Real Estate Public Company Performance in 2024 Contracts with Economic Conditions

Companies have been gradually announcing their performance for the year 2024, especially the major players in the stock market, who have now fully disclosed their results. Most have reported a decrease in total revenue compared to the same period in 2023. However, there are several companies that have seen an increase in total revenue compared to the previous year, contrary to the growth trend of the housing market in 2024. The Real Estate Information Center reported that the total value of property transfers for the entire year of 2024 decreased by approximately 6.3% from 2023 due to various negative factors affecting the decision to purchase housing, including difficulties in obtaining housing loans as financial institutions have tightened their credit approval processes. This has resulted in a decline in both the number and total value of property transfers in 2024, prompting most operators to seek continuous revenue generation throughout the past year.

Mr. Surachet Kongcheep, Head of Research and Consulting at Cushman & Wakefield Thailand believes that most operators in the stock market experienced a total revenue decline of more than 15% in 2024 compared to 2023. However, some operators have reported either a slight increase or a minimal decrease of about 2-3%, indicating that there is still purchasing power in the housing market. It depends on which operators can reach and attract buyers to reserve and transfer ownership more effectively.

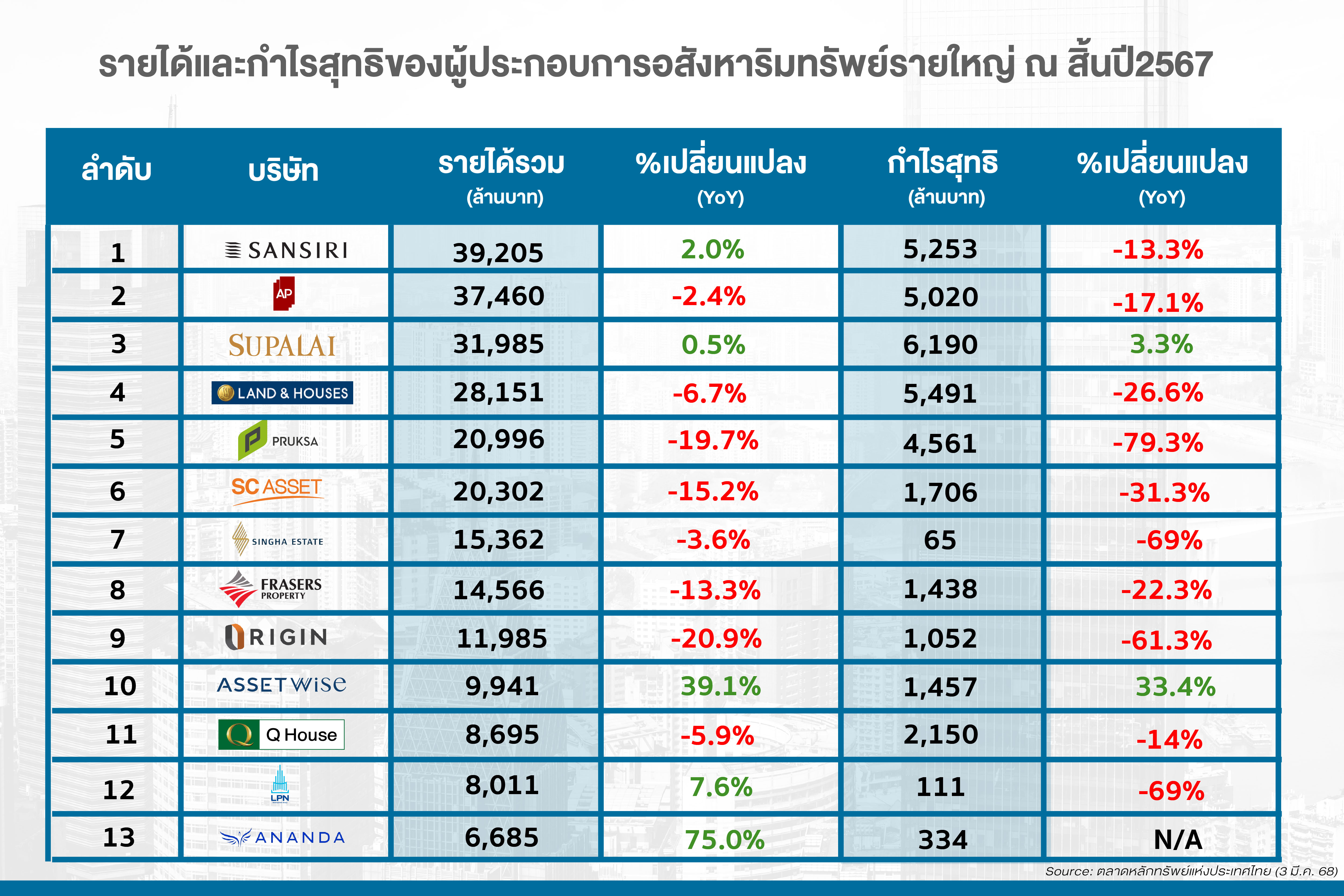

As for the top 5 operators with the highest revenue in 2024, Sansiri reported a total revenue of approximately 39.204 billion baht, an increase of about 2% from 2023, followed by AP (Thailand) with a total revenue of approximately 37.460 billion baht, and Supalai with about 31.985 billion baht. Land and Houses reported a total revenue of 28.151 billion baht, while Pruksa had a total revenue of 20.996 billion baht. These top five companies have consistently led the housing market in both revenue and sales. Some operators may have held the top positions for a long time, but changing market conditions and shifting focuses have also impacted their total revenue.

In terms of net profit among the top 5, only Supalai reported a positive profit compared to its net profit in 2023, while other operators experienced minor or insignificant declines in their profits. Notably, Sansiri and AP (Thailand) saw declines of 13.3% and 17.1%, respectively, although their profits still exceeded 5 billion baht. The profit decline from last year may be compensated in 2025, even though the real estate market conditions this year have yet to recover and will require close monitoring.

Nevertheless, in 2025, major operators plan to launch more new projects than in 2024, with competition primarily among three key players: AP (Thailand), which announced an investment plan worth up to 65 billion baht across 42 projects, while Sansiri plans to launch only 29 new projects but with a total project value of up to 52 billion baht, focusing more on high-end and luxury products, resulting in a higher average value per project than other operators. Supalai is set to launch 36 new projects with a total value of approximately 46 billion baht.

Despite ongoing pressures in the housing market this year, even with the policy interest rate reduced to 2%, there has been no movement on assistance measures or stimulus for the real estate business from the government. Furthermore, all operators are pressing the Bank of Thailand to relax credit assessment criteria and temporarily ease LTV regulations to bring some purchasing power back into the market. However, it seems there has been no response from government agencies. If this continues, it is believed that 2025 will still be another challenging year for the housing market, following the difficulties of the previous year.