rate of 93% of the current total supply. The new projects are likely to highlight distinct features, branded residences, and unique selling points. The average selling price of condominiums in the city center is expected to rise by up to 15% compared to the previous year due to the launch of more super-luxury projects, which prioritize privacy and exclusivity along with superior amenities and services."

Meanwhile, the midtown and suburban markets continue to face high rejection rates for loans, prompting developers to focus on launching new projects in locations with clear demand drivers, such as transportation hubs, near educational institutions, and hospitals. These areas can attract both end-users and investors. Additionally, fierce competition from large projects emphasizing value in the affordable segment may lead to an average selling price decrease of up to 10% compared to the previous year.

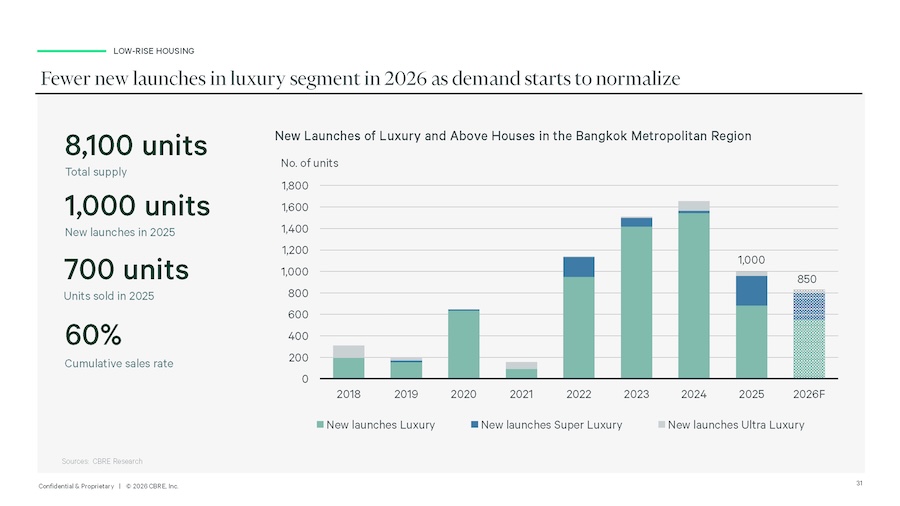

Low-rise Residential Market: Cautious Project Development Amid Rising Unsold Inventory

As the number of unsold low-rise residences increases, developers must carefully assess market demand before launching new projects. Due to various uncertainties, buyer confidence remained low throughout 2025, leading developers to remain cautious and wait for signs of market recovery. The number of new land allocation permits for residential projects in Bangkok and its vicinity dropped by 30% in 2025, reflecting low confidence among developers.

"The second-hand home market has noticeably picked up, primarily due to clearer intentions from buyers and better chances of securing loan approvals, along with fewer new projects in the lower market segment. Additionally, the self-built home market remains an important sub-market influencing overall housing demand. The launch of low-rise projects in the luxury and high-end segments will become more selective, limited to experienced developers, and will involve phased launches to assess actual demand and buyer confidence in the market," Ms. Chotika added.

Office Market: Flight-to-Quality Trend Boosts Rental Growth in Premium Buildings

The office market in 2026 will remain vibrant, with tenants continuing to benefit from a tenant-friendly market. The "Flight-to-Quality" trend is clearly evident, as many tenants move to newer, higher-grade office buildings, resulting in increased occupancy rates in the best A+ grade buildings. This allows building owners to raise rents and widens the rental gap between premium buildings and older ones.

With limited new office space expected to enter the market over the next four years, many building owners are accelerating asset enhancement plans. Well-improved buildings with attractive rents located in prime business districts will become key magnets for office relocations. Given the limited new supply, occupancy rates in premium buildings are expected to improve.

For net take-up demand in 2026, it is expected to be slightly lower than in 2025, at around 100,000 square meters. CBRE's analysis in 2025 revealed that 95% of office relocations were for upgrading to higher-quality buildings or moving to the same grade, and this trend is expected to continue.

"In 2026, the best new A+ grade office buildings located in prime locations with occupancy rates exceeding 80% may see slight rent increases of up to 3% compared to the previous year. In contrast, rents in older office buildings, even with good management, will continue to decline before stabilizing by year-end. Older buildings that are poorly managed or not improved will continue to face declining occupancy rates and lower rents," Ms. Rungrat added.

Industrial and Logistics Space Market: Continuous Growth with Changing Demand

The industrial space market continues to perform strongly, with CBRE forecasting that 2026 will be another active year for industrial land transactions, driven by high pre-booking levels and ongoing government support. However, CBRE expects demand for serviced industrial land plots (SILP) to normalize in 2026 after experiencing significant growth for four consecutive years, influenced by external factors such as geopolitical tensions and uncertainties in U.S. policies, which may slow Thailand's export growth. "Nevertheless, regional trade growth will encourage companies to relocate their production bases to Southeast Asia, including Thailand," Ms. Chotika stated.

The increasing demand for ready-built factories (RBF) supports new supply chains among second- and third-tier suppliers, as well as established companies looking to expand production capacity. The low vacancy rate (below 5%) and limited new supply will continue into 2026.

The modern logistics property market (MLP) remains dominated by large developers, with most new supply being built on a pre-lease or build-to-suit basis for tenants, while speculative spaces are primarily from new developers both domestic and international. CBRE predicts that in 2026, the volume of new space will exceed current demand, leading to an increase in the vacancy rate from 10% to 13%.

"Overall, the trends in the real estate market vary across sectors, but geopolitical stability and improved economic adaptability will be the two most important factors positively impacting the market atmosphere in 2026," Ms. Chotika concluded.