Home Loan Growth in the Banking Sector in 2024 Hits Lowest in 23 Years

- Home loans in Thailand's financial institutions continue to slow down, reflecting the overall weakness in the housing market. Specifically, within the banking sector, home loans grew only 0.8% YoY in Q2 2024, suggesting that the overall growth for 2024 may not exceed 1.2%, marking the lowest growth rate in 23 years.

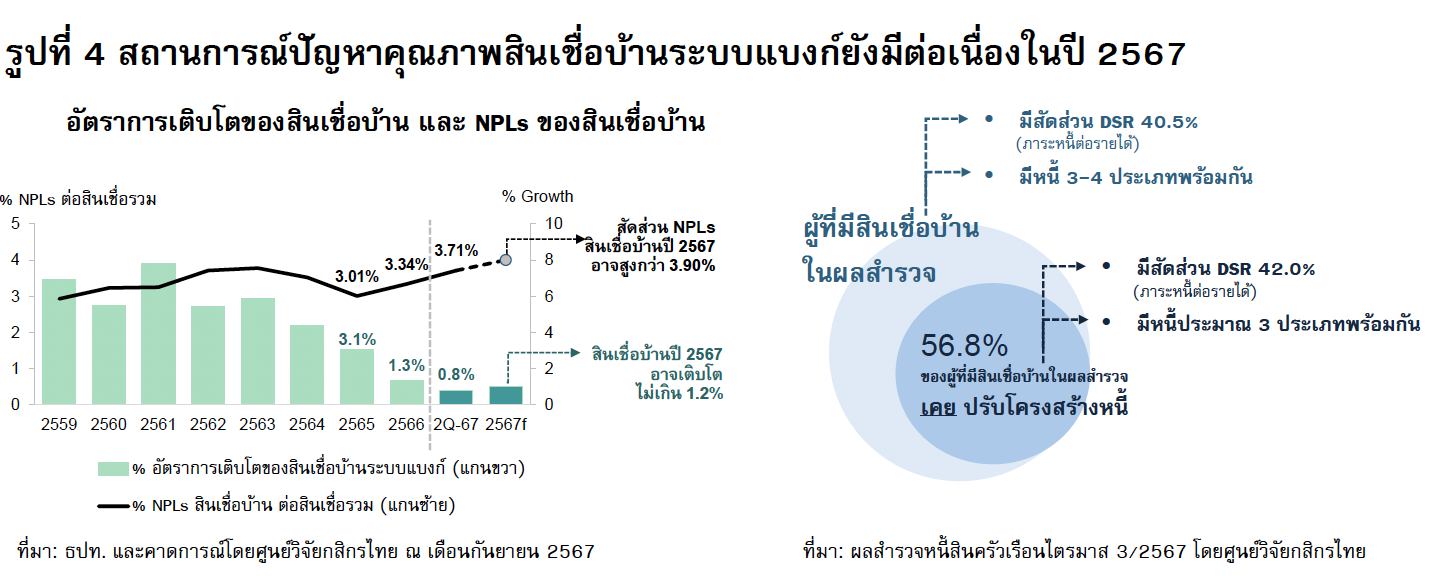

- The ongoing economic situation, which has not fully recovered, impacts household income and may cause the ratio of NPLs in home loans within the banking sector in 2024 to rise above 3.90% of total loans, up from 3.71% in Q2 2024.

- In addition to debt quality issues, in the remaining months of 2024, we may see new loans focusing more on the middle-to-upper income group and the refinancing market. We also need to monitor additional measures from the authorities regarding sustainable debt management, which may influence the future trend of home loans.

Home loans in Thailand's financial institutions continue to slow down, reflecting the overall weakness in the housing market.

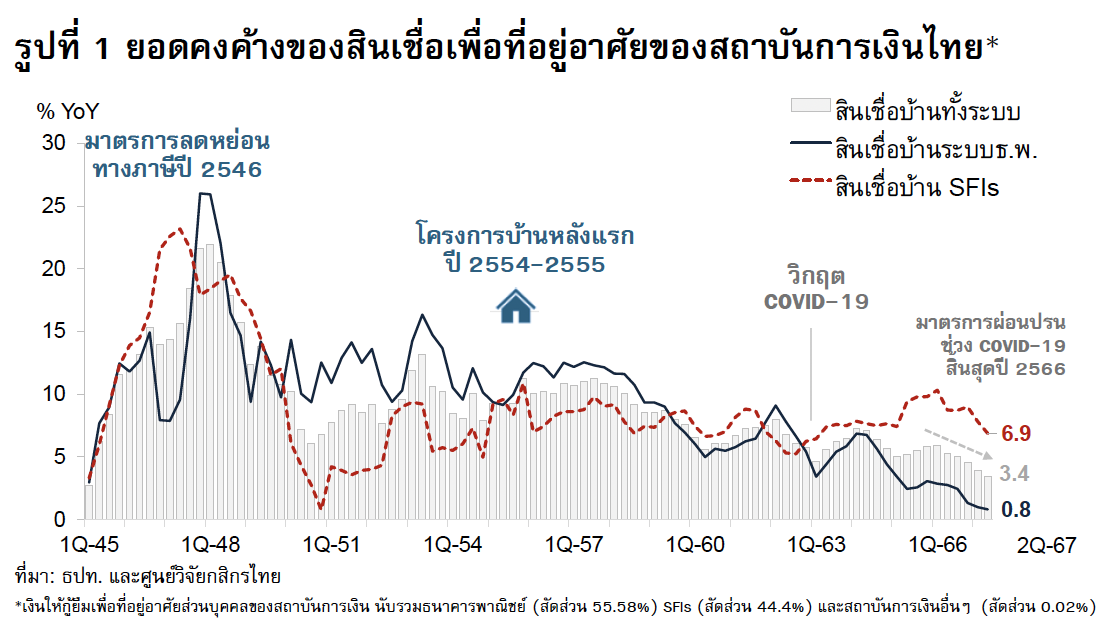

The outstanding balance of home loans in Q2 2024 from Thailand's financial institutions led by commercial bank home loans and specialized financial institutions that accept deposits grew 3.4% from the same period last year (YoY), marking the lowest growth rate since Q2 2002, down from 3.9% YoY in the first quarter of 2024 (Figure 1), and indicating a continuous slowdown over the past six quarters since the easing measures during the COVID-19 pandemic gradually ended.

The slowdown in the outstanding balance of home loans is primarily due to commercial banks (commercial bank home loans grew 0.8% YoY in Q2 2024, down from 1.0% YoY in Q1 2024). Commercial bank home loans, which hold about 55-56% of the total home loan market, have been continuously slowing down over the past year and a half amid declining purchasing power and household income, contrasting with the high debt burden of households, leading to a significant contraction in new loans from commercial banks in both the single-family home and condominium segments.

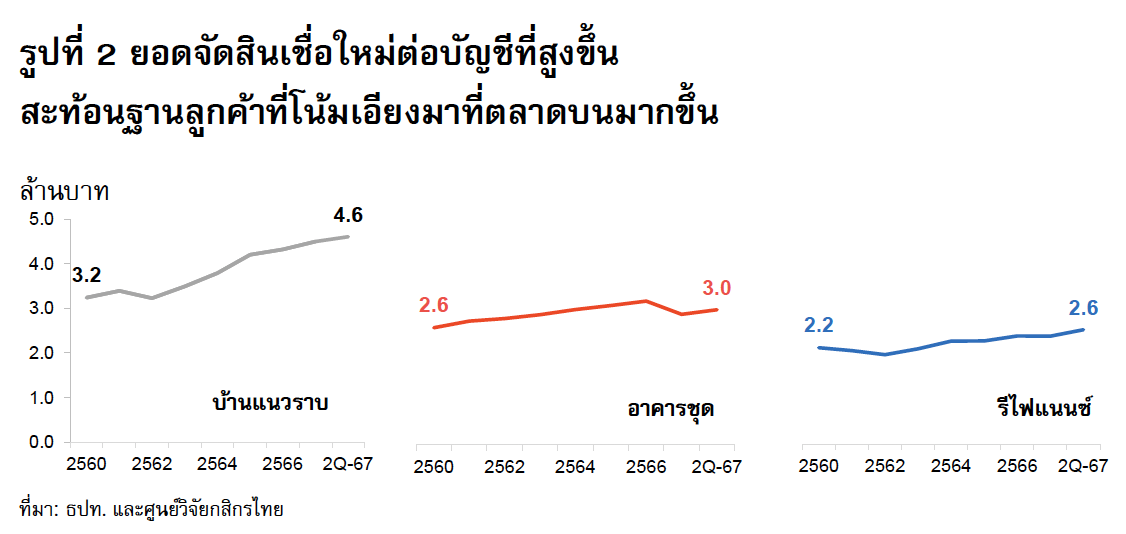

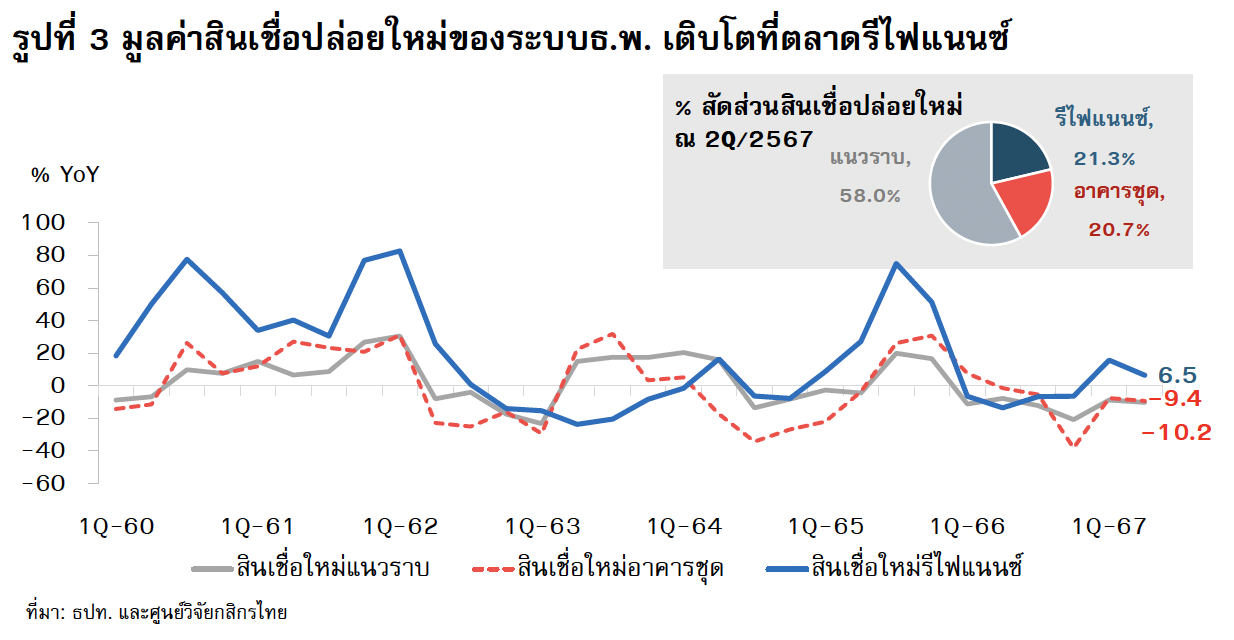

It is noteworthy that the value of home loans per account has been increasing, reflecting the rising income levels of borrowers. This group of borrowers is more resilient to risks and the impacts of environmental factors on income and living costs (Figure 2). While new home loans have contracted, new home loans for refinancing have seen positive growth, increasing their market share of total new home loans to 21.3% at the end of Q2 2024, compared to 13.6% at the end of 2020 (Figure 3).

The trend of commercial bank home loans is expected to close 2024 with the lowest growth rate in 23 years.

Looking ahead to the second half of 2024, Kasikorn Research Center estimates that the outstanding balance of home loans issued by commercial banks will grow no more than 1.2% YoY, which is the lowest annual growth rate for banking sector home loans in 23 years. This is due to issues related to income and high debt burdens affecting households' ability to take on large debts, particularly in new markets such as younger generations starting with small debts and car loans, which reduces opportunities for home loans.

The direction of the home loan market remains trapped in debt issues that push up NPLs, with key points to monitor being:

- Debt quality may worsen, as the Kasikorn Research Center predicts that the ratio of NPLs in home loans from Thailand's commercial banking sector may rise above 3.90% of total loans, compared to 3.71% at the end of Q2 2024, reflecting signs of deteriorating debt quality (Figure 4). This includes both Stage 2 debts and NPLs in homes priced below 10 million baht, which have started to increase since the last quarter of 2023, as well as Stage 2 debts in the 10-50 million baht home price range that have also risen. This situation may reflect repayment issues that are likely to spread to borrowers with moderate incomes and SME borrowers taking on relatively high-priced homes.

This trend aligns with a survey of household debt conducted in Q3 2024 with 963 samples by the Kasikorn Research Center, which found that 56.8% of respondents with home loans had previously undergone debt restructuring after being affected by high living costs and uncertain income situations (especially among contract workers). On average, respondents with home loans who had undergone debt restructuring had about three types of debt simultaneously, resulting in a DSR burden exceeding 42.0% of their income (Figure 4), while also facing high expenses and having low or no savings. Therefore, they are more sensitive to various risk factors than other debtor groups.

Furthermore, the Bank of Thailand's requirement for creditors to propose a debt restructuring plan once before and after becoming NPLs may slow down the rapid decline in debt quality somewhat, but as long as the surrounding situation affecting income and household expenses does not change significantly, the trend of deteriorating quality for home loans is likely to continue. This means we will have to wait for new government measures to address home debt issues to alleviate these problems and improve the management of bad debt quality in the home loan sector, as the current pace of asset liquidation from asset management companies has also slowed down, affecting the prices at which debts are purchased from financial institutions.

- New loans continue to focus on the middle-to-upper market and the refinancing market. If we assess borrowing capacity against the average prices of single-family homes and condominiums, it is found that borrowers need an average monthly income for new loans of about 50,000 baht for a condominium assumed to be priced around 3 million baht and 76,000 baht for a new loan for a single-family home assumed to be priced around 4.6 million baht (including joint borrowing). This preliminary calculation does not include cases where borrowers have other debt obligations, meaning that the average monthly income would need to be even higher. Meanwhile, the trend of economic conditions and household income remains highly uncertain, leading financial institutions to likely continue to focus on customers with relatively high incomes.

- In addition to the refinancing market, which remains an opportunity for financial institutions, it is expected that in the second half of the year, we will see financial institutions collaborating with major real estate development companies to launch marketing campaigns by offering special interest rates to customers and various marketing discounts, such as price reductions and waiving transfer fees to stimulate purchasing decisions before the end of 2024, especially targeting middle-to-upper income customers.

- Sustainable debt management measures may impact the ability to take on large debts. For example, the Responsible Lending and DSR criteria, which were originally planned to be gradually applied to consumer loans such as credit cards and personal loans in 2025, mean that generally, for customers with incomes below 30,000 baht per month, if they have small debt obligations nearing the limit set at no more than 60% of income (for those with incomes below 30,000 baht per month, the DSR for new debts must not exceed 60%), this will limit their ability to take on new debts such as home or car loans. Meanwhile, for customers with incomes above 30,000 baht per month, their debt burden after including new debts must not exceed 70% of income (for those with incomes above 30,000 baht per month, the DSR for new debts must not exceed 70%). This measure will need to be monitored for final details and the actual implementation timeline from the Bank of Thailand.

-

[1] Assuming a repayment period of 30 years at an interest rate of approximately 6%